When performing substantive tests using sampling methods, the auditor’s main concern

is the risk of incorrect rejection.

The deep pocket theory represents a misunderstanding whereby shareholders

mistakenly believe that they are entitled to recover losses on investments for which the

auditor provided an unqualified opinion on the financial statements.

The individual auditable elements defined by the auditor are the sampling units.

Any major disagreement the auditor has with management should be discussed with the

audit committee.

Auditors are responsible to fraud even if it has an immaterial effect on the financial

statements.

Random sampling can be used to determine sample size or evaluate sampling results

even if the auditor does not plan on using statistical sampling.

Auditing is the process of verifying the accuracy of the financial statements.

Negative assurance infers that nothing has come to the reviewer’s attention that requires

change.

If an omission of an important audit procedure is discovered, the auditor should

immediately issue a disclaimer of opinion for the audit.

Planning is not required in an audit as long as an audit program has been developed.

The Public Company Accounting Oversight Board obtains its authority to set audit

standards for public companies from the U.S. Congress.

The auditor generally reports things that management could do better in a management

letteras a constructive part of the audit.

Auditor needs to assess disclosures about what lines of business the company may

discontinue.

Management may feel pressure to maintain debt covenants, which is a deterrent to

fraud.

Control risk refers to the risk that a misstatement could occur in an assertion about a

class of transaction, account balance, or disclosure and that could be material, either

individually or when aggregated with other misstatements, will not be prevented, or

detected and corrected, on a timely basis by the entity’s internal control.

The significant judgments related to debt depend on specific accounting rules (U.S. or

international) that the company is following.

For proper control, the receiving department should receive a copy of the purchase

order that has the quantities blanked out.

Complex transactions such as derivative instruments provide management certain

opportunities to manipulate financial statements to its advantage.

The auditor is only concerned about the aggregate internal control deficiencies when

determining the appropriate opinion on internal control over financial reporting (ICFR).

An auditor must have a good understanding of the risks associated with a client’s

industry in order to ensure that the financial statements reflect the underlying substance

of accounting transactions and the economic effects of such transactions.

Bondholders are one of the users of financial statements.

Auditors of public companies need not adhere to the requirements of statutory or

regulatory organizations.

An auditor would test control over the objective of the occurrence of sales transactions

by sampling recorded revenues and tracing them back to invoices and shipping

documents.

An auditor’s consideration of materiality is a matter of professional judgment and is

influenced by the auditor’s perception of the needs of users of financial statements.

Auditors need to consider fraud arising from misappropriation of assets and fraudulent

financial reporting.

Analytical review of related expense accounts when auditing accounts payable would

be used when control risk is assessed as low.

In order to gain an understanding of internal controls, an auditor will use walkthrough

of the process, inquiry, observation, and review of the client’s documentation.

An auditor uses sampling to determine the reasonableness of an account balance by

performing detailed analysis of the selected items making up the account balance.

An audit firm culture that emphasizes “doing the right thing,” encourages auditors to

deal with difficult issues in a short period of time.

When planning the audit procedures related to long-lived assets, the auditor is required

to perform preliminary analytical procedures.

Internal controls are implemented in order to give perpetrators the impression that the

risk of being caught is low.

Independence of the internal audit function is obtained by giving the Chief Audit

Executive (CAE) unrestricted access to the board and senior management.

Testing internal control for effectiveness is done in every audit.

The purpose of the audit program is to list the audit procedures to be followed in

gathering audit evidence and to help those in charge of the audit to monitor the progress

and supervise the work.

Which of the following facts would result in an auditor issuing an adverse report over

internal control?

A.The controls are believed to be effective.

B.The tests of controls support the documented understanding of controls.

C.There is a material weakness in the design or operation of controls.

D.A confirmation is not returned by a customer timely.

What is the nature of the relationship between risk of material misstatement and audit

risk?

A.Direct.

B.None.

C.Correlational.

D.Inverse.

Rule 201 deals with the General Standards that are applicable to all CPAs no matter the

type of services that are rendered does not include which of the following factors?

A.Due professional care.

B.Integrity and objectivity.

C.Planning and supervision.

D.Sufficient relevant data.

Which of the following is not included in the scope of services performed in internal

auditing by a CIA?

A.Assurance and consulting.

B.Operations analysis.

C.Operational efficiency reviews.

D.Internal control analysis.

E.They are all included in the scope of services.

Adverse opinions can only be issued by auditors based on which of the following?

A.Violations of GAAP.

B.Scope limitations.

C.Going concern.

D.Lack of independence.

E.Either B or D.

Which of the following audit procedures does not address the rights, presentation and

disclosure assertion for pledged, discounted, assigned, and related-party accounts

receivable?

A.Review work performed in other audit areas.

B.Inquire of management.

C.Review adequacy of allowance for doubtful accounts.

D.Review loan agreements.

Which of the following statements is false regarding reporting on sustainability

activities and outcomes?

A.Investor interest, socially responsible investment funds, and the Dow Jones

Sustainability Index have increased demand for these sustainability disclosures.

B.Specific sustainability disclosures that companies make vary little from company to

company.

C.Many corporate websites now include sustainability reports, and the placement on

those websites is usually quite prominent.

D.Regarding sustainability, companies determine what to report and how to report it by

using various available guidelines, the most prominent of which is the Global Reporting

Initiative (GRI) G3 Reporting Framework.

When responding to the auditor as a result of the audit client’s letter of inquiry, how

might the attorney limit the response?

A.Limit the response to litigations in process.

B.Limit the response to asserted claims.

C.Limit the response to matters to which the attorney has given substantive attention in

the form of legal consultation or representation.

D.Limit the response to items which the attorney believes will result in loss to the

client.

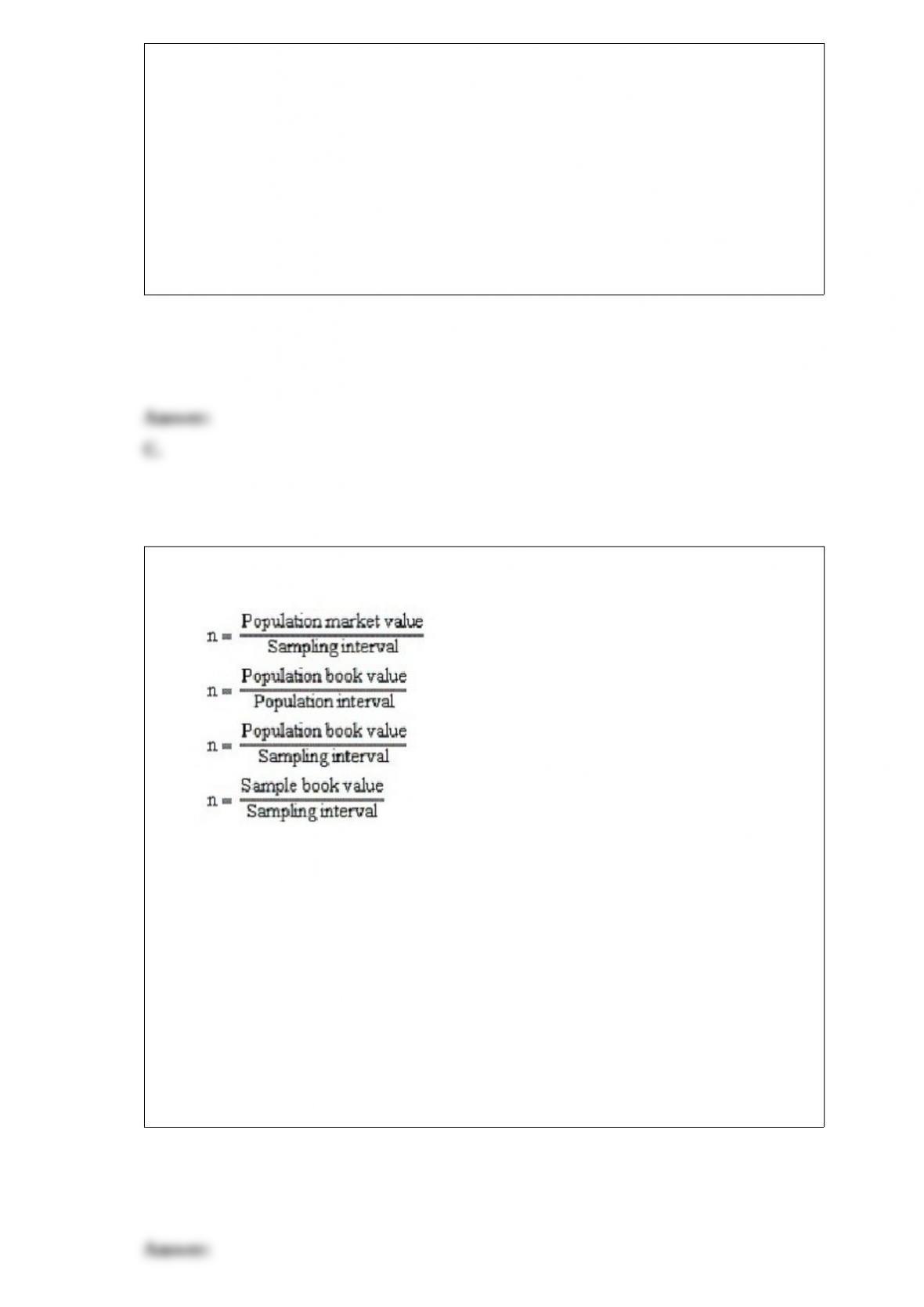

In using MUS, once the auditor has determined the sample size, which of the following

is needed to determine the sampling interval?

A.Expected misstatement.

B.Tolerable misstatement.

C.Population size.

D.Mean.

Which of the following long-lived assets presents the most difficult in determining its

cost?

A.Equipment.

B.Inventory.

C.Patent.

D.All the above are equally difficult in determining cost.

Which of the following is false regarding the management letter?

A.The management letter is not required

B.The management letter is the same as the management representation letter.

C.The management letter helps to provide management comfort that the auditor has

done a quality job.

D.The management letter helps provide management with information that the auditor

knows and understands the client’s business.

Which of the following actions is not a potential fraud scheme related to long-lived

assets?

A.Impairment losses on long-lived assets are not recognized.

B.Costs that should have been expenses are improperly capitalized.

C.Amortization of intangible assets is miscalculated.

D.All the above are potential fraud schemes.

The date of the audit opinion of Upton Industries, Inc. reads: March 7, 2014 except for

Note D, as to which the date is March 12, 2014. What is this an example of?

A.Improper reporting.

B.A GAAP violation.

C.Dual dating.

D.A contingent event.

Which one of the following groups is interested in an organization’s control structure?

A.Board members.

B.Lenders.

C.Auditors.

D.All of the above.

Which of the following is not a reason why the auditor needs to take special care to

review significant estimates in the financial statements?

A.Organizations may try to use the estimates to ‘smooth” earnings.

B.Organizations may create hidden reserves in unusually good years that can be used in

years when real profits do not meet expectations.

C.Companies may underestimate liabilities or impairment of asset values to achieve

reported earning goals in years when real profits to not meet expectations.

D.Companies may try to overestimate liabilities in computing leverage ratios.

When an accountant is asked to compile financial statements that omit substantially all

of the required disclosures, which of the following actions is appropriate?

A.The CPA cannot accept the engagement.

B.The CPA may accept the engagement.

C.The CPA may accept the engagement if the CPA believes the omission is not

undertaken to mislead users.

D.The CPA must express an adverse opinion.

Which of the following would be a reason that industry and client data were not directly

comparable?

A.Broad industry.

B.Use of different accounting principles.

C.Neither of the above.

D.Both A & B are correct.

Which of the following is not a typical analytical procedure for the completion of the

audit?

A.Ratio analysis.

B.Common-size analysis.

C.Changes from the prior year.

D.All of the above would typically be used.

How many auditing standards has the PCAOB issued?

A.7.

B.16.

C.22.

D.5.

Sufficient evidence gathered by the auditor involves which of the following?

A.The quantity of evidence to be obtained.

B.The type of evidence to be obtained.

C.Obtaining limited evidence to achieve efficiency.

D.The use of an audit program to obtain evidence.

If substantial doubt remains about going concern for a client at the end of the audit, then

which of the following reports should the auditor typically issue?

A.Issue an unqualified audit report.

B.Issue an unqualified audit report with an explanatory paragraph.

C.Issue a qualified report.

D.Issue an adverse report.

If conclusion is drawn that there may be a going concern problem, which of the

following should the auditor do?

A.Withdraw from the engagement.

B.Issue a qualified or adverse opinion.

C.Identify and assess management’s plan to overcome the problem.

D.Communicate this fact with management that is one level above the controller.

Which of the following types of software would the auditor use to foot the property

ledger, agree the property ledger to the general ledger, take a sample of items contained

in the property ledger, and recalculate depreciation for the items chosen?

A.Specified Audit Software (SAS).

B.Generalized Audit Software (GAS).

C.Reporting Audit Software (RAS).

D.Property Ledger Audit Software (PLAS).

When auditing marketable securities, the auditor will do which of the following?

A.Examine broker’s advices evidencing purchase of securities.

B.Recompute income.

C.Foot schedule.

D.Both A and B.

E.All of the above.

Which of the following is a use of audit documentation?

A.Assisting the engagement team in planning and performing the audit.

B.Assisting members of the engagement team responsible for supervising and

reviewing the audit work.

C.Retaining a record of matters of continuing significance to future audits of the same

organization.

D.All of the above.

Which of the following creates an opportunity for fraud to be committed in an

organization?

A.Management demands financial success.

B.Poor internal control.

C.Commitments tied to debt covenants.

D.Management is aggressive in its application of accounting rules.

An auditor who is professionally skeptical will do which of the following?

A.Critically question contradictory audit evidence..\

B.Carefully evaluate the reliability of audit evidence, especially in situations in which

fraud risk is high.

C.Reasonably question the authenticity of documentation, while accepting that

documents are to be considered genuine unless there is reason to believe the contrary.

D.All of the above.

Which one of the following does not constitute probable relationships between

accounts?

A.Equipment and depreciation.

B.Patent and amortization.

C.Assets under capital leases and amortization.

D.Oil reserves and depreciation.

Which of the following is not an indicator of a potential going-concern problem?

A.Negative trends in profitability.

B.External matters increasing regulatory requirements.

C.Significant changes in competition.

D.An Altman Z-score above 3.0.

Which of the following statements is not true regarding the use of a judgmental

approach by auditors in determining whether a misstatement is clearly trivial?

A.The determination is based on past auditor experience.

B.The determination is usually not very defensible to third-party users.

C.The determination is usually not very defensible to regulators.

D.The determination uses percentages for the likelihood of misstatement.

Identify and briefly describe the two principles that should govern the monitoring

function.

The fourth internal control principles requires organizations demonstrate a commitment

to attract, develop, and retain competent individuals in alignment with objectives.

Discuss how this can be done?

Discuss how each of the following procedures could be used in the audit of fixed assets,

e.g., various types of equipment used in the business.

Explain why monetary unit sampling is not useful for detecting understatements

After assessing internal control weakness the auditor develops audit procedures to

explicitly test for the existence of the types of fraud or misstatement that could occur

because of the weakness. In the linkage process from control deficiencies to audit

procedures, what are the four questions involved in linking changes to the audit

program?

Why is there a demand for independent assurance on sustainability reporting? Describe

the features of external assurance over sustainability provided in the Global Reporting

Initiative Reporting Framework.

Identify at least five steps involved in an audit.

The Auditing Standards Board established guidelines to assist auditors in evaluating the

reliability of audit evidence. Discuss the criteria for the more reliable types of evidence

and include an example for each.

List the common substantive procedures used to address the risks relating to fraud in

investments:

What are the steps of the brainstorming process?

When auditing a manufacturing concern, what major inquiries might be made by the

auditor about the cost accounting system?

In the financial statements, there are many risks associated with an audit that must be

considered. Identify and discuss five separate risks that may exist related to accounts

receivable.

Why is the appropriateness of audit evidence obtained by the auditor important in

forming an audit opinion? Describe the qualities information should have to be

considered appropriate by the auditor.

What are the steps in management’s evaluation of internal control over financial

reporting?

There are two parts in a standard bank confirmation. Discuss the purposes and what

would be requested by each component and to whom it would be sent.

For each of the following independent situations, determine the type of opinion that will

most likely be issued by the firm auditing the financial statements of a U.S. company.

1. The client will not allow the auditor to view the minutes for the entire year

under audit and beyond.

2. The auditor finds that the firm is not independent of the client on the last day

of fieldwork.

3. The client declines to include a statement of cash flow in the financial

statements.

4. The client fails to record an immaterial amount of insurance paid in advance

as an asset.

5. The client does not record impairment of goodwill and will not depreciate

property and equipment. Both are considered very material.

6. There is substantial doubt about the client’s ability to continue as a going

concern.

Explain the application of an integrated audit as it relates to regulation. Discuss the

reasons that this integrated approach may occur.

You are a staff auditor on the audit of Cosmo Technologies, Inc. The audit partner asks

you to carefully read the new mortgage contract with the Hometown Bank and abstract

all pertinent information that might be needed for a financial disclosure.

Required:

(1) List the information in a mortgage that is likely to be relevant to the auditor.

(2) What are the pros and cons of using a disclosure checklist for this task?

Discuss the purpose of the audit program and its importance to the auditor.