1) Shelby Boat Wash’s cost formula for its cleaning equipment and supplies is $2,200

per month plus $34 per boat. For the month of September, the company planned for

activity of 82 boats, but the actual level of activity was 32 boats. The actual cleaning

equipment and supplies for the month was $3,340.

The cleaning equipment and supplies in the flexible budget for September would be

closest to:

A.$1,947

B.$3,288

C.$3,340

D.$4,988

2) The times interest earned for Year 2 is closest to:

A.2.22

B.4.17

C.3.17

D.5.95

3) A soft drink bottler incurred the following factory utility cost: $3,936 for 800 cases

bottled and $3,988 for 900 cases bottled. Factory utility cost is a mixed cost containing

both fixed and variable components. The variable factory utility cost per case bottled is

closest to:

A) $4.92

B) $0.52

C) $4.43

D) $4.66

4) Baad Industries is a division of a major corporation. Last year the division had total

sales of $20,440,000, net operating income of $1,860,040, and average operating assets

of $7,000,000.

The division’s margin is closest to:

A.9.1%

B.34.2%

C.26.6%

D.43.3%

5) Wittels Corporation has provided the following data:

In Year 2, the company’s net operating income was $42,571, its net income before taxes

was $21,571, and its net income was $15,100. The company’s equity multiplier is

closest to:

A.1.14

B.0.53

C.0.88

D.1.87

6) Swagg Jewelry Corporation manufactures custom jewelry. In the past, Swagg has

been using a traditional overhead allocation system based solely on direct labor-hours.

Sensing that this system was distorting costs and selling prices, Swagg has decided to

switch to an activity-based costing system using three activity cost pools. Information

on these activity cost pools are as follows:

Job #309 incurred $900 of direct material, 30 hours of direct labor at $40 per hour, 80

machine hours, and 5 inspections.

Required:

a. What is the cost of the job under the activity-based costing system?

b. Relative to the activity-based costing system, would Job #309 have been overcosted

or undercosted under the traditional system and by how much?

7) The company’s times interest earned for Year 2 is closest to:

A.2.74

B.8.02

C.5.21

D.4.21

8) The finished goods inventory at the end of November after allocation of any

underapplied or overapplied manufacturing overhead for the month is closest to:

A.$53,864

B.$53,870

C.$52,856

D.$52,850

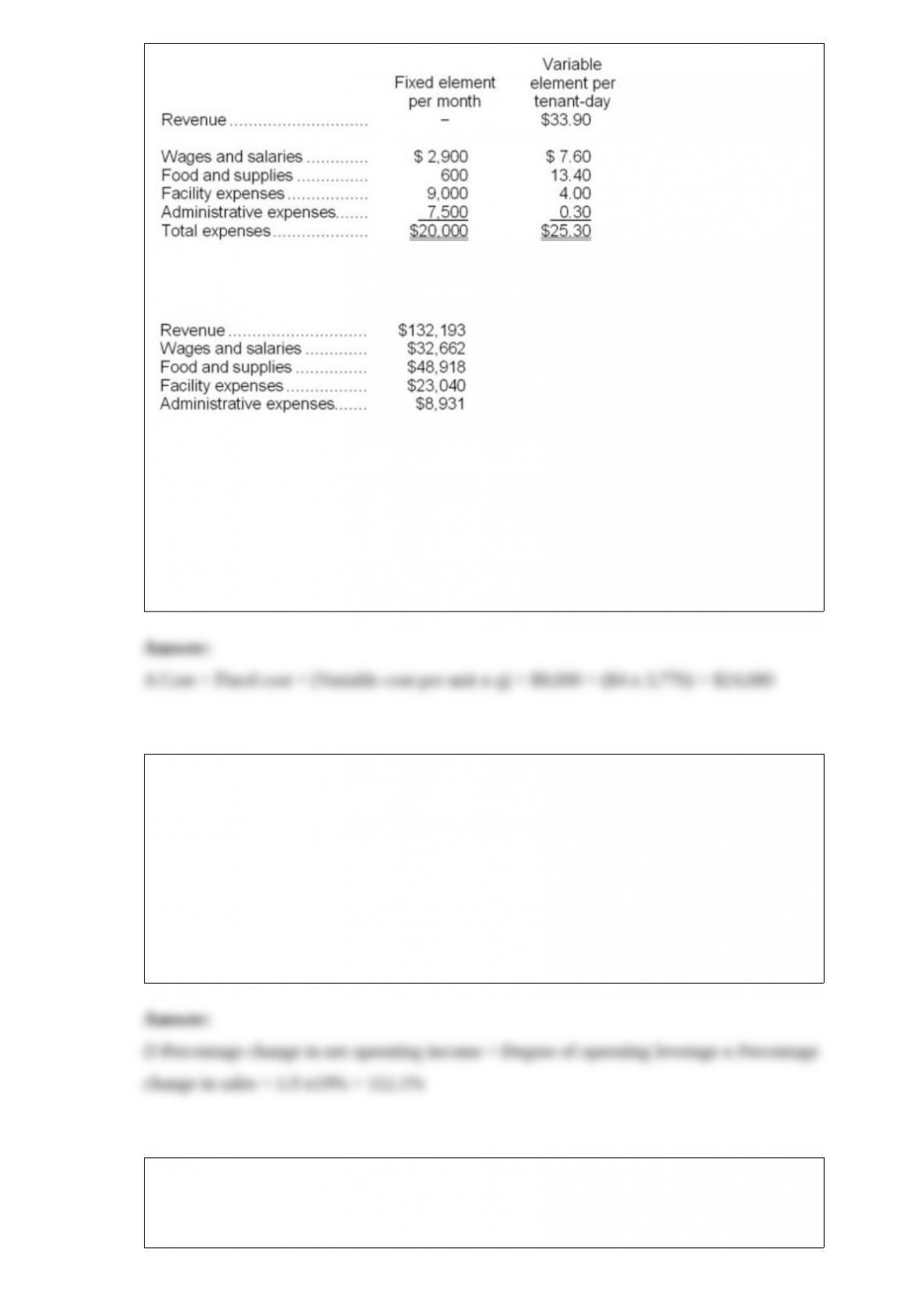

9) Juenemann Kennel uses tenant-days as its measure of activity; an animal housed in

the kennel for one day is counted as one tenant-day. During December, the kennel

budgeted for 3,800 tenant-days, but its actual level of activity was 3,770 tenant-days.

The kennel has provided the following data concerning the formulas used in its

budgeting and its actual results for December:

Data used in budgeting:

Actual results for December:

The facility expenses in the flexible budget for December would be closest to:

A.$24,080

B.$22,858

C.$23,223

D.$24,200

10) Cleckley Corporation’s operating leverage is 5.9. If the company’s sales increase by

19%, its net operating income should increase by about:

A.5.9%

B.31.1%

C.19.0%

D.112.1%

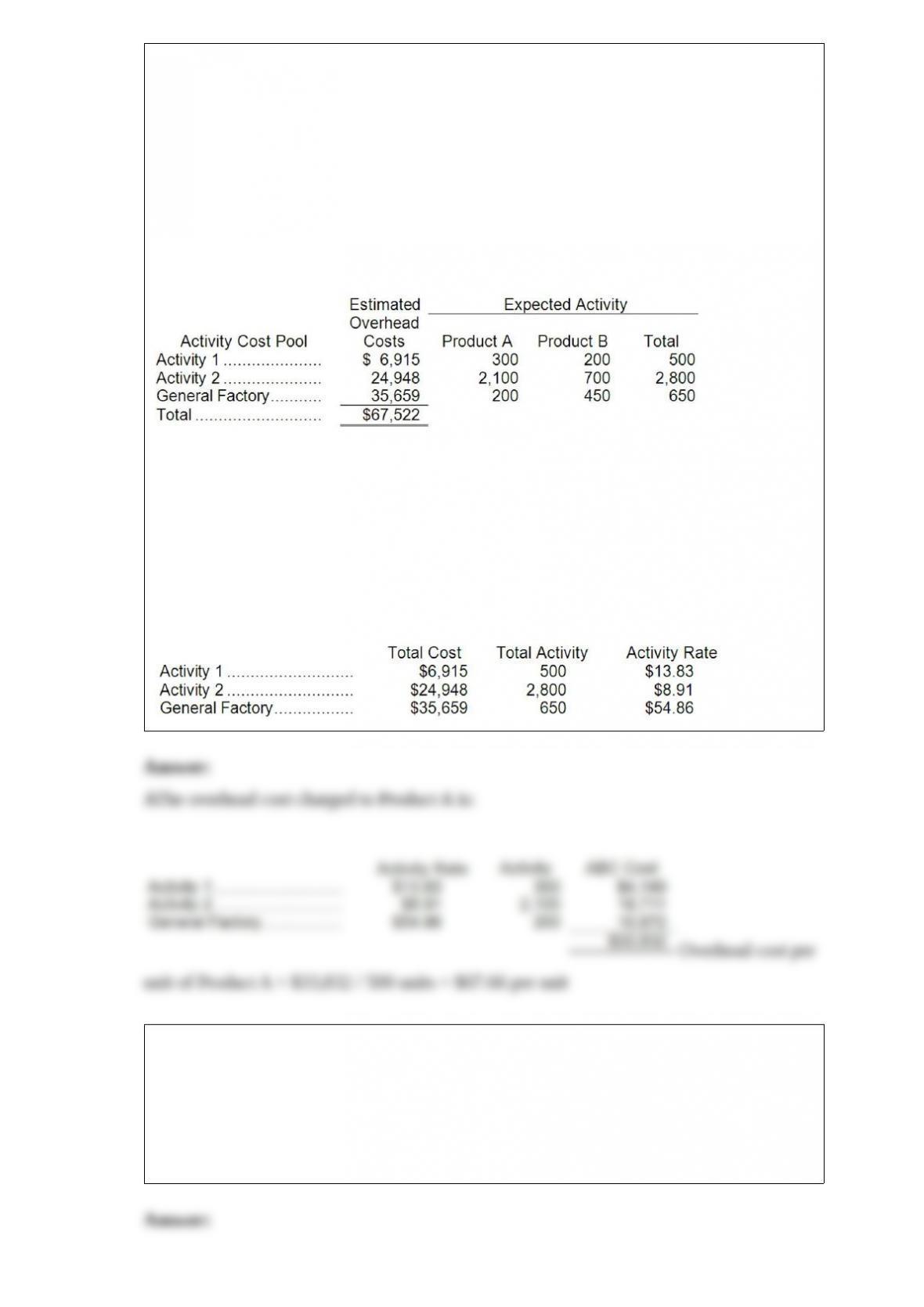

11) The overhead cost per unit of Product A under the activity-based costing system is

closest to:

Adams Corporation makes two products: Product A and Product B. Annual production

and sales are 500 units of Product A and 900 units of Product B. The company has

traditionally used direct labor-hours as the basis for applying all manufacturing

overhead to products. Product A requires 0.4 direct labor-hours per unit and Product B

requires 0.5 direct labor-hours per unit. The total estimated overhead for next period is

$67,522.

The company is considering switching to an activity-based costing system for the

purpose of computing unit product costs for external reports. The new activity-based

costing system would have three overhead activity cost pools–Activity 1, Activity 2,

and General Factory–with estimated overhead costs and expected activity as follows:

(Note: The General Factory activity cost pool’s costs are allocated on the basis of direct

labor-hours.)

A.$67.66

B.$21.94

C.$48.23

D.$41.55

The activity rates for each activity cost pool are computed as follows:

12) In July, Essinger Inc. incurred $72,000 of direct labor costs and $3,000 of indirect

labor costs. The journal entry to record the accrual of these wages would include a:

A.debit to Manufacturing Overhead of $3,000

B.credit to Manufacturing Overhead of $3,000

C.credit to Work in Process of $75,000

D.debit to Work in Process of $75,000

13) For planning, control, and decision-making purposes:

A) fixed costs should be converted to a per unit basis.

B) discretionary fixed costs should be eliminated.

C) variable costs should be ignored.

D) mixed costs should be separated into their variable and fixed components.

14) Bobe Air uses two measures of activity, flights and passengers, in the cost formulas

in its budgets and performance reports. The cost formula for plane operating costs is

$44,580 per month plus $2,390 per flight plus $8 per passenger. The company expected

its activity in May to be 68 flights and 211 passengers, but the actual activity was 71

flights and 210 passengers. The actual cost for plane operating costs in May was

$215,140.

The activity variance for plane operating costs in May would be closest to:

A.$6,352 F

B.$7,162 U

C.$7,162 F

D.$6,352 U

15) Baad Industries is a division of a major corporation. Last year the division had total

sales of $20,440,000, net operating income of $1,860,040, and average operating assets

of $7,000,000.

The division’s turnover is closest to:

A.0.27

B.2.92

C.10.99

D.2.31

16) Rogers Corporation is preparing its cash budget for July. The budgeted beginning

cash balance is $25,000. Budgeted cash receipts total $141,000 and budgeted cash

disbursements total $139,000. The desired ending cash balance is $30,000.

To attain its desired ending cash balance for July, the company should borrow:

A.$30,000

B.$0

C.$3,000

D.$57,000

17) At what purchase price for the wheels would Talbot be indifferent between making

or buying the wheels?

A) $1.70 per wheel

B) $1.60 per wheel

C) $1.55 per wheel

D) $1.15 per wheel