The Petty Cash account is a separate chequing account used for small amounts.

Adjusting entries are designed primarily to correct errors made by bookkeepers.

A debit to Sales Returns and Allowances and a credit to Accounts Receivable mean that

a customer may have returned merchandise.

To check for accuracy after posting: first a trial balance is completed, then the

subsidiary ledgers are tested by preparing a schedule of the controlling account.

In a periodic inventory system, cost of goods sold is not recorded as each sale occurs.

Accounts that appear in the balance sheet are often called permanent or nominal

accounts.

Because accounting information systems are so accurate, decision makers in practice do

not need to have a basic knowledge of how the systems work.

Current liabilities are cash and other resources that are expected to be sold, collected, or

used within the longer of one year or the company’s operating cycle.

A contra-asset account has a normal debit balance.

Outstanding cheques are cheques the bank has paid and deducted from the customer’s

account during the month.

Trekking Company’s cost of inventory was $317,500. Due to phenomenal demand the

net realizable value has increased to $323,000. Trekking Company should write up the

value of inventory under the LCNRV rule.

Payment of accounts payable decreases both liabilities and assets.

The timeliness principle assumes that an organization’s activities can be divided into

specific periods.

Double-entry accounting means that every transaction affects and is recorded in at least

two accounts.

The retail inventory method of estimating inventory can be used to estimate the amount

of inventory shortage if a physical count is also done.

The gross profit ratio measures how much of each dollar of net sales is gross profit.

The cash basis of accounting is an accounting system in which revenues are reported in

the income statement when cash is received and expenses are reported when cash is

paid.

Internal operating functions include research and development, distribution, and human

resources.

An NSF cheque for $17.50 would be recorded as a debit to Cash and a credit to

Accounts Receivable.

Adjusting entries are used to record the effects of internal economic events.

The accounting equation is the link between a company’s assets, liabilities and equity.

Under the cash basis of accounting, no adjustments are made for prepaid, unearned, and

accrued items.

Y-Mart had net sales of $645,000. Its cost of goods was $445,000. Its gross margin was

$200,000.

All monies disbursed from petty cash should be documented by a petty cash receipt.

Non-business organizations often operate educational and religious services for profit.

The left side of a T-account is always the credit side, while the right side is always the

debit side.

Social responsibility is concern for the impact of our actions on society as a whole.

The periodic system does not record the increase in cost of goods sold and decrease in

inventory at the time of sale.

Computerized accounting systems should include controls to show when and where

corrections are made.

The accrual basis of accounting is an accounting system in which revenues are reported

as earned when cash is received.

Internal transactions have no effect on the accounting equation.

Off-the-shelf accounting software is inadequate to meet the needs of small businesses.

If your inventory is destroyed by fire you can estimate the amount of inventory

destroyed if you know: beginning inventory, purchases, net sales, and gross profit ratio.

The consistency principle helps ensure that financial statements are comparable across

periods.

The assignment of costs to cost of goods sold and inventory using (moving) weighted

average usually gives different results depending on whether a perpetual or periodic

system is used.

Because pledged receivables only serve as collateral for a loan and are not sold, it is not

necessary to disclose the pledging.

Cost of goods sold is reported on both the income statement and the balance sheet.

The agreed cost of an item to be purchased by a business on credit is $4,000. The

applicable cost will be debited to advertising expense. The item is subject to 5% goods

and services tax (GST) and 7% provincial sales tax (PST). When this transaction is

recorded, what amount will be credited to accounts payable?

A. $4,000

B. $4,200

C. $4,240

D. $4,480

E. None of these answers is correct.

An inventory error carried forward into the next period causes misstatements in:

A. Cost of goods sold.

B. Gross profit.

C. Net income.

D. Gross profit and net income.

E. All of these answers are correct.

A subsidiary ledger:

A. Includes transactions not covered by special journals.

B. Is a listing of all of the accounts of a business.

C. Is a listing of individual accounts with a common characteristic.

D. Is a listing of all accounts with balances.

E. Is a listing of all special journals.

Unearned revenues are:

A. Revenues that have been earned and received.

B. Revenues that have been earned but not yet collected.

C. Liabilities created by advance cash payments from customers for products or

services.

D. Recorded as an asset in the accounting records.

E. Increases to owners’ equity.

The Accounts Receivable ledger is:

A. used for recording credit sales.

B. used for storing transaction data for individual customers.

C. used for storing transaction data for individual creditors.

D. used for recording cash receipts from customers.

E. also the controlling account.

On May 31, Don Company had an Accounts Payable balance of $57,000. During the

month of June, total credits to Accounts Payable were $34,000, which resulted from

purchases on credit. The June 30 Accounts Payable balance was $32,000. What was the

amount of payments made during June?

A. $32,000.

B. $34,000.

C. $57,000.

D. $59,000.

E. $84,000.

A bank statement includes:

A. A list of outstanding cheques.

B. A list of petty cash amounts.

C. The beginning and ending balance of the depositor’s chequing account.

D. A list of outstanding cheques and a list of petty cash amounts.

E. All of these answers are correct.

Two clerks sharing the same cash register is a violation of which internal control

principle?

A. Establish responsibilities.

B. Maintain adequate records.

C. Insure assets.

D. Bond key employees.

E. Apply technological controls.

The cash to be received at maturity on a $10,000, 8%, 90-day note receivable is:

A. $197.26.

B. $5,126.26.

C. $6,187.26.

D. $10,197.26.

E. $12,297.26.

The cash sales operating cycle moves from:

A. Purchases to inventory for sale to cash sales.

B. Purchases to inventory for sale to accounts receivable to cash sales.

C. Inventory for sale to cash sales to purchases.

D. Accounts receivable to purchases to inventory for sale to cash sales.

E. Accounts receivable to inventory for sale to cash sales.

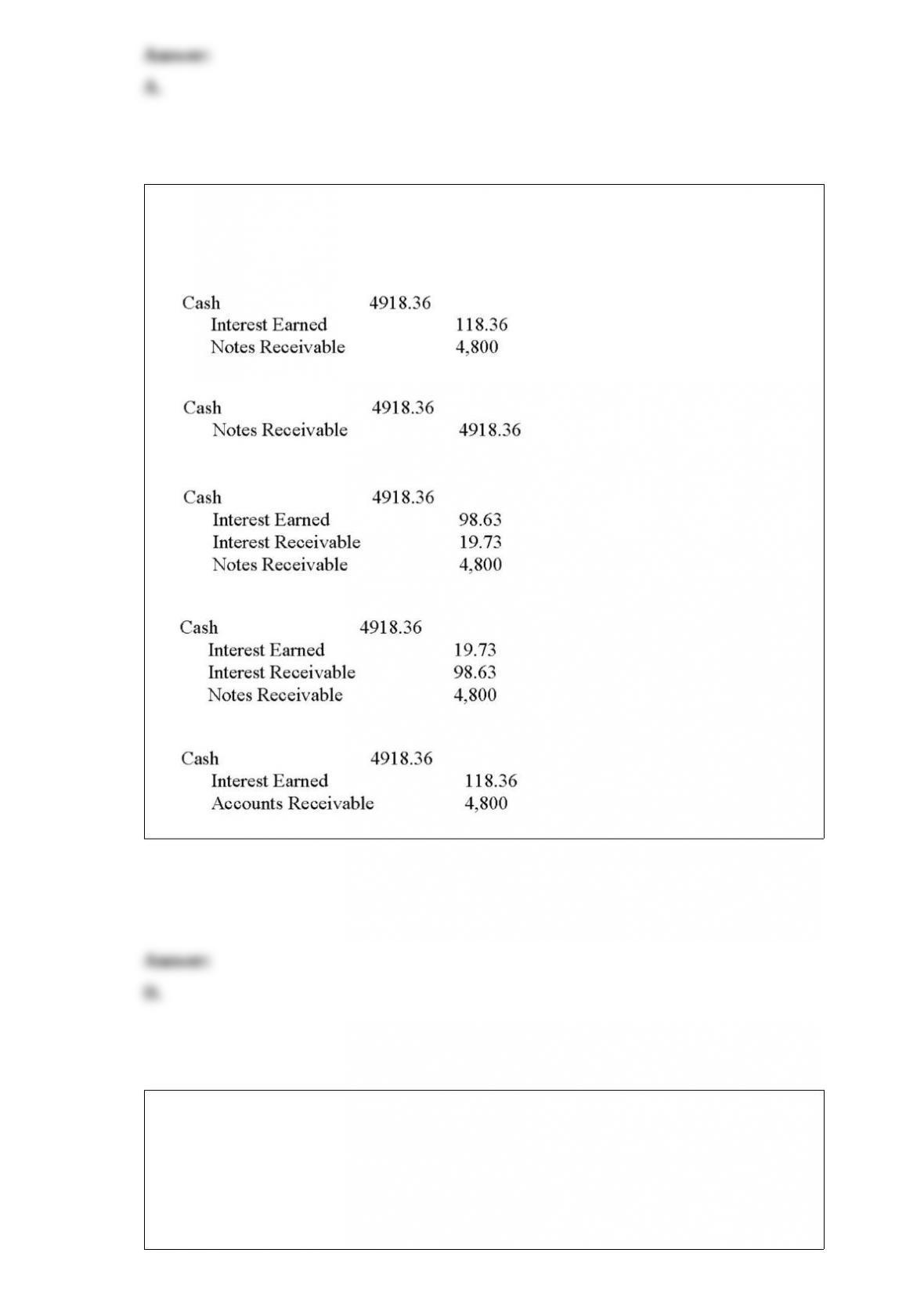

Rotel purchased merchandise from TechCom on October 17, 2014. TechCom accepted

Rotel’s $4,800, 90-day, 10% note as payment. TechCom has a December 31st year end.

What entry should TechCom make on January 15, 2015 when the note is honoured?

A.

B.

C.

D.

E.

An individual or organization that owes an amount to a business is known to the

business as a:

A. Debtor.

B. Shareholder.

C. Controller.

D. Creditor.

E. Bookkeeper.

When a Sales Journal’s sales amount column is totalled at the end of the month, the total

is:

A. Debited to Sales and credited to Accounts Receivable.

B. Debited to Accounts Receivable and credited to Cash.

C. Debited to Cash and credited to Accounts Receivable.

D. Debited to Accounts Receivable and credited to Sales.

E. Debited to Cash and credited to Sales.

Assets created by selling products or services on credit are:

A. Accounts payable.

B. Accounts receivable.

C. Liabilities.

D. Expenses.

E. Equity.

The area of accounting aimed at serving the decision-making needs of internal users is:

A. Financial accounting.

B. Managerial accounting.

C. Auditing.

D. Internal control.

E. Marketing.

The financial statement that describes where a company’s cash came from and where it

went during the period is the:

A. Statement of financial position.

B. Statement of cash flows.

C. Balance sheet.

D. Income statement.

E. Statement of changes in equity.

The quick assets are:

A. Cash, short-term investments, prepaid expenses.

B. Cash, short-term investments, accounts receivable.

C. Cash, inventory, accounts receivable.

D. Cash, accounts receivable, prepaid expenses.

E. Accounts receivable, inventory, prepaid expenses.

A balance sheet lists:

A. The types and amounts of the revenues and expenses of a business.

B. Only the information about what happened to equity during a specific time period.

C. The types and amounts of assets, liabilities, and equity of a business at a specific

date.

D. The inflows and outflows of cash during a specific time period.

E. The assets and liabilities of a business but not the equity.

When a maker of a note honours a note:

A. The note is signed.

B. The note is paid off.

C. The note is written.

D. The note is notarized.

E. The note is cosigned.

Management must include which of the following considerations when accounting for

inventory:

A. Costing method.

B. Inventory system.

C. Items to be included and their cost.

D. Use of lower of cost and net realizable value.

E. All of these answers are correct.

Cash equivalents:

A. Are readily convertible to a known cash amount.

B. Include short-term investments purchased to increase earnings.

C. Are often combined with cash as a single balance sheet item.

D. Are readily convertible to a known cash amount and include short-term investments

purchased to increase earnings.

E. All of these answers are correct.

Wholesalers:

A. Buy products from manufacturers and sell to retailers.

B. Buy products from other wholesalers and sell to consumers.

C. Buy products from manufacturers and sell to consumers.

D. Buy products from retailers and sell to consumers.

E. All of these answers are correct.

Which of the following does not require an adjusting entry at year-end?

A. Accrued interest on notes payable.

B. Supplies used during the period.

C. Cash invested by owner.

D. Accrued wages.

E. Expired portion of prepaid insurance.

Emilia Feridy, the proprietor of EF Services, withdrew a total of $50 for to pay for her

daughter’s swimming lessons. What is the entry needed to record this transaction?

A. Debit Emilia Feridy, Capital and credit Cash for $50.

B. Debit Emilia Feridy, Withdrawals and credit Cash for $50.

C. Debit Emilia Feridy, Withdrawals and credit Emilia Feridy, Capital for $50.

D. Debit Emilia Feridy, Capital and credit Emilia Feridy, Withdrawals for $50.

E. Debit Cash and credit Emilia Feridy, Withdrawals for $50.

The entry to record reimbursement of the petty cash fund for postage expense should

include:

A. A debit to Postage Expense.

B. A debit to Petty Cash.

C. A debit to Cash.

D. A debit to Cash Short and Over.

E. A debit to Supplies.

The general rule for posting to a subsidiary ledger and its controlling account is:

A. The controlling account is debited periodically for an amount or amounts equal to

the sum of the debits to the subsidiary ledger.

B. The controlling account is credited periodically for an amount or amounts equal to

the sum of the credits to the subsidiary ledger.

C. A trial balance ledger.

D. The controlling account is both debited and credited periodically for an amount or

amounts equal to the sum of the debits or credits to the subsidiary ledger.

E. All of these answers are correct.

The balance sheet equation is:

A. Revenues minus expenses equals net income.

B. Debits equal credits.

C. The bookkeeping phase of accounting.

D. Another name for the accounting equation.

E. Assets minus liabilities.

Journal entries recorded at the end of each accounting period to prepare the revenue,

expense, and withdrawals accounts for the upcoming year and to update the owner’s

capital account for the events of the year just finished are:

A. Adjusting entries.

B. Closing entries.

C. Final entries.

D. Work sheet entries.

E. None of these answers is correct.

The accounting principle that requires financial statements to report all contingent

liabilities is called:

A. Relevance.

B. Evaluation.

C. Full disclosure.

D. Materiality.

E. Matching.

Damaged or obsolete goods:

A. Are not counted as saleable inventory.

B. Are counted at full cost.

C. Are included in inventory at net realizable value if that is less than cost.

D. Are not counted as saleable inventory or are counted at full cost.

E. Are not counted as saleable inventory and are included in inventory at net realizable

value if that is less than cost.

The acid-test ratio differs from the current ratio:

A. Because liabilities are divided by current assets.

B. Because prepaid expenses and inventory are excluded.

C. Because it measures profitability.

D. Because it excludes short-term investments.

E. Because prepaid expenses and inventory are excluded and because it measures

profitability.

A book of original entry that is designed and used for recording only a specified type of

transaction is called a:

A. Schedule.

B. Columnar ledger.

C. Special journal.

D. General journal.

E. Subsidiary ledger.

Shrinkage:

A. Refers to the loss of inventory for merchandising companies.

B. Is not able to be directly measured by a perpetual inventory system.

C. Is recognized by debiting Cost of Goods Sold.

D. Can arise because of theft and deterioration of merchandise.

E. All of these answers are correct.

Match the following terms with the appropriate definition.

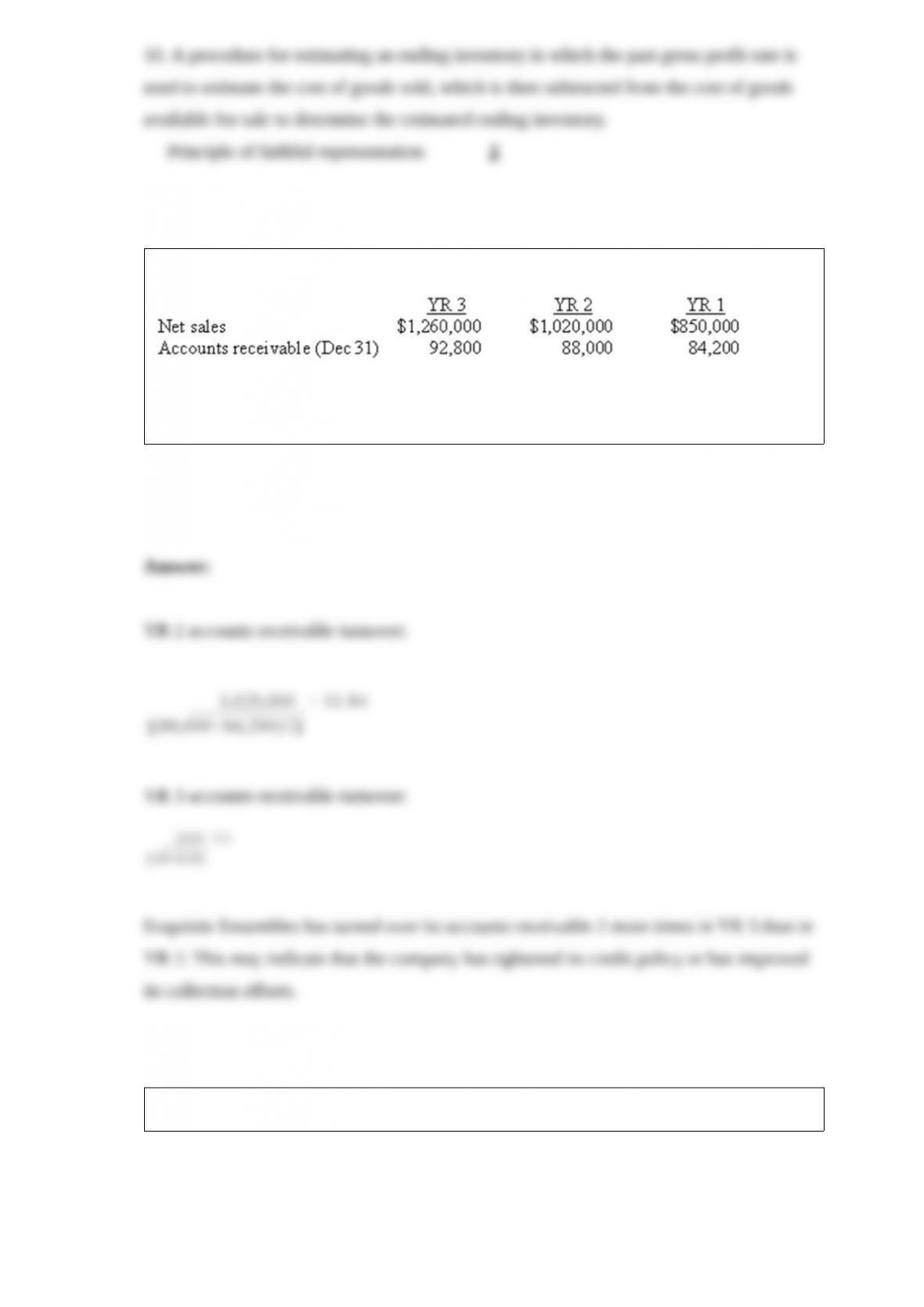

The following information is from the financial statements of Exquisite Ensembles:

Calculate Exquisite Ensembles’ accounts receivable turnover ratio for YR 2 and YR 3.

Compare the two results and give a possible explanation for any significant change.

Describe accounts receivable and how they are recorded into the accounting system.

Explain the recording and posting processes.

An internal control system is all policies and procedures managers use to

_______________, ensure reliable accounting, promote efficient operations, and

encourage adherence to company policies.