Heidi Aurora Imports applies International Financial Reporting Standards. The

company issued shares of the company”s Class B stock. Heidi Aurora Imports should

report the stock in the company”s statement of financial position:

a. Among liabilities if the shares are mandatorily redeemable or redeemable at the

option of the shareholder.

b. As equity unless the shares are mandatorily redeemable.

c. As equity unless the shares are redeemable at the option of the issuer.

d. Among liabilities unless the shares are mandatorily redeemable.

During periods when costs are rising and inventory quantities are stable, cost of goods

sold will be:

a. Higher under FIFO than LIFO.

b. Higher under FIFO than average cost.

c. Lower under average cost than LIFO.

d. Lower under LIFO than FIFO.

Which of the following statements characterizes an operating lease?

a. The lessee records depreciation and interest.

b. The lessor records depreciation and lease revenue.

c. The lessor transfers title at the end of the lease term.

d. The lessee records a leased asset.

The declaration and issuance of a stock dividend on shares of common stock:

a. Has no effect on assets, liabilities, or total shareholders’ equity.

b. Decreases total shareholders’ equity and increases common stock.

c. Decreases assets and decreases total shareholders’ equity.

d. Does not change retained earnings or paid-in capital.

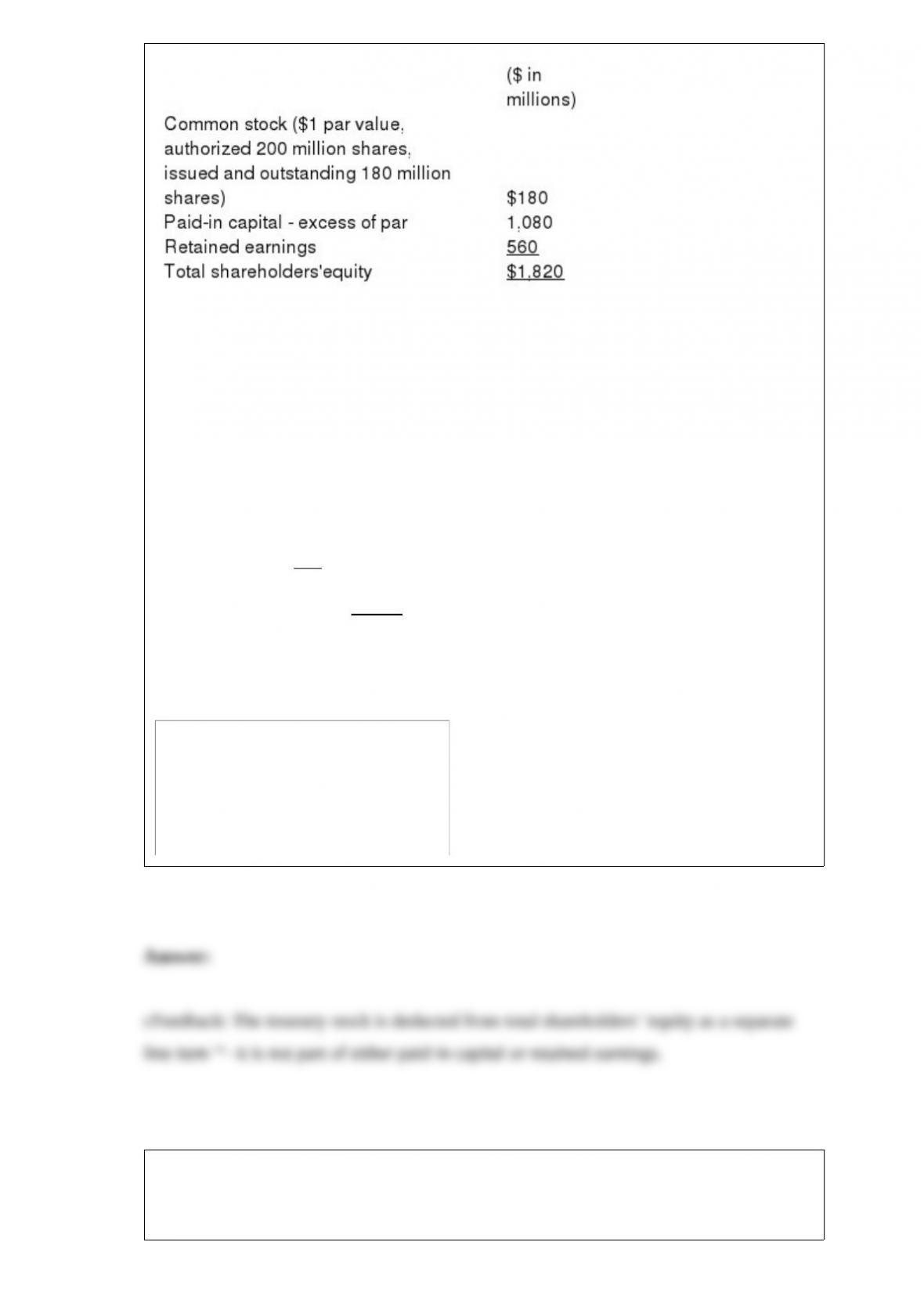

The balance sheet of Messi Services included the following shareholders’ ‘equity

section at December 31, 2016:

($ in millions)

Common stock ($1 par value,

authorized 200 million shares,

issued and outstanding 180 million shares) $ 180

Paid-in capital ‘“ excess of par 1,080

Retained earnings 560

Total shareholders’ equity $1,820

On January 5, 2017, Holmes purchased 2 million treasury shares for $9 million.

Immediately after the purchase of the shares, the balances in the paid-in capital’“-

excess of par and retained earnings accounts are:

Under IFRS No. 9, an investment can be accounted for at amortized cost if:

a. The debt consists of interest and principal, and the investor is holding the debt to

collect those cash flows.

b. The investor elects amortized cost.

c. The investor owns between 20% and 50% of outstanding shares.

d. The debt is not in technical default.

Which of the following best describes the additional information that companies use to

meet the requirements of full disclosure in financial statements?

a. Parenthetical comments or modifying comments placed on the face of the financial

statements.

b. Disclosure notes conveying additional insights about company operations,

accounting principles, contractual agreements, and pending litigation.

c. Supplemental schedules and tables that report more detailed information than is

shown in the primary financial statements.

d. Comments on the face of the financial statements, and schedules, tables, and

narrative disclosures in notes to the financial statements.

Under International Financial Reporting Standards (IFRS), inventory is valued at the

lower of cost and:

a. Replacement cost.

b. Net realizable value.

c. Net realizable value reduced by a normal profit margin.

d. None of these answer choices are correct.

An example of fraud would be:

a. Issuing a purchase order without first securing bids.

b. Buying raw materials from an affiliated company.

c. Knowingly classifying a material noncurrent receivable as a current receivable.

d. Forgetting to accrue salaries and wages payable.

When bonds are retired prior to their maturity date:

a. GAAP has been violated.

b. The issuing company probably will report an ordinary gain or loss.

c. The issuing company probably will report a gain.

d. The issuing company will report a non-operating gain or loss.

New Oaks Winery requires two months to make wine, two years to age it, one month to

bottle it, two months to sell it, and one month to collect the receivable. Its operating

cycle is:

a. Twelve months.

b. Thirty months.

c. Six months.

d. Three months.

Under IFRS, the conceptual framework:

a. Emphasizes the overarching concept of the financial statements providing a ‘œ”true

and fair representation'” of the company.

b. Is not designed to provide guidance to standard setters, but rather only to

practitioners.

c. Is not designed to provide guidance to practitioners, but rather only to standard

setters.

d. Specifies a set of rules that determine what constitutes a true IFRS standard.

Investments in securities to be held for an unspecified period of time are reported at:

a. Historical cost.

b. Present value.

c. Lower of cost or market.

d. Fair value.

The gross profit method and retail method are both ways of estimating ending

inventory. Briefly explain how the two methods differ.

List and briefly describe the three levels of inputs described in the fair-value

measurement hierarchy.

() Prepare all appropriate journal entries, assuming a cash dividend in the amount of

$00 per share.

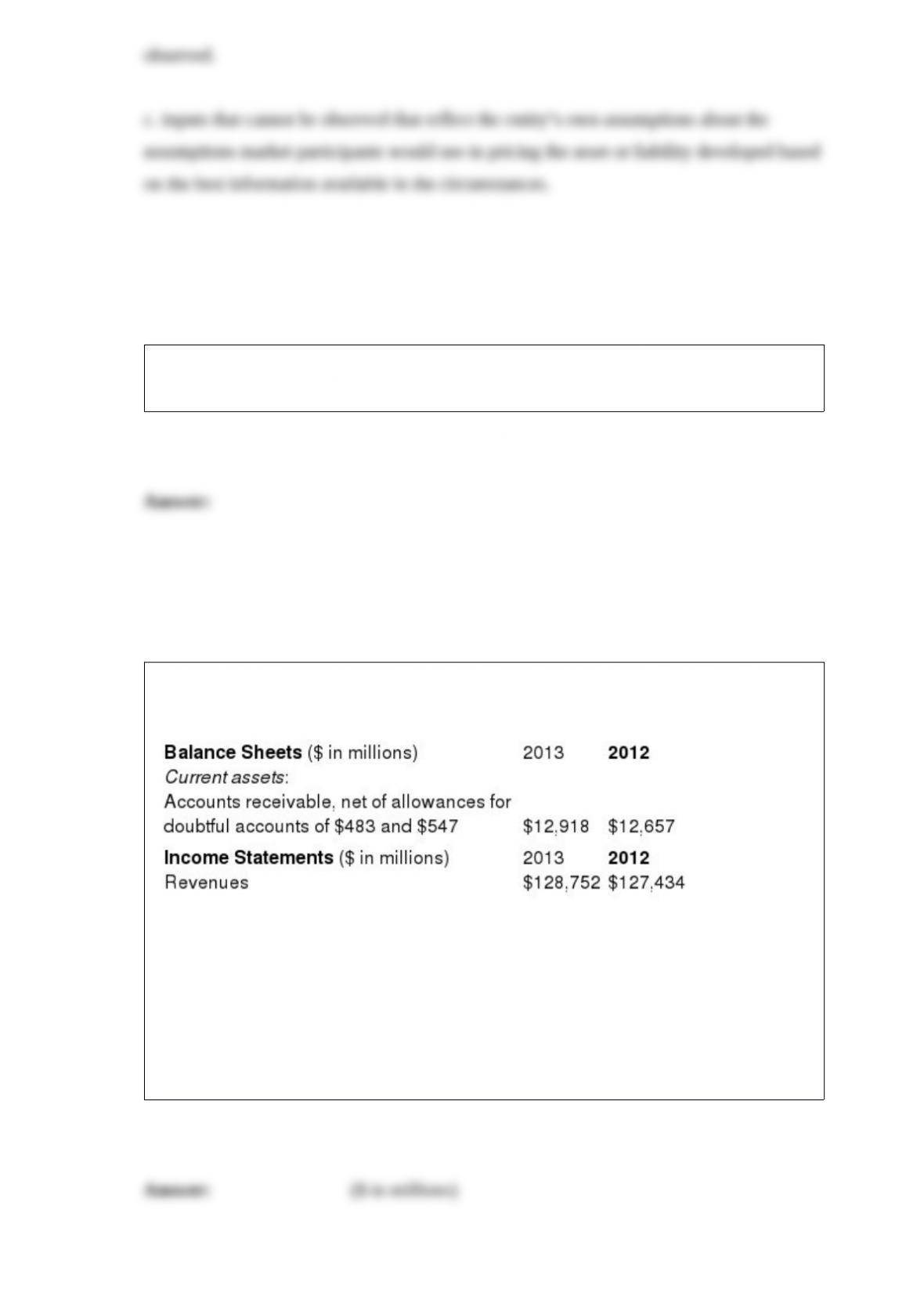

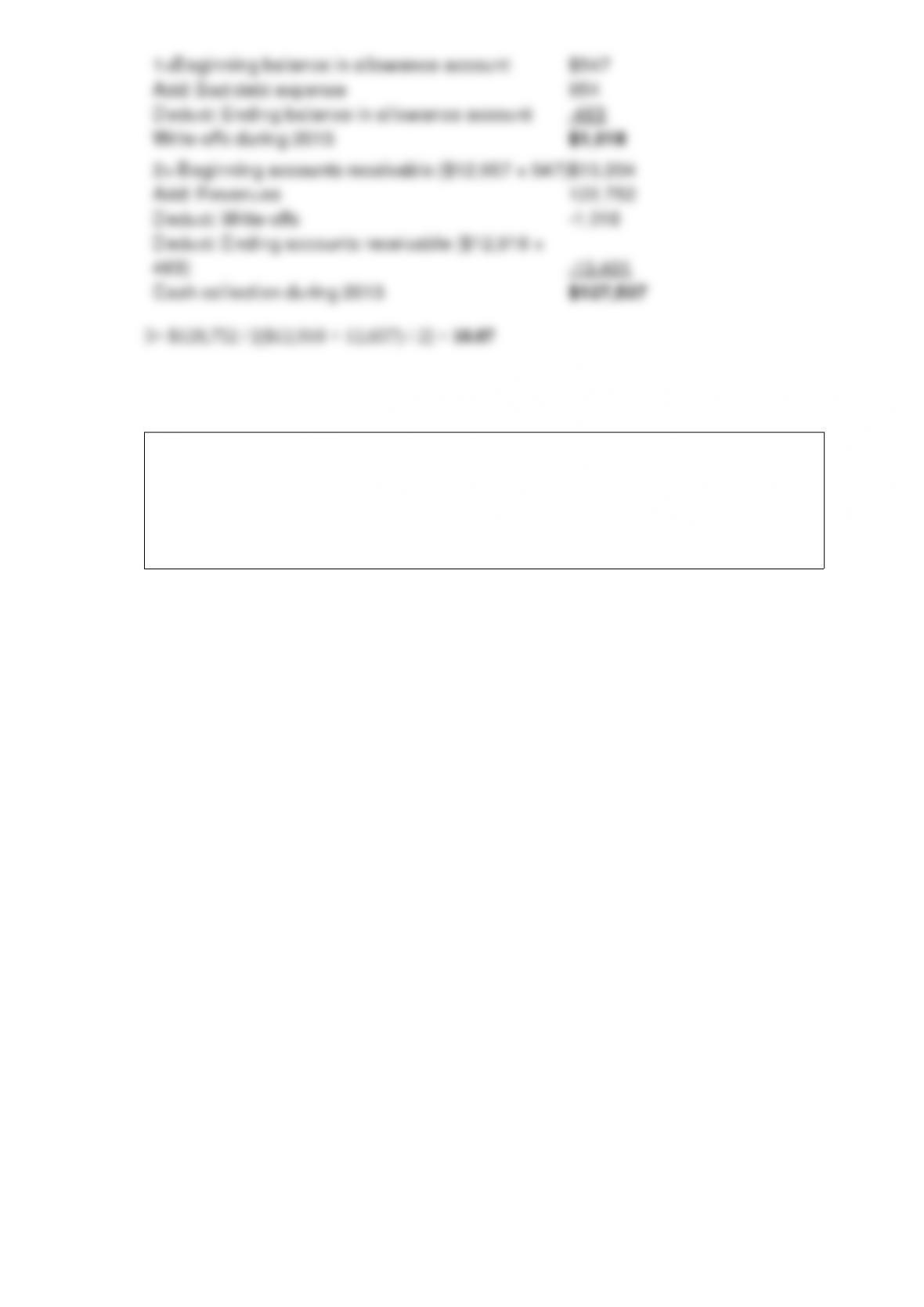

AT&T’s financial statements for the 2013 and 2012 fiscal years contained the following

information:

In addition, the statement of cash flows disclosed bad debt expense of $954 million in

2013 and $1,117 million in 2012. Required:

1> Determine the amount of actual bad debt write-offs made during 2013.

2> Determine the amount of cash collected from customers during 2013.

3> Compute the receivables turnover ratio for 2013.

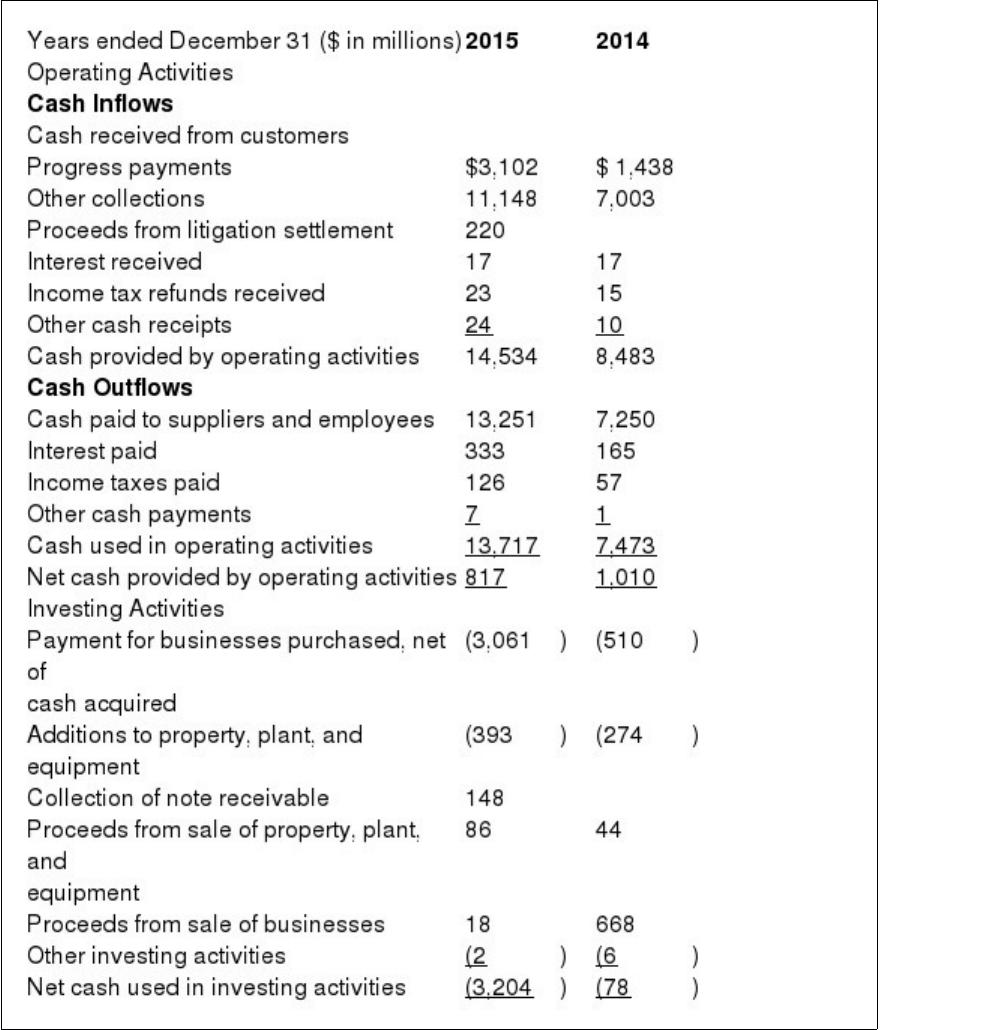

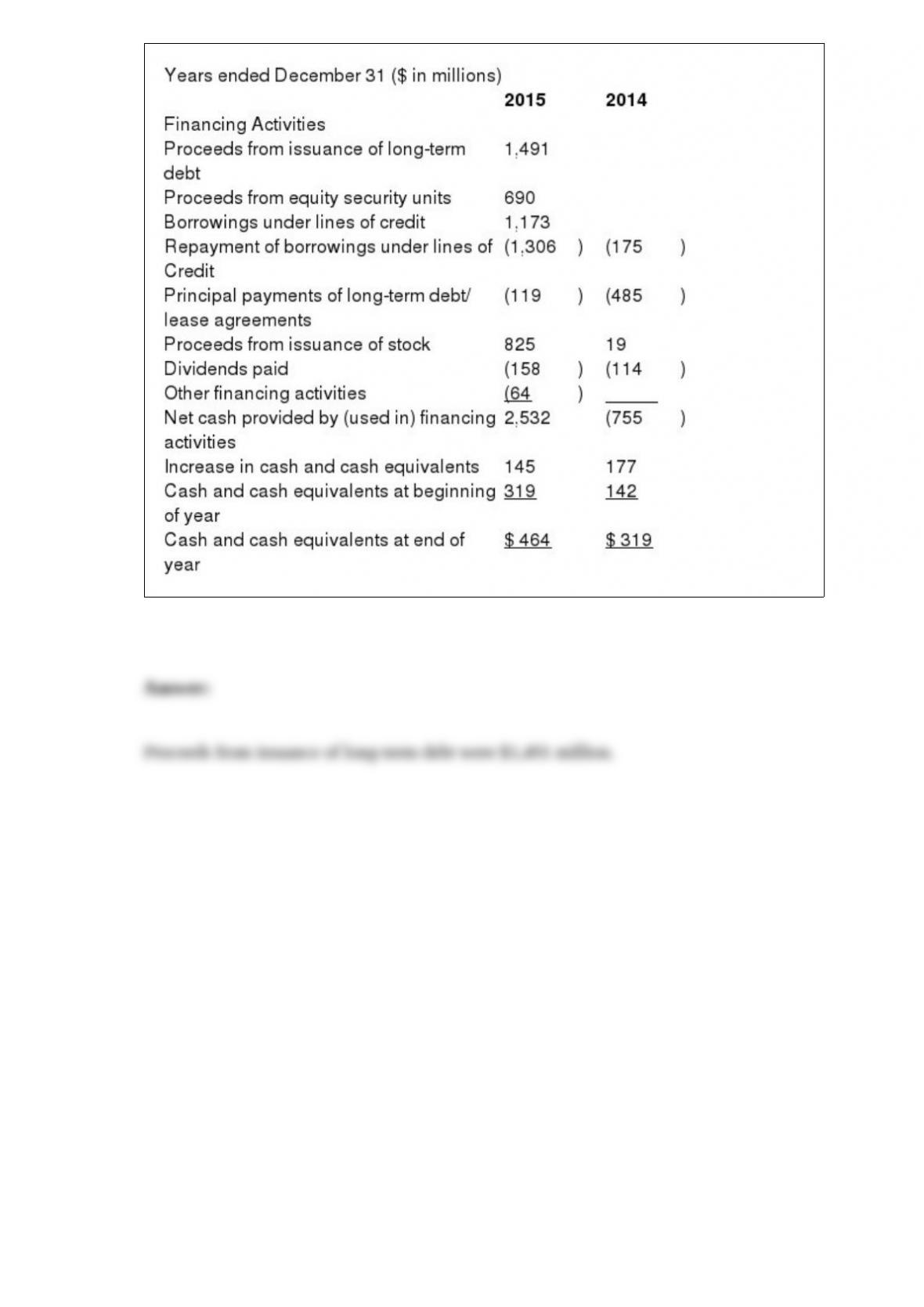

What was most responsible for the positive cash flow from financing activities during

2015? What amount was received?

In its 2015 Annual Report to Shareholders, Henchman & Co. provided the following

Statement of Cash Flows: