What do the following classes of ratios measure?

(a) Liquidity ratios.

(b) Profitability ratios.

(c) Solvency ratios.

Answer:

At April 30, Yaddof Company has the following bank information: cash balance per

bank $2,300; outstanding checks $390; deposits in transit $275; credit memo for

interest $50; bank service charge $10. What is Mareska’s adjusted cash balance on April

30?

a. $2,185

b. $2,245

c. $2,300

d. $2,340

Answer:

Santayana Company purchased a machine on January 1, 2013, for $60,000 with an

estimated salvage value of $15,000 and an estimated useful life of 8 years. On January

1, 2015, Santayana decides the machine will last 12 years from the date of purchase.

The salvage value is still estimated at $15,000. Using the straight-line method, the new

annual depreciation will be

a. $3,375.

b. $3,750.

c. $4,500.

d. $5,000.

Answer:

Fat Possum’s Service Shop started the year with total assets of $330,000 and total

liabilities of $2400,000. During the year, the business recorded $630,000 in revenues,

$420,000 in expenses, and paid dividends of $60,000.

The net income reported by Fat Possum’s Service Shop for the year was

a. $150,000.

b. $210,000.

c. $240,000.

d. $270,000.

Answer:

Given the following information, compute the amount of cash finally remitted by the

customer.

Oct. 22’”Sale on credit, terms of 2/10, n/30’”$6,000

Oct. 27’”Allowance granted due to some items being damaged’”$600

Oct. 31’”Payment in full received from customer’”$?

a. $5,292.

b. $6,000.

c. $5,280.

d. $5,628.

Answer:

Identify the following expenditures as capital expenditures or revenue expenditures.

(a) Replacement of worn out gears on factory machinery.

(b) Construction of a new wing on an office building.

(c) Painting the exterior of a building.

(d) Oil change on a company truck.

(e) Painting and lettering of a used truck upon acquisition of the truck.

(f) Overhaul of a truck motor. One year extension in useful life is expected.

(g) Purchased a wastebasket at a cost of $10.

Answer:

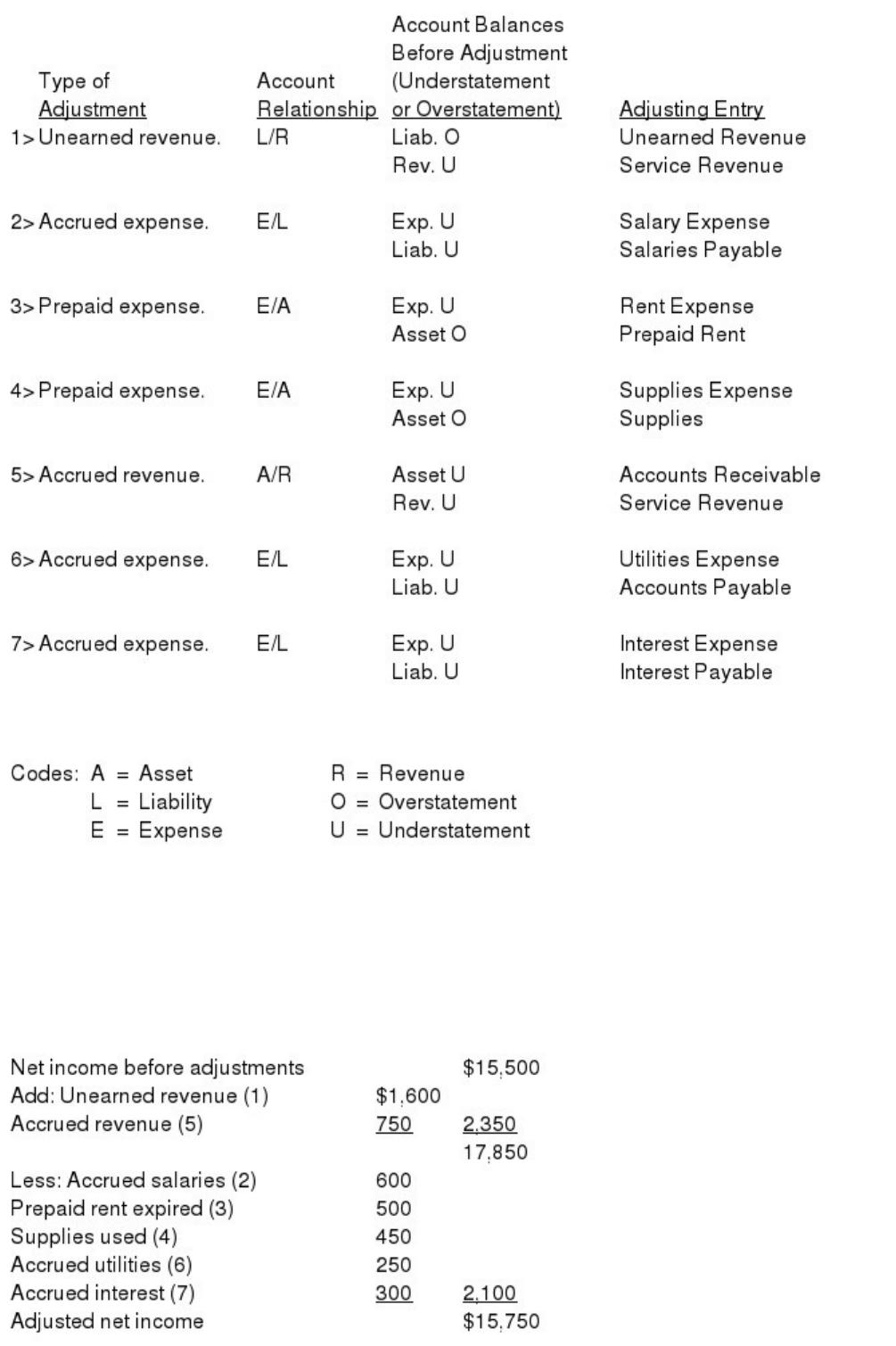

Buena Vista Social Club accumulates the following adjustment data at December 31.

1> Revenue of $1,600 collected in advance has been recognized.

2> Salaries of $600 are unpaid.

3> Prepaid rent totaling $500 has expired.

4> Supplies of $450 have been used.

5> Revenue recognized but unbilled total $750.

6> Utility expenses of $250 are unpaid.

7> Interest of $300 has accrued on a note payable.

Instructions

(a) For each of the above items indicate:

1> The type of adjustment (prepaid expense, unearned revenue, accrued revenue, or

accrued expense).

2> The account relationship (asset/liability, liability/revenue, etc.).

3> The status of account balances before adjustment (understatement or overstatement).

4> The adjusting entry.

(b) Assume net income before the adjustments listed above was $15,500. What is the

adjusted net income?

Prepare your answer in the tabular form presented below.

Account Balances

Before Adjustment

Type of Account (Understatement

Adjustment Relationship or Overstatement) Adjusting Entry

Answer:

On July 1, 2015, Hale Kennels sells equipment for $220,000. The equipment originally

cost $600,000, had an estimated 5-year life and an expected salvage value of $100,000.

The accumulated depreciation account had a balance of $350,000 on January 1, 2015,

using the straight-line method. The gain or loss on disposal is

a. $30,000 gain.

b. $20,000 loss.

c. $30,000 loss.

d. $20,000 gain.

Answer:

IFRS allows companies to revalue plant assets to fair value. Which of the following

statements is true regarding revaluation?

a. At the time a company purchases an asset it must decide whether to follow

revaluation procedures for the asset; once the election is made, it must be followed for

the remainder of the asset’s useful life.

b. Assets that are experiencing rapid price changes must be revalued quarterly, other

assets can be revalued on an annual basis.

c. The journal entry to record a revaluation when the asset’s price has increased includes

a credit to the account revaluation surplus.

d. All of the choices are correct regarding revaluation of plant assets.

IFRS:

Answer:

If the board of directors authorizes a $100,000 restriction of retained earnings for a

future plant expansion, the effect of this action is to

a. decrease total assets and total stockholders’ equity.

b. increase stockholders’ equity and decrease total liabilities.

c. decrease total retained earnings and increase total liabilities.

d. reduce the amount of retained earnings available for dividend declarations.

Answer:

Which of the following steps in the accounting cycle may be performed most

frequently?

a. Prepare a post-closing trial balance

b. Journalize closing entries

c. Post closing entries

d. Prepare a trial balance

Answer:

Powell’s Courier Service recorded a loss of $9,000 when it sold a van that originally

cost $84,000 for $15,000. Accumulated depreciation on the van must have been

a. $78,000.

b. $24,000.

c. $75,000.

d. $60,000.

Answer:

Evidence that would not help with determining the effects of a transaction on the

accounts would be a(n)

a. cash register sales tape.

b. bill.

c. advertising brochure.

d. check.

Answer:

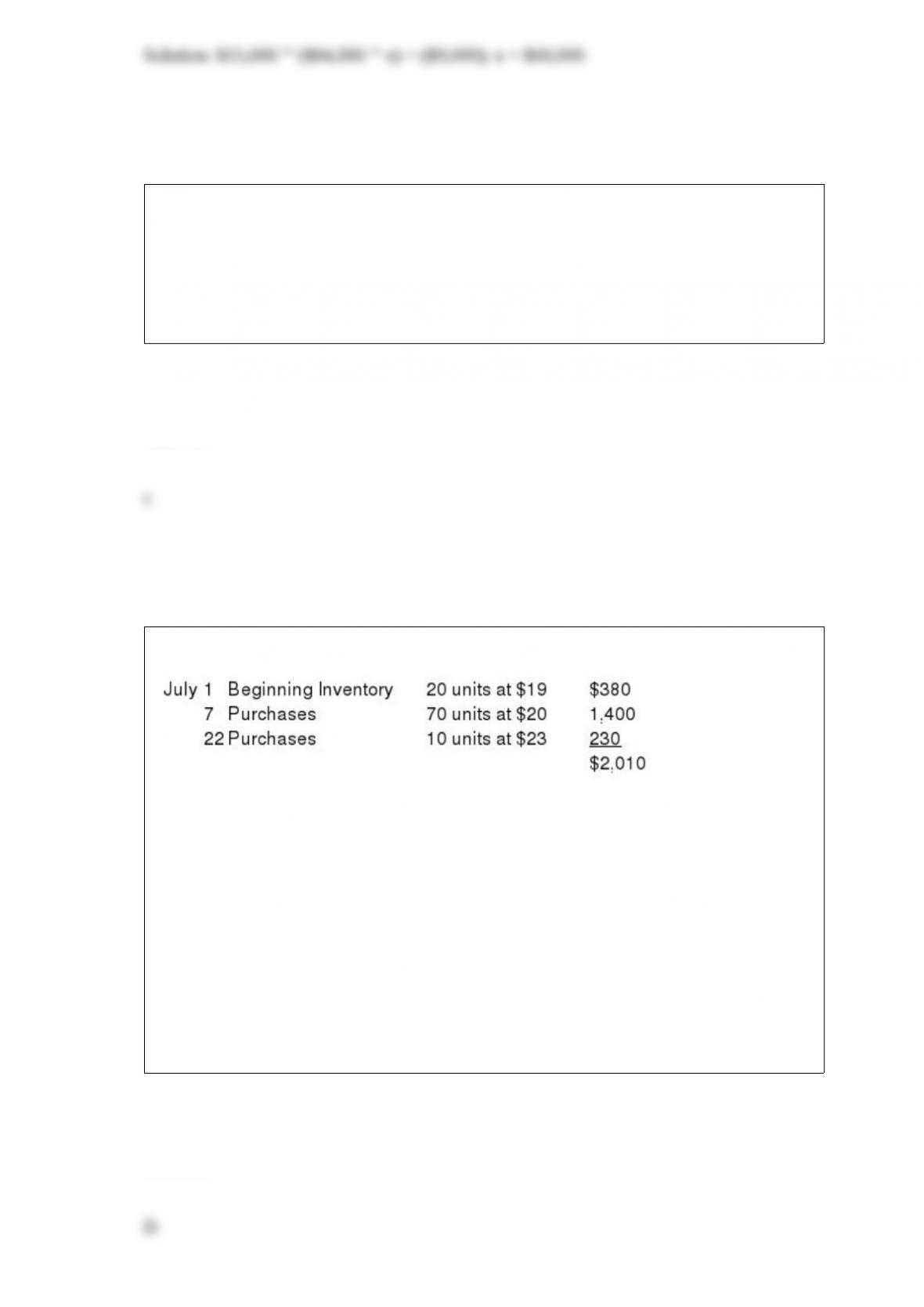

Priscilla has the following inventory information.

A physical count of merchandise inventory on July 31 reveals that there are 35 units on

hand. Using the LIFO inventory method, the amount allocated to cost of goods sold for

July is

a. $1,280.

b. $1,287.

c. $1,306.

d. $1,330.

Answer:

The following information pertains to Ortiz Company. Assume that all balance sheet

amounts represent both average and ending balance figures. Assume that all sales were

on credit.

What is the accounts receivable turnover for Ortiz?

a. 1.3 times

b. 1.1 times

c. 2.8 times

d. 12.7 times

Answer:

During 2015, Morlan Company had an asset turnover of four times with sales totaling

$1,000,000. If net income was $60,000, Morlan Company’s return on assets in 2015

was

a. 6%.

b. 24%.

c. 30%.

d. 60%.

Answer:

Bacon Corporation began business by issuing 180,000 shares of $5 par value common

stock for $25 per share. During its first year, the corporation sustained a net loss of

$30,000. The year-end balance sheet would show

a. Common stock of $900,000.

b. Common stock of $4,500,000.

c. Total paid-in capital of $4,470,000.

d. Total paid-in capital of $930,000.

Answer:

A perpetual inventory system would likely be used by a(n)

a. automobile dealership.

b. hardware store.

c. drugstore.

d. convenience store.

Answer:

Generally, convertible bonds do not pay interest.

Answer:

Karley Company sold equipment on July 1, 2015 for $75,000. The equipment had cost

$210,000 and had $120,000 of accumulated depreciation as of January 1, 2015.

Depreciation for the first 6 months of 2015 was $12,000.

Instructions

Prepare the journal entry to record the sale of the equipment.

Answer:

If the proceeds from the sale of a plant asset exceed its ______________, a gain on

disposal will occur.

Answer:

When the volume of transactions is large, recording them in tabular form is more

efficient than using journals and ledgers.

Answer:

A statement of cash flows should help investors and creditors assess the entity’s ability

to generate future income.

Answer:

A fellow classmate is confused about how debits and credits relate to the basic

accounting equation. State the basic accounting equation, convert it into the expanded

accounting equation, and then explain how it ties into the rules for debits and credits.

Answer:

Transaction and adjustment data for Doty Company for the calendar year end is as

follows:

1> December 24 [initial salary entry): $12,000 of salaries earned between December 1

and December 24 are paid.

2> December 31 [adjusting entry): Salaries earned between December 25 and

December 31 are $3,000. These will be paid in the January 8 payroll.

3> January 8 [subsequent salary entry): Total salary payroll amounting to $8,000 was

paid.

Instructions

Prepare two sets of journal entries as specified below. The first set of journal entries

should assume that the company does not use reversing entries, and the second set

should assume that reversing entries are utilized by the company.

Assume no reversing entries Assume reversing entries

[a] Initial Salary Entry

Dec. 24

[b] Adjusting Entry

Dec. 31

[c] Closing Entry

Dec. 31

[d] Reversing Entry

Jan. 1

[e) Subsequent Salary Entry

Jan. 8

Answer:

The employer incurs a payroll tax expense equal to the amount contributed by each

employee for ______________ taxes.

Answer:

Both correcting entries and adjusting entries always affect at least one balance sheet

account and one income statement account.

Answer:

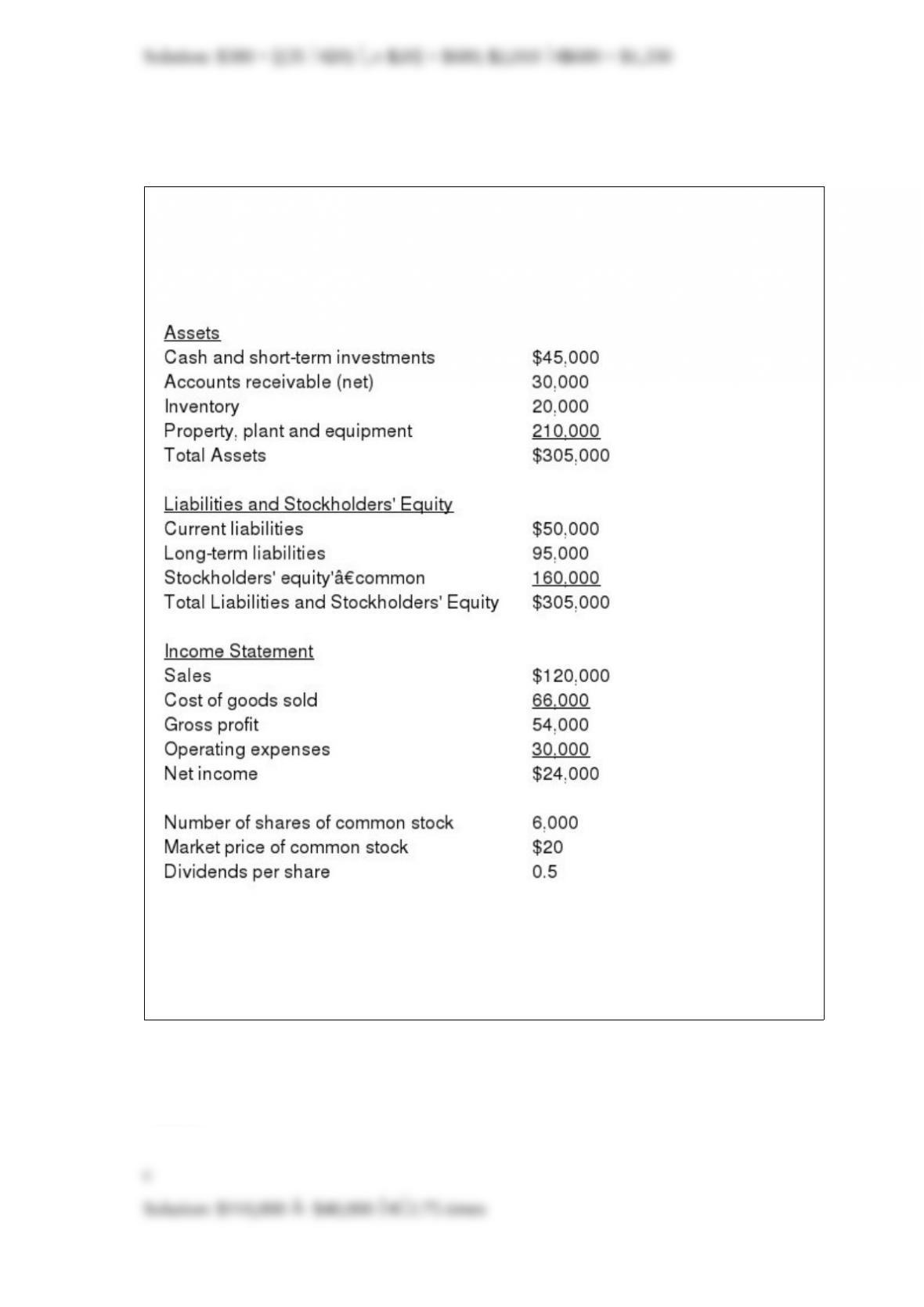

The following items were taken from the financial statements Wyatt Company. [All

dollars re in thousands.)

2015 net income was 1,000 and dividends paid were $700.

Instructions

Prepare a classified balance sheet in good form as of December 31, 2015.

Answer: