Using the gross method, purchase discounts lost are: A. Included in purchases.

B. Added to accounts payable.

C. Included in interest expense.

D. Deducted from discount income.

Answer:

The par value of common stock represents: A. The arbitrary dollar amount assigned to a

share of stock.

B. The liquidation value of a share.

C. The book value of a share of stock.

D. The amount received when the stock was issued.

Answer:

To evaluate the risk and quality of an individual bond issue, savvy investors rely

heavily on: A. Bond ratings provided by financial investment services such as Moody’s.

B. Newspaper articles.

C. Bond interest payments.

D. The company’s audit report.

Answer:

Which of the following is not true about how the proposed ASU treats impairments? A.

The objective is to calculate expected losses of contractual cash flows.

B. Losses are discounted for the time value of money.

C. Different buckets capture differences in the deterioration of credit quality.

D. Losses always are estimated for the remaining life of the investment.

Answer:

Excerpts from Hulkster Company’s December 31, 2013 and 2012, financial statements

are presented below:

Hulkster’s 2013 average days in inventory is (rounded): A. 61 days.

B. 92 days.

C. 101 days.

D. 90 days.

Answer:

An important argument in support of historical cost information is: A.Relevance.

B.Predictive quality for future cash flows.

C.Materiality.

D.Verifiability.

Answer:

On January 1, 2013, Black Inc. issued stock options for 200,000 shares to a division

manager. The options have an estimated fair value of $6 each. To provide additional

incentive for managerial achievement, the options are not exercisable unless divisional

revenue increases by 6% in three years. Black initially estimates that it is probable the

goal will be achieved. In 2014, after one year, Black estimates that it is not probable

that divisional revenue will increase by 6% in three years. Ignoring taxes, what is the

effect on earnings in 2014? A. $200,000 decrease.

B. $200,000 increase.

C. $400,000 increase.

D. No effect.

Answer:

Of the four criteria for a capital lease, which two are not applied if the lease begins

during the final quarter of the asset’s useful life? A. The 75% test and the bargain

purchase option.

B. The 90% test and the 75% test.

C. The 90% test is the only one to which this applies.

D. The bargain purchase and the passage of title criteria.

Answer:

When using the equity method to account for an investment, cash dividends received by

the investor from the investee should be recorded: A. As a reduction in the investment

account.

B. As an increase in the investment account.

C. As dividend income.

D. As a contra item to stockholders’ equity.

Answer:

Issued stock refers to the number of shares: A. Outstanding plus treasury shares.

B. Shares issued for cash.

C. In the hands of shareholders.

D. That may be issued under state law.

Answer:

Which of the following statements is true with regard to preferred stock (preference

shares)? A. Most preferred stock (preference shares) is reported under U.S. GAAP as

debt.

B. Most preferred stock (preference shares) is reported under IFRS as equity.

C. Under U.S. GAAP, mandatorily redeemable preferred stock is reported as equity.

D. Under IFRS, preferred stock dividends are reported in the income statement as

interest expense.

Answer:

The principal concern with accounting for related-party transactions is: A. The size of

the transactions.

B. Differences between economic substance and legal form.

C. The absence of legally binding contracts.

D. The lack of accurate data to record transactions.

Answer:

Excerpts from Hulkster Company’s December 31, 2013 and 2012, financial statements

are presented below:

Hulkster’s 2013 return on assets is (rounded): A. 7.1%.

B. 7.8%.

C. 13.5%.

D. 44.7%.

Answer:

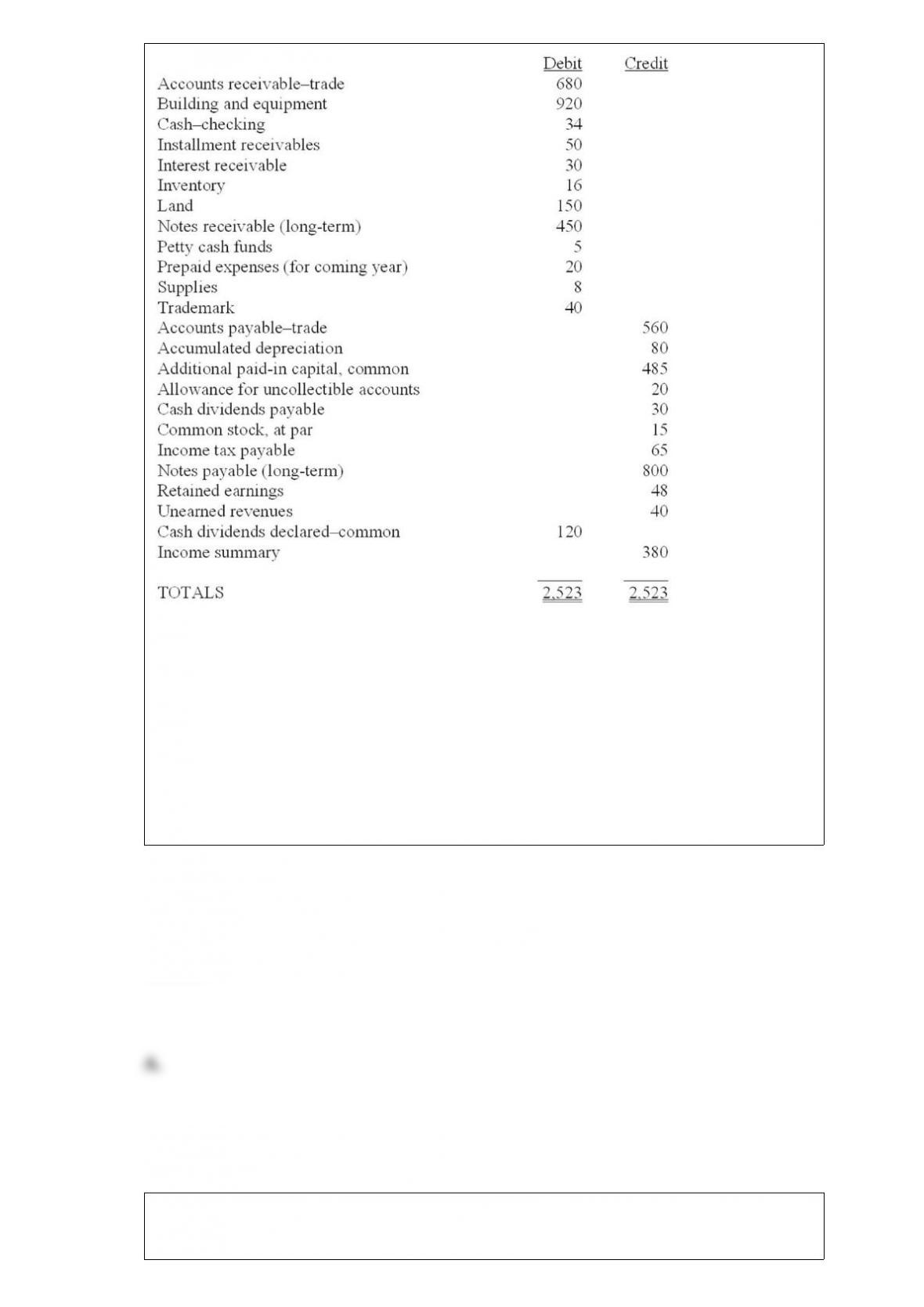

Listed below are account balances (in $ millions) taken from the records of Symphony

Stores. All of these are permanent accounts, except the last two that have yet to be

closed. The installment receivables are current. Symphony uses a perpetual inventory

system.

Cash equivalents would not include:

A. Cash not available for current operations.

B. Money market funds.

C. U.S. treasury bills.

D. Bank drafts.

Answer:

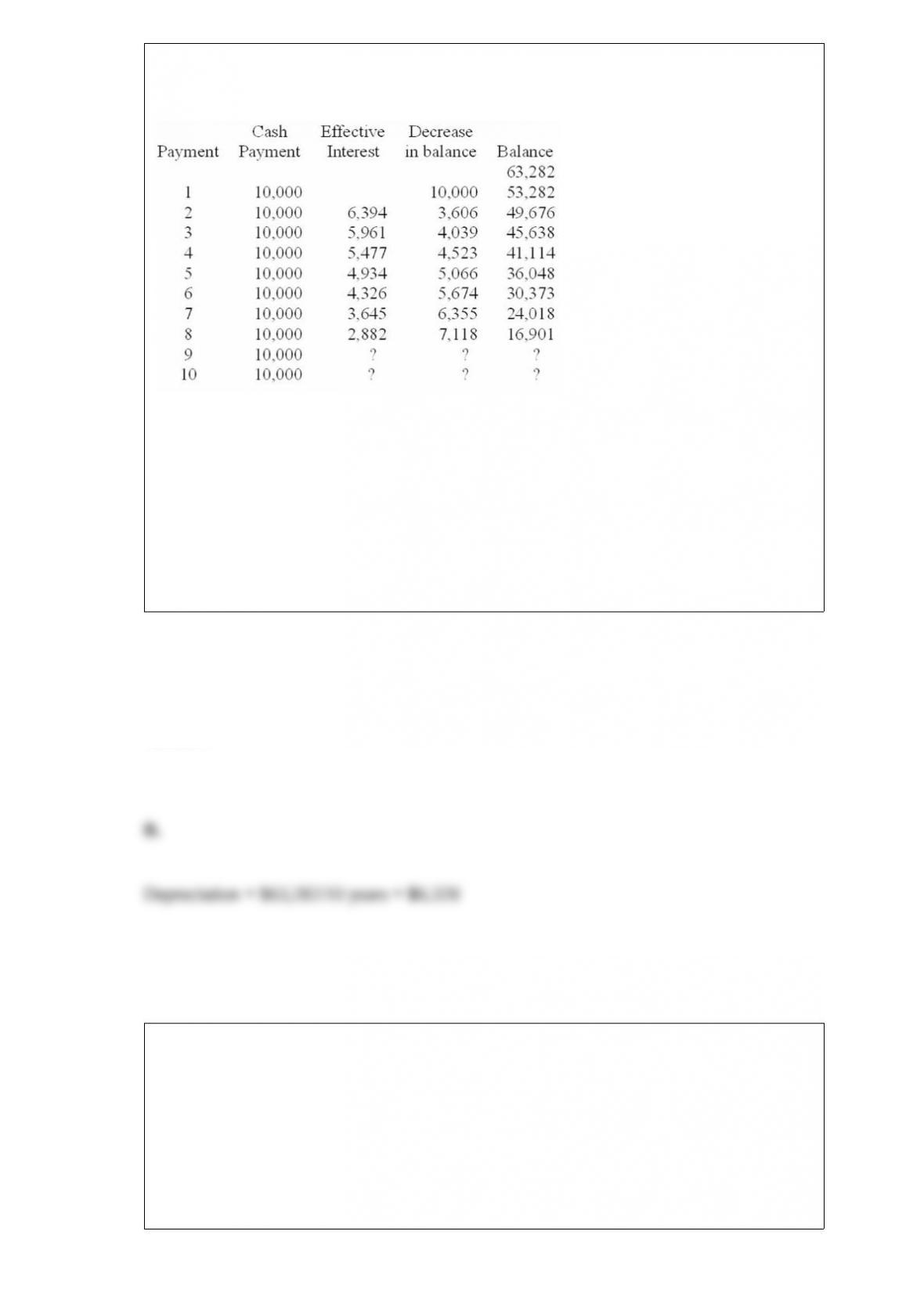

Refer to the following lease amortization schedule. The 10 payments are made annually

starting with the inception of the lease. Title does not transfer to the lessee and there is

no bargain purchase option or guaranteed residual value. The asset has an expected

economic life of 12 years. The lease is noncancelable.

What would the lessee record as annual depreciation on the asset using the straight-line

method? A. $5,328.

B. $6,328.

C. $6,392.

D. $10,000.

Answer:

Which of the following Statements of Financial Accounting Concepts defines the 10

elements of financial statements? A.SFAC 4.

B.SFAC 3.

C.SFAC 5.

D.SFAC 6.

Answer:

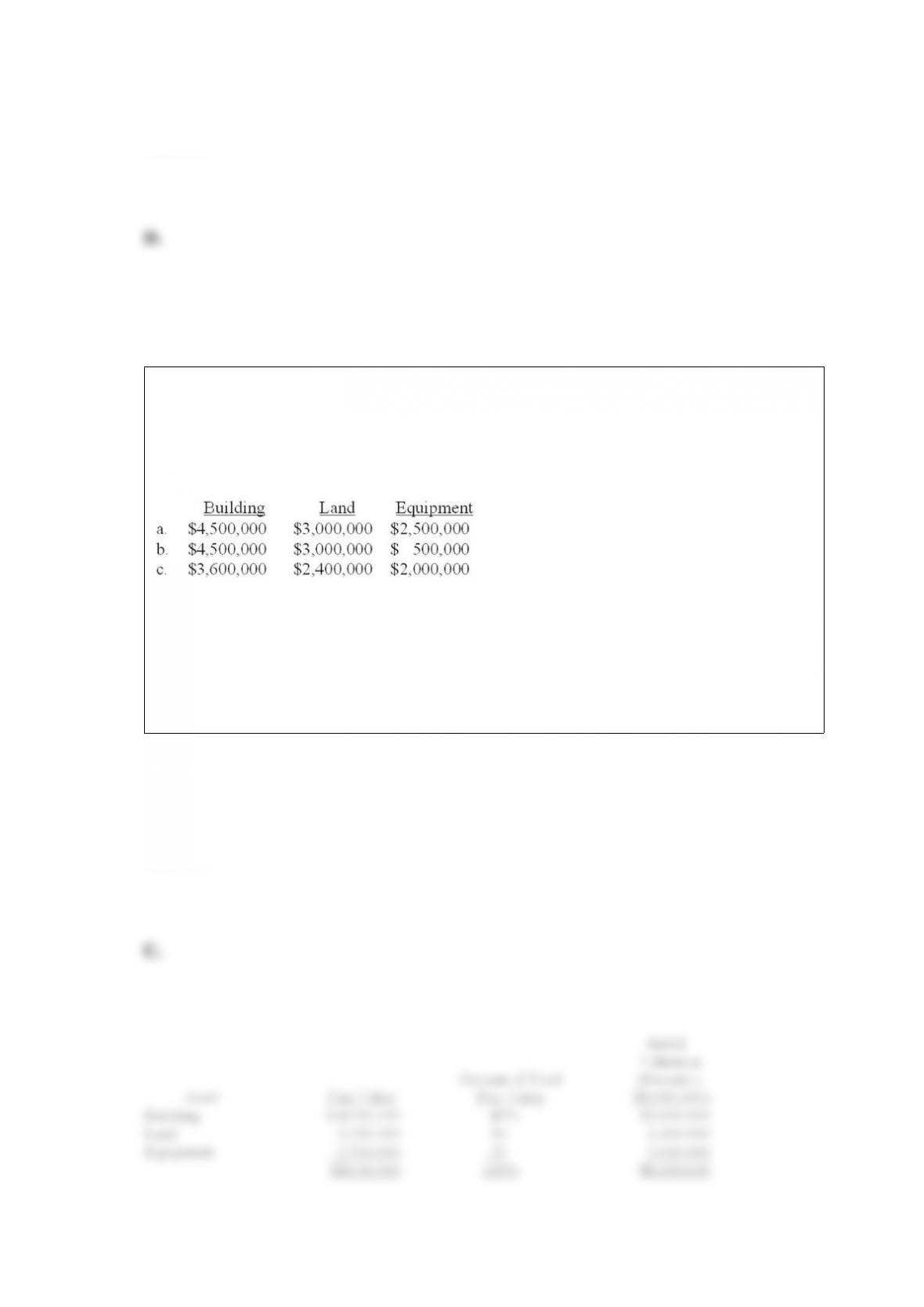

Cantor Corporation acquired a manufacturing facility on four acres of land for a

lump-sum price of $8,000,000. The building included used but functional equipment.

According to independent appraisals, the fair values were $4,500,000, $3,000,000, and

$2,500,000 for the building, land, and equipment, respectively. The initial values of the

building, land, and equipment would be:

A. Option a

B. Option b

C. Option c

D. None of the above.

Answer:

A company that prepares its financial statements according to International Financial

Reporting Standards can use each of the following inventory valuation methods except:

A. Average cost.

B. FIFO.

C. LIFO.

D. All of the above methods can be used.

Answer:

Excerpts from Hulkster Company’s December 31, 2013 and 2012, financial statements

are presented below:

Hulkster’s 2013 inventory turnover is (rounded): A. 3.62.

B. 3.96.

C. 4.07.

D. 6.03.

Answer:

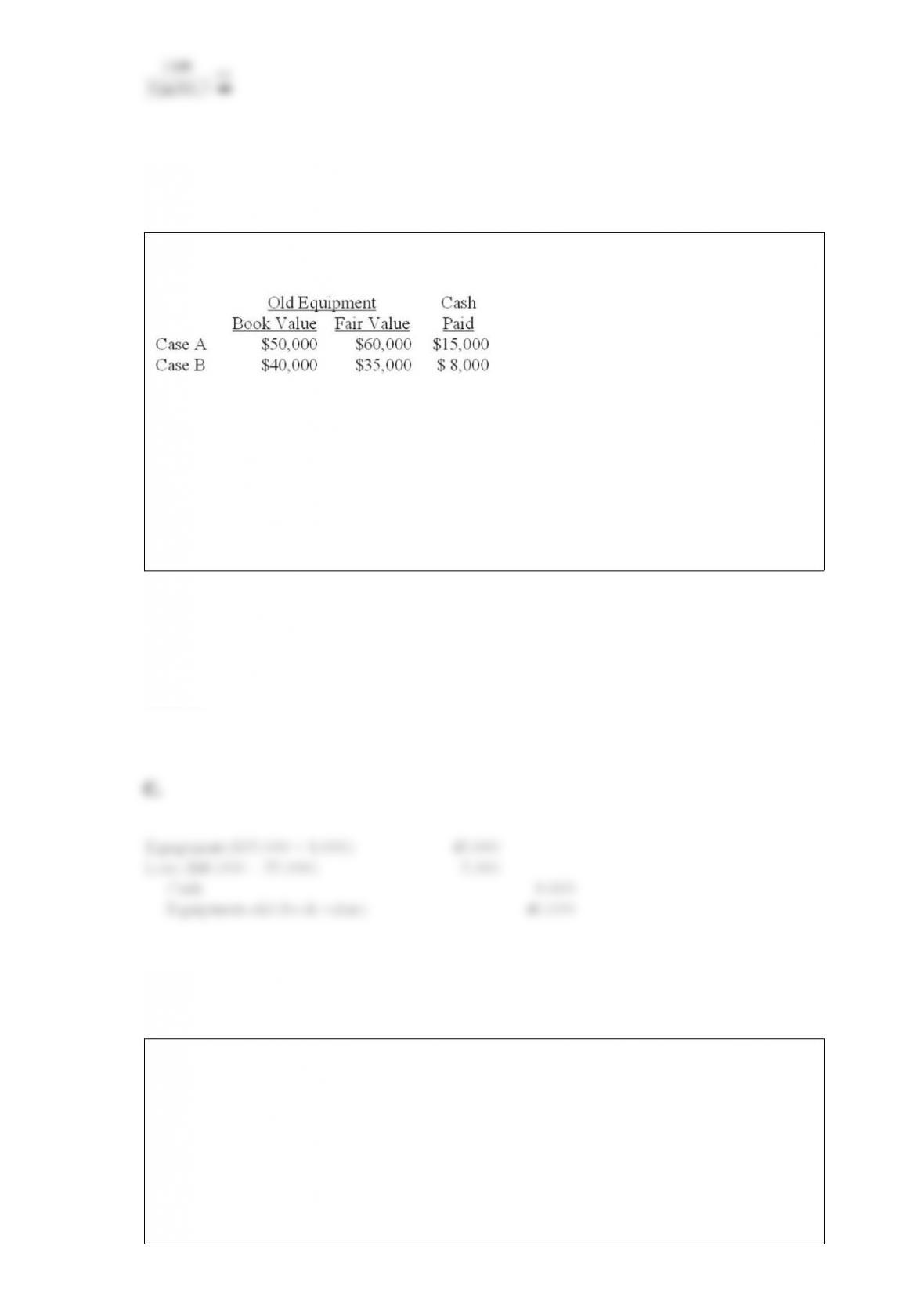

Below is information relative to an exchange of similar assets by Grand Forks Corp.

Assume the exchange has commercial substance.

In Case B, Grand Forks would record a gain/(loss) of: A. $5,000.

B. $3,000.

C. $(5,000).

D. $(3,000).

Answer:

The percentage-of-completion method violates the general rule for revenue recognition

that: A. Collection is reasonably assured.

B. Costs are known or reasonably estimated.

C. The earnings process is complete.

D. Collections have been received.

Answer:

During the current year, Stern Company had pretax accounting income of $45 million.

Stern’s only temporary difference for the year was rent received for the following year

in the amount of $15 million. Stern’s taxable income for the year would be: A. $30

million.

B. $60 million.

C. $50 million.

D. $45 million.

Answer:

The three components of pension expense that are present most often are: A. Service

cost, prior service cost, and gain on plan assets.

B. Service cost, interest cost, and gain from revisions in pension liability.

C. Service cost, contribution cost, and prior service cost.

D. Service cost, interest cost, and expected return on plan assets.

Answer:

Despot declared a property dividend to give marketable securities to its common

stockholders. The securities had cost Despot $7 million and currently have a fair value

of $16 million. Which of the following would be included in recording the property

dividend declaration? A. Increase in a liability for $16 million.

B. Decrease in retained earnings for $7 million.

C. Decrease in marketable securities by $16 million.

D. All of the above are correct.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Service life

2)Change in depreciation method

3)Depletion

4)Depreciable base

5)Amortization

A. Cost allocation for a natural resource

B. Treated prospectively like a change in estimate

C. Amount of use expected from plant and equipment asset

D. Cost less residual value

E. Cost allocation for an intangible asset.

Answer:

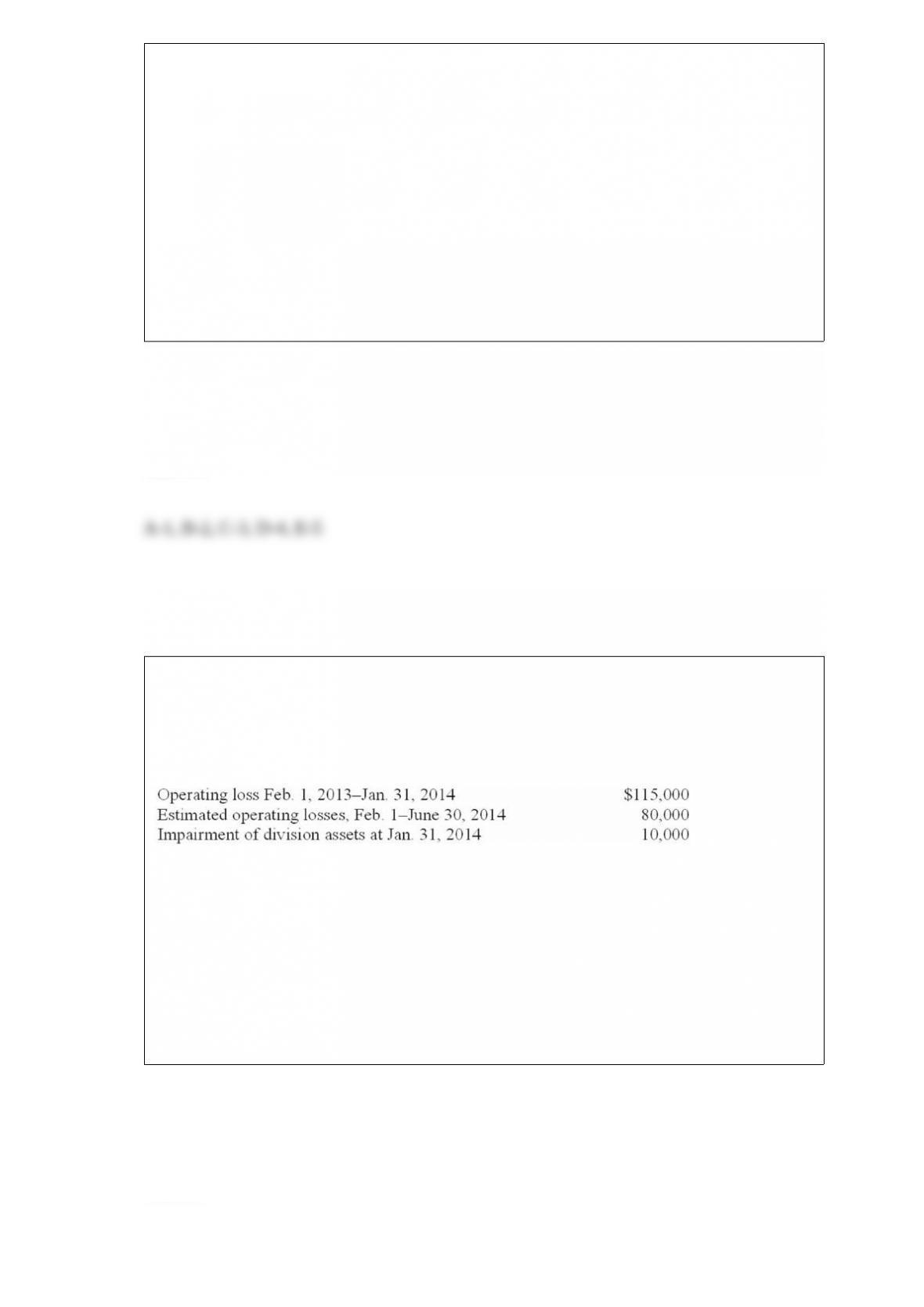

On August 1, 2013, Rocket Retailers adopted a plan to discontinue its catalog sales

division, which qualifies as a separate component of the business according to GAAP

regarding discontinued operations. The disposal of the division was expected to be

concluded by June 30, 2014. On January 31, 2014, Rocket’s fiscal year-end, the

following information relative to the discontinued division was accumulated:

In its income statement for the year ended January 31, 2014, Rocket would report a

before-tax loss on discontinued operations of: A. $115,000.

B. $195,000.

C. $65,000.

D. $125,000.

Answer:

The Guitar World (TGW) holds an investment that increased in fair value over 2013,

and accounts for that investment as available for sale. When considering taxes, TGW

would: A. Recognize tax expense on the income statement, and probably increase taxes

payable.

B. Recognize tax expense on the income statement, and probably increase its deferred

tax liability.

C. Reduce accumulated other comprehensive income (AOCI) for tax expense, and

probably increase taxes payable.

D. Reduce accumulated other comprehensive income (AOCI) for tax expense, and

probably increase its deferred tax liability.

Answer:

Permanent accounts would not include: A. Interest expense.

B. Wages payable.

C. Prepaid rent.

D. Unearned revenues.

Answer:

Hazelton Manufacturing prepares a bank reconciliation at the end of every month. At

the end of May, the general ledger checking account showed a balance of $1,360 and

the bank statement showed a bank balance of $1,445. Outstanding checks totaled $350

and deposits in transit were $150. The bank statement listed service charges of $30 and

NSF checks totaling $85. The corrected cash balance is: A. $1,130.

B. $1,160.

C. $1,245.

D. $1,445.

Answer:

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2012. Collections on this sale were $20,000 in 2012, $15,000 in

2013, and $20,000 in 2014.

In its 2012 year-end balance sheet, Reliable would report installment receivables (net)

of:A. $20,000.

B. $35,000.

C. $25,909.

D. $10,000.

Answer:

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment method

for revenue recognition. In 2012, Lake began operations and sold jet skis with a total

price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2012, $300,000

in 2013, and $300,000 in 2014 associated with those sales. In 2013, Lake sold jet skis

with a total price of $1,500,000 that cost Lake $900,000. Lake collected $500,000 in

2013, $400,000 in 2014, and $400,000 in 2015 associated with those sales. In 2015,

Lake also repossessed $200,000 of jet skis that were sold in 2013. Those jet skis had a

fair value of $75,000 at the time they were repossessed.

In 2014, Lake would recognize realized gross profit of:A. $0.

B. $450,000.

C. $310,000.

D. $700,000.

Answer:

Granite Enterprises acquired a patent from Southern Research Corporation on January

1, 2013, for $4 million. The patent will be used for 5 years, even though its legal life is

20 years. Rocky Corporation has made a commitment to purchase the patent from

Granite for $200,000 at the end of five years. Compute Granite’s patent amortization for

2013, assuming the straight-line method is used. A. $380,000.

B. $400,000.

C. $760,000.

D. $800,000.

Answer:

Nu Company reported the following pretax data for its first year of operations.

What is Nu’s net income if it elects FIFO? A. $480.

B. $288.

C. $1,360.

D. $144.

Answer: