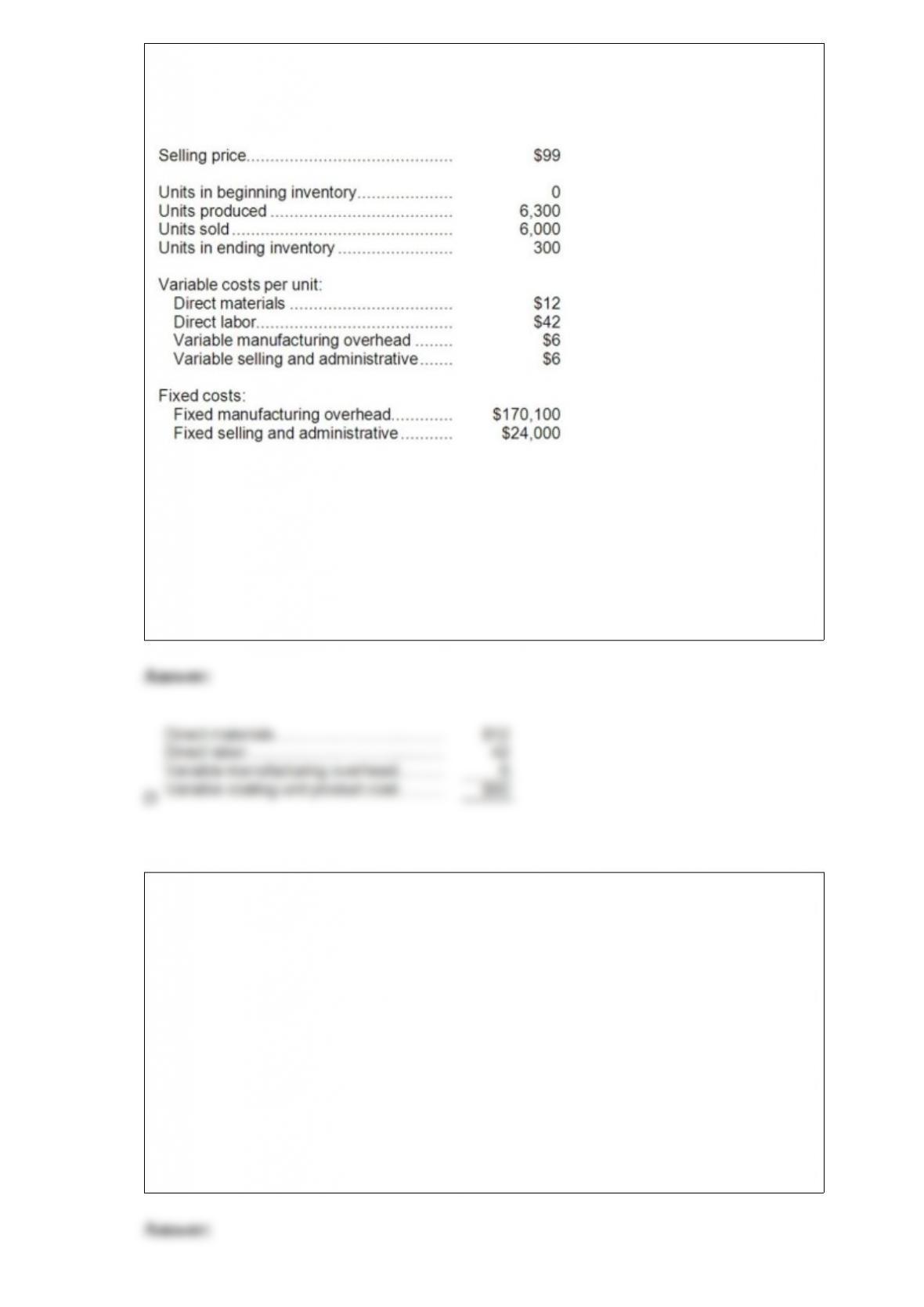

1) Aaker Corporation, which has only one product, has provided the following data

concerning its most recent month of operations:

What is the unit product cost for the month under variable costing?

A.$66 per unit

B.$93

C.$87

D.$60

2) Larance Detailing’s cost formula for its materials and supplies is $2,230 per month

plus $1 per vehicle. For the month of November, the company planned for activity of 75

vehicles, but the actual level of activity was 25 vehicles. The actual materials and

supplies for the month was $2,160.

The activity variance for materials and supplies in November would be closest to:

A.$145 U

B.$145 F

C.$50 U

D.$50 F

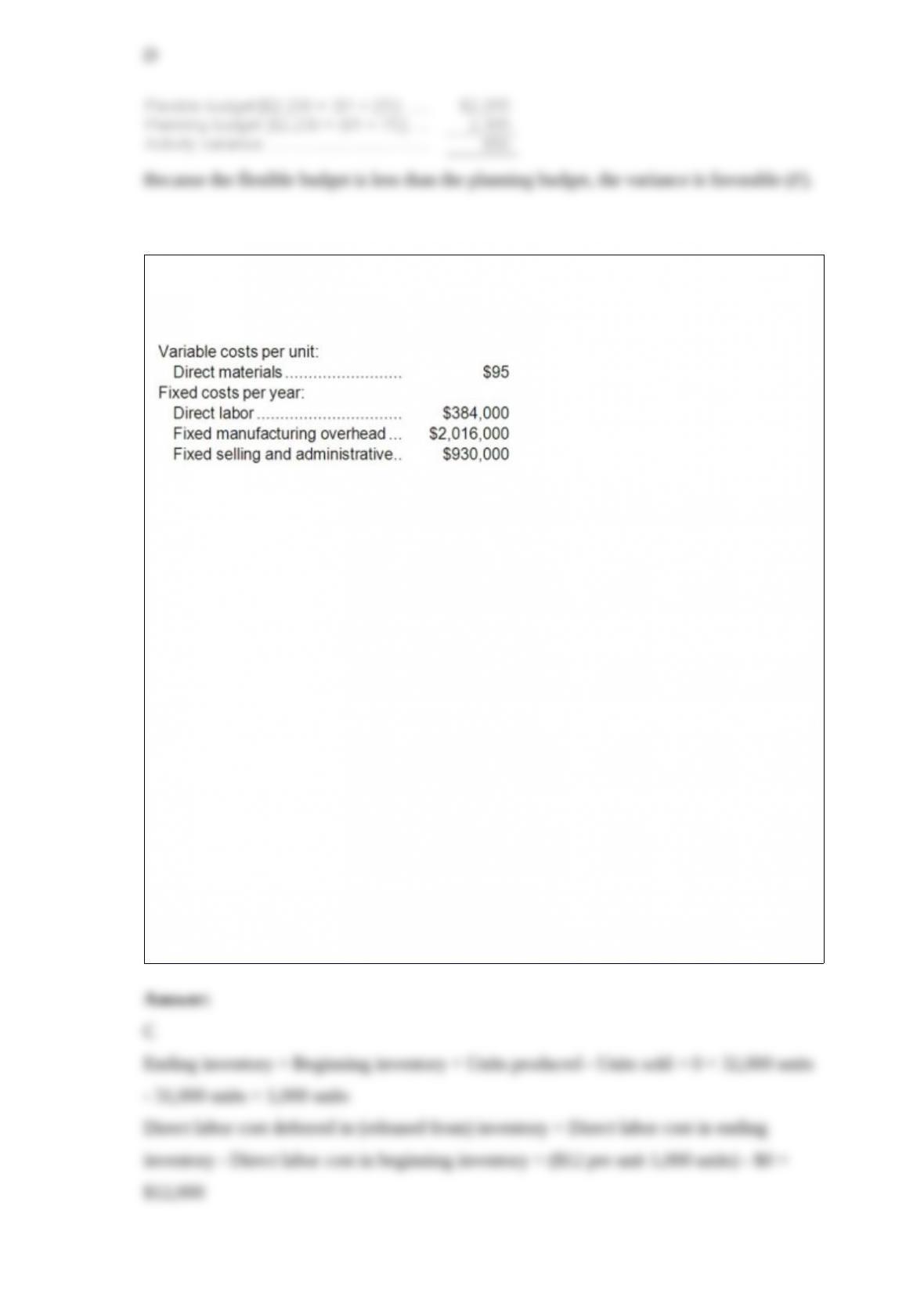

3) Quiller Corporation manufactures and sells one product. The following information

pertains to the company’s first year of operations:

The company does not have any variable manufacturing overhead costs or variable

selling and administrative costs. During its first year of operations, the company

produced 32,000 units and sold 31,000 units. The company’s only product is sold for

$233 per unit.

The company is considering using either super-variable costing or a variable costing

system that assigns $12 of direct labor cost to each unit that is produced. Which of the

following statements is true regarding the net operating income in the first year?

A.Super-variable costing net operating income exceeds variable costing net operating

income by $63,000.

B.Super-variable costing net operating income exceeds variable costing net operating

income by $12,000.

C.Variable costing net operating income exceeds super-variable costing net operating

income by $12,000.

D.Variable costing net operating income exceeds super-variable costing net operating

income by $63,000.

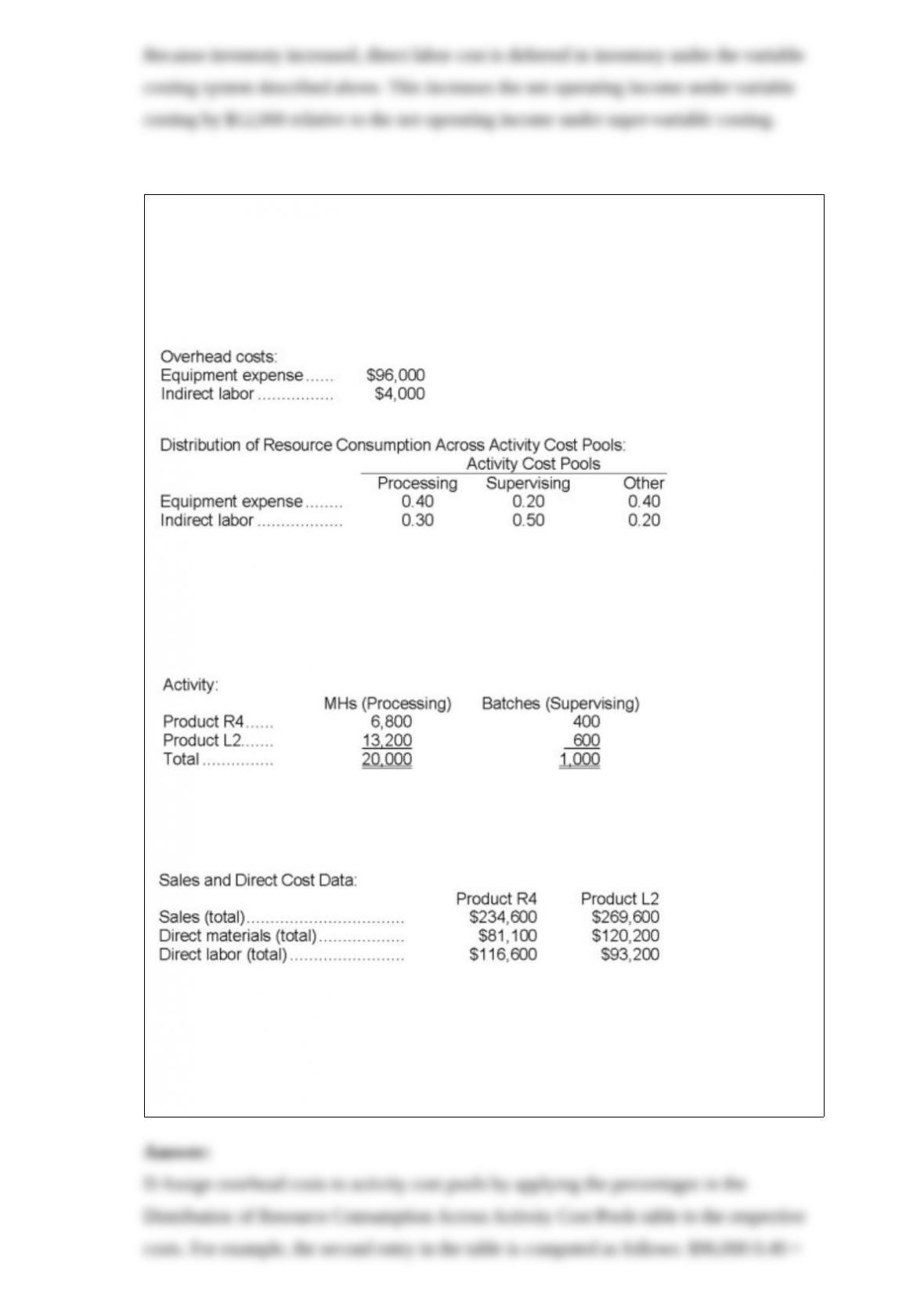

4) Lake Corporation has an activity-based costing system with three activity cost

pools-Processing, Supervising, and Other. In the first stage allocations, costs in the two

overhead accounts, equipment expense and indirect labor, are allocated to the three

activity cost pools based on resource consumption. Data used in the first stage

allocations follow:

Processing costs are assigned to products using machine-hours (MHs) and Supervising

costs are assigned to products using the number of batches. The costs in the Other

activity cost pool are not assigned to products. Activity data for the company’s two

products follow:

Finally, the costs of Processing and Supervising are combined with the following sales

and direct cost data to determine product margins.

How much overhead cost is allocated to the Supervising activity cost pool under

activity-based costing?

A.$19,200

B.$2,000

C.$39,200

D.$21,200

5) The net cash provided by (used in) investing activities for the year was:

A.$74

B.$(74)

C.$(72)

D.$72

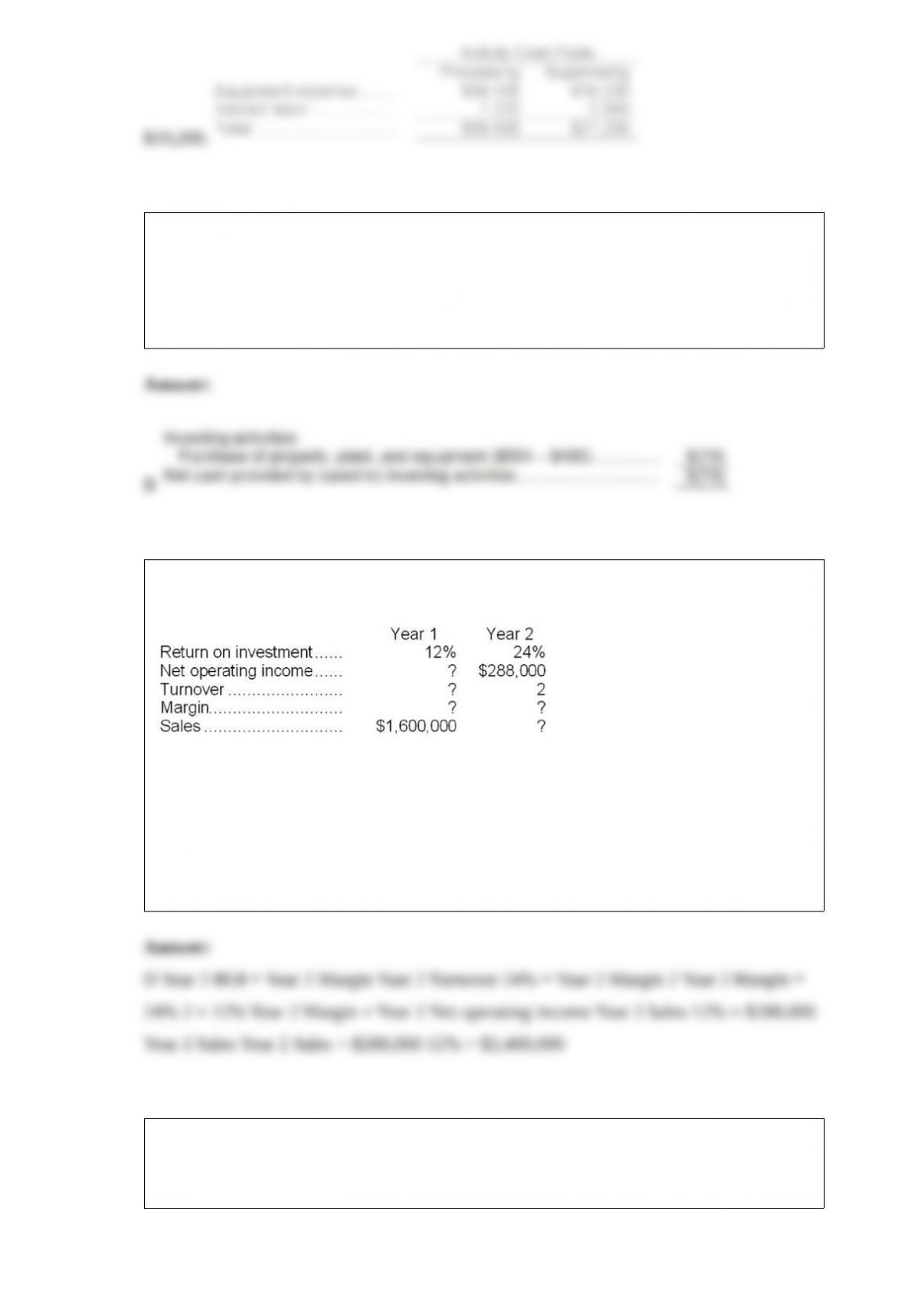

6) The Portland Division’s operating data for the past two years is as follows:

The Portland Division’s margin in Year 2 was 150% of the margin for Year 1.

The sales for Year 2 were:

A.$750,000

B.$2,000,000

C.$3,846,154

D.$2,400,000

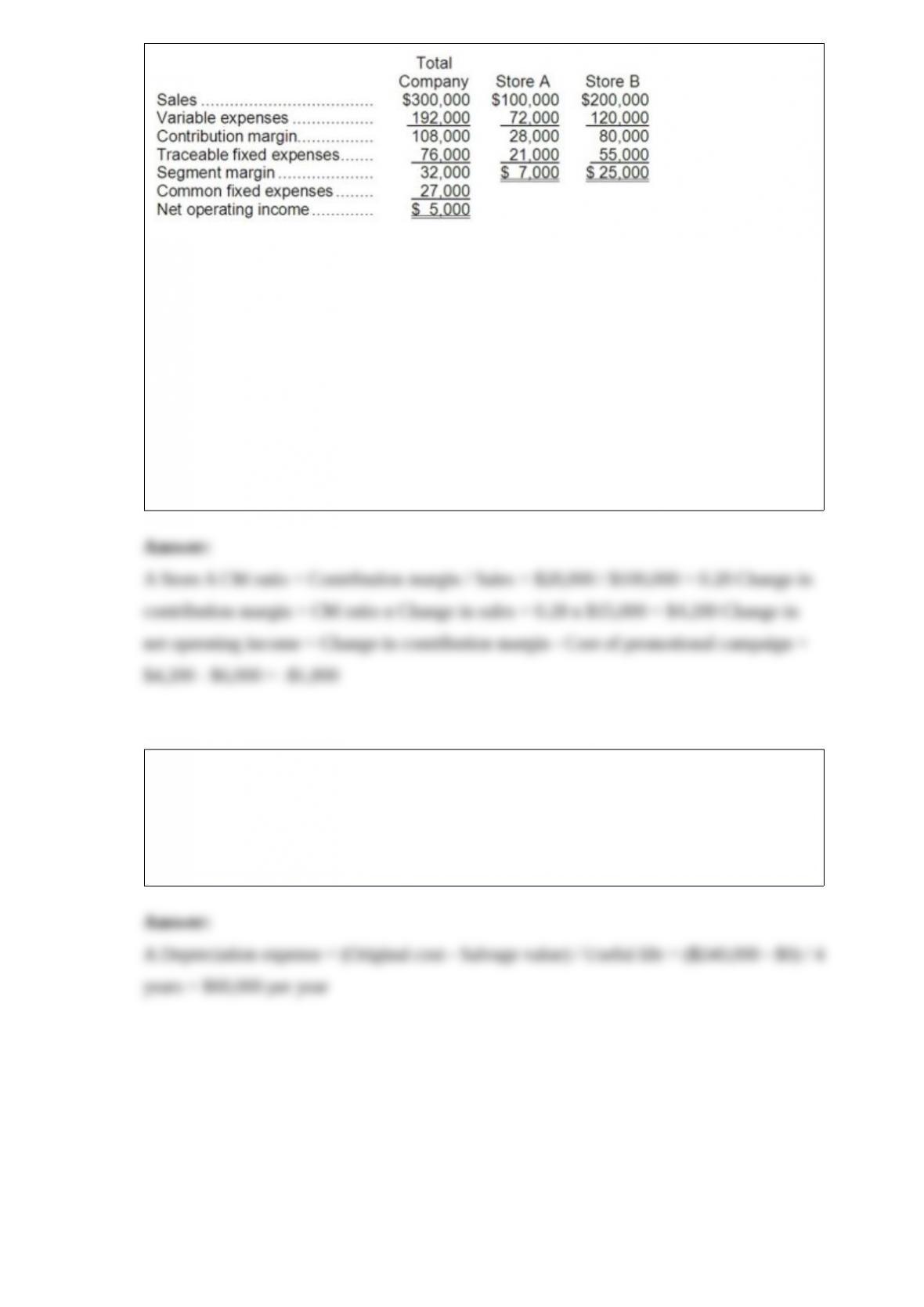

7) O’Neill, Incorporated’s segmented income statement for the most recent month is

given below.

For each of the following questions, refer back to the above original data.

The marketing department believes that a promotional campaign at Store A costing

$6,000 will increase sales by $15,000. If its plan is adopted, overall company net

operating income should:

A.decrease by $1,800

B.decrease by $10,200

C.increase by $10,200

D.increase by $1,800

8) The net present value of the entire project is closest to:

A.$141,583

B.$223,630

C.$381,583

D.$238,000

9) If the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

The management of Cordona Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller

has provided an example to illustrate how this new system would work. In this

example, the allocation base is machine-hours and the estimated amount of the

allocation base for the upcoming year is 27,000 machine-hours. In addition, capacity is

33,000 machine-hours and the actual level of activity for the year is 27,900

machine-hours. All of the manufacturing overhead is fixed and is $231,660 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year. A number of jobs were

worked on during the year, one of which was Job I86N. This job required 370

machine-hours.

A.$35,802 Underapplied

B.$7,722 Underapplied

C.$35,802 Overapplied

D.$7,722 Overapplied

Predetermined overhead rate = Estimated total manufacturing overhead at capacity /

Estimated total amount of the allocation base at capacity = $231,660 / 33,000

machine-hours = $7.02 per machine-hour

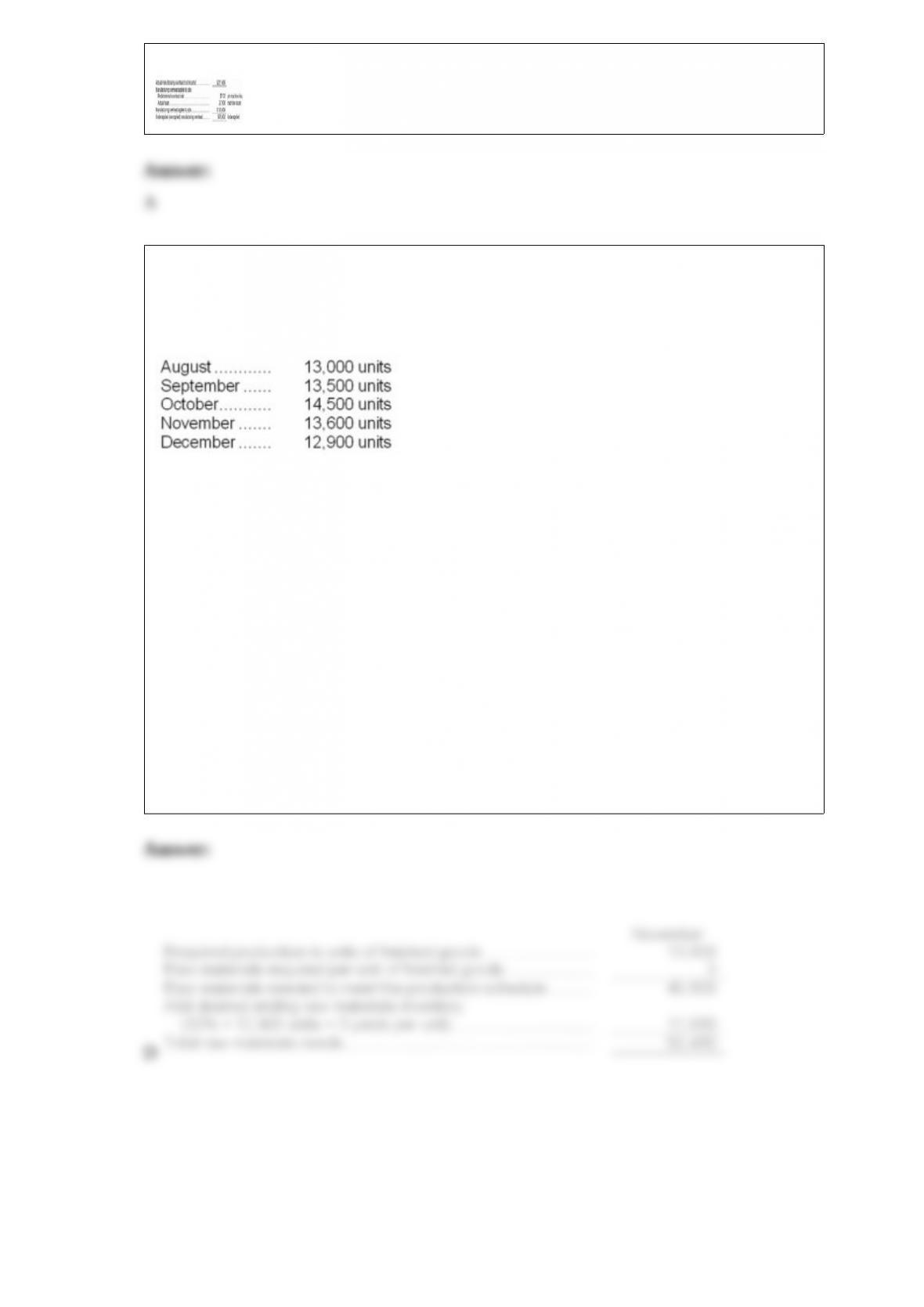

10) Cowles Corporation, Inc. makes and sells a single product, Product R. Three yards

of Material K are needed to make one unit of Product R. Budgeted production of

Product R for the next five months is as follows:

The company wants to maintain monthly ending inventories of Material K equal to 30%

of the following month’s production needs. On July 31, this requirement was not met

because only 3,500 yards of Material K were on hand. The cost of Material K is $0.80

per yard. The company wants to prepare a Direct Materials Purchase Budget for the rest

of the year.

The total needs (i.e., production requirements plus desired ending inventory) of

Material K for November are:

A.40,800 yards

B.44,940 yards

C.37,380 yards

D.52,410 yards