At the end of the current year, a company failed to accrue interest of $500,000 on its

investments in municipal bonds. Its tax rate is 30%. As a result of this error, net income

is:

a. Unaffected.

b. Understated by $350,000.

c. Understated by $500,000.

d. Understated by $150,000.

On March 1, 2020, when the market price of Wilson’s stock was $14 per share, 3

million of the options were exercised. The journal entry to record this would include:

Wilson Inc. developed a business strategy that uses stock options as a major

compensation incentive for its top executives. On January 1, 2016, 20 million options

were granted, each giving the executive owning them the right to acquire five $1 par

common shares. The exercise price is the market price on the grant date-$10 per share.

Options vest on January 1, 2020. They cannot be exercised before that date and will

expire on December 31, 2022. The fair value of the 20 million options, estimated by an

appropriate option pricing model, is $40 per option. Ignore income tax.

a. A debit to paid-in capital-stock options for $42 million

b. A credit to paid-in capital-excess of par for $255 million

c. A credit to common stock for $75 million

d. All of these answer choices are correct.

On September 30, 2016, Bricker Enterprises purchased a machine for $200,000. The

estimated service life is 10 years with a $20,000 residual value. Bricker records

partial-year depreciation based on the number of months in service. Depreciation for

2016, using double-declining balance, would be:

a. $40,000.

b. $10,000.

c. $36,000.

d. $ 9,000.

When accounting for pensions, delayed recognition of gains and losses in earnings

achieves:

a. Income averaging.

b. Expense averaging.

c. Income optimization.

d. Income smoothing.

Recognizing tax benefits in a loss year due to a net operating loss carryforward

requires:

a. Creating a tax refund receivable.

b. Note disclosure only.

c. Creating a deferred tax asset.

d. Creating a deferred tax liability.

El Dorado Foods Inc. owns a chain of specialty stores in the Pacific Northwest.

Recently, four of the stores have experienced declining profits due to market saturation

in the area. As a result, management gathered data about possible impairment of the

assets of the stores. The information gathered was as follows: Book value: $17.5

million

Fair value: $14.9 million

Undiscounted sum of future cash flows: $16.5 million Required:

Assume that the undiscounted sum of future cash flows is $18.2 million, instead of

$16.5 million. Determine the amount, if any, of the impairment loss that El Dorado

must recognize on these assets.

Revenue likely is recognized over time for all the following arrangements except for

a. Bank earning interest on a long term loan

b. Construction of a building

c. Providing a two-year gym membership

d. Manufacturing generally stocked items ordered by a favored customer

Chez Fred Bakery estimates the allowance for uncollectible accounts at 3% of the

ending balance of accounts receivable. During 2016, Chez Fred’s credit sales and

collections were $125,000 and $131,000, respectively. What was the balance of

accounts receivable on January 1, 2016, if $180 in accounts receivable were written off

during 2016 and if the allowance account had a balance of $750 on December 31,

2016?

a. $5,820.

b. $31,000.

c. $31,180.

d. None of these answer choices are correct.

Assets do not include:

a. Property, plant, and equipment.

b. Investments.

c. Paid-in capital.

d. Unexpired insurance.

Hazelton Manufacturing prepares a bank reconciliation at the end of every month. At

the end of May, the general ledger checking account showed a balance of $1,360 and

the bank statement showed a bank balance of $1,445. Outstanding checks totaled $350

and deposits in transit were $150. The bank statement listed service charges of $30 and

NSF checks totaling $85. The corrected cash balance is:

a. $1,130.

b. $1,160.

c. $1,245.

d. $1,445.

Fulbright Corp. uses the periodic inventory system. During its first year of operations,

Fulbright made the following purchases (listed in chronological order of acquisition):

– 40 units at $100

– 70 units at $ 80

– 170 units at $ 60 Sales for the year totaled 270 units, leaving 10 units on hand at the

end of the year. Ending inventory using the FIFO method is:

a. $ 650.

b. $1,000.

c. $ 707.

d. $ 600.

Cooper Inc. took physical inventory at the end of 2015. Purchases that were acquired

FOB destination were in transit, so they were not included in the physical count.

a. Cooper needs to correct an accounting error.

b. Cooper has made a change in accounting principle, requiring retrospective

adjustment.

c. Cooper is required to adjust a change in accounting estimate prospectively.

d. Cooper is not required to make any accounting adjustments.

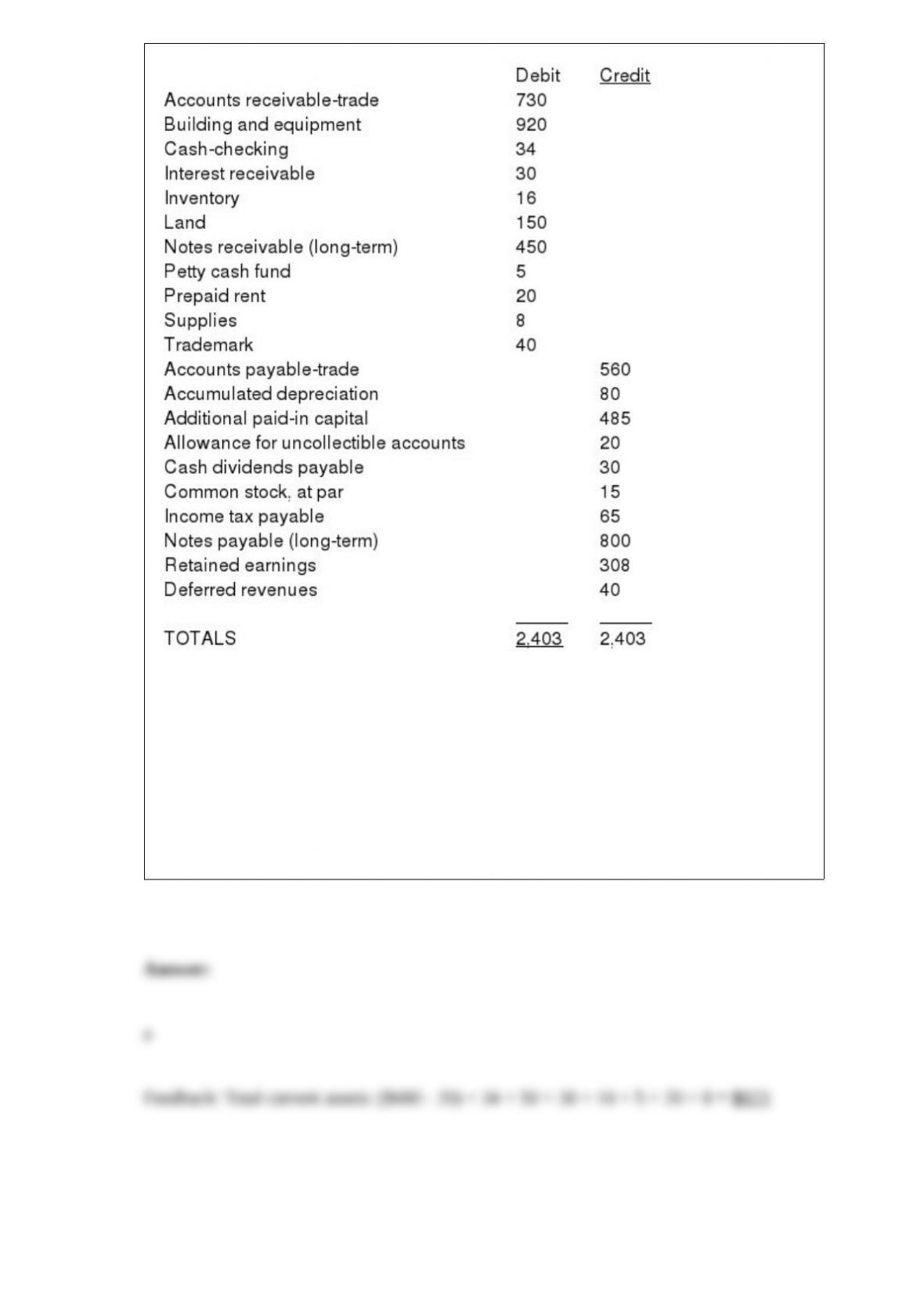

Listed below are year-end account balances (in $millions) taken from the records of

Symphony Stores.

What would Symphony report as total current assets?

a. $823.

b. $838.

c. $843.

d. $1,696.

Retrospective restatement usually is appropriate for a change in:

Accounting Estimate Accounting Principle

a. Yes Yes

b. Yes No

c. No Yes

d. No No

An exception that is so serious that even a qualified opinion is not justified would result

in:

a. A disclaimer.

b. An unqualified opinion.

c. An adverse opinion.

d. A consistency exception.

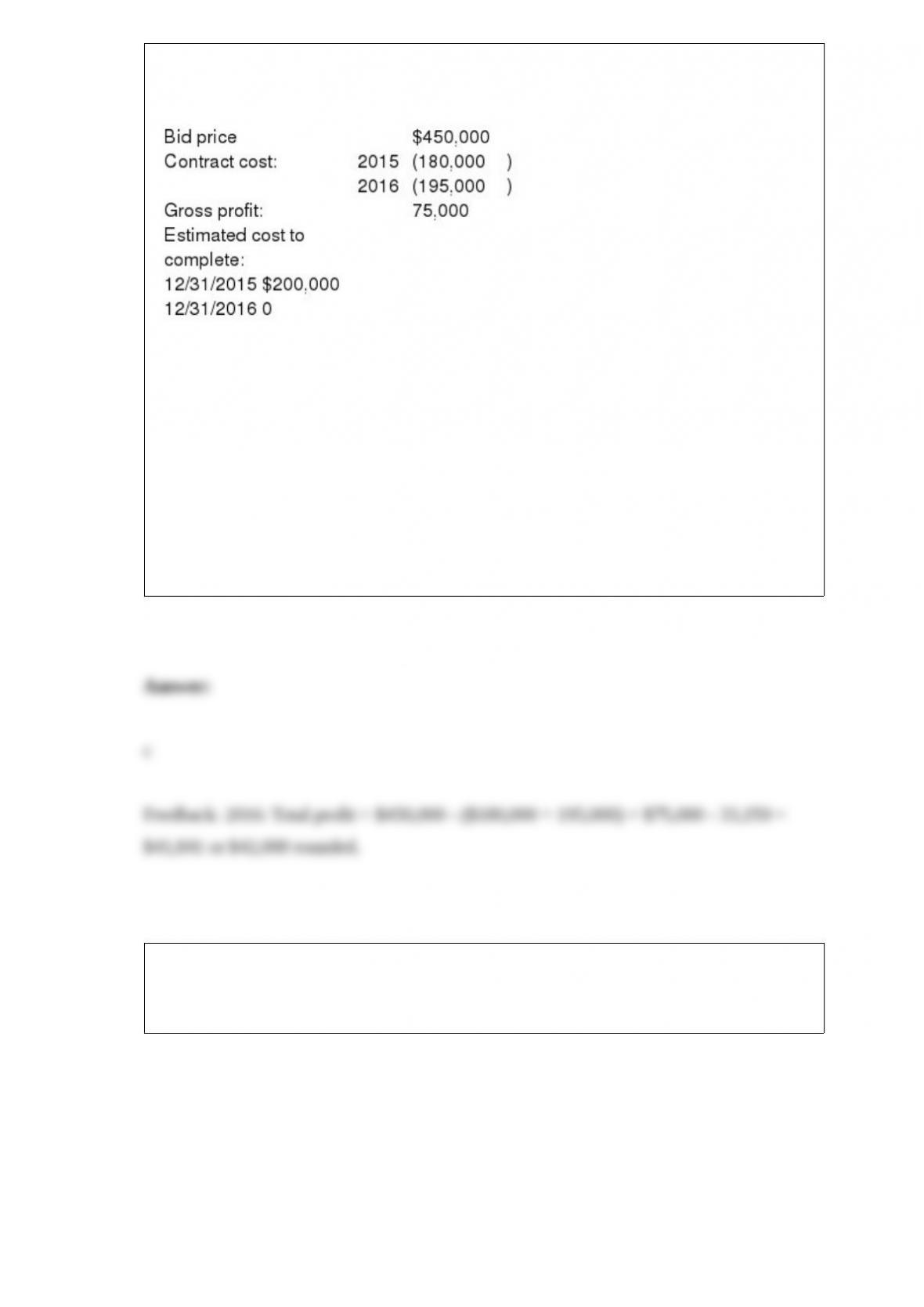

Summary data for Benedict Construction Co.’s (BCC) Job 1227, which was completed

in 2016, are presented below:

Assuming BCC recognizes revenue over time according to percentage of completion

for this contract, the gross profit recognized in 2016 would be (rounded to the nearest

thousand):

a. $ 6,000.

b. $39,000.

c. $42,000.

d. $45,000.

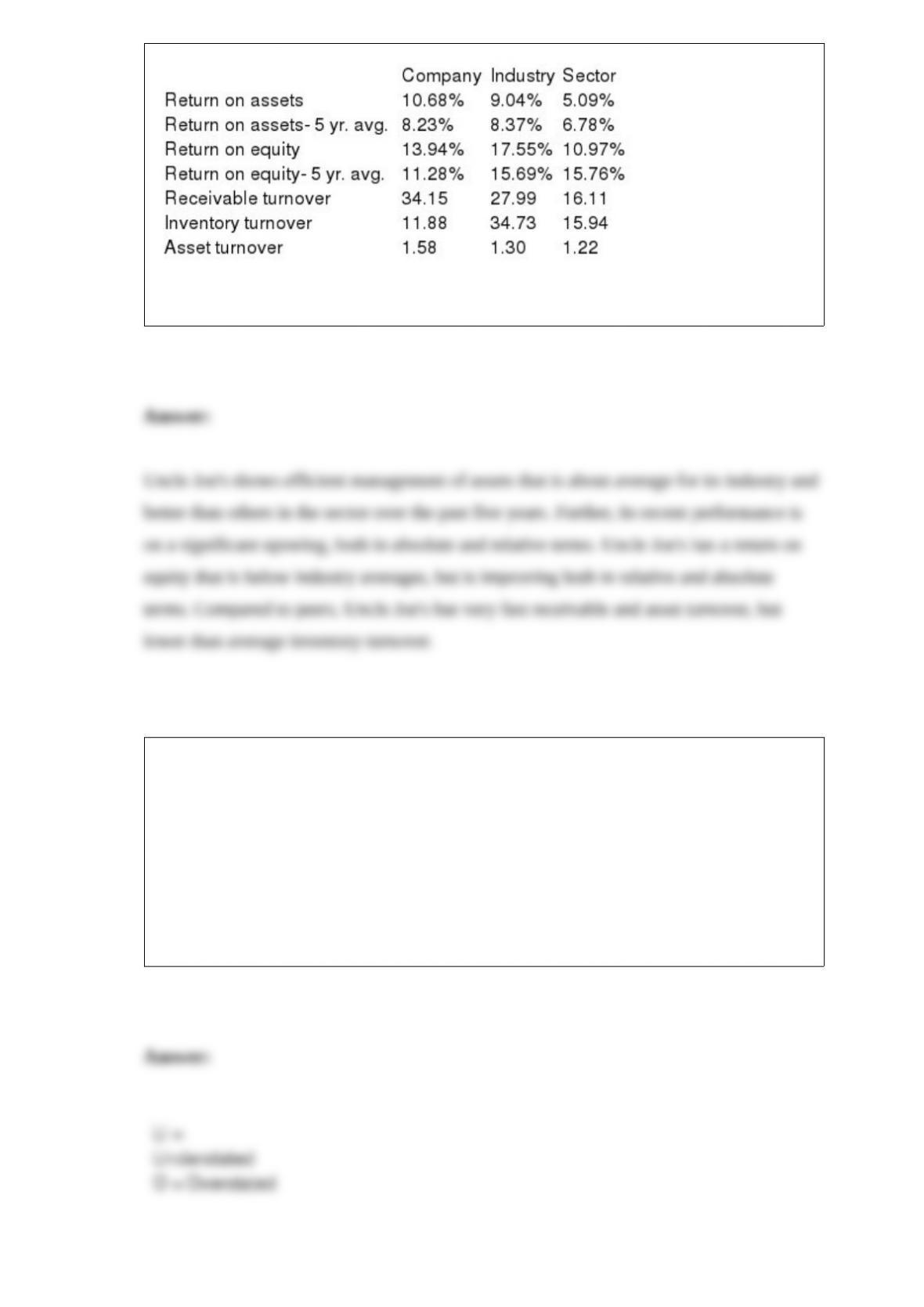

The following table presents a summary of ratio analysis for Uncle Joe’s Coffee, based

on the most recent 12 months and five-year comparisons of Uncle Joe’s with averages

in the restaurant industry and the services sector, respectively.

Using the information provided above, briefly summarize the operating performance of

Uncle Joe’s relative to its benchmark competitors.

In 2016, the internal auditors of Blooper Inc. discovered that goods costing $12 million

that were shipped f.o.b. shipping point in December of 2015 were in transit on

December 31. The goods were recorded as a purchase in December of 2015 but were

not included in the 2015 year-end inventory.

Required:

Prepare the journal entry needed in 2016 to correct the error. Also, briefly describe any

other measures Blooper would take in connection with correcting the error. (Ignore

income taxes.)

When stock is issued for consideration other than cash, what is the measurement

objective?

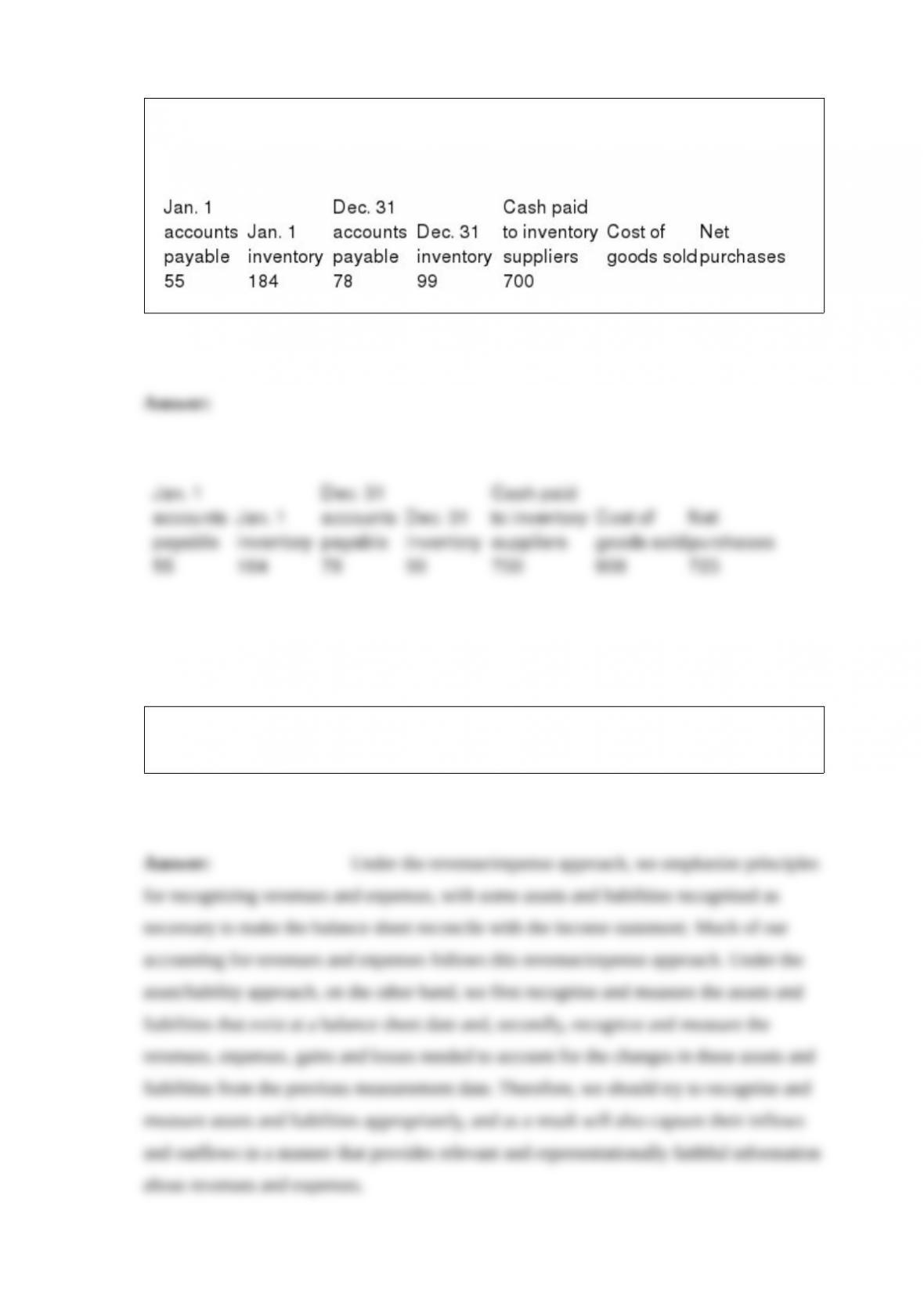

The following information is taken from the accounting records of Madeline Inc. for the

year 2016. Missing information has been left blank. Inventory is the only supply that

Madeline purchases on credit. Required: Compute the missing amounts.

Contrast the asset/liability and revenue/expense approaches to accounting standard

setting.