Interest expense is computed annually when a bond is issued for other than its face

value. For a bond issued at a discount, how will this component change as the bond

approaches maturity?

a. decrease

b. increase

c. remain constant

d. not enough information given to decide

Several terms which represent components of a bookkeeping system are listed below.

For each term, write a brief explanation of how that component is used in a

bookkeeping system. Space is provided for your answer immediately below each term.

A) Accounts B) Chart of Accounts C) Double-entry system with debits and credits D)

General Journal E) General Ledger F) Trial Balance

a. A liability resulting from the signing of a promissory note.

b. A measure of how long it takes to collect receivables.

c. A written promise to repay a definite sum of money on demand or at a fixed or

determinable date in the future.

d. The length of time a note is outstanding, that is, the period of time between the date it

is issued and the date it matures.

e. The party that will receive the money from a promissory note at some future date.

f. The process of selling a promissory note.

g. The date the promissory note is due.

h. The amount of cash the maker is to pay the payee on the maturity date of the note.

i. The difference between the principal amount of the note and its maturity value.

j. An asset resulting from the acceptance of a promissory note from another company.

k. Securities issued by corporations and governmental bodies as a form of borrowing.

l. Securities issued by corporations as a form of ownership in the business.

m. The party that agrees to repay the money for a promissory note at some future date.

n. The amount of cash received, or the fair value of the products or services received,

by the maker when a promissory note is issued.

Payee

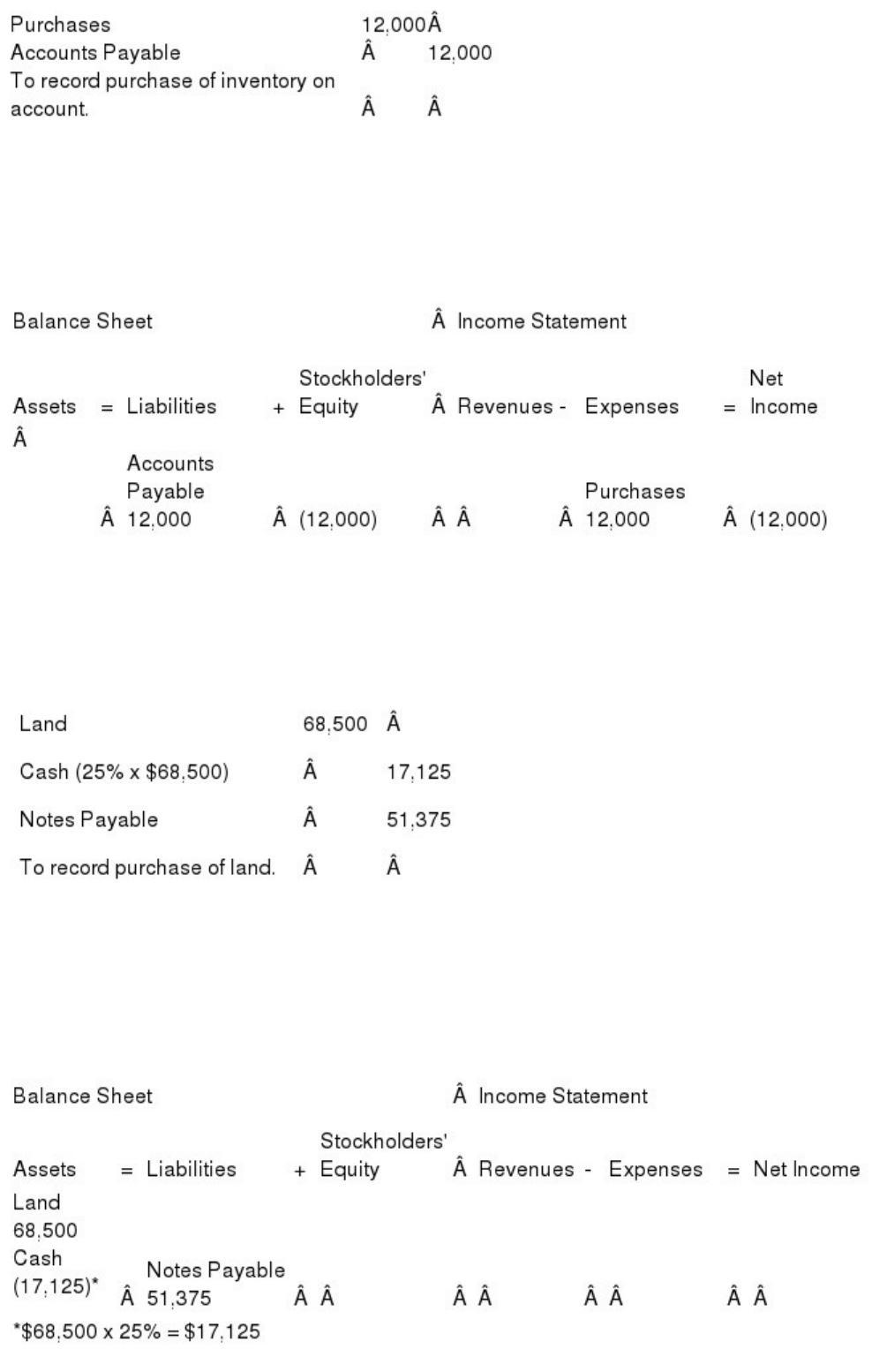

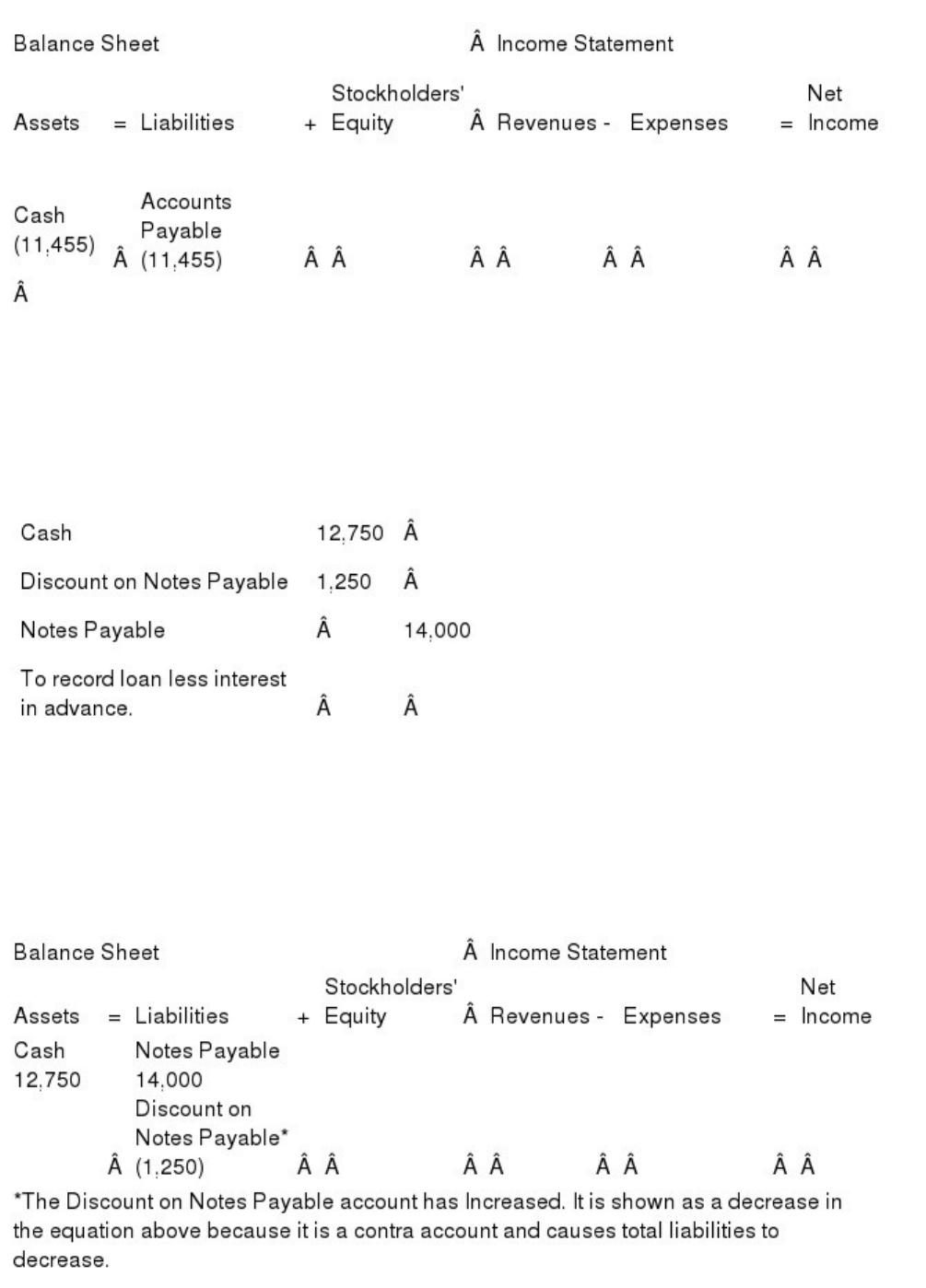

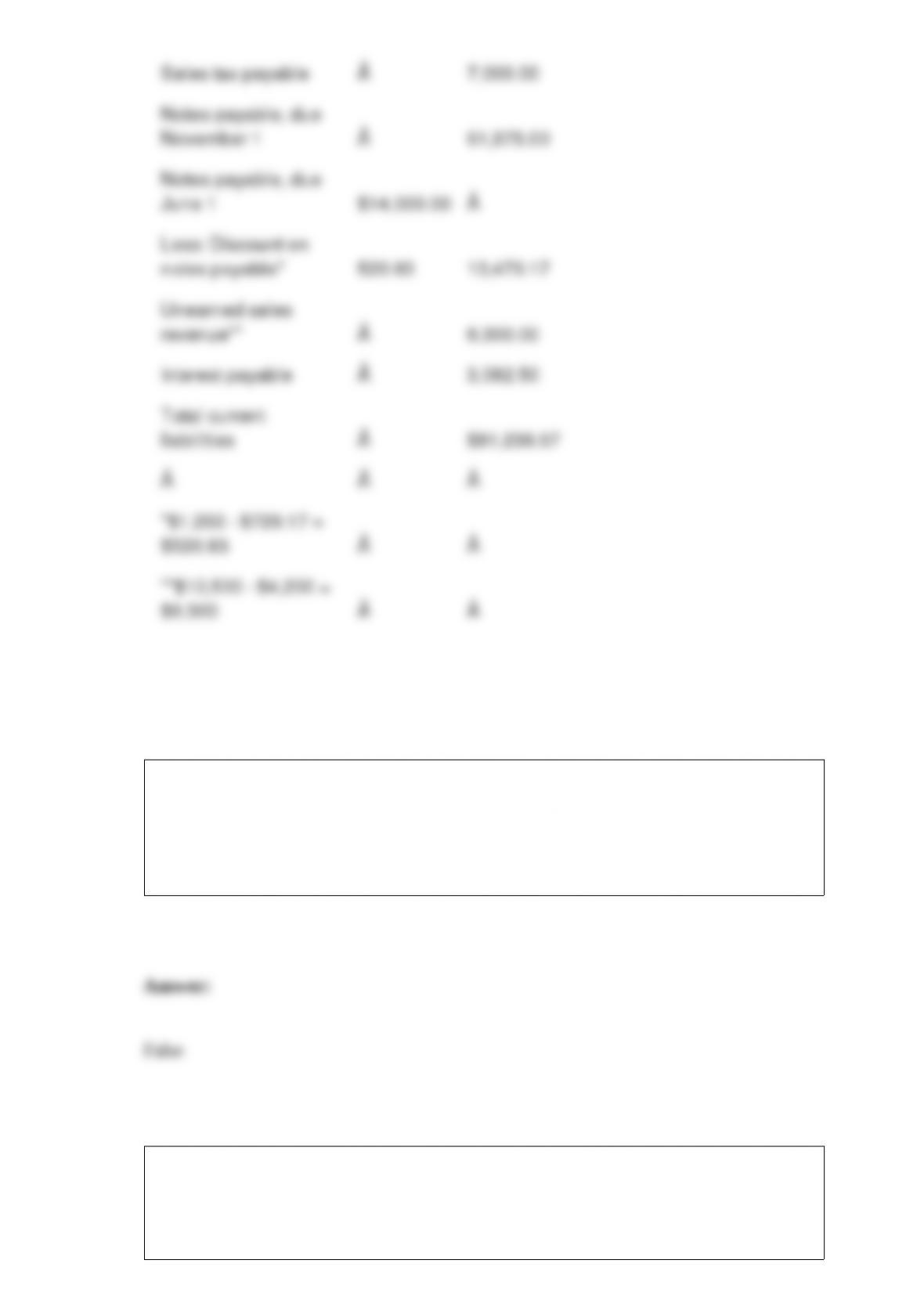

Newton Industries had the following transactions during the year: a. Newton purchased

inventory on account from a supplier for $12,000. Assume that Appleton uses a periodic

inventory system.

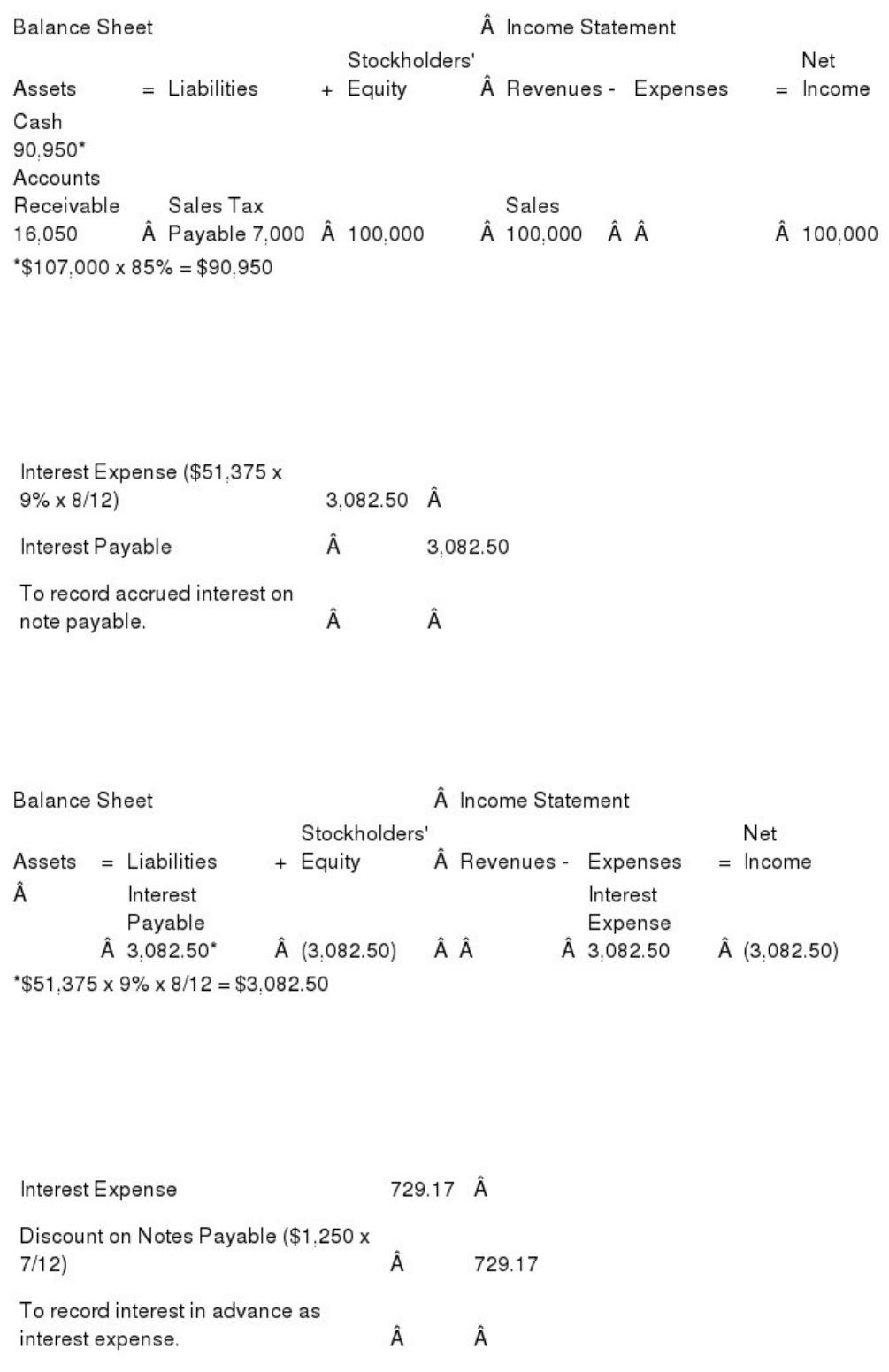

b. On May 1, land was purchased for $68,500. A 25% down payment was made, and an

18-month, 9% note was signed for the remainder.

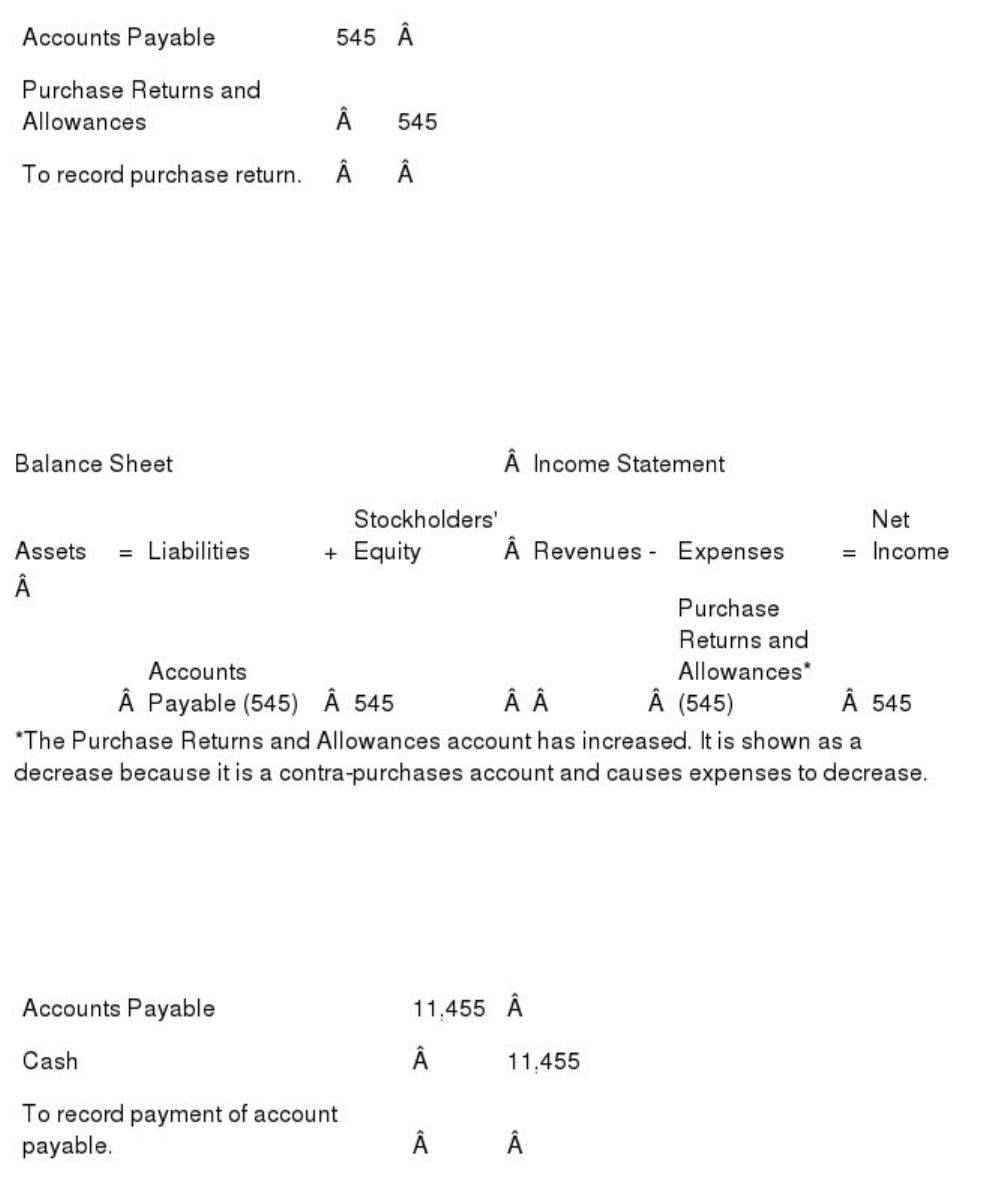

c. Newton returned $545 worth of inventory purchased in (a), which was found broken

when the inventory was received.

d. Newton paid the balance due on the purchase of inventory.

e. On June 1, Newton signed a one-year, $14,000 note to Plains State Bank and received

$12,750.

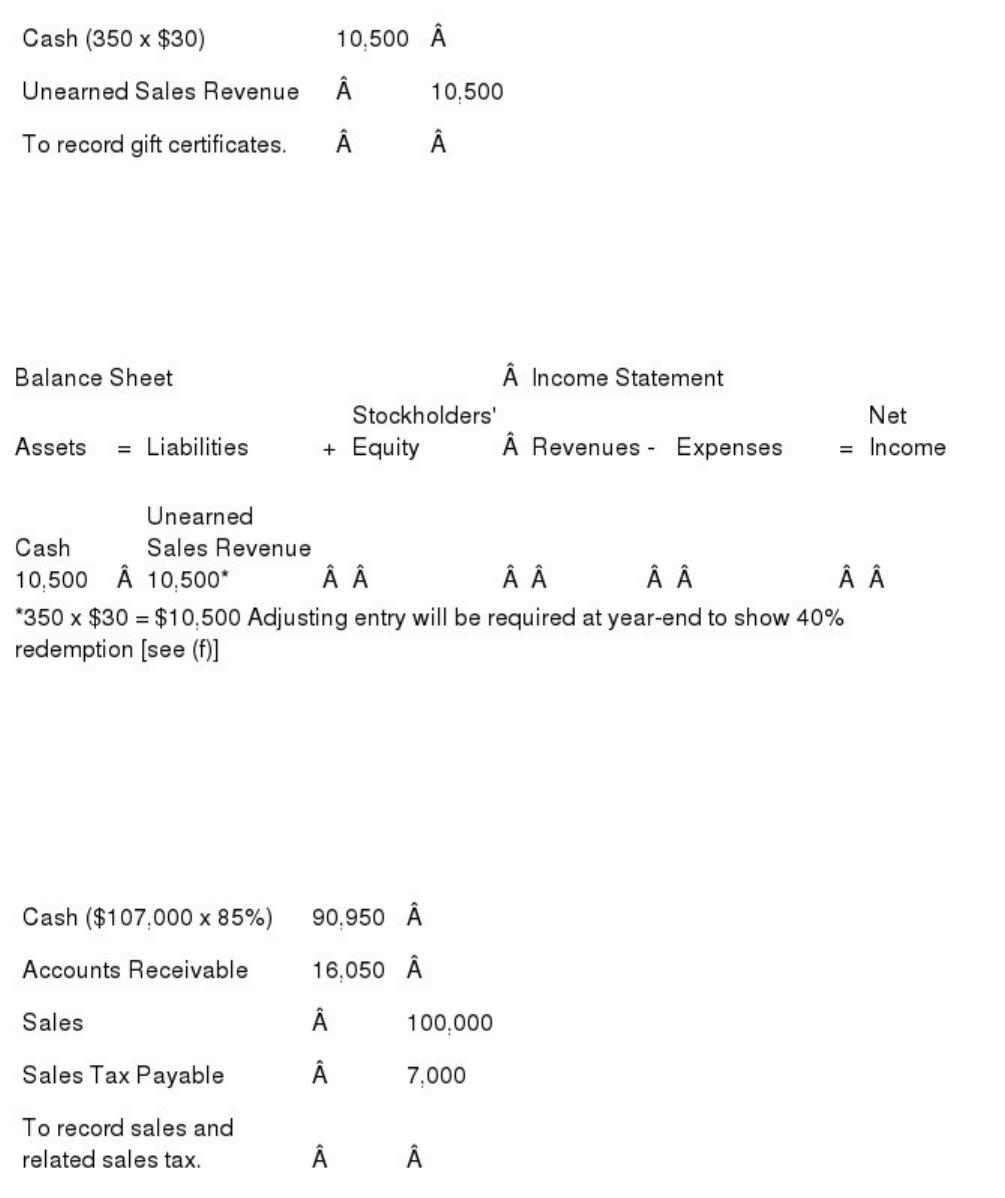

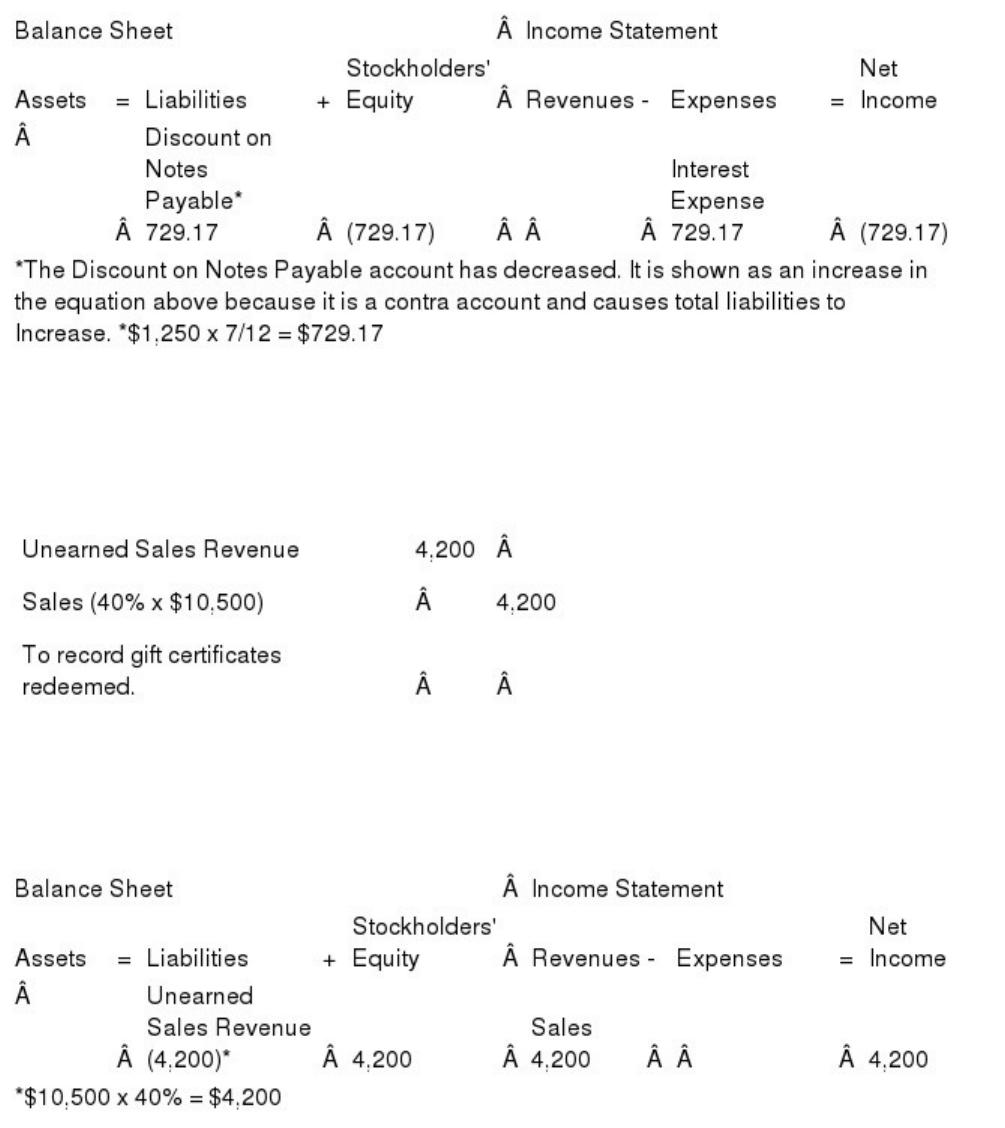

f. Newton sold 350 gift certificates for $30 each for cash. Sales of gift certificates are

recorded as a liability. At year-end, 40% of the gift certificates had been redeemed.

g. Sales for the year were $100,000, of which 85% were for cash. State sales tax of 7%

applied to all sales must be remitted to the state by January 31. REQUIRED:

1> Record all necessary journal entries relating to these transactions.

2> Assume that Newton’s accounting year ends on December 31. Prepare any necessary

adjusting journal entries.

3> What is the total of the current liabilities at the end of the year?

Adjustments are recorded for all transactions involving outside entities.

a. True

b. False

For each of the following sentences, select the phrase or group of words that best

completes the statement.

a. Earnings per share

b. Dividend yield ratio

c. Dividend payout ratio

d. Leverage

e. Return on assets ratio

f. Return on common stockholders’ equity ratio

g. Debt-to-equity ratio

h. Price/earnings ratio

The measure of a company’s success in earning a return for the common stockholders.

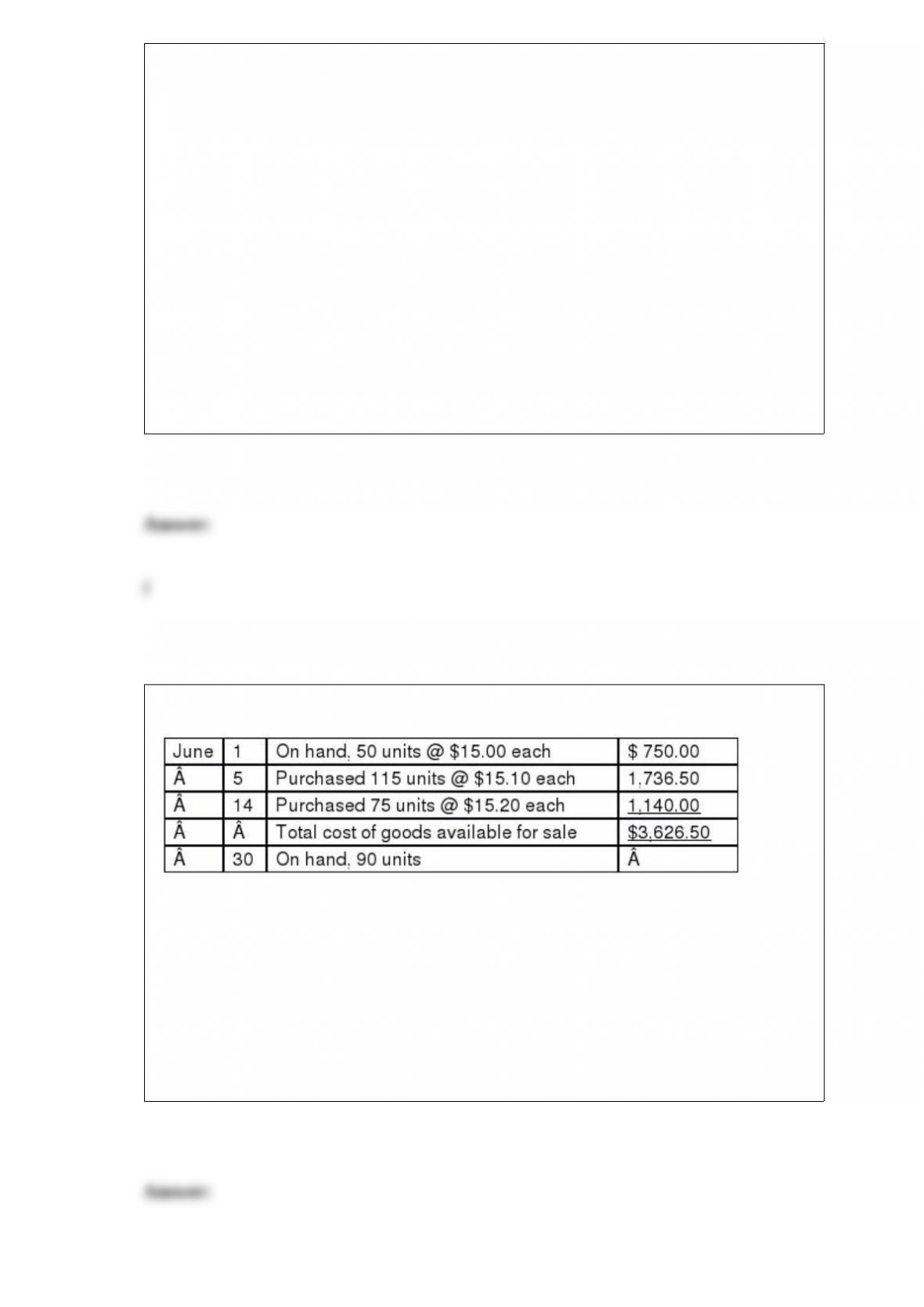

Eversoll Inc. uses the periodic inventory system.

How many units did Eversoll, Inc. sell during June?

a. 50

b. 90

c. 100

d. 150

Which of the following is considered a profitability ratio?

a. Earnings per share

b. Debt-to-equity ratio

c. Acid-test ratio

d. Inventory turnover ratio

Which of the following ratios is used to analyze a company’s liquidity?

a. Return on assets ratio

b. Inventory turnover ratio

c. Earnings per share

d. Asset turnover ratio

Crimson Corp. constructed equipment to manufacture a new line of home products

during 2015. The average balance of accumulated expenditures on the equipment

during September through December 2015 was $500,000. Construction started on

September 1, 2015 and was still in progress at the end of 2015. If Crimson borrowed

$500,000 for one year on September 1, 2015, to finance the construction, and the

interest rate on the construction loan was 6%, how much interest can Crimson capitalize

as part of the equipment cost for 2015?

a. $ -0-

b. $10,000

c. $20,000

d. $30,000

A source document is a record used to accumulate amounts for each individual asset,

liability, revenue, expense,

and component of stockholders’ equity.

a. True

b. False

Portland Sound Cafe began business on January 1, 2015. The corporate charter

authorized issuance of 1,000 shares of no-par value common stock, of which 200 shares

were issued, and 4,000 shares of $8 par value, 6% cumulative preferred stock, of which

none were issued. Portland Sound sold 400 shares of common stock at $8 per share on

May 1. The entry to record the issuance of the shares on May 1 will:

a. Increase Cash, $1,000; Increase Additional PaidÂin Capital-Common, $320;

Increase Common Stock, $680

b. Increase Cash, $3,200; Increase Additional PaidÂin Capital-Common, $2,800;

Increase Common Stock,

$400

c. Increase Cash, $4,800; Increase Common Stock, $4,800

d. Increase Cash, $3,200; Increase Common Stock, $3,200

A partnership can be owned by one or more entities or individuals.

a. True

b. False

Deferred tax is an amount that reconciles the differences between the income for

financial purposes with the income reported for tax purposes. In most cases, it is a

long-term liability.

a. True

b. False

Clarke Shop purchased supplies at a cost of $18,000 during 2015. At January 1, 2015,

the beginning balance in the supplies account was $1,000. For 2015, supplies expense

was $16,000. How much “Supplies” are on hand as of December 31, 2015?

a. $ 1,000

b. $ 3,000

c. $16,000

d. $17,000

The Securities and Exchange Commission (SEC) is concerned with

a. All companies in the United States regardless of size.

b. Companies that issue securities to the general public.

c. Accounting reports issued by government entities.

d. All domestic and international companies that issue accounting reports.