1) gross profit for a merchandising concern is net sales minus

a.operating expenses

b.cost of goods sold

c.sales discounts

d.cost of goods available for sale

2) which of the following statements concerning ifrs and u.s. gaap is true?

a.ifrs permits revaluation of all intangible assets, whereas u.s. gaap prohibits revaluation

of intangible assets

b.gains on exchange of assets when the exchange has commercial substance are

recognized under both ifrs and u.s. gaap

c.changes in depreciation method under ifrs are reported in current and future periods,

under u.s. gaap such changes are treated as prior period adjustments

d.all of the choices are true regarding ifrs and u.s. gaap

3) the corporate charter of torres corporation allows the issuance of a maximum of

3,000,000 shares of $1 par value common stock. during its first three years of operation,

torres issued 1,560,000 shares at $15 per share. it later acquired 60,000 of these shares

as treasury stock for $25 per share.

instructions

based on the above information, answer the following questions:

(a)how many shares were authorized?

(b)how many shares were issued?

(c)how many shares are outstanding?

(d)what is the balance of the common stock account?

(e)what is the balance of the treasury stock account?

4) ifrs requires loans and receivables to be recorded at

a.amortized cost

b.amortized cost, adjusted for allowances for doubtful accounts

c.unamortized cost

d.unamortized cost, adjusted for allowances for doubtful accounts

5) using the percentage of receivables method for recording bad debts expense,

estimated uncollectible accounts are $29,000. if the balance of the allowance for

doubtful accounts is $9,000 debit before adjustment what is the amount of bad debt

expense for that period?

a.$29,000

b.$ 9,000

c.$38,000

d.$20,000

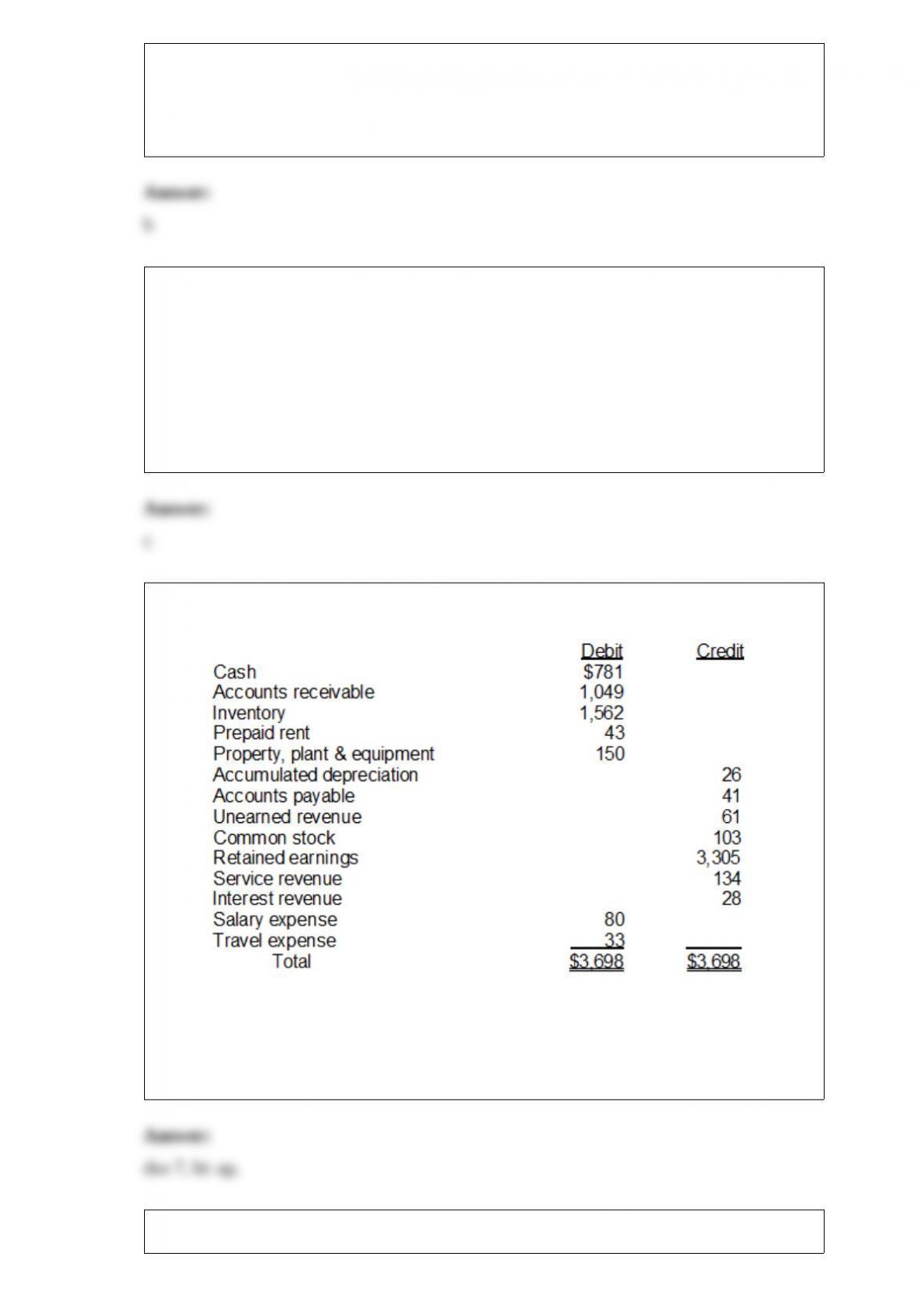

6) given the following adjusted trial balance:

after closing entries have been posted, the balance in retained earnings will be:

a.$3,256

b.$3,170

c.$3,440

d.$3,354

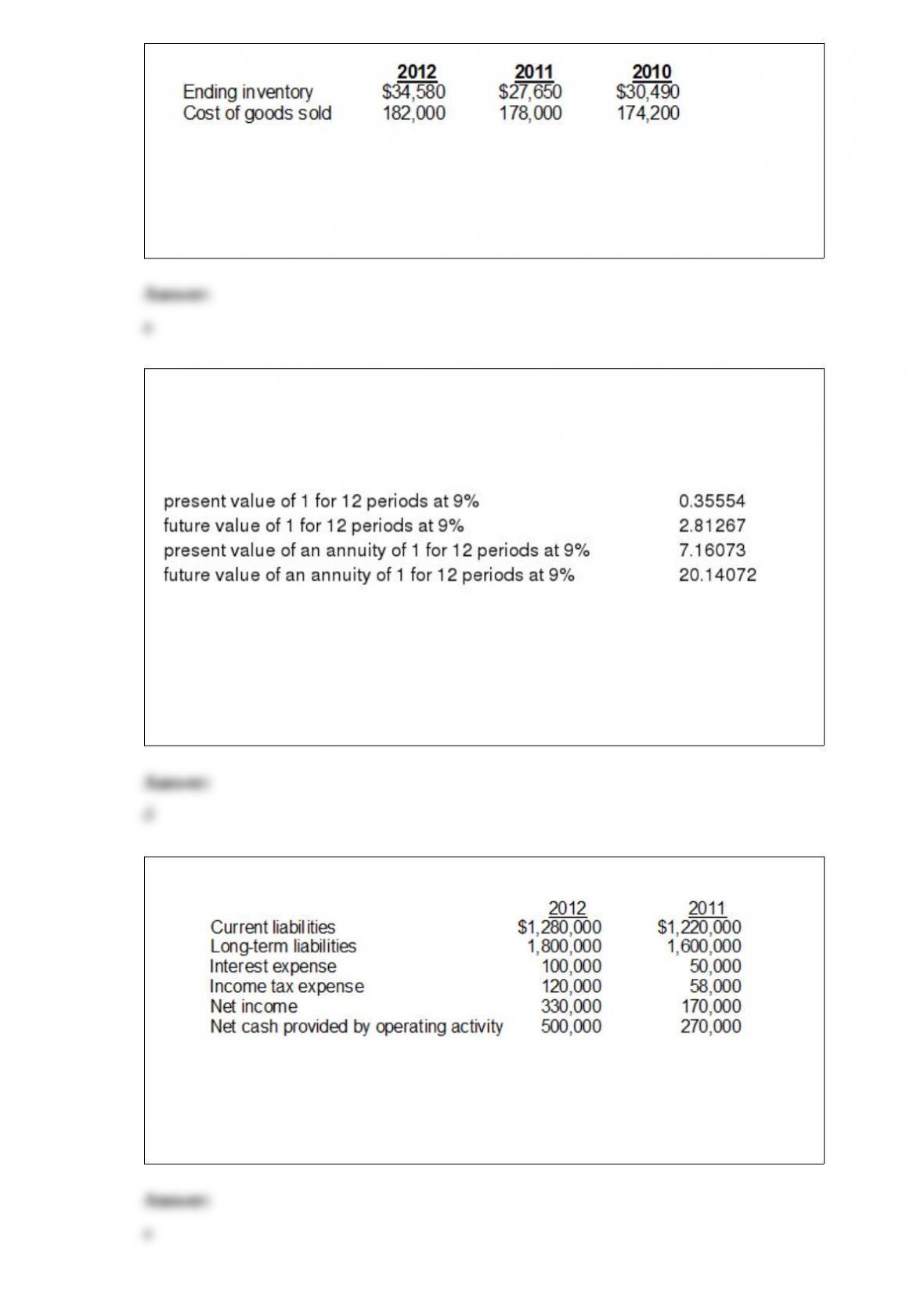

7) redeker company had the following records:

what is redekers inventory turnover ratio for 2011? (rounded)

a.6.1 times

b.5.7 times

c. .2 times

d.6.4 times

8) barnard company is considering investing in an annuity contract that will return

$40,000 annually at the end of each year for 12 years. barnard has obtained the

following values related to the time value of money to help in its planning process and

compounded interest decisions.

to the closest dollar, what amount should ritz company pay for this investment if it

earns a 9% return?

a.$497,066

b.$592,507

c.$805,629

d.$286,429

9) the following amounts were taken from the financial statements of brandt company:

the cash debt coverage ratio for 2012 is

a.16.9%

b.16.2%

c.11.2%

d.29.4%

10) which statement is incorrect?

a.periodic inventory systems provide better control over inventories than perpetual

inventory systems

b.computers and electronic scanners allow more companies to use a perpetual inventory

system

c.freight-in is debited to merchandise inventory when a perpetual inventory system is

used

d.regardless of the inventory system that is used, companies should take a physical

inventory count

11) henry company deposits $15,000 in a fund at the end of each year for 5 years. the

fund pays interest of 3% compounded annually. the balance in the fund at the end of 5

years is computed by multiplying

a.$15,000 by the future value of 1 factor

b.$75,000 by 1.03

c.$75,000 by 1.30

d.$15,000 by the future value of an annuity factor

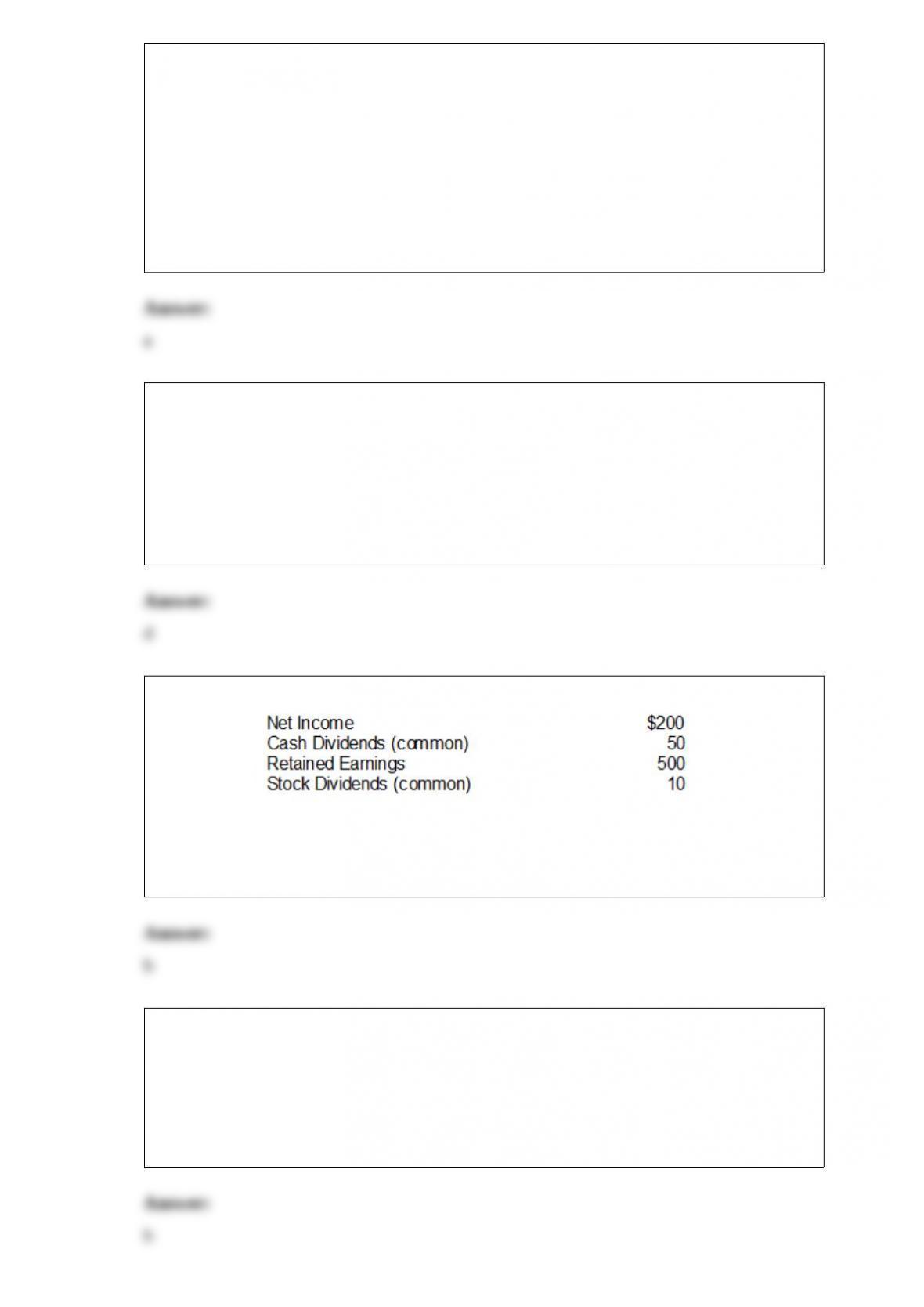

12) from the information below, compute the payout ratio for kevins trailers.

a.30%

b.25%

c.10%

d.2%

13) when two or more people get together for the purpose of circumventing prescribed

controls, it is called

a.a fraud committee

b.collusion

c.a division of duties

d.bonding of employees

14) in its simplest form, an account consists of all of the following except

a.right (credit) side.

b.account title.

c.left side.

d.explanation column.

15) which one of the following items would not be considered cash?

a.coins

b.money orders

c.currency

d.postdated checks

16) selected transactions for the locey company are listed below.

1>collected accounts receivable.

2>declared and paid dividends on common stock.

3>sold long-term investments for cash.

4>issued stock for equipment.

5>repaid five year note payable.

6>paid employee wages.

7>converted bonds payable to common stock.

8>acquired long-term investment with cash.

9>sold buildings and equipment for cash.

10>sold merchandise to customers.

instructions

classify each transaction as either (a) an operating activity, (b) an investing activity, (c)

a financing activity, or (d) a noncash investing and financing activity.

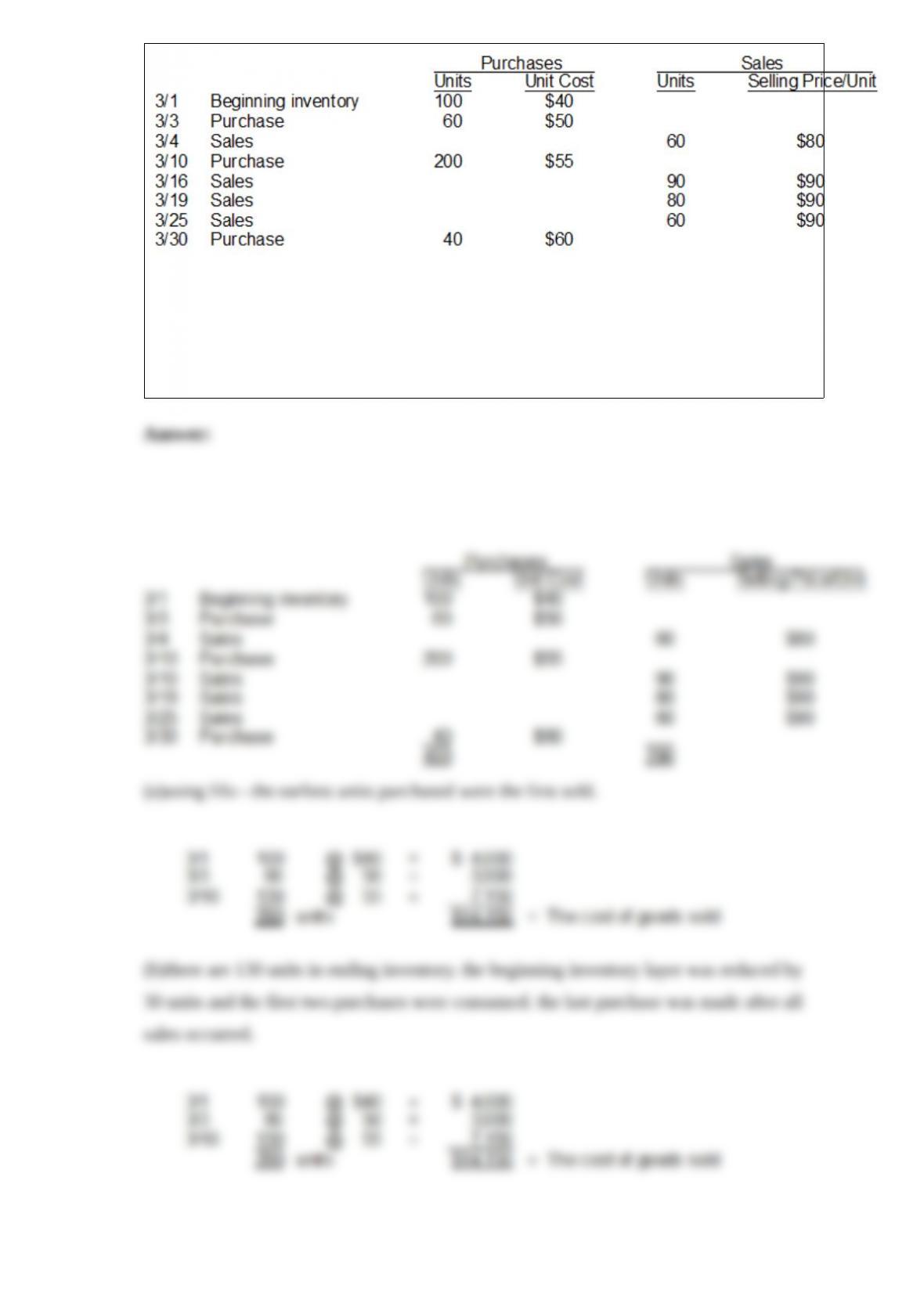

17) woodson company sells many products. gizmo is one of its popular items. below is

an analysis of the inventory purchases and sales of gizmo for the month of march.

woodson company uses the perpetual inventory system.

instructions

(a)using the fifo assumption, calculate the amount charged to cost of goods sold for

march. (show computations)

(b)using the lifo assumption, calculate the amount assigned to the inventory on hand on

march 31. (show computations)

18) customarily, a trial balance is prepared

a.at the end of each day.

b.after each journal entry is posted.

c.at the end of an accounting period.

d.only at the inception of the business.