1) The management of Roger Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity rather than on the

estimated amount of activity for the year. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation

base is machine-hours and the estimated amount of the allocation base for the upcoming

year is 49,000 machine-hours. In addition, capacity is 60,000 machine-hours and the

actual activity for the year is 47,900 machine-hours. All of the manufacturing overhead

is fixed and is $1,587,600 per year. For simplicity, it is assumed that this is the

estimated manufacturing overhead for the year as well as the manufacturing overhead at

capacity and the actual amount of manufacturing overhead for the year. Job T43G,

which required 130 machine-hours, is one of the jobs worked on during the year.

Required:

a. Determine the predetermined overhead rate if the predetermined overhead rate is

based on the amount of the allocation base at capacity.

b. Determine how much overhead would be applied to Job T43G if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

c. Determine the underapplied or overapplied overhead for the year if the predetermined

overhead rate is based on the amount of the allocation base at capacity.

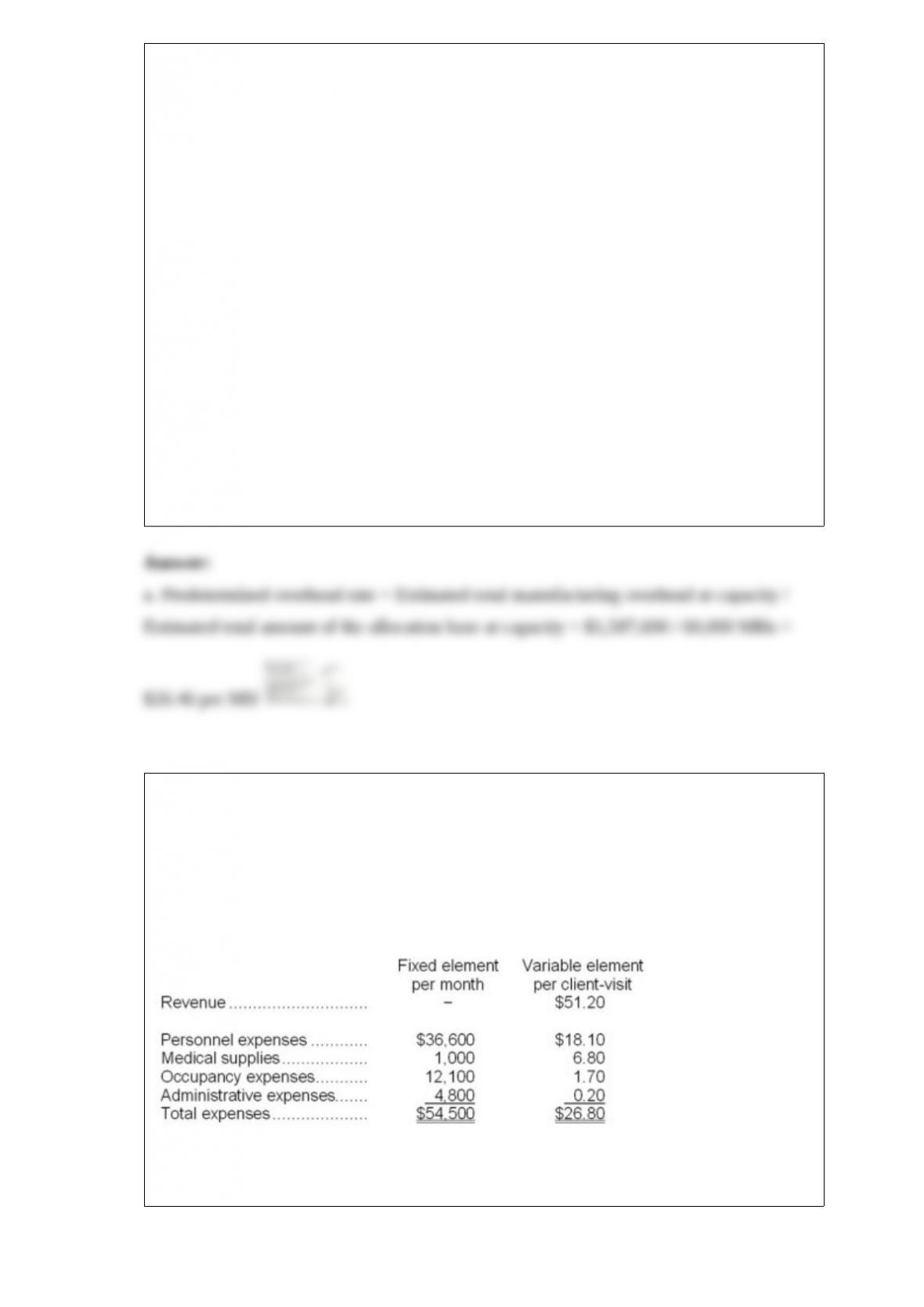

2) Federick Clinic uses client-visits as its measure of activity. During October, the clinic

budgeted for 3,000 client-visits, but its actual level of activity was 3,040 client-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for October:

Data used in budgeting:

Actual results for October:

The occupancy expenses in the flexible budget for October would be closest to:

A.$17,268

B.$18,289

C.$17,811

D.$17,200

3) Midgley Corporation makes a product whose direct labor standards are 0.8 hours per

unit and $22.00 per hour. In April the company produced 6,900 units using 5,250 direct

labor-hours. The actual direct labor cost was $113,925.

The labor efficiency variance for April is:

A.$5,940 U

B.$5,940 F

C.$5,859 F

D.$5,859 U

4) Salter Corporation uses the FIFO method in its process costing system. The company

reported 25,000 equivalent units for materials last month. The company’s beginning

work in process inventory consisted of 6,000 units, 40% complete with respect to

materials. The ending work in process inventory consisted of 4,000 units, 70%

complete with respect to materials. The number of units started during the month was:

A.25,400 units

B.23,400 units

C.22,600 units

D.24,600 units

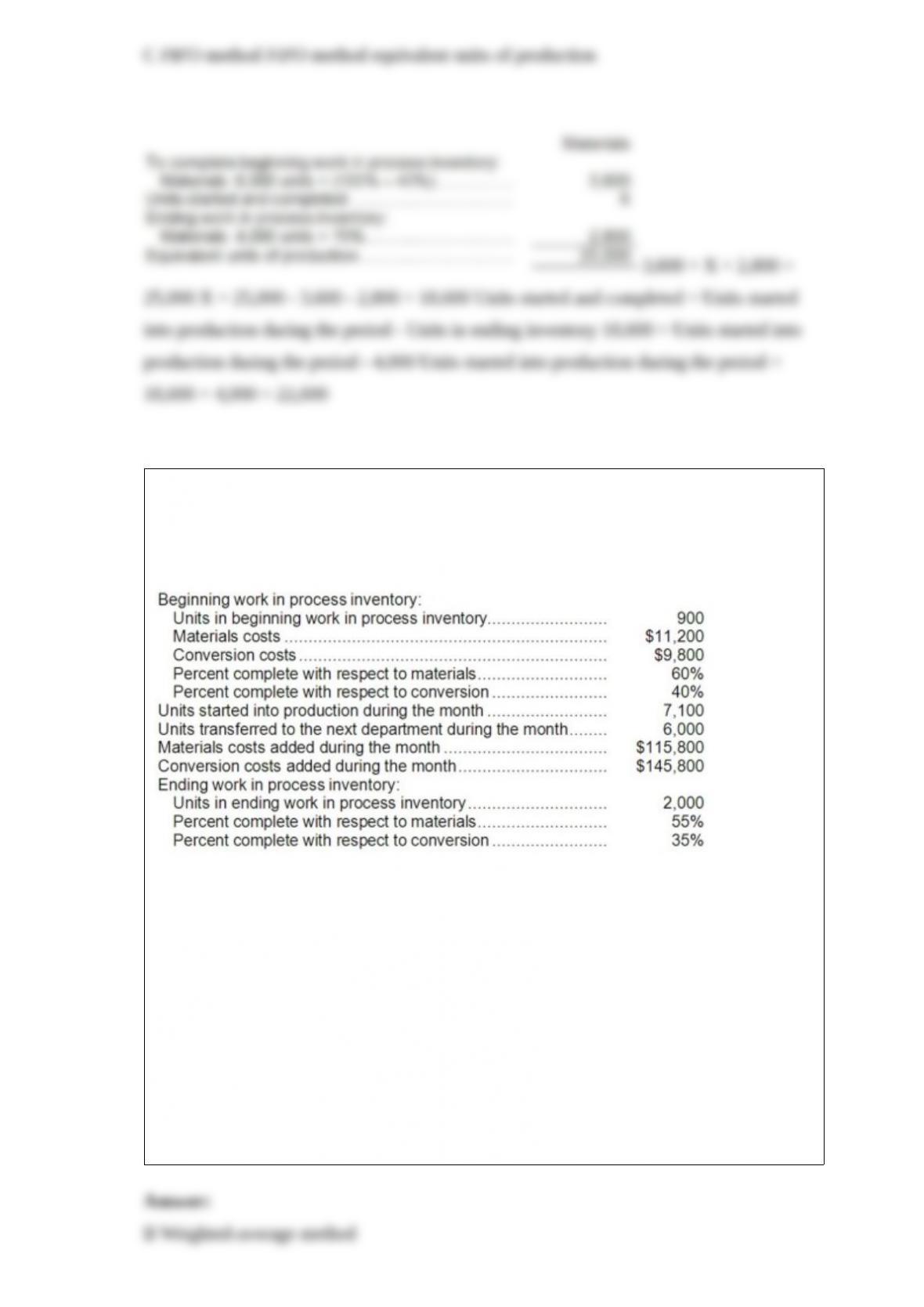

5) Jublot Corporation uses the weighted-average method in its process costing system.

Data concerning the first processing department for the most recent month are listed

below:

Note: Your answers may differ from those offered below due to rounding error. In all

cases, select the answer that is the closest to the answer you computed. To reduce

rounding error, carry out all computations to at least three decimal places.

The cost per equivalent unit for materials for the month in the first processing

department is closest to:

A.$16.31

B.$17.89

C.$14.48

D.$15.88

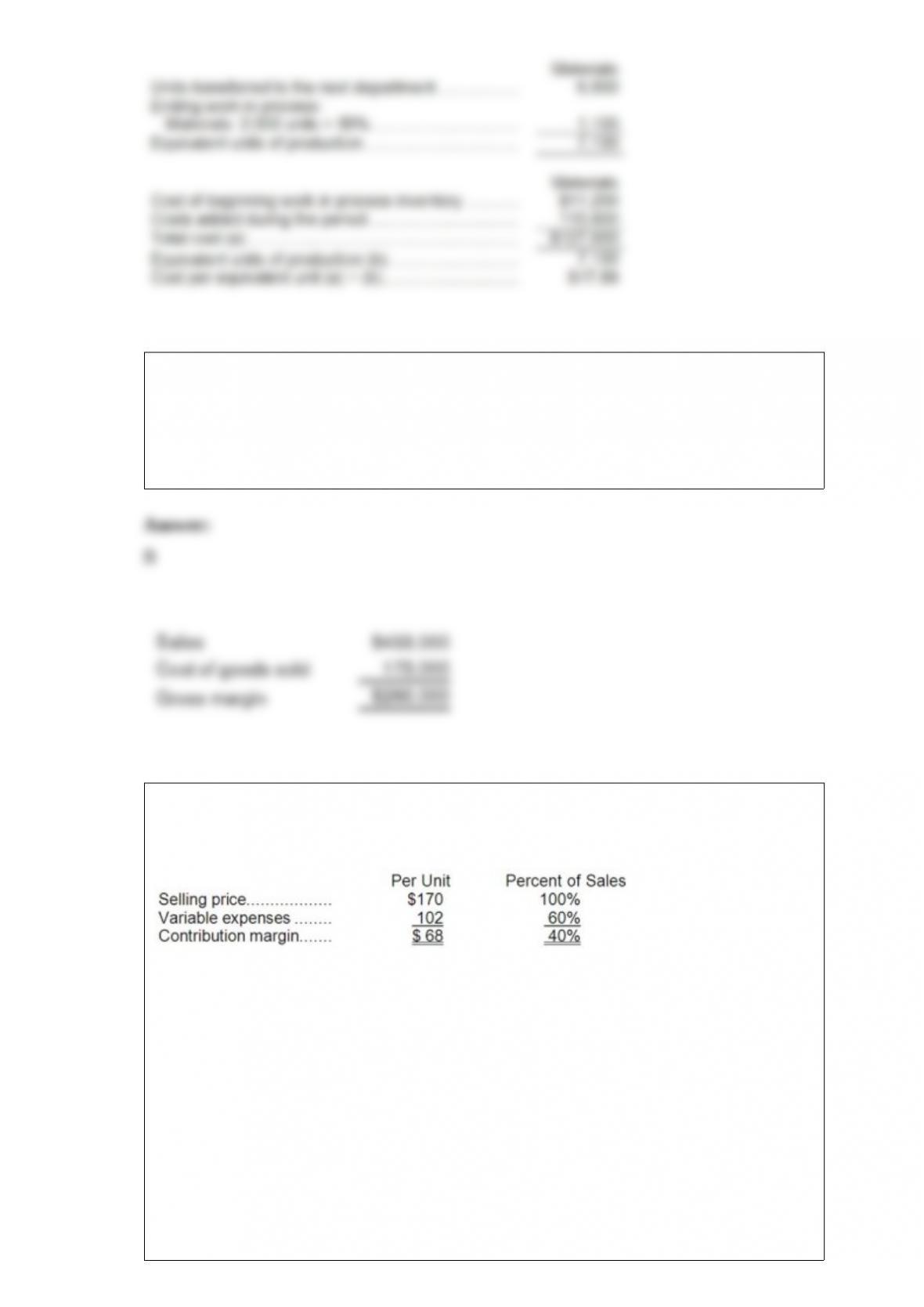

6) The gross margin for October is:

A) $232,000

B) $260,000

C) $397,500

D) $196,500

7) Boenisch Corporation produces and sells a single product with the following

characteristics:

The company is currently selling 8,000 units per month. Fixed expenses are $406,000

per month. Consider each of the following questions independently.

Management is considering using a new component that would increase the unit

variable cost by $3. Since the new component would increase the features of the

company’s product, the marketing manager predicts that monthly sales would increase

by 400 units. What should be the overall effect on the company’s monthly net operating

income of this change?

A.decrease of $2,000

B.increase of $26,000

C.increase of $2,000

D.decrease of $26,000

8) Emco Company uses direct labor cost as a basis for computing its predetermined

overhead rate. In computing the predetermined overhead rate for last year, the company

misclassified a portion of direct labor cost as indirect labor. The effect of this

misclassification will be to:

A.understate the predetermined overhead rate.

B.overstate the predetermined overhead rate.

C.have no effect on the predetermined overhead rate.

D.cannot be determined from the information given.

9) ( The management of Stanforth Corporation is investigating automating a process.

Old equipment, with a current salvage value of $24,000, would be replaced by a new

machine. The new machine would be purchased for $516,000 and would have a 6 year

useful life and no salvage value. By automating the process, the company would save

$173,000 per year in cash operating costs. The simple rate of return on the investment is

closest to:

A.17.7%

B.16.9%

C.33.5%

D.16.7%

10) Lacy Corporation uses the absorption costing approach to cost-plus pricing

described in the text to set prices for its products. Based on budgeted sales of 86,000

units next year, the unit product cost of a particular product is $81.60. The company’s

selling and administrative expenses for this product are budgeted to be $1,247,000 in

total for the year. The company has invested $360,000 in this product and expects a

return on investment of 12%.

The markup on absorption cost for this product would be closest to:

A.12.0%

B.18.4%

C.29.8%

D.17.8%