Under group and composite depreciation methods, gains and losses on the disposal of

individual assets need not be computed.

All changes reported using the retrospective approach require prior period adjustments.

Pension expense and funding amounts are both accounting decisions.

A customer advance produces a liability that is satisfied when the product or service is

provided.

Future taxable amounts result in deferred tax assets.

The enhancing qualitative characteristic of understandability means that information

should be understood by:

a. Those who are experts in the interpretation of financial information.

b. Those who have a reasonable understanding of business and economic activities.

c. Financial analysts.

d. CPAs.

A company should accrue a loss contingency only if the likelihood that a liability has

been incurred is:

a. More likely than not and the amount of the loss is known.

b. At least reasonably possible and the amount of the loss is known.

c. At least reasonably possible and the amount of the loss can be reasonably estimated.

d. Probable and the amount of the loss can be reasonably estimated.

At the end of the current year, a company overstated prepaid insurance by $80,000 and

understated supplies expense by $100,000. Its effective tax rate is 40%. As a result of

this error, net income is:

a. Overstated by $108,000.

b. Overstated by $12,000.

c. Understated by $108,000.

d. Understated by $12,000.

The prospective approach usually is required for:

a. A change in accounting principle.

b. A change in reporting entity.

c. A change in estimate.

d. A correction of an error.

Proceeds from the sale of a plant site are:

a. Reported as an operating activity in the statement of cash flows.

b. Reported as an investing activity in the statement of cash flows.

c. Reported as a financing activity in the statement of cash flows.

d. None of these answer choices is correct.

A sales-type lease differs from a direct financing lease in one respect:

a. The lessor receives a manufacturer’s or dealer’s profit.

b. The lessor receives more interest than on a direct financing lease.

c. The lessor receives less interest than on a direct financing lease.

d. The lessor uses a longer amortization period than on a direct financing lease.

Markel Inc. has bonds outstanding during a year in which the general (risk-free) rate of

interest has not changed. Markel elected the fair value option for the bonds upon

issuance. What will the company report for the bonds in its income statement for the

year?

a. Interest expense and a gain.

b. Interest expense and a loss.

c. A gain and no interest expense.

d. Interest expense and no gain or loss.

Wilson’s compensation expense in 2016 for these stock options was:

Wilson Inc. developed a business strategy that uses stock options as a major

compensation incentive for its top executives. On January 1, 2016, 20 million options

were granted, each giving the executive owning them the right to acquire five $1 par

common shares. The exercise price is the market price on the grant date-$10 per share.

Options vest on January 1, 2020. They cannot be exercised before that date and will

expire on December 31, 2022. The fair value of the 20 million options, estimated by an

appropriate option pricing model, is $40 per option. Ignore income tax.

a. $0.

b. $200 million.

c. $400 million.

d. $800 million.

Interest payments to creditors are reported in a statement of cash flows as:

a. An investing activity.

b. A borrowing activity.

c. A financing activity.

d. An operating activity.

The debt to equity ratio indicates:

a. The margin of safety provided to creditors.

b. The extent of “trading on the equity” or financial leverage.

c. Profitability without regard to how resources are financed.

d. The effectiveness of employing resources provided by owners.

A cause-and-effect relationship is implicit in the:

a. Realization principle.

b. Historical cost principle.

c. Matching principle.

d. Going concern assumption.

Which of the following is not true about the “fair value through other comprehensive

income” approach for accounting for investments under IFRS No. 9?

a. Is allowed for equity method investments.

b. Includes unrealized gains in other comprehensive income.

c. Does not require reclassification of realized gains from other comprehensive income.

d. Is allowed for equity investments.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

double-declining balance method, depreciation for 2017 would be:

a. $28,800.

b. $18,240.

c. $17,280.

d. None of these answer choices are correct.

Patrick Rach International issued 5% bonds convertible into shares of the company’s

common stock. Rach applies U.S. GAAP. Upon issuance, Patrick Rach International

should record:

a. The proceeds of the bond issue as part debt and part equity.

b. The proceeds of the bond issue entirely as debt.

c. The proceeds of the bond issue entirely as equity.

d. The proceeds of the bond issue entirely as debt if the bonds are mandatorily

redeemable.

On January 1, 2016, Nana Company paid $100,000 for 8,000 shares of Papa Company

common stock. These securities were classified as trading securities. The ownership in

Papa Company is 10%. Papa reported net income of $52,000 for the year ended

December 31, 2016. The fair value of the Papa stock on that date was $45 per share.

What amount will be reported in the balance sheet of Nana Company for the investment

in Papa at December 31, 2016?

a. $284,400.

b. $300,000.

c. $315,600.

d. $360,000.

Which of the following does not apply to secondary markets?

a. Transactions are important to the efficient allocation of resources in our economy.

b. New resources are provided when shares of stock are sold by the corporation to the

initial owners.

c. Transactions help to establish market prices for additional shares that may be issued

in the future.

d. Many investors might be unwilling to provide resources to corporations if there is no

available mechanism for the future sale of their stocks and bonds to others.

Retrospective treatment of prior years’ financial statements is required when there is a

change from:

a. Average cost to FIFO.

b. FIFO to average cost.

c. LIFO to average cost.

d. All of these answer choices are correct.

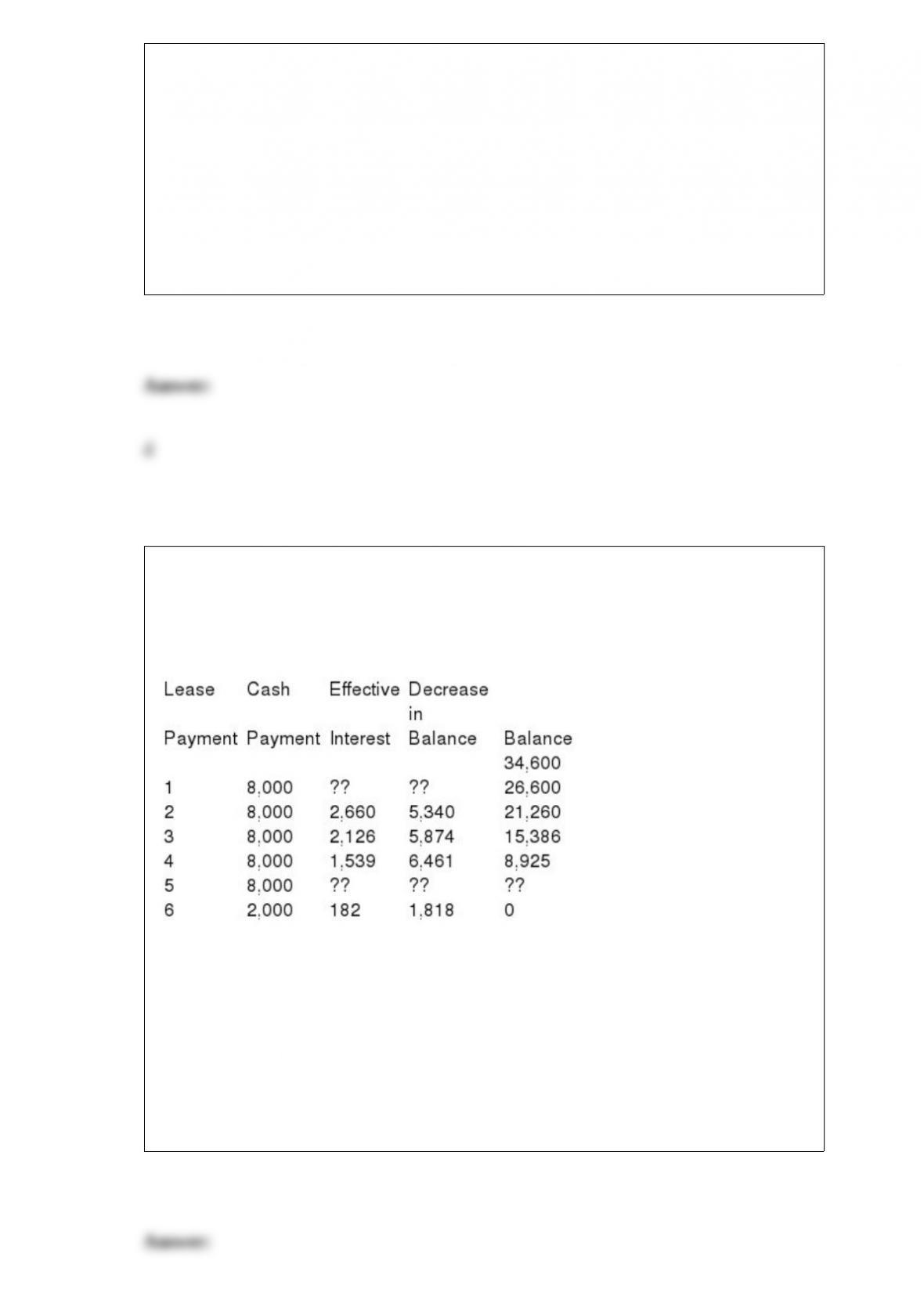

Refer to the following lease amortization schedule. The five payments are made

annually starting with the inception of the lease. A $2,000 bargain purchase option is

exercisable at the end of the five-year lease. The asset has an expected economic life of

eight years.

What is the outstanding balance after payment 5?

a. $1,818.

b. $2,000.

c. $2,182.

d. $3,818.

Which of the following must be known to compute the interest rate paid from financing

an asset purchase with an annuity?

a. Fair value of the asset purchased, number and dollar amount of the annuity payments.

b. Present value of the annuity, dollar amount and timing of the annuity payments.

c. Fair value of the asset and timing of the annuity payments.

d. Number of annuity payments and future value of the annuity.

Mobic Inc. acquired some manufacturing equipment in January 2013 for $400,000 and

depreciated it $40,000 each year for three years on a straight-line basis. During 2016,

the manufacturer announced a new technology for this type of equipment that will make

the old models obsolete by the end of 2019. As a result, Mobic will plan to replace the

equipment at that time, effectively reducing the asset’s life from ten to seven years. In

its financial statements for 2016, Mobic should:

a. Charge $280,000 in depreciation expense.

b. Report the book value of the equipment in its12/31/2016 balance sheet at $210,000.

c. Make an adjustment to retained earnings for the error in measuring depreciation

during 2013-2015.

d. None of these answer choices is correct.

Yummy Rice Cereal offers an all-star bowl in exchange for three coupons. Yummy Rice

estimates that 30% of coupons will be redeemed. The bowls cost Yummy Rice $1 each.

In 2016, 5,000,000 coupons were distributed. By year-end 900,000 coupons had been

redeemed.

Required:

Calculate the liability that Yummy Rice should report at December 31, 2016.

Listed below are 10 organizations followed by a list of phrases that describe or

characterize the organizations. Match each phrase with the correct organization by

placing the number designating the best term in the space provided by the phrase.

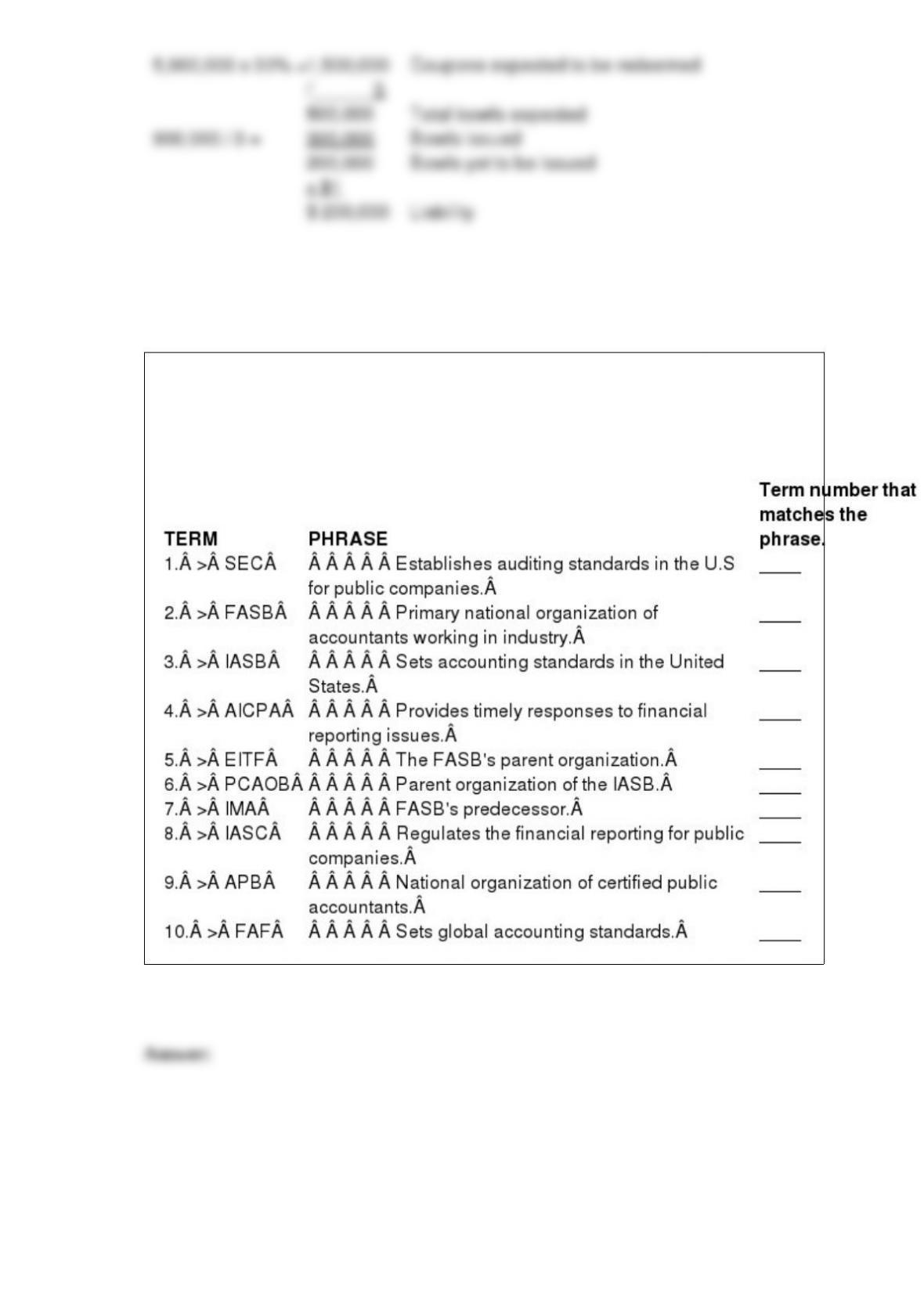

On December 31, 2015, Vitners Company had outstanding 400,000 shares of common

stock and 40,000 shares of 8% cumulative preferred stock (par $10).

February 28, 2016, issued an additional 36,000 shares of common stock

September 1, 2016, 9,000 shares were retired.

A 10% stock dividend was declared and distributed on July 1, 2016.

At year-end, there were fully vested incentive stock options outstanding for 30,000

shares of common stock (adjusted for the stock dividend). The exercise price was $18.

The market price of the common stock averaged $20 during the year. Also outstanding

were $1,000,000 face amount of 10% convertible bonds issued in 2013 and convertible

into 50,000 common shares (adjusted for the stock dividend). Net income was

$900,000. The tax rate for the year was 40%.

Required:

Compute basic and diluted EPS (rounded to 2 decimal places) for the year ended

December 31, 2016.

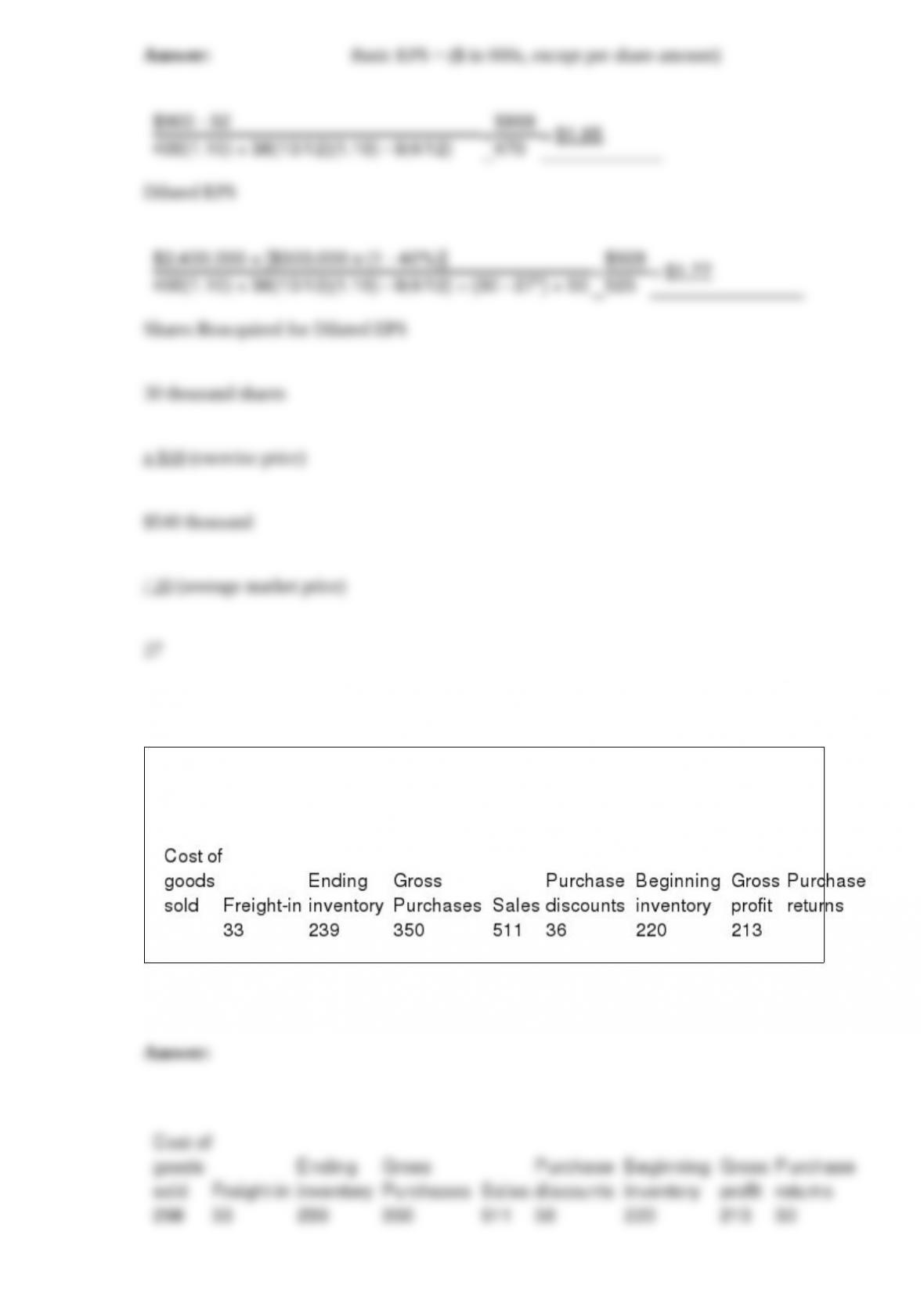

The following information is taken from the accounting records of Rapid Runner Inc.

for the year 2016. Missing information has been left blank. Required: Compute the

missing amounts.

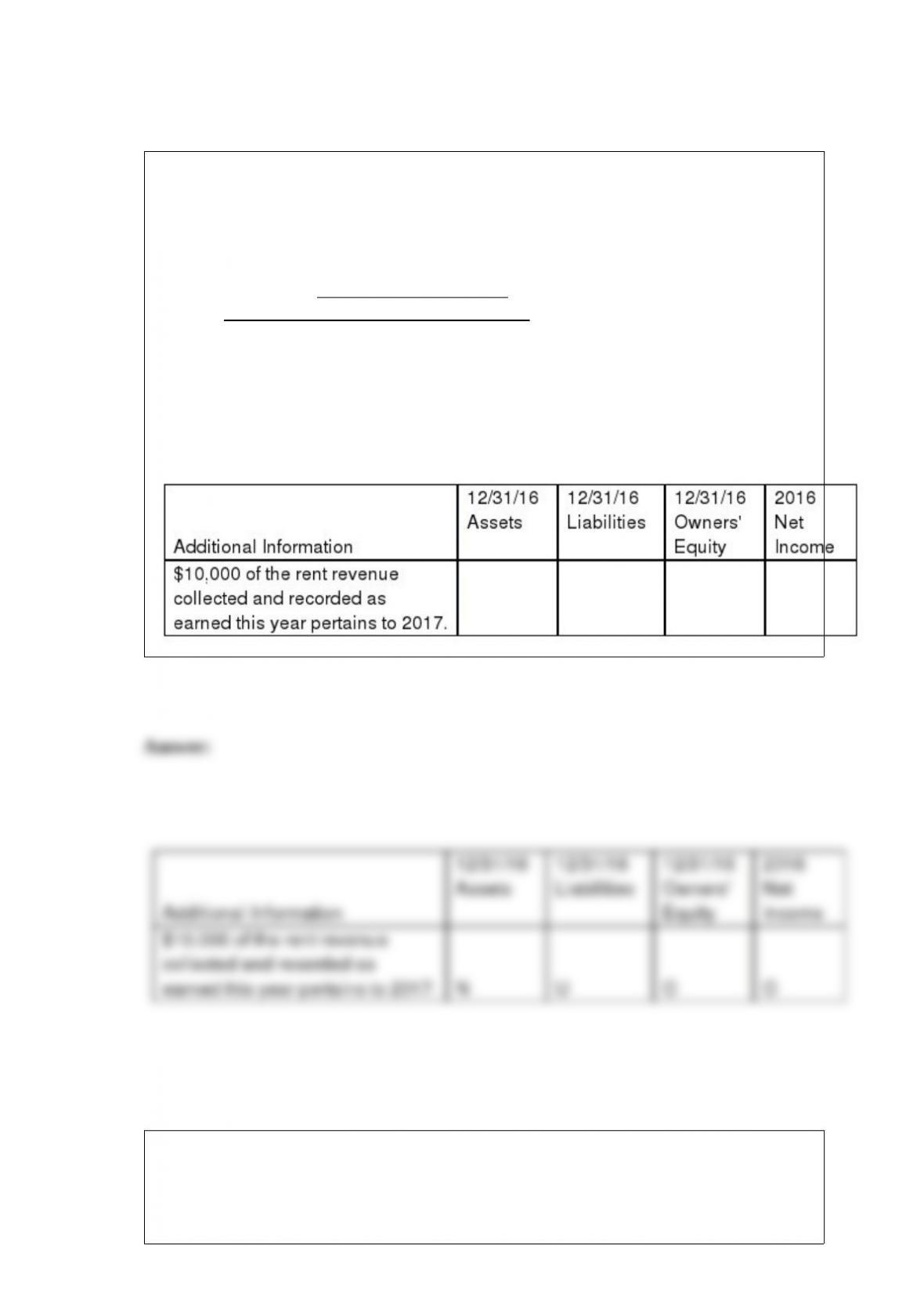

Use the following to answer questions 119-124: You are reviewing O’Brian Co.’s

adjusted trial balance for the year ended 12/31/16. You notice several omissions and

incorrect items during your review, some of which are noted below. For each one, you

are to determine what effect, if any, these items would have on the stated components of

O’Brian Co.’s 2016 Income Statement and 12/31/16 Balance Sheet if they are not

corrected or updated. Assume no income taxes. Use the following code for your

answers. You need not include any dollar amounts.

N = No Effect

O = Overstated

U = Understated

On October 1, 2016, Home Builders Company issued to Carlton Bank a $600,000,

8-month, noninterest-bearing note. Interest was discounted by the bank at a 12%

discount rate. Required:

1> Prepare the appropriate journal entry by Home Builders to record the issuance of the

note.

2> Determine the effective interest rate.

3> Suppose the note had been structured as a 12% note with interest and principal

payable at maturity. Prepare the appropriate journal entry to record the issuance of the

note by Home Builders.

4> Prepare the appropriate journal entry on December 31, 2016, to accrue interest

expense on the note described in number 3 for the 2016 financial statements.

Heirloom Watch Corporation

BALANCE SHEET

At January 1, 2017 ($ in millions)

Cash $ 40

Receivables 80

Inventory 250

Land 90

Buildings and equipment (net) 180

$640

Liabilities $480

Common stock (640 million shares at $.25 par) 160

Additional paid-in capital 0

Retained earnings (deficit) (0)

$640

Topic Area:

Essay

Instructions:

The following answers point out the key phrases that should appear in students’

answers. They are not intended to be examples of complete student responses. It might

be helpful to provide detailed instructions to students on how brief or in-depth you want

their answers to be.

A company changes depreciation methods. Briefly describe the steps the company

should take to report this accounting change in its current comparative financial

statements.