Panther Co. had a quality-assurance warranty liability of $350,000 at the beginning of

2016 and $310,000 at the end of 2016. Warranty expense is based on 4% of sales, which

were $50 million for the year. What were the warranty expenditures for 2016?

a. $0.

b. $1,960,000.

c. $2,000,000.

d. $2,040,000.

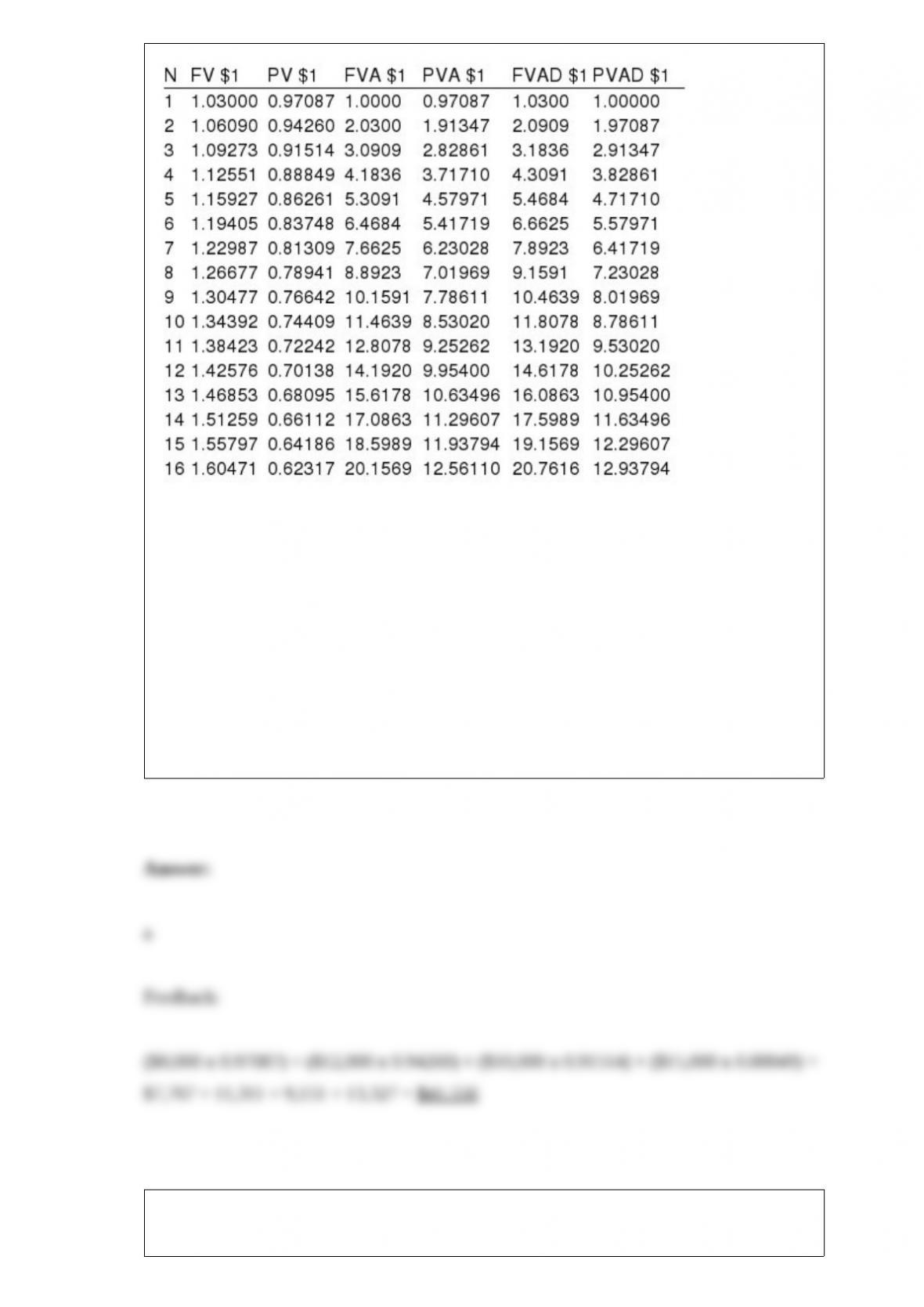

Present and future value tables of $1 at 3% are presented below:

At the end of the next four years, a new machine is expected to generate net cash flows

of $8,000, $12,000, $10,000, and $15,000, respectively. What are the (rounded) cash

flows worth today if a 3% interest rate properly reflects the time value of money in this

situation?

a. $41,556.

b. $39,982.

c. $32,400.

d. $38,100.

What amount should M recognize as compensation expense for 2016?

On January 1, 2016, M Company granted 90,000 stock options to certain executives.

The options are exercisable no sooner than December 31, 2018, and expire on January

1, 2022. Each option can be exercised to acquire one share of $1 par common stock for

$12. An option-pricing model estimates the fair value of the options to be $5 on the date

of grant.

a. $ 30,000.

b. $ 60,000.

c. $120,000.

d. $150,000.

Cracker Company had 2 million shares of common stock outstanding all through

2015. On April 1, 2016, an additional 100,000 shares were sold and issued. On

September 30, 2016, Cracker declared a 2-for-1 stock split. Net income in 2016 and

2015 was $10 million and $8 million, respectively. In the 2016 comparative financial

statements, EPS (rounded) would be reported as follows:

2016 EPS 2015 EPS

a. 2.41 $2.00

b. 2.41 $4.00

c. 4.82 $4.00

d. 4.82 $4.00

All investment securities are initially recorded at:

a. Cost.

b. Present value.

c. Equity value.

d. None of these answer choices is correct.

Archie Co. purchased a framing machine for $45,000 on January 1, 2016. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years. Using the double-declining balance method, depreciation for 2016 and book

value at December 31, 2016, would be:

a. $22,500 and $22,500.

b. $22,500 and $17,500.

c. $20,000 and $25,000.

d. $20,000 and $20,000.

If the fair value of a trading security declines for a reason that is viewed as “other than

temporary”:

a. The investment is not written down to fair value.

b. The investment is written down to fair value, and an “impairment loss” is recognized

in net income.

c. The investment is written down to fair value, and the impairment loss is recognized

in accumulated other comprehensive income.

d. The investment is treated the same way it would be treated if the decline in fair value

was viewed as temporary.

Under the dollar-value LIFO retail method, to determine if the increase in the value of

inventory was due to an increase in quantities:

a. Compare beginning and ending inventory amounts at current year prices.

b. Compare beginning and ending inventory amounts after adjusting both amounts to

the average price level for the year.

c. Inflate beginning inventory amount to end of year prices and compare to ending

inventory amount.

d. Deflate the ending inventory amount to beginning of year prices and compare to the

beginning inventory amount.

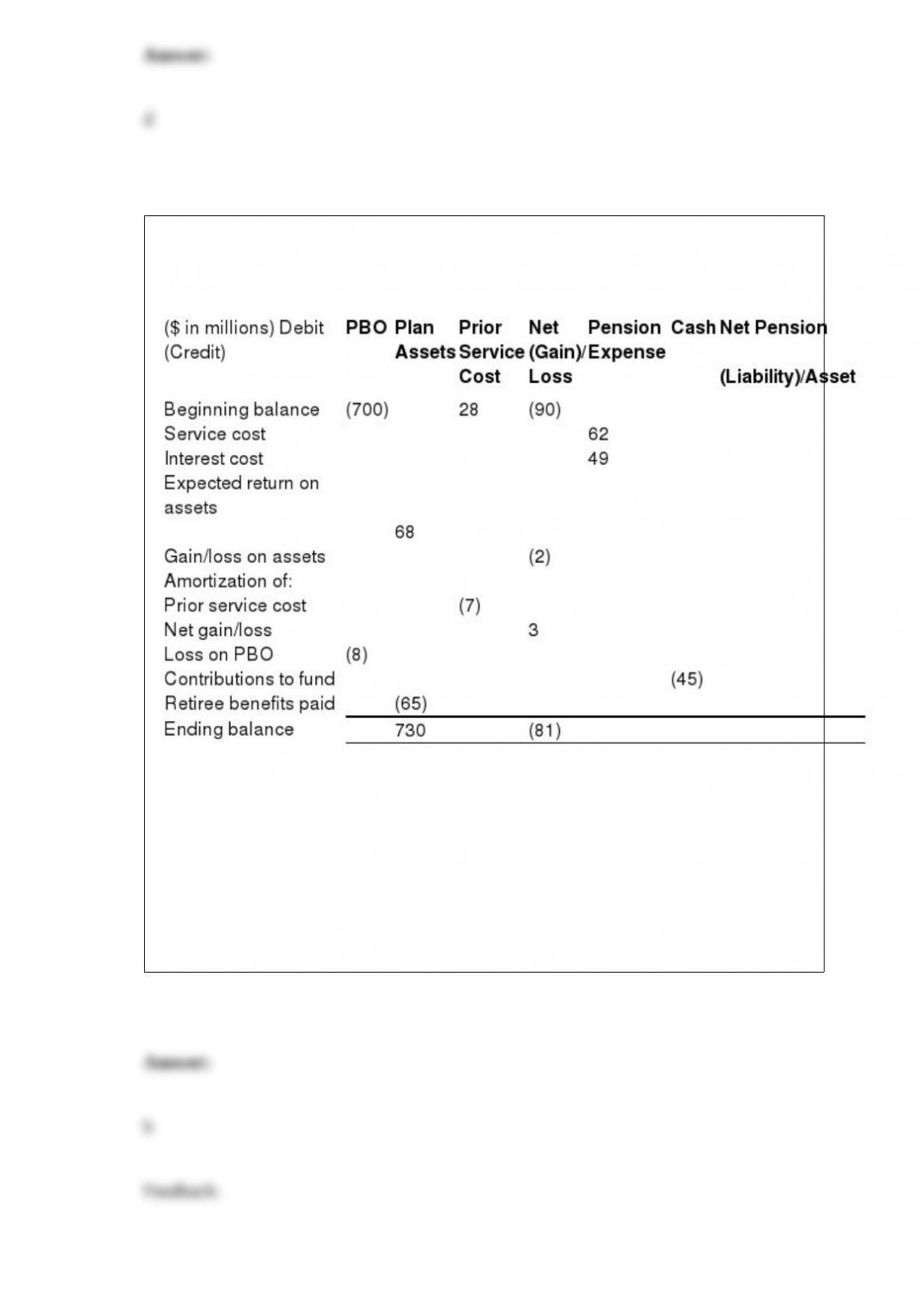

The following incomplete (columns have missing amounts) pension spreadsheet is for

the current year for First Republic Corporation (FRC).

What was FRC’s pension expense for the year?

a. $44.

b. $47.

c. $49.

d. $107.

Eve’s Apples opened business on January 1, 2016, and paid for two insurance policies

effective that date. The liability policy was $36,000 for 18 months, and the crop damage

policy was $12,000 for a two-year term. What is the balance in Eve’s prepaid insurance

as of December 31, 2016?

a. $ 9,000.

b. $18,000.

c. $30,000.

d. $48,000.

Damon, Inc., acquired 25% of Jolie Enterprises for $8,000,000 on October 1, 2016. The

total fair value of Jolie’s identifiable net assets was $27,000,000 on that date, and the

total book value of those net assets was $23,000,000. The difference between fair value

and book value is attributed to equipment that has a remaining useful life of 4 years.

During 2016 Jolie recognized net income of $2,000,000 and paid dividends of

$1,200,000 ($300,000 per quarter). Jolie had a fair value of $36,000,000 as of

December 31, 2016.

Required: Assume Damon accounts for the Jolie investment under the equity method.

Indicate the total effect of the Jolie investment on Damon’s:

1) net income for 2016

2) the balance in Damon’s investment account on December 31, 2016.

For a typical manufacturing company, the most common critical point for recognizing

revenue is the date:

m. An order is received.

n. Production is completed.

o. The product is delivered.

p. Payment is received.

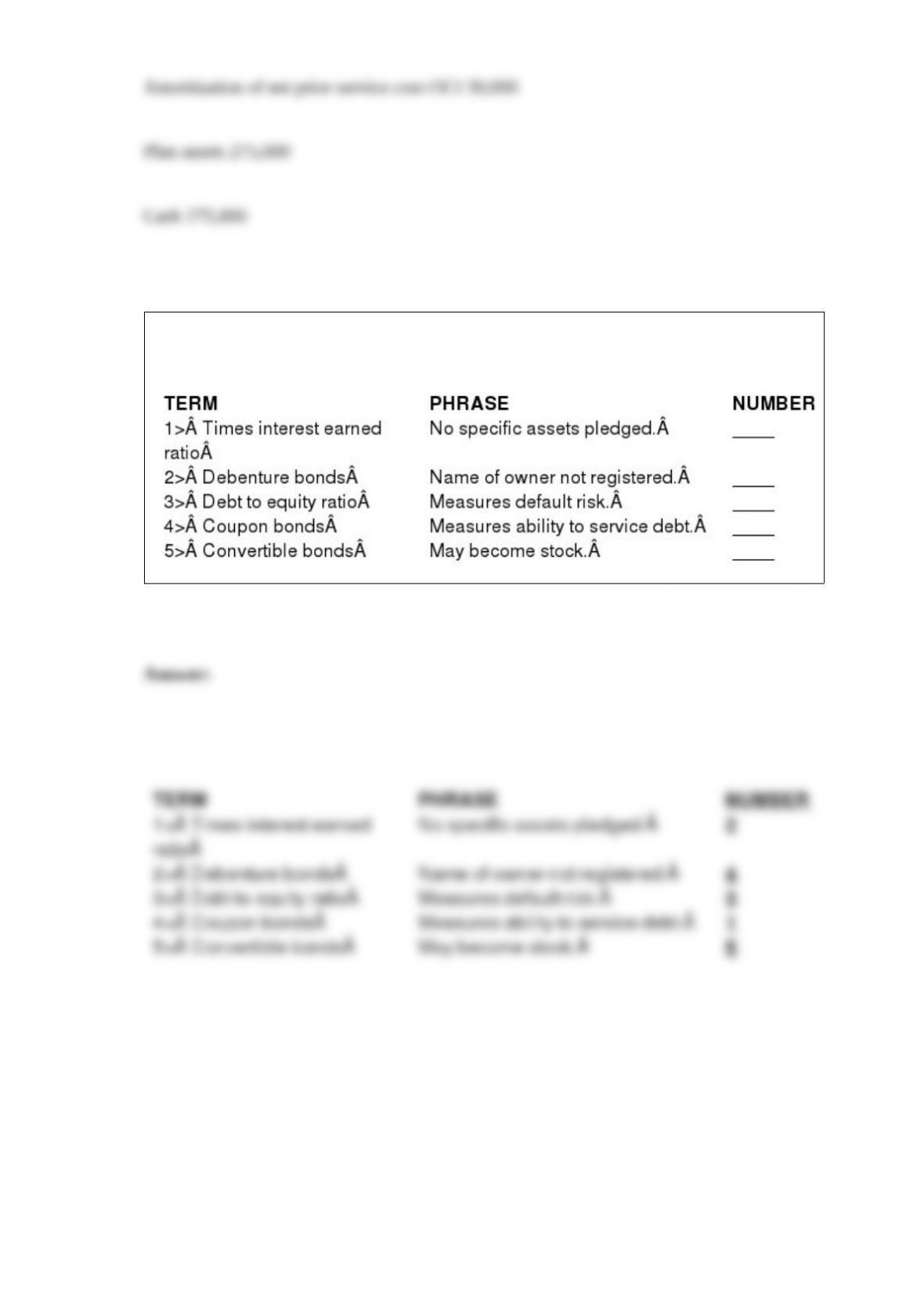

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

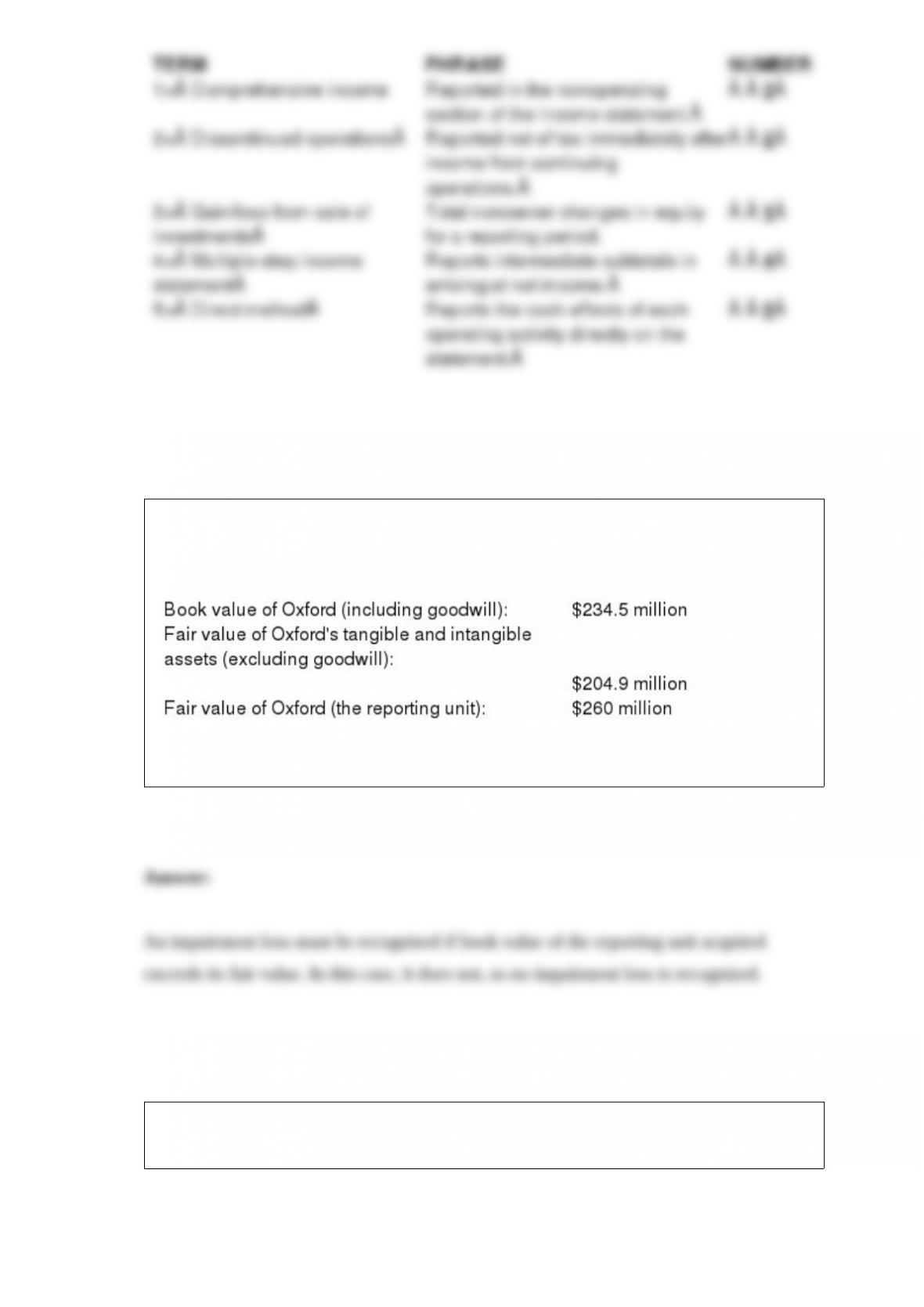

In 2015, Dooling Corporation acquired Oxford Inc. for $250 million, of which $50

million was attributed to goodwill. At the end of 2016, Dooling’s accountants derive the

following information for a required goodwill impairment test:

Required: Determine the amount, if any, of the goodwill impairment loss that Dooling

must recognize on these assets.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the most correct term.

Peanut Corporation exchanged land and cash of $6,500 for equipment. The land had a

book value of $45,000 and a fair value of $34,000. Assume the exchange has

commercial substance.

Required:

Prepare the journal entry to record the exchange.

On December 31, 2015, Jackson Company had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $50 par, cumulative preferred stock outstanding.

On February 28, 2016, Jackson purchased 24,000 shares of common stock on the open

market as treasury stock paying $45 per share. Jackson sold 6,000 of the treasury shares

on September 30, 2016, for $47 per share. Net income for 2016 was $180,905. Also

outstanding at December 31, 2015, were fully vested incentive stock options giving key

personnel the option to buy 50,000 common shares at $40. These stock options were

exercised on November 1, 2016. The market price of the common shares averaged $50

during 2016.

Required:

Compute Jackson’s basic and diluted earnings per share (rounded to 2 decimal places)

for 2016.

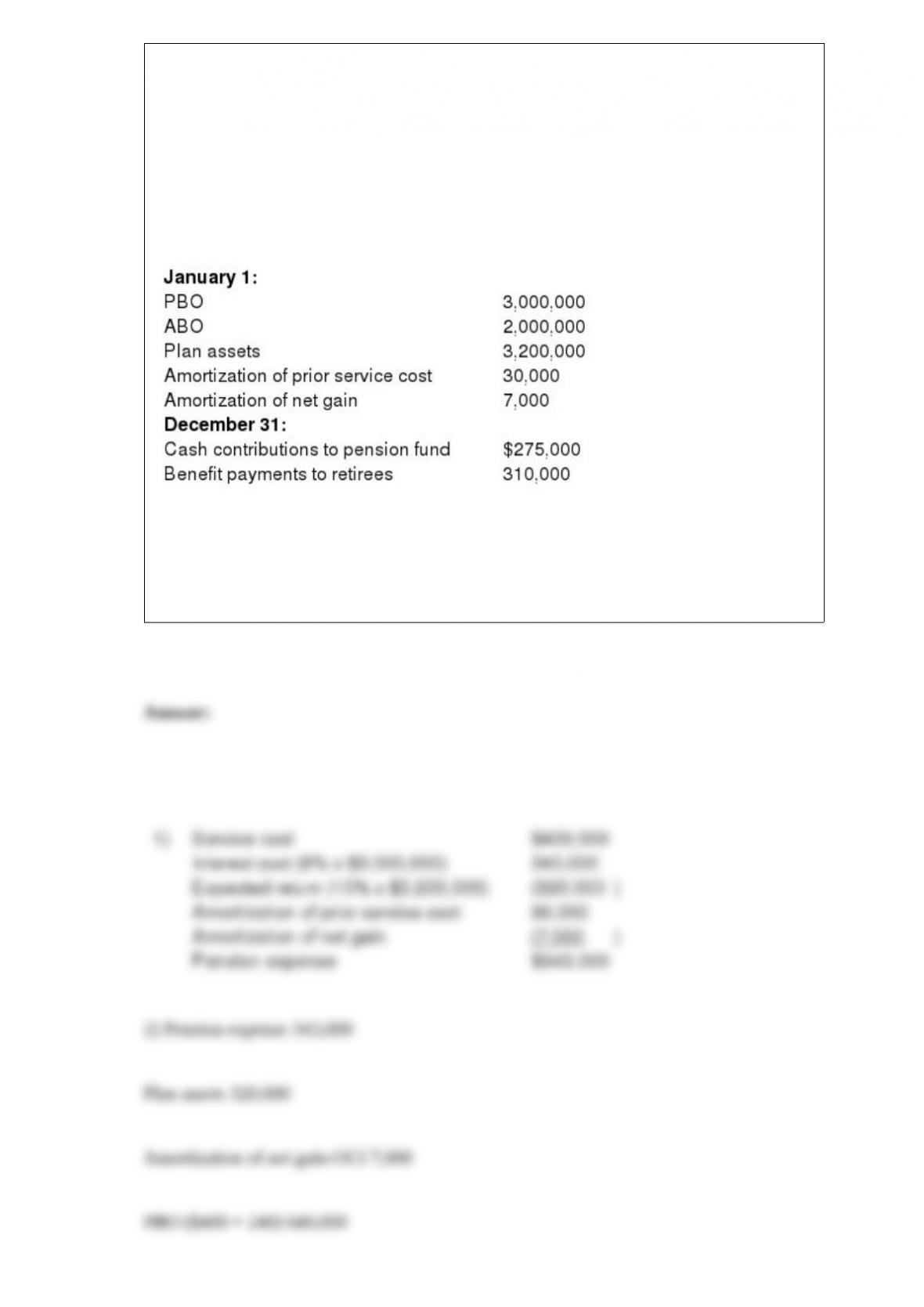

Pension data for Sam Adams Inc. include the following for the current calendar year:

Discount rate, 8%

Expected return on plan assets, 10%

Actual return on plan assets, 9%

Service cost, $400,000

Required:

1) Determine pension expense for the year.

2) Prepare the journal entries to record pension expense and funding for the year.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the most correct term.