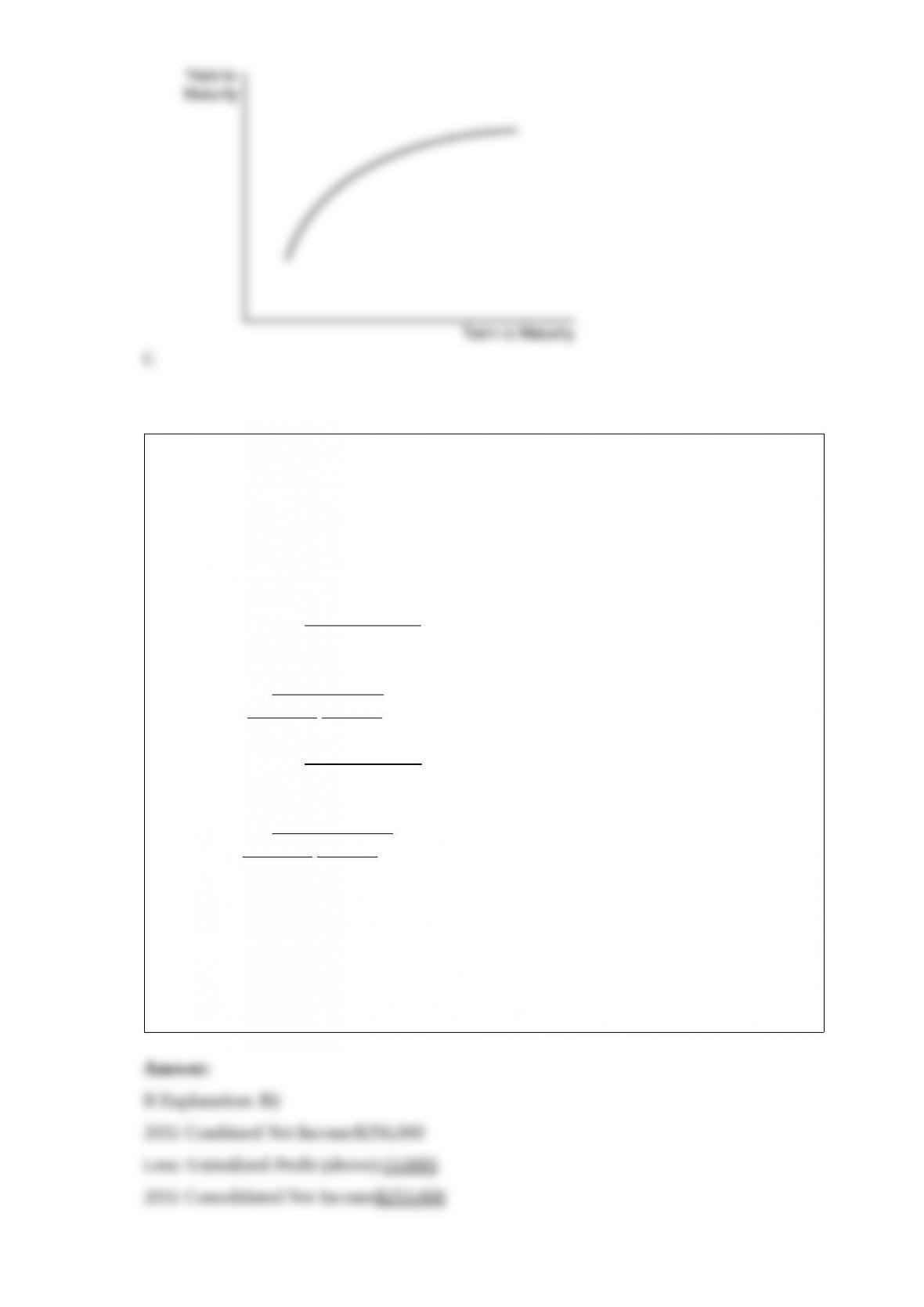

1) The steeply upward sloping yield curve in the figure above indicates that ________

interest rates are expected to ________ in the future

A) short-term; rise

B) short-term; fall moderately

C) short-term; remain unchanged

D) long-term; fall moderately

2) If the price paid by a parent company to acquire the debt of a subsidiary is greater

than the book value of the liability, a ________ occurs.

A) realized loss on the retirement of debt from the viewpoint of the subsidiary

B) realized gain on the retirement of debt from the viewpoint of the subsidiary

C) constructive loss on the retirement of debt from the viewpoint of the consolidated

entity

D) constructive gain on the retirement of debt from the viewpoint of the consolidated

entity

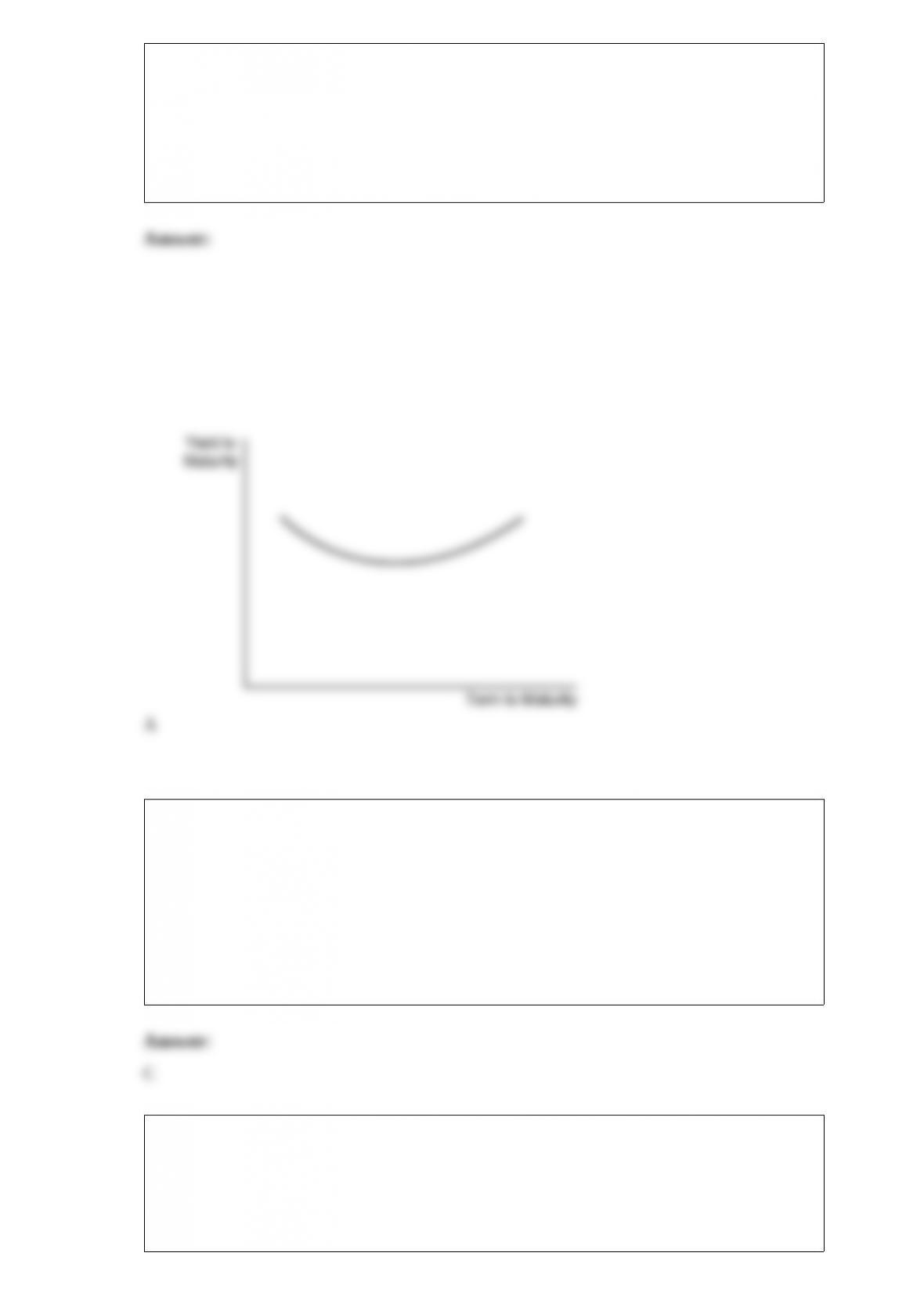

3) If the yield curve is flat for short maturities and then slopes downward for longer

maturities, the liquidity premium theory (assuming a mild preference for shorter-term

bonds) indicates that the market is predicting

A) a rise in short-term interest rates in the near future and a decline further out in the

future

B) constant short-term interest rates in the near future and a decline further out in the

future

C) a decline in short-term interest rates in the near future and a rise further out in the

future

D) a decline in short-term interest rates in the near future and an even steeper decline

further out in the future

4) The key focus of government fund accounting concerns

A) capital expenditures

B) intergovernmental transfers from the general fund

C) income measurement

D) the current ability to provide and fund services and goods

5) A particularly attractive feature of the ________ is that it tells you what the market is

predicting about future short-term interest rates by just looking at the slope of the yield

curve

A) segmented markets theory

B) expectations theory

C) liquidity premium theory

D) separable markets theory

6) Paggle Corporation owns 80% of Spillway Inc.’s common stock that was purchased

at its underlying book value. At the time of purchase, the book value and fair value of

Spillway’s net assets were equal. The two companies report the following information

for 2011 and 2012 .

During 2011, one company sold inventory to the other company for $50,000 which cost

the transferor $40,000. As of the end of 2011, 30% of the inventory was unsold. In

2012, the remaining inventory was resold outside the consolidated entity.

2011 Selected Data:PaggleSpillway

Sales Revenue $600,000 $320,000

Cost of Goods Sold320,000155,000

Other Expenses100,00089,000

Net Income $180,000 $76,000

Dividends Paid19,0000

2012 Selected Data:PaggleSpillway

Sales Revenue$580,000 $445,000

Cost of Goods Sold300,000180,000

Other Expenses130,000171,000

Net Income$150,000 $94,000

Dividends Paid16,0005,000

For 2011, consolidated net income will be what amount if the intercompany sale was

downstream?

A) $180,000

B) $253,000

C) $256,000

D) $259,000

7) On June 30, 2011, the Able, Baker, and Charlie partnership had the following fiscal

year-end balance sheet:

Cash$8,000Accounts payable$14,000

Accounts receivable12,000Loan from Charlie10,000

Inventory28,000Able, capital (20%)28,000

Plant assets-net24,000Baker, capital (20%)20,000

Loan to Able12,000Charlie,capital (60%)12,000

Total assets$84,000Total liab./equity$84,000

The percentages shown are the residual profit and loss sharing ratios. The partners

dissolved the partnership on July 1, 2011, and began the liquidation process. During

July the following events occurred:

*Receivables of $6,000 were collected.

*All inventory was sold for $8,000.

*All available cash was distributed on July 31, except for

$4,000 that was set aside for contingent expenses.

The cash available for distribution to the partners on July 31, 2011 is

A) $ 4,000

B) $ 8,000

C) $14,000

D) $22,000

8) Pelga Company routinely receives goods from its 80%-owned subsidiary, Swede

Corporation. In 2011, Swede sold merchandise that cost $80,000 to Pelga for $100,000.

Half of this merchandise remained in Pelga’s December 31, 2011 inventory. This

inventory was sold in 2012 . During 2012, Swede sold merchandise that cost $160,000

to Pelga for $200,000. $62,500 of the 2012 merchandise inventory remained in Pelga’s

December 31, 2012 inventory. Selected income statement information for the two

affiliates for the year 2012 was as follows:

PelgaSwede

Sales Revenue$500,000$400,000

Cost of Goods Sold400,000320,000

Gross profit$100,000$80,000

What amount of unrealized profit did Pelga Company have at the end of 2012?

A) $10,000

B) $12,500

C) $50,000

D) $62,500

9) Under the Revised Uniform Principal and Income Act, gains or losses incurred on

investments that occur after the death of the decedent

A) are considered to be income of the estate

B) are included in the inventory fair value at the time of death

C) are taxed separately from other estate income

D) are adjustments to the principal of the estate

10) A decrease in the liquidity of corporate bonds will ________ the price of corporate

bonds and ________ the yield of Treasury bonds, everything else held constant

A) increase; increase

B) decrease; decrease

C) increase; decrease

D) decrease; increase

11) Pinkerton Inc. owns 10% of Sable Company. In the most recent year, Sable had net

earnings of $40,000 and paid dividends of $6,000. Pinkerton’s accountant mistakenly

assumed Pinkerton had considerable influence over Sable and used the equity method

instead of the cost method. What is the impact on the investment account and net

earnings, respectively?

A) By using the equity method, the accountant has understated the investment account

and overstated the net earnings

B) By using the equity method, the accountant has overstated the investment account

and understated the net earnings

C) By using the equity method, the accountant has understated the investment account

and understated the net earnings

D) By using the equity method, the accountant has overstated the investment account

and overstated the net earnings

12) Paiva Corporation owns 80% of Ackroyd Corporation’s outstanding common stock

and Ackroyd owns 80% of the outstanding common stock of Bailey Corporation. Bailey

Corporation owns 10% of the outstanding common stock of Ackroyd Corporation. The

cost of the investments was equal to book value and there were not fair value/book

value differences for the investments. The separate net incomes for the three affiliated

companies for the year ended December 31, 2011 (excluding investment income) are as

follows: Paiva Corporation, $100,000, Ackroyd Corporation, $50,000, and Bailey

Corporation, $30,000. Use the conventional approach.

Symbols used:

P = Income of Paiva on a consolidated basis

A = Income of Ackroyd on a consolidated basis

B = Income of Bailey on a consolidated basis

Bailey’s noncontrolling interest share for 2011 is

A) $7,609

B) $8,044

C) $15,652

D) $23,696

13) What funds are reported in Government-wide financial statements?

A) Governmental only

B) Proprietary only

C) Governmental and proprietary

D) Governmental, proprietary and fiduciary

14) Similar operating segments may be combined if the segments have similar

economic characteristics. Which one of the following is a similar economic

characteristic under GAAP?

A) The segments’ management teams

B) The tax reporting law sections

C) The distribution method for products or services

D) The expected rates of return and risk for the segments’ productive assets

15) When yield curves are downward sloping,

A) long-term interest rates are above short-term interest rates

B) short-term interest rates are above long-term interest rates

C) short-term interest rates are about the same as long-term interest rates

D) medium-term interest rates are above both short-term and long-term interest rates

16) From the standpoint of accounting theory, which of the following statements is the

best justification for the preparation of consolidated financial statements?

A) In substance the companies are separate, but in form the companies are one entity

B) In substance the companies are one entity, but in form they are separate

C) In substance and form the companies are one entity

D) In substance and form the companies are separate entities

17) When preparing their year-end financial statements, the Warner Company includes

a footnote regarding their hedging activities during the year. Which of the following is

not required to be disclosed?

A) How hedge effectiveness is determined and assessed

B) The specific types of risks being hedged, and how they are being hedged

C) Alternative hedging options declined

D) The net gain or loss reported for the period for fair value hedges and where in the

financial statements it is reported

18) Pace Corporation owns 70% of Abaza Corporation and 60% of Babon Corporation.

Abaza Corporation owns 20% of Babon Corporation. Pace’s investment in Abaza was

consummated in one transaction at a purchase price $20,000 in excess of the book

value. Pace’s purchase of Babon was made in one transaction at a price $30,000 above

book value. Abaza’s investment in Babon was completed in one transaction at a

purchase price $10,000 in excess of the book value. The purchase price differential for

all three investments was attributable to goodwill. (There were no fair value/book value

differences in assets and liabilities for each investment.) Pace’s separate net income for

the current year is $100,000. Abaza’s separate net income is $190,000, which includes a

$10,000 unrealized loss on the sale of land to Pace. Babon’s separate net income is

$150,000. Separate net incomes exclude investment income.

The amount of noncontrolling interest share for the current year is

A) $69,000

B) $85,000

C) $95,000

D) $99,000

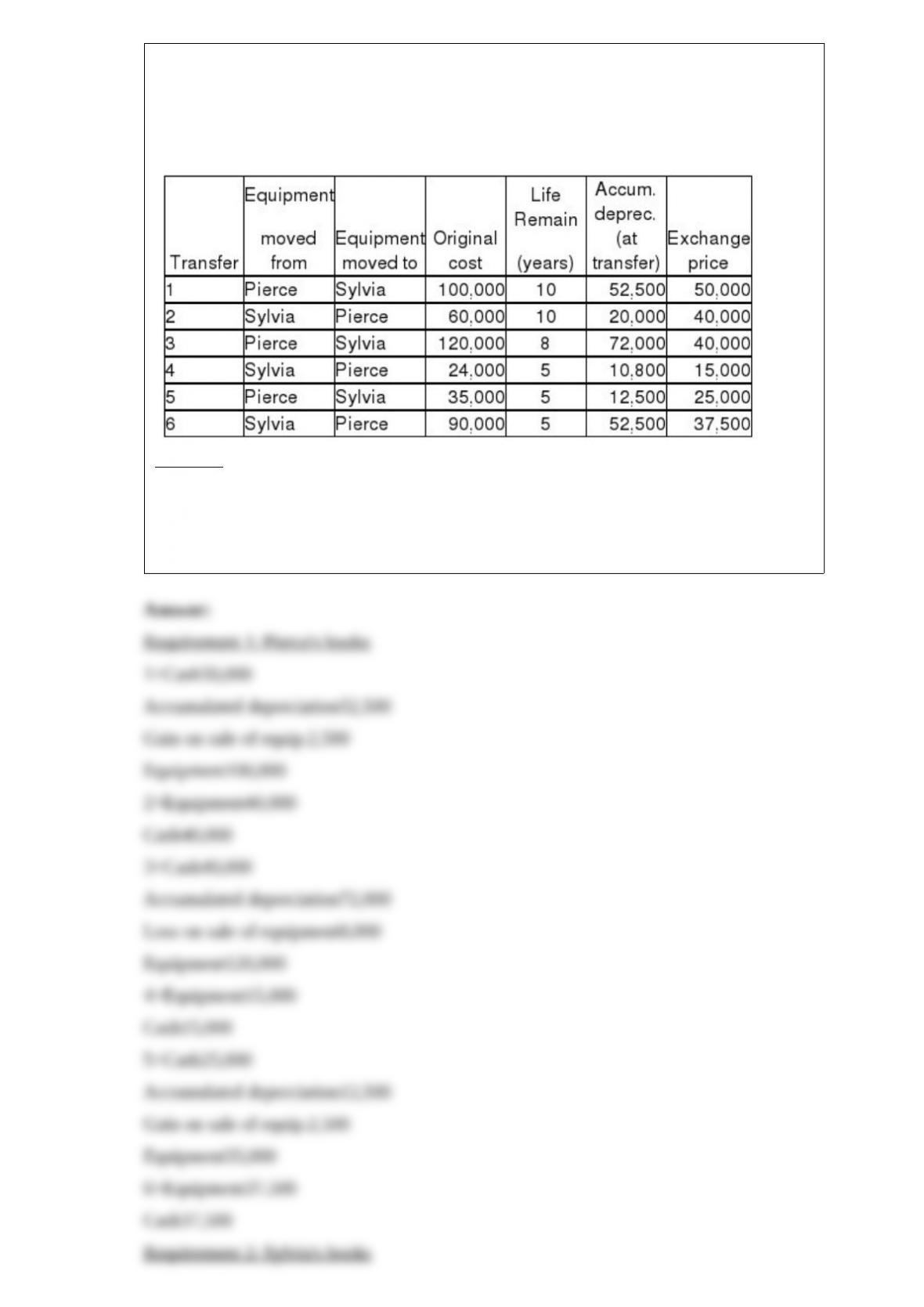

19) Pierce Manufacturing owns all of the outstanding voting common stock of Sylvia

Company, as acquired several years ago when the book values and fair values of

Sylvia’s net assets were equal.

In 2010, Pierce set out to re-structure the company, and in doing so, re-aligned the

manufacturing processes to streamline the use of automated equipment. As a result,

they set out to move certain equipment around between the facilities owned by both

Pierce and Sylvia, and ultimately agreed on the following transfers and exchange

prices. It was agreed that the exchange price would be paid in cash on January 1, 2011,

the date the equipment was transferred. Straight-line depreciation is used and the

different pieces of equipment have no salvage value.

Required:

1> Prepare the journal entry that Pierce would record for each transfer listed.

2> Prepare the journal entry that Sylvia would record for each transfer listed.

3> Prepare the consolidation worksheet entries that would be required as a result of the

above transactions for 2011 .

20) Parrot Incorporated purchased the assets and liabilities of Sparrow Company at the

close of business on December 31, 2011 . Parrot borrowed $2,000,000 to complete this

transaction, in addition to the $640,000 cash that they paid directly. The fair value and

book value of Sparrow’s recorded assets and liabilities as of the date of acquisition are

listed below. In addition, Sparrow had a patent that had a fair value of $50,000.

Book ValueFair Value

Cash$120,000$120,000

Inventories220,000250,000

Other current assets630,000600,000

Land270,000320,000

Plant assets-net 4,650,000 4,600,000

Total Assets$5,890,000

Accounts payable$1,200,000$1,200,000

Notes payable2,100,0002,100,000

Capital stock, $5 par700,000

Additional paid-in capital1,400,000

Retained Earnings 490,000

Total Liabilities & Equities$5,890,000

Required:

1>Prepare Parrot’s general journal entry for the acquisition of Sparrow, assuming that

Sparrow survives as a separate legal entity.

2>Prepare Parrot’s general journal entry for the acquisition of Sparrow, assuming that

Sparrow will dissolve as a separate legal entity.

21) Paradise Corporation owns 100% of Aldred Corporation, 90% of Balme

Corporation, 80% of Calder Corporation, 75% of Dale Corporation, 20% of East

Corporation, and 8% of Faber Corporation. Paradise, Aldred, Balme and Calder belong

to an affiliated group. All of these corporations are domestic corporations. During 2011,

Paradise Corporation reports net income of $1,500,000. This net income includes the

full amount of dividends received from Aldred and Faber, but does not include the

dividends received from Balme, Calder, Dale, and East Corporations. All investees have

paid out all of their net income in the form of dividends. Paradise’s share of the various

dividend distributions is as follows:

From Aldred:$90,000

From Balme:$92,000

From Calder:$88,000

From Dale:$66,000

From East:$50,000

From Faber:$40,000

Required:

Calculate the correct amount of taxable income for Paradise Corporation if a

consolidated tax return is filed.

22) Journalize the following municipal zoo transactions in the Lackluster County

Enterprise Fund:

1>The zoo issued $1,000,000 of 5% revenue bonds at 99 on July 1, 2011 (an interest

payment date). The bond proceeds are to be used for a new polar bear exhibit and the

issue will mature in 20 years. Interest is paid on January 1 and July 1 .

2>Depreciation for the year-ended December 31, 2011 included $175,000 for buildings

and $105,000 for outdoor exhibit areas.

3>The zoo paid $800,000 in construction costs for the new exhibit. The exhibit is still

under construction.

4>Interest on the revenue bonds was accrued at year-end, December 31, 2011 .

Straight-line amortization is used for bond discounts and premiums.

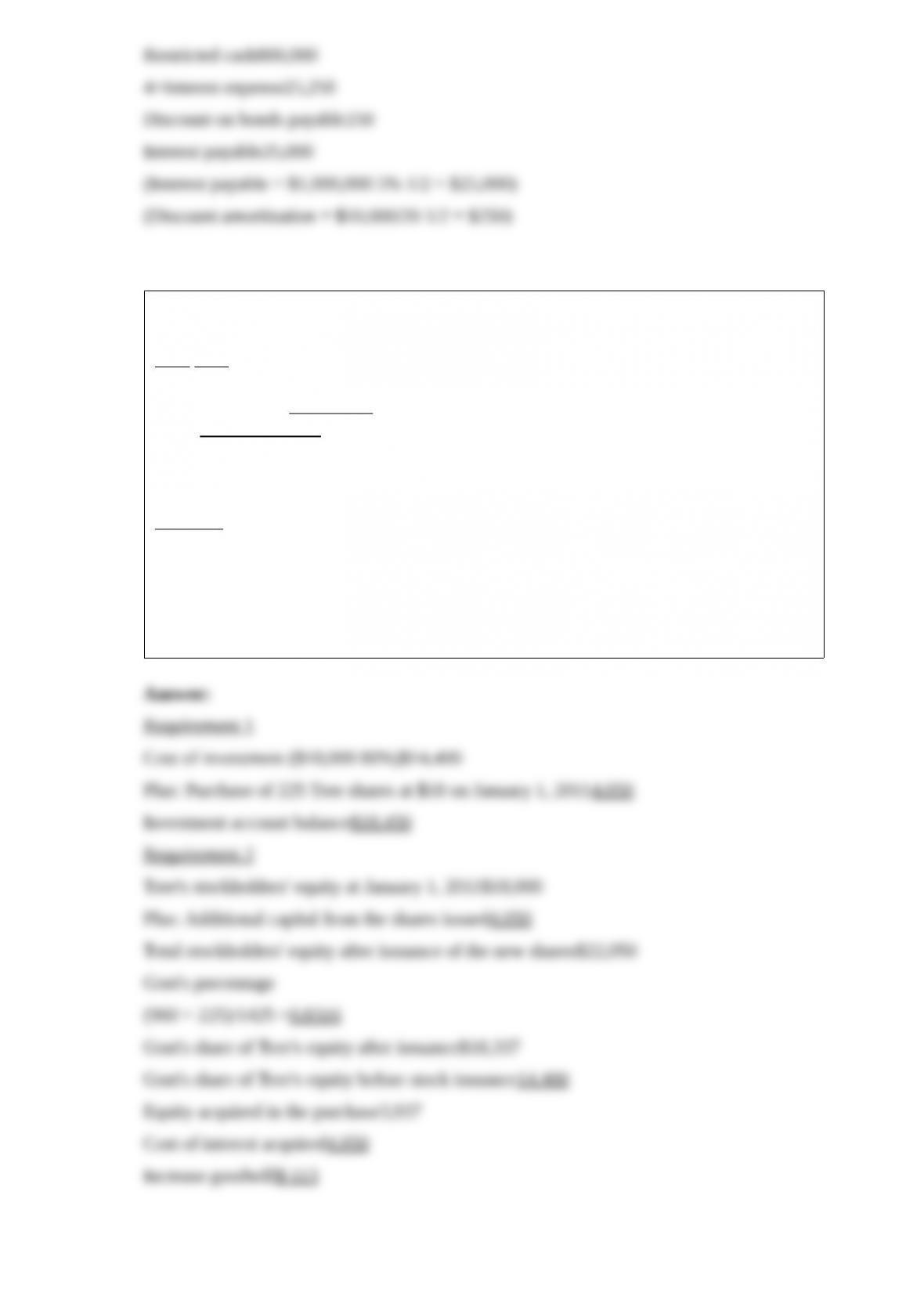

23) At December 31, 2010, the stockholders’ equity of Gost Corporation and its

80%-owned subsidiary, Tree Corporation, are as follows:

Gost Tree

Common stock, $10 par value$20,000$12,000

Retained earnings8,0006,000

Totals$28,000$18,000

Gost’s Investment in Tree is equal to 80 percent of Tree’s book value. Tree Corporation

issued 225 additional shares of common stock directly to Gost on January 1, 2011 at

$18 per share.

Required:

1> Compute the balance in Gost’s Investment in Tree account on January 1, 2011 after

the new investment is recorded.

2> Determine the increase or decrease in goodwill from Gost’s new investment in the

225 Tree shares. Use four decimal places for the ownership percentage. Assume the fair

values of Tree’s assets and liabilities are equal to book values.

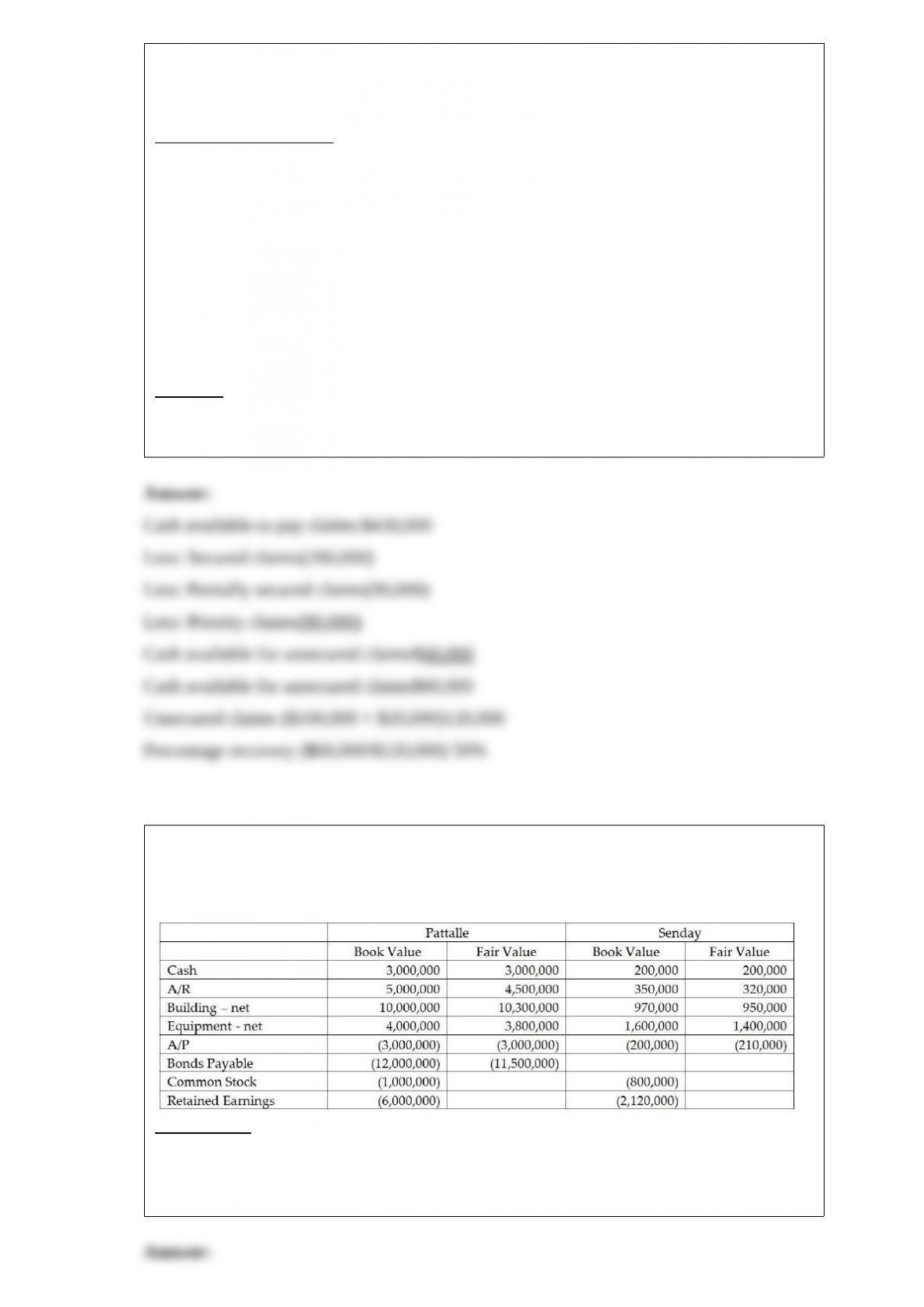

24) Aqua Corporation filed a petition under Chapter 7 of the bankruptcy act in January,

2011 . On February 28, the following information was presented regarding Aqua’s

financial status.

Book ValuesFair Values

Cash$50,000$50,000

A/R – net100,00090,000

Inventories80,00060,000

Fixed Assets – net200,000230,000

Priority Claims80,000

A/P100,000

N/P110,000

Mortgage Payable200,000

The Note Payable is secured by Accounts Receivable, and the Mortgage Payable is

secured by the Fixed Assets.

Required:

Calculate the amount expected to be available for unsecured claims and the percentage

recovery that the unsecured class should expect to receive.

25) Pattalle Co purchases Senday, Inc. on January 1 of the current year for $70,000

more than the fair value of Senday’s net assets. Push-down accounting is used. At that

date, the following values exist:

Requirement: Determine what amounts will appear in the listed accounts on Pattalle’s

general ledger, on Senday’s general ledger, and on the consolidated balance sheet

immediately following the acquisition. Make sure you post the entry to record the

investment on Pattalle’s books.

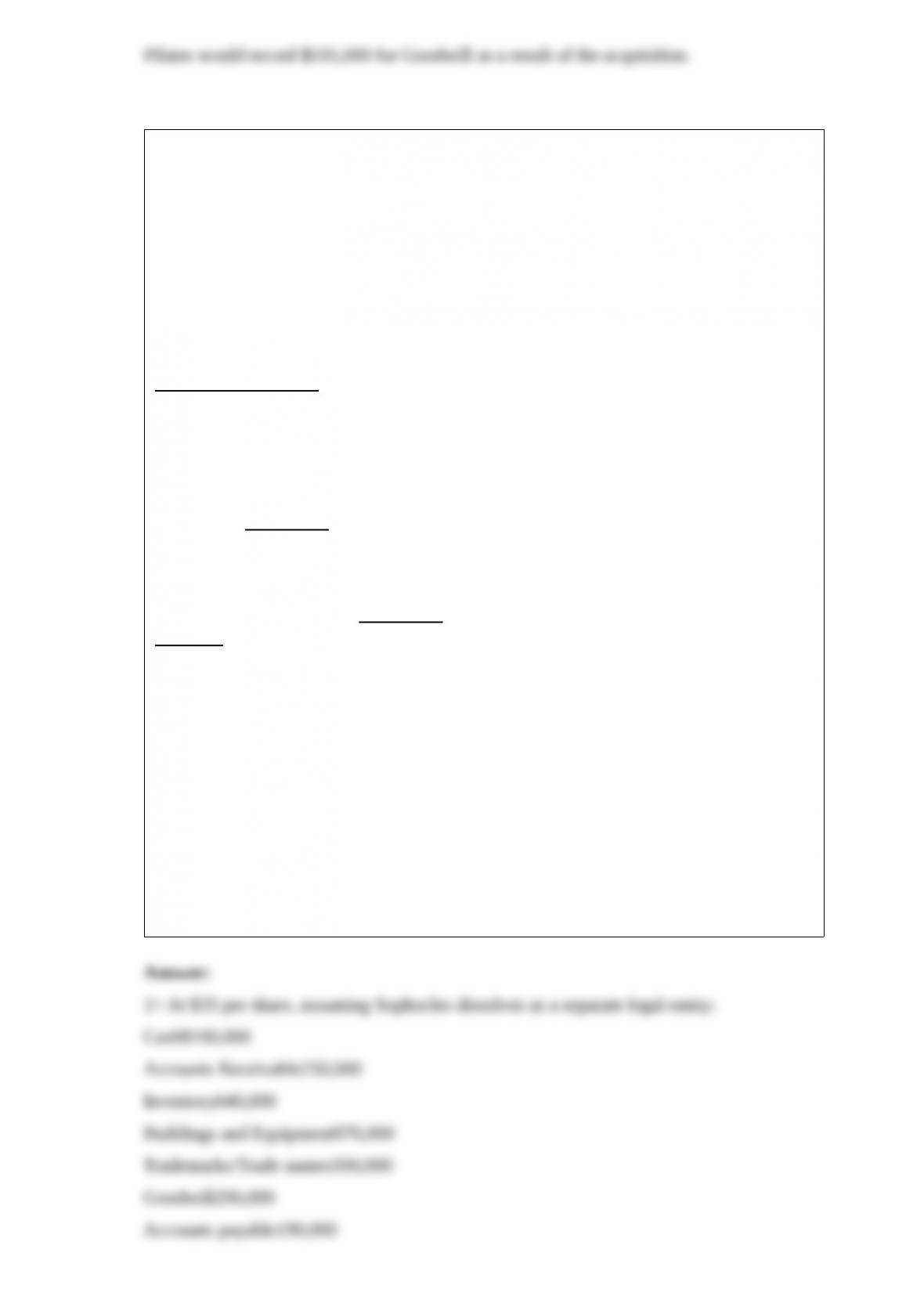

26) On January 2, 2011, Pilates Inc. paid $900,000 for all of the outstanding common

stock of Spinning Company, and dissolved Spinning Company. The carrying values for

Spinning Company’s assets and liabilities are recorded below.

Cash$200,000

Accounts Receivable220,000

Copyrights (purchased)400,000

Goodwill120,000

Liabilities(180,000)

Net assets$760,000

On January 2, 2011, Spinning anticipated collecting $185,000 of the recorded Accounts

Receivable. Pilates entered into the acquisition because Spinning had Copyrights that

Pilates wished to own, and also unrecorded patents with a fair value of $100,000.

Required:

Calculate the amount of goodwill that will be recorded on Pilate’s balance sheet as of

the date of acquisition.

27) At December 31, 2011, Pandora Incorporated issued 40,000 shares of its $20 par

common stock for all the outstanding shares of the Sophocles Company. In addition,

Pandora agreed to pay the owners of Sophocles an additional $200,000 if a specific

contract achieved the profit levels that were targeted by the owners of Sophocles in

their sale agreement. The fair value of this amount, with an agreed likelihood of

occurrence and discounted to present value, is $160,000. In addition, Pandora paid

$10,000 in stock issue costs, $40,000 in legal fees, and $48,000 to employees who were

dedicated to this acquisition for the last three months of the year. Summarized balance

sheet and fair value information for Sophocles immediately prior to the acquisition

follows.

Book ValueFair Value

Cash$100,000$100,000

Accounts Receivable280,000250,000

Inventory520,000640,000

Buildings and Equipment (net)750,000870,000

Trademarks and Tradenames0500,000

Total Assets$1,650,000

Accounts Payable$200,000$190,000

Notes Payable900,000900,000

Retained Earnings550,000

Total Liabilities and Equity$1,650,000

Required:

1>Prepare Pandora’s general journal entry for the acquisition of Sophocles assuming

that Pandora’s stock was trading at $35 at the date of acquisition and Sophocles

dissolves as a separate legal entity.

2>Prepare Pandora’s general journal entry for the acquisition of Sophocles assuming

that Pandora’s stock was trading at $35 at the date of acquisition and Sophocles

continues as a separate legal entity.

3>Prepare Pandora’s general journal entry for the acquisition of Sophocles assuming

that Pandora’s stock was trading at $25 at the date of acquisition and Sophocles

dissolves as a separate legal entity.

4>Prepare Pandora’s general journal entry for the acquisition of Sophocles assuming

that Pandora’s stock was trading at $25 at the date of acquisition and Sophocles survives

as a separate legal entity.