1) If two annuities have the same number of rents with the same dollar amount, but one

is an annuity due and one is an ordinary annuity, the present value of the annuity due

will be greater than the present value of the ordinary annuity.

2) In the retail inventory method, abnormal shortages are deducted from both the cost

and retail amounts and reported as a loss.

3) LIFO liquidation often distorts net income, but usually leads to substantial tax

savings.

4) The accounting for defined-benefit pension plans is the same under U.S. GAAP and

IFRS.

5) The International Accounting Standards Board (IASB) defines revenue to include

both revenues and gains.

6) Callable preferred stock permits the corporation at its option to redeem the

outstanding preferred shares at specified future dates and at stipulated prices.

7) Adoption of a new principle in recognition of events that have occurred for the first

time or that were previously immaterial is treated as an accounting change.

8) Jones Company has notes receivable that have a fair value of $570,000 and a

carrying amount of $750,000. Jones decides on December 31, 2014, to use the fair

value option for these recently-acquired receivables. Which of the following entries will

be made on December 31, 2014 to record the unrealized holding gain/loss?

a.Unrealized Holding Gain or LossIncome180,000

Notes Receivable180,000

b.Unrealized Holding Gain or LossEquity180,000

Notes Receivable180,000

c.Notes Receivable180,000

Unrealized Holding Gain or LossIncome180,000

d.Notes Receivable180,000

Unrealized Holding Gain or LossEquity180,000

9) If a material amount of inventory has been ordered through a formal purchase

contract at the balance sheet date for future delivery at firm prices,

a.this fact must be disclosed

b.disclosure is required only if prices have declined since the date of the order

c.disclosure is required only if prices have since risen substantially

d.an appropriation of retained earnings is necessary

10) Muggs Co. includes one coupon in each bag of dog food it sells. In return for eight

coupons, customers receive a leash. The leashes cost Muggs $3 each. Muggs estimates

that 45 percent of the coupons will be redeemed. Data for 2014 and 2015 are as follows:

2014 2015

Bags of dog food sold500,000600,000

Leashes purchased18,00022,000

Coupons redeemed120,000150,000

The premium expense for 2014 is

a.$187,500

b.$45,000

c.$75,000

d.$84,375

11) Which of the following terms is associated with recording a contingent liability?

a.Possible

b.Likely

c.Remote

d.Probable

12) Which of the following statements is true regarding IFRS and inventories?

a.In order to determine market valuation of inventories, IFRS uses a ceiling and a floor

b.IFRS permits the option of valuing inventories at fair value

c.With respect to inventories, IFRS defines market as net realizable value

d.IFRS allows inventory to be written up above its original cost

13) Elmer Corporation has $1,800,000 of short-term debt it expects to retire with

proceeds from the sale of 50,000 shares of common stock. If the stock is sold for $20

per share subsequent to the balance sheet date, but before the balance sheet is issued,

what amount of short-term debt could be excluded from current liabilities?

a.$1,000,000

b.$1,800,000

c.$800,000

d.$0

14) Which of the following statements about the statement of cash flows is correct?

a.The indirect method starts with income before extraordinary items

b.The direct method is known as the reconciliation method

c.The direct method is more consistent with the primary purpose of the statement of

cash flows

d.All of these answers are correct

15) Rule 203 of the Code of Professional Conduct addresses:

a.ethical requirements

b.financial statements being based on generally accepted accounting principles

c.advertising to obtain clients

d.auditing financial statements

16) Gage Co. purchases land and constructs a service station and car wash for a total of

$360,000. At January 2, 2014, when construction is completed, the facility and land on

which it was constructed are sold to a major oil company for $400,000 and immediately

leased from the oil company by Gage. Fair value of the land at time of the sale was

$40,000. The lease is a 10-year, noncancelable lease. Gage uses straight-line

depreciation for its other various business holdings. The economic life of the facility is

15 years with zero salvage value. Title to the facility and land will pass to Gage at

termination of the lease. A partial amortization schedule for this lease is as follows:

Payments InterestAmortization Balance

Jan. 2, 2014$400,000.00

Dec. 31, 2014$65,098.13$40,000.00$25,098.13374,901.87

Dec. 31, 201565,098.1337,490.1927,607.94347,293.93

Dec. 31, 201665,098.1334,729.3930,368.74316,925.19

What is the amount of the lessees liability to the lessor after the December 31, 2016

payment? (Rounded to the nearest dollar.)

a.$400,000

b.$374,902

c.$347,294

d.$316,925

17) In measuring an impairment loss, IFRS uses

a.undiscounted cash flows

b.discounted cash flows

c.a fair value test

d.a replacement value test

18) AG Inc. made a $15,000 sale on account with the following terms: 1/15, n/30. If the

company uses the gross method to record sales made on credit, what is/are the debit(s)

in the journal entry to record the sale?

a.Debit Accounts Receivable for $14,850

b.Debit Accounts Receivable for $14,850 and Sales Discounts for $150

c.Debit Accounts Receivable for $15,000

d.Debit Accounts Receivable for $15,000 and Sales Discounts for $150

19) A debt instrument with no ready market is exchanged for property whose fair value

is currently indeterminable. When such a transaction takes place

a.the present value of the debt instrument must be approximated using an imputed

interest rate

b.it should not be recorded on the books of either party until the fair value of the

property becomes evident

c.the board of directors of the entity receiving the property should estimate a value for

the property that will serve as a basis for the transaction

d.the directors of both entities involved in the transaction should negotiate a value to be

assigned to the property

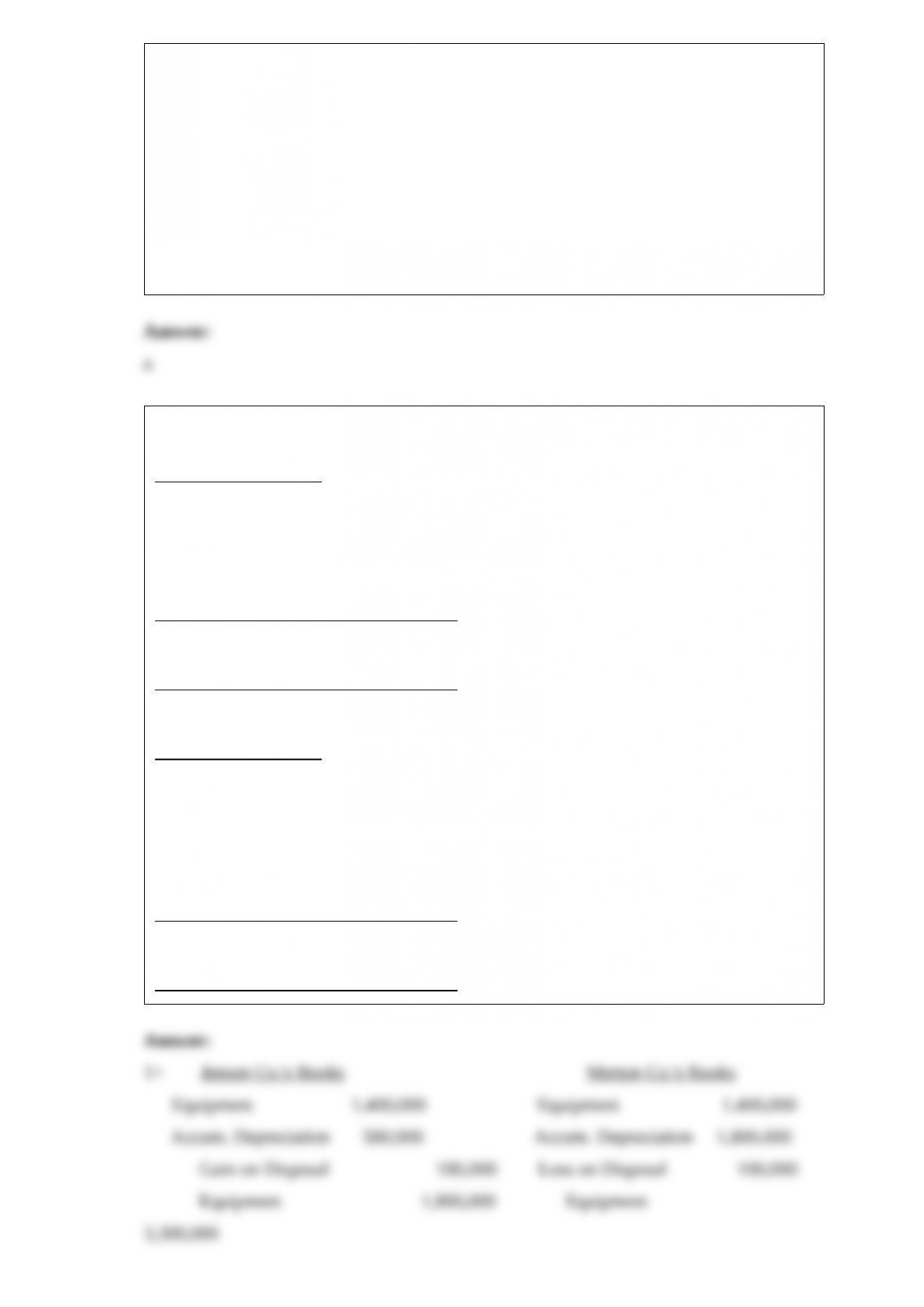

20) Assume that the following cases are independent and rely on the following data.

Make entries on the books of both companies.

Jensen Co.Merton Co.

Equipment (cost)$1,800,000$3,300,000

Accumulated depreciation580,0001,800,000

Fair value of equipment1,400,0001,400,000

1>Jensen Co. and Merton Co. traded the above equipment. The exchange has

commercial substance.

Jensen Co.’s Books:Merton Co.’s Books:

2>Jensen Co. and Merton Co. traded the above equipment. The exchange lacks

commercial substance.

Jensen Co.’s Books:Merton Co.’s Books:

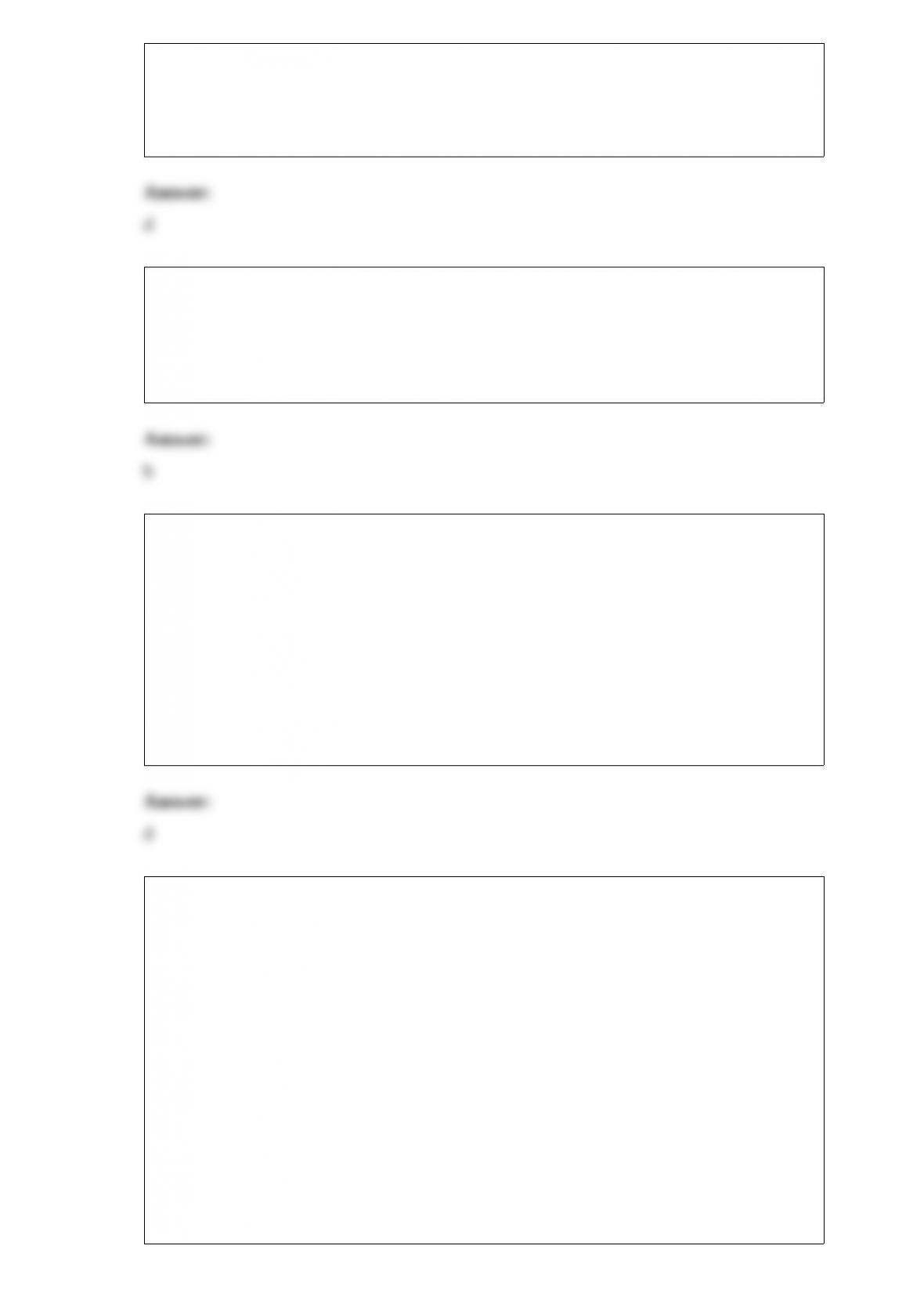

Assume that the following cases are independent and rely on the following data. Make

entries on the books of both companies.

Jensen Co.Merton Co.

Equipment (cost)$1,800,000$3,300,000

Accumulated depreciation580,0002,100,000

Fair value of equipment1,120,0001,400,000

Cash received (paid)(280,000)280,000

3>Jensen Co. and Merton Co. traded the above equipment. The exchange has

commercial substance.

Jensen Co.’s Books:Merton Co.’s Books:

4>Jensen Co. and Merton Co. traded the above equipment. The exchange lacks

commercial substance.

Jensen Co.’s Books:Merton Co.’s Books:

21) Theoretically, the costs of issuing bonds could be

a.expensed when incurred

b.reported as a reduction of the bond liability

c.debited to a deferred charge account and amortized over the life of the bonds

d.any of these answers are correct

22) In March, 2014, Mallory Mines Co. purchased a coal mine for $8,000,000.

Removable coal is estimated at 1,500,000 tons. Mallory is required to restore the land at

an estimated cost of $960,000, and the land should have a value of $840,000. The

company incurred $2,000,000 of development costs preparing the mine for production.

During 2014, 450,000 tons were removed and 300,000 tons were sold. The total amount

of depletion that Mallory should record for 2014 is

a.$1,832,000

b.$2,024,000

c.$2,748,000

d.$3,036,000

23) Under the deposit method

a.the seller recognizes revenue or income on the receipt of cash

b.a company receives cash from the buyer before it transfers the goods or property

c.the buyer reports the property as an asset on its balance sheet

d.the seller has performed on the contract and a legitimate claim exists

24) Net cash flow from operating activities for 2015 for Graham Corporation was

$330,000. The following items are reported on the financial statements for 2015:

Depreciation and amortization$ 20,000

Cash dividends paid on common stock 12,000

Increase in accounts receivable 24,000

Based only on the information above, Grahams net income for 2015 was:

a.$286,000

b.$294,000

c.$326,000

d.$334,000

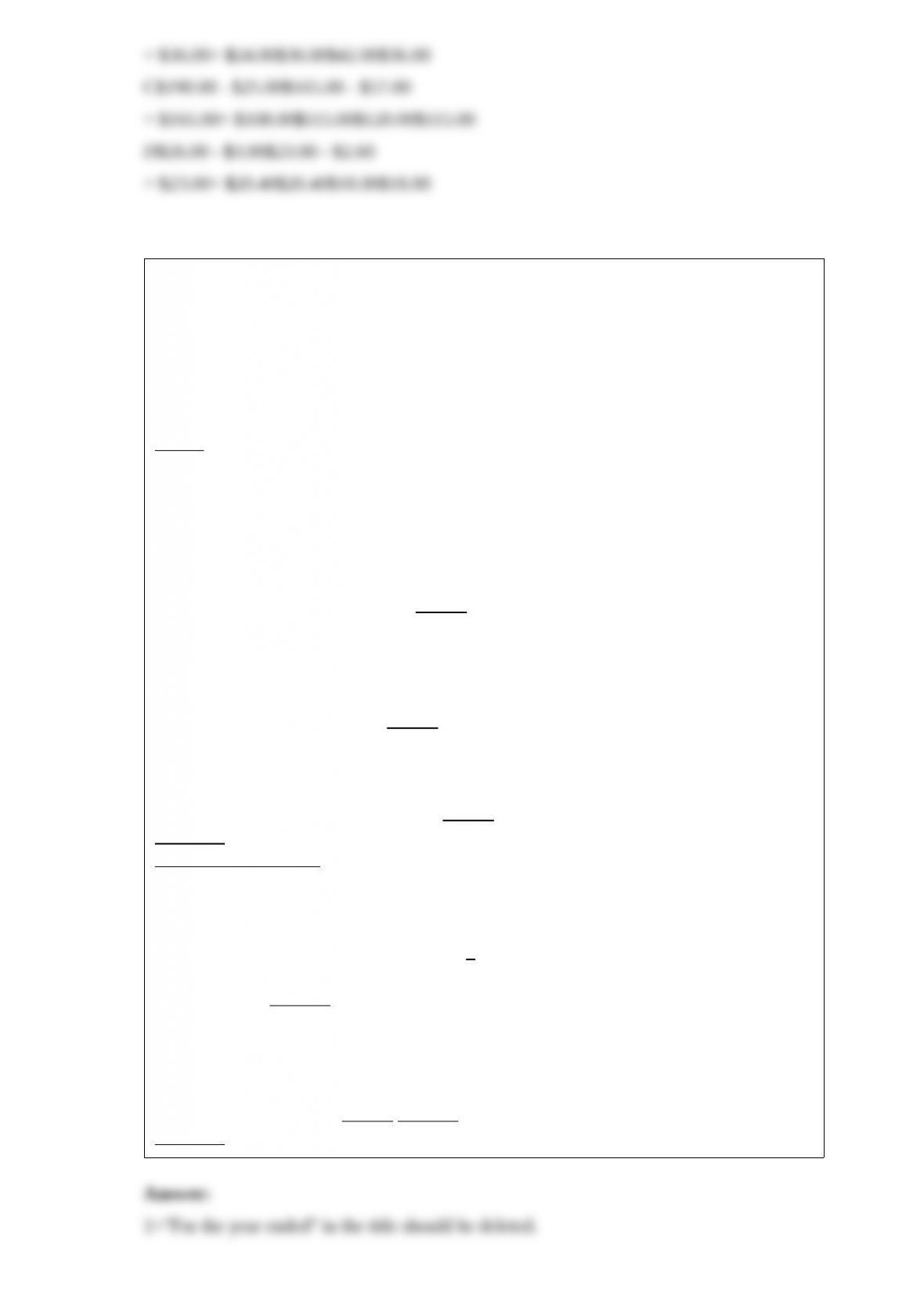

25) Indicate for each of the following what should be disclosed on a statement of cash

flows (indirect method). If not disclosed, write “Not shown.” There may be more than

one answer for some items. For an item that is added to net income, write “Add,” and

for an item that is deducted from net income, write “Deduct.” Show financing and

investing outflows in parentheses. For example, an answer might be: Deduct $4,700 or

Investing ($31,000). If the item is a noncash transaction that should be disclosed

separately, write “Noncash.”

(a)The deferred tax liability increased $10,000.

(b)The balance in Investment in Hoyt Co. Stock increased $12,000 as a result of using

the equity method.

(c)Issuance of a stock dividend increased common stock $40,000 and paid-in capital

$16,000.

(d)Amortization of bond discount, $1,600.

(e)Machinery that cost $100,000 and had accumulated depreciation of $48,000 was sold

for $54,000.

(f)Issued 9,000 shares of common stock ($10 par) with a market price of $15 per share

for machinery. (Show the amount, too.)

(g)Amortization of patents, $3,000.

(h)Cash dividends paid, $60,000.

26) Moon Co. records all sales using the installment-sales method of accounting.

Installment sales contracts call for 36 equal monthly cash payments. According to the

FASB’s conceptual framework, the amount of deferred gross profit relating to

collections 12 months beyond the balance sheet date should be reported in the

a.current liabilities section as a deferred revenue

b.noncurrent liabilities section as a deferred revenue

c.current assets section as a contra account

d.noncurrent assets section as a contra account

27) The December 31, 2014 inventory of Gwynn Company consisted of four products,

for which certain information is provided below.

ReplacementEstimatedExpectedNormal Profit

ProductOriginal Cost CostDisposal CostSelling Price on Sales

A$25.00$22.00$6.50$40.0020%

B$42.00$40.00$12.00$48.0025%

C$120.00$115.00$25.00$190.0030%

D$18.00$15.80$3.00$26.0010%

Instructions

Using the lower-of-cost-or-market approach applied on an individual-item basis,

compute the inventory valuation that should be reported for each product on December

31, 2014 .

28) List the corrections needed to present in good form the balance sheet below. Errors

include misclassifications, lack of adequate disclosure, and poor terminology. Do not

concern yourself with the arithmetic. If an item can be classified in more than one

category, select the category most favored by the authors of your textbook.

Tanner Corporation

Balance Sheet

For the year ended December 31, 2014

Assets

Current Assets:

Cash$ 18,000

Equity investmentstrading (fair value, $32,000)27,000

Accounts receivable75,000

Inventory60,000

Supplies inventory3,000

Investment in subsidiary company 60,000$243,000

Investments:

Treasury stock78,000

Tangible Fixed Assets:

Buildings and land213,000

Less: Reserve for depreciation 60,000153,000

Deferred Charges:

Discount on bonds payable3,000

Other Assets:

Cash surrender value of life insurance 54,000

$531,000

Liabilities and Capital

Current Liabilities:

Accounts payable$ 45,000

Reserve for income taxes42,000

Customer’s accounts with credit balances 3$ 87,003

Long-Term Liabilities:

Bonds payable 120,000

Total Liabilities207,003

Capital Stock:

Capital stock225,000

Earned surplus74,997

Cash dividends declared 24,000 323,997

$531,000

29) Presented below is an income statement for Kinder Company for the year ended

December 31, 2014 .

Kinder Company

Income Statement

For the Year Ended December 31, 2014

Net sales$800,000

Costs and expenses:

Cost of goods sold560,000

Selling, general, and administrative expenses70,000

Other, net 30,000

Total costs and expenses 660,000

Income before income taxes140,000

Income taxes 42,000

Net income$98,000

Additional information:

1>”Selling, general, and administrative expenses” included a usual but infrequent

charge of $7,000 due to a loss on the sale of investments.

2>”Other, net” consisted of interest expense, $10,000, and an extraordinary loss of

$20,000 before taxes due to earthquake damage. If the extraordinary loss had not

occurred, income taxes for 2014 would have been $48,000 instead of $42,000.

4>Kinder had 20,000 shares of common stock outstanding during 2014 .

Instructions

Using the single-step format, prepare a corrected income statement, including the

appropriate per share disclosures.

30) For each of the unrelated transactions described below, present the entry(ies)

required to record the bond transactions.

1>On August 1, 2015, Lane Corporation called its 10% convertible bonds for

conversion. The $7,000,000 par bonds were converted into 280,000 shares of $20 par

common stock. On August 1, there was $700,000 of unamortized premium applicable to

the bonds. The fair value of the common stock was $20 per share. Ignore all interest

payments.

2>Packard, Inc. decides to issue convertible bonds instead of common stock. The

company issues 10% convertible bonds, par $3,000,000, at 97 . The investment banker

indicates that if the bonds had not been convertible they would have sold at 94 .

3>Gomez Company issues $8,000,000 of bonds with a coupon rate of 8%. To help the

sale, detachable stock warrants are issued at the rate of ten warrants for each $1,000

bond sold. It is estimated that the value of the bonds without the warrants is $7,896,000

and the value of the warrants is $504,000. The bonds with the warrants sold at 101 .

31) Redstone Company spent $190,000 developing a new process, $45,000 in legal fees

to obtain a patent, and $91,000 to market the process that was patented. How should

these costs be accounted for in the year they are incurred?

32) A concept is a group of related ideas. Matching could be considered a concept

because it includes ideas related to expense recognition. Briefly explain the ideas in

expense recognition.