The entry to record inventory shrinkage includes a debit to the Merchandise Inventory

account. Assume a perpetual inventory system is used.

Prenumbered source documents provide necessary control in a system by automatically

assigning a sequential number to each new transaction.

Tri-City Installations Company uses the direct method to prepare its statement of cash

flows. Tri-City has reported sales revenues of $200,000 on its income statement for

2018. If the balance in Accounts Receivable has increased by $10,000 during the year,

then $10,000 needs to be added to $200,000 to calculate collections from customers.

The distribution of dividends represents an increase in retained earnings.

The declaration of a stock dividend creates a liability for the corporation.

A business keeps cash in a bank account because banks have established practices for

safeguarding the business’s money.

The rate of return on total assets is a ratio that measures a company’s success in using

its assets to earn income.

The cost paid to a laborer to assemble a desk is recorded as an expense.

The current ratio may indicate that the company is using its assets effectively.

The asset turnover ratio is a way to evaluate how well a company can pay its short-term

liabilities.

Dress Designers, Inc. has entered into a contract to design 50 new dresses for a

customer. It will collect a total of $42,000 after the design services are complete. Dress

Designers started design work on June 1. As of June 30, it finished 10 of the 50 designs.

The company will make an adjusting entry at the end of June to accrue $10,500 of

service revenue.

An acid-test ratio of 1.0 is considered safer than a ratio of 0.50.

Equity increases when revenues are earned.

An overstatement of ending merchandise inventory in the current period results in an

overstatement of cost of goods sold in the current period.

The worksheet is a useful step in preparing adjusting entries and the unadjusted trial

balance.

A lump-sum purchase or basket purchase involves paying a single price for several

assets as a group.

The times-interest-earned ratio is also called the short interest ratio.

Vertical analysis involves comparing an amount for a line item in the financial

statements with a corresponding amount for the line item of the previous year.

In a multi-step income statement, interest revenue and interest expense are included in

operating income.

Impairment of an intangible asset occurs when the book value of an asset is less than

the fair value.

Equity decreases with expenses and revenues.

A business can be organized as a sole proprietorship, partnership, corporation, or

limited-liability company (LLC).

Stockholders of a corporation are not personally liable for the corporation’s debt.

The trial balance is also known as the balance sheet.

Usually, the issue price exceeds par value because par value is normally set as a

percentage of the issue price of the stock.

Using the LIFO method of inventory valuation will always produce the same results for

cost of goods sold and ending inventory whether a company uses perpetual or periodic

inventory costing methods.

In a periodic inventory system, purchases, purchase discounts, and purchase returns and

allowances are recorded in the Merchandise Inventory account as and when they occur.

The Accounts Receivable account is a permanent account.

Companies often disclose that the LCM rule is followed in notes to their financial

statements.

The issuance of a note is recorded, on the books of the borrower, by crediting Cash and

debiting Notes Receivable.

Which of the following is the correct order of preparation of financial statements?

A) Income statement → statement of retained earnings → balance sheet → statement of

cash flows

B) Statement of retained earnings → balance sheet → income statement → statement of

cash flows

C) Balance sheet → statement of retained earnings → income statement → statement of

cash flows

D) Balance sheet → income statement → statement of retained earnings → statement of

cash flows

Which of the following is an asset account?

A) Wages Payable

B) Notes Payable

C) Unearned Revenue

D) Accounts Receivable

Which of the following is provided in a typical chart of accounts?

A) Account balance

B) Account number

C) Dates of transactions

D) Transaction amounts

Which of the following is a permanent account?

A) Wages Expense

B) Salaries Payable

C) Service Revenue

D) Utilities Expense

A merchandiser uses a perpetual inventory system. The third step in the process of

closing the accounts of a merchandiser is to ________.

A) make the revenue accounts equal to zero via the Income Summary account

B) make the Income Summary account equal to zero via the Dividends account

C) make the expense accounts equal to zero via the Income Summary account

D) make the Income Summary account equal to zero via the Retained Earnings account

Which one of the following items requires an adjustment on the bank side of the bank

reconciliation?

A) interest earned

B) a bank service charge

C) a note collected by the bank

D) deposits in transit

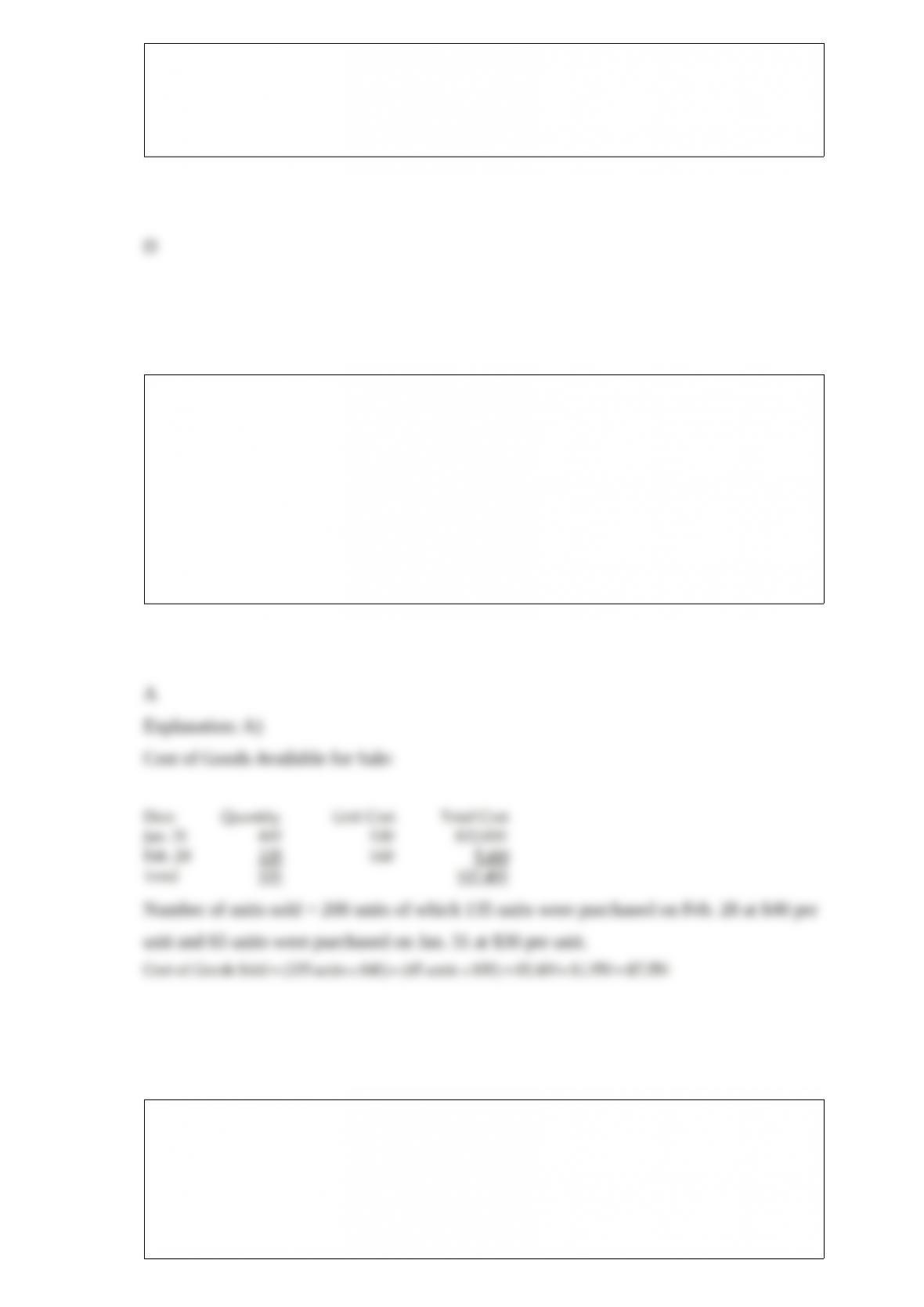

A company purchased 400 units for $30 each on January 31. It purchased 135 units for

$40 each on February 28. It sold 200 units for $55 each from March 1 through

December 31. If the company uses the last-in, first-out inventory costing method, what

is the amount of Cost of Goods Sold on the income statement for the year ending

December 31? (Assume that the company uses a perpetual inventory system.)

A) $7,350

B) $5,400

C) $12,000

D) $17,400

A restaurant is being sued because a customer claims to have found a bug in her chili.

The company’s lawyers believe there is only a remote possibility that the lawsuit will

result in an actual liability. Which of the following actions should be taken by the

company’s management?

A) The situation should be described in a note to the financial statements.

B) The possible liability should not be shown in the financial statements.

C) The liability should be estimated and accrued as an expense.

D) An expense must be matched to the period in which the incident occurred.

The bank statement reveals an EFT received from a customer that has not yet been

recorded in the journal. How would this information be included on the bank

reconciliation?

A) an addition on the bank side

B) a deduction on the bank side

C) a deduction on the book side

D) an addition on the book side

Evaluated Receipts Settlement is ________.

A) a streamlined process that bypasses paper documents altogether

B) a process that eliminates the need for separation of duties

C) a procedure that compresses the payment approval process into a single step by

comparing the receiving report to the purchase order

D) an organizational plan and all the related measures adopted by an entity to safeguard

assets, encourage employees to follow company policies, promote operational

efficiency, and ensure accurate and reliable accounting records

Under the perpetual inventory system, when a seller grants a sales allowance,

________.

A) Merchandise Inventory is debited

B) a credit memo is issued

C) Estimated Refunds Payable are increased

D) the seller receives any nonstandard goods

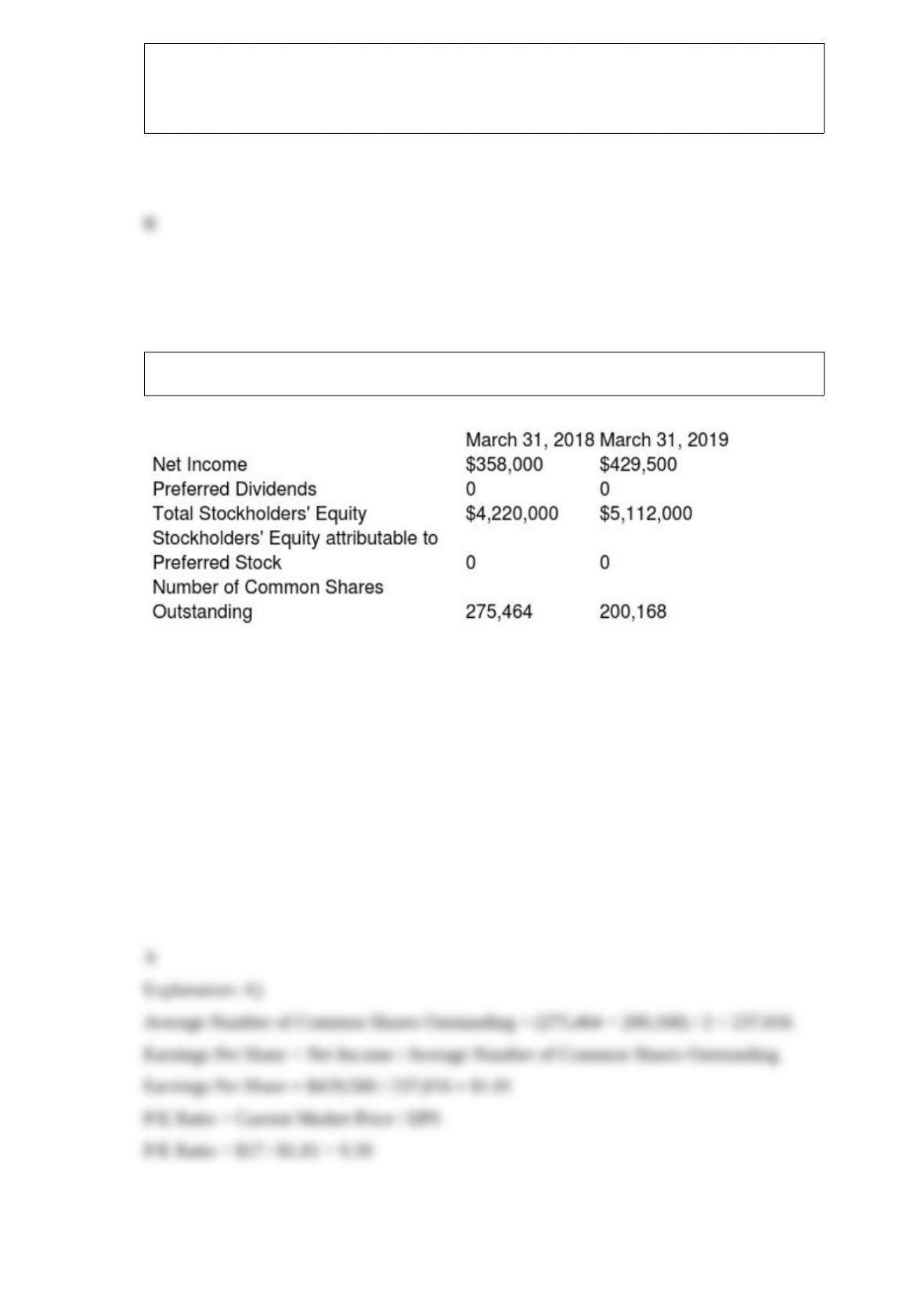

Rather Corporation’s annual report is as follows.

If the current market price is $17 on March 31, 2019, compute the price/earnings ratio on

March 31, 2019. (Round any intermediate calculations and your final answer to the nearest

cent.)

A) 9.39

B) 2.15

C) 1.81

D) 7.91

The profit margin ratio ________.

A) focuses on the liquidity of the business

B) is computed by dividing net sales by net income

C) shows how much gross profit a business earns on every $1.00 of sales

D) is often compared to the industry average

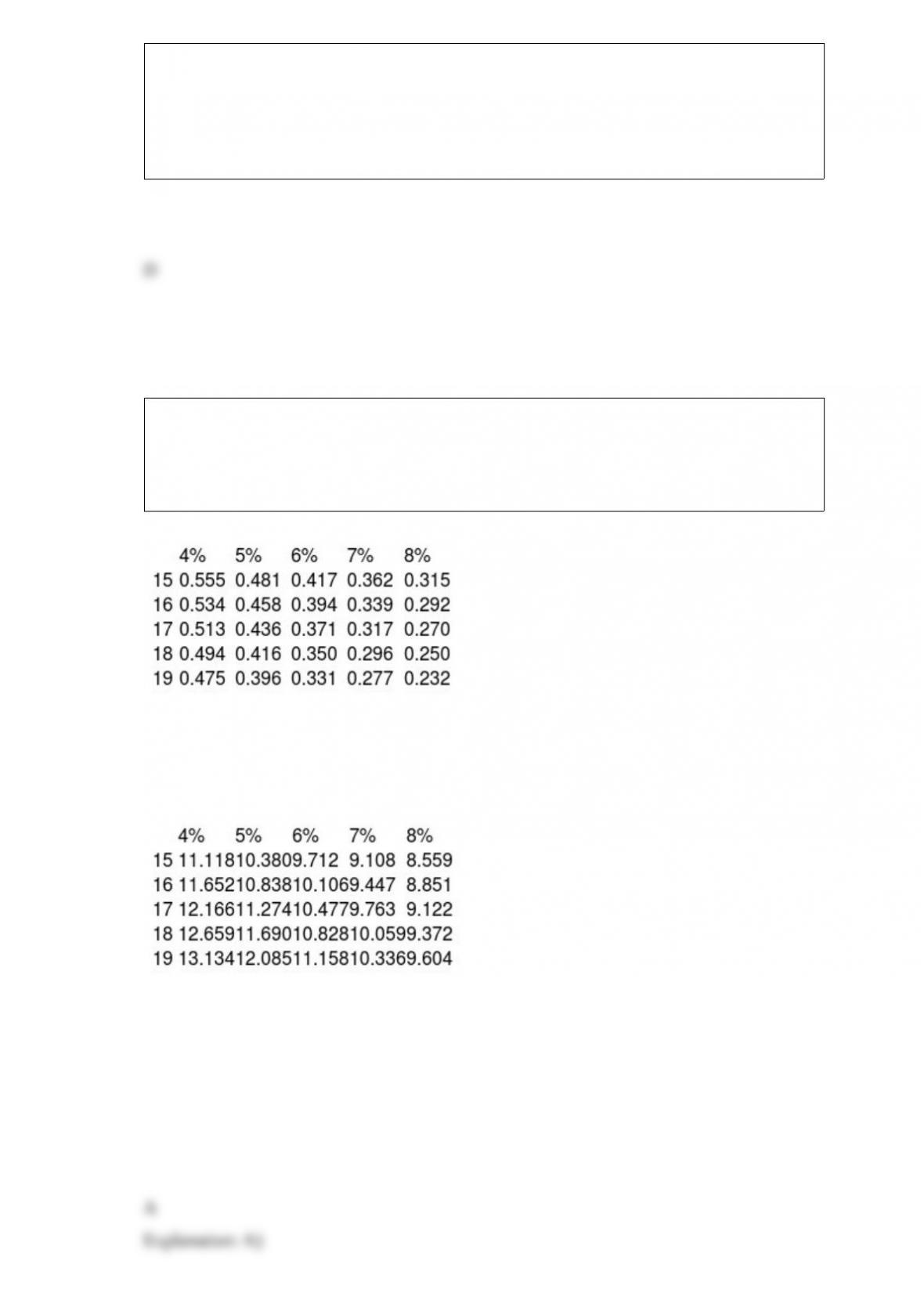

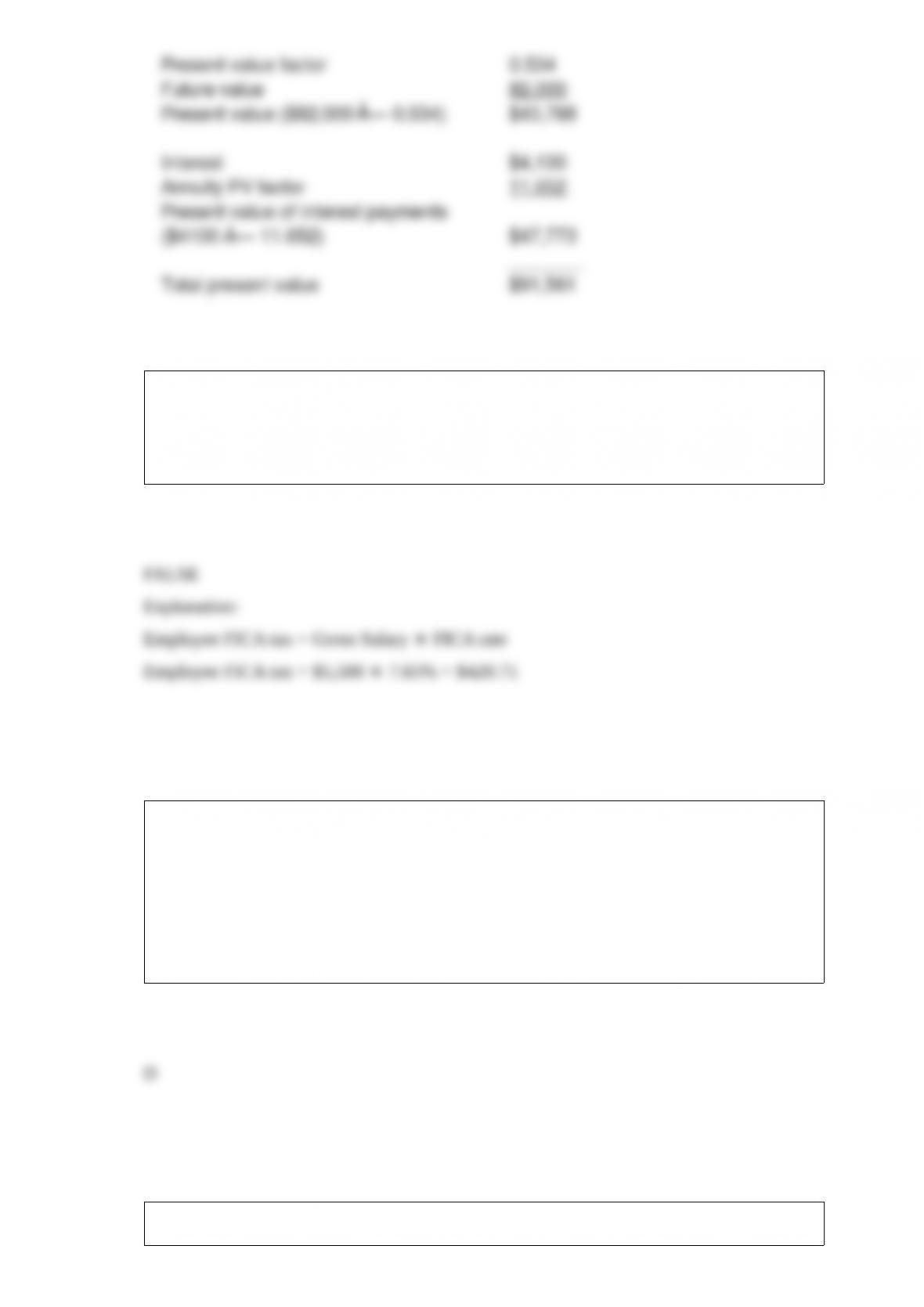

The face value is $82,000, the stated rate is 10%, and the term of the bond is eight

years. The bond pays interest semiannually. At the time of issue, the market rate is 8%.

What is the present value of the bond at the issue date?

Present value of $1:

Present value of ordinary annuity of $1:

A) $91,561

B) $47,773

C) $43,673

D) $84,788

Andrew, an employee of Super Retailer, Inc., has gross salary for March of $5,500. The

entire amount is under the OASDI limit of $118,500 and thus subject to FICA. The total

amount of employee FICA tax is $841.50. (Assume a FICA—OASDI Tax of 6.2% and

FICA—Medicare Tax of 1.45%.)

The Income Summary account has a credit balance of $27,000 after the revenue and

expense accounts have been closed. Which of the following is credited to close the

Income Summary account?

A) Dividends

B) Sales Revenue

C) Cost of Goods Sold

D) Retained Earnings

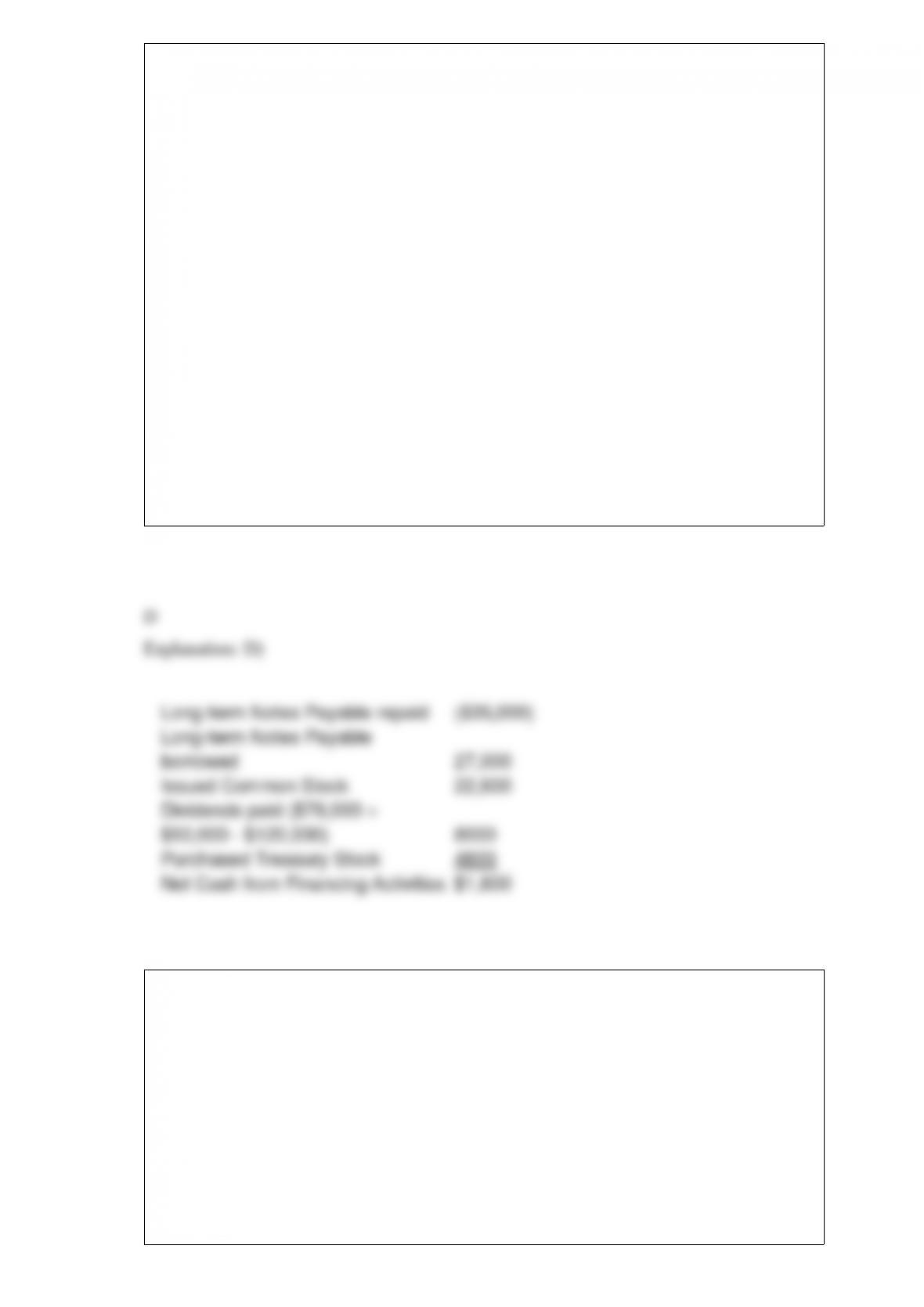

Oklahoma Corp. uses the indirect method to prepare its statement of cash flows. Refer

to the following information for 2018:

1. Long-Term Notes Payable, beginning balance, $84,000

2. Long-Term Notes Payable, ending balance, $99,000

3. Common Stock, beginning balance, $3400

4. Common Stock, ending balance, $26,000

5. Retained Earnings, beginning balance, $78,000

6. Retained Earnings, ending balance, $120,000

7. Treasury Stock, beginning balance, $5800

8. Treasury Stock, ending balance, $10,600

9. No stock was retired.

10. No treasury stock was sold.

11. During 2018, the company repaid $35,000 of long-term notes payable.

12. During 2018, the company borrowed $27,000 on new long-term notes payable.

13. Net income for the year was $50,000.

14. Assume all dividends declared during the year were paid.

What is the net cash provided by financing activities?

A) $17,800

B) $9800

C) ($8000)

D) $1800

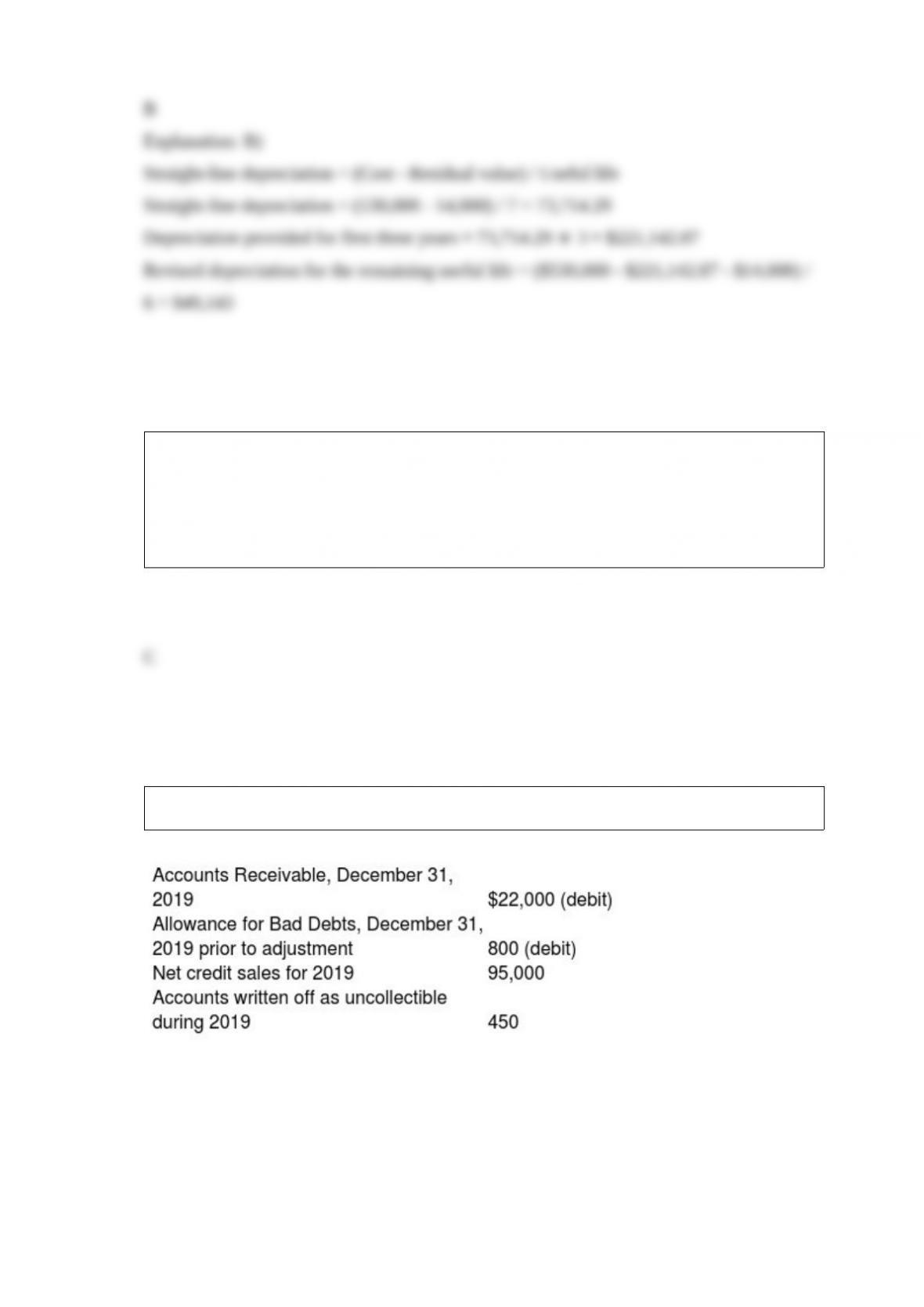

Carpenters, Inc., a manufacturing company, acquired equipment on January 1, 2017 for

$530,000. Estimated useful life of the equipment was seven years and the estimated

residual value was $14,000. On January 1, 2020, after using the equipment for three

years, the total estimated useful life has been revised to nine total years. Residual value

remains unchanged. The company uses the straight-line method of depreciation.

Calculate depreciation expense for 2020. (Round any intermediate calculations to two

decimal places, and your final answer to the nearest dollar.)

A) $50,476

B) $49,143

C) $58,889

D) $57,333

Which of the following is true of freight in?

A) It is an administrative expense.

B) It is a selling expense.

C) It is the transportation cost on purchases.

D) It is the transportation cost on sales.

The following information is from the records of Chicago Photography:

Bad debts expense is estimated by the aging-of-receivables method. Management

estimates that $2,850 of accounts receivable will be uncollectible. Calculate the amount of

net accounts receivable after the adjustment for bad debts.

A) $19,950

B) $19,150

C) $18,350

D) $17,900

Which of the following accounts increases with a debit?

A) Prepaid Rent

B) Interest Payable

C) Accounts Payable

D) Common Stock

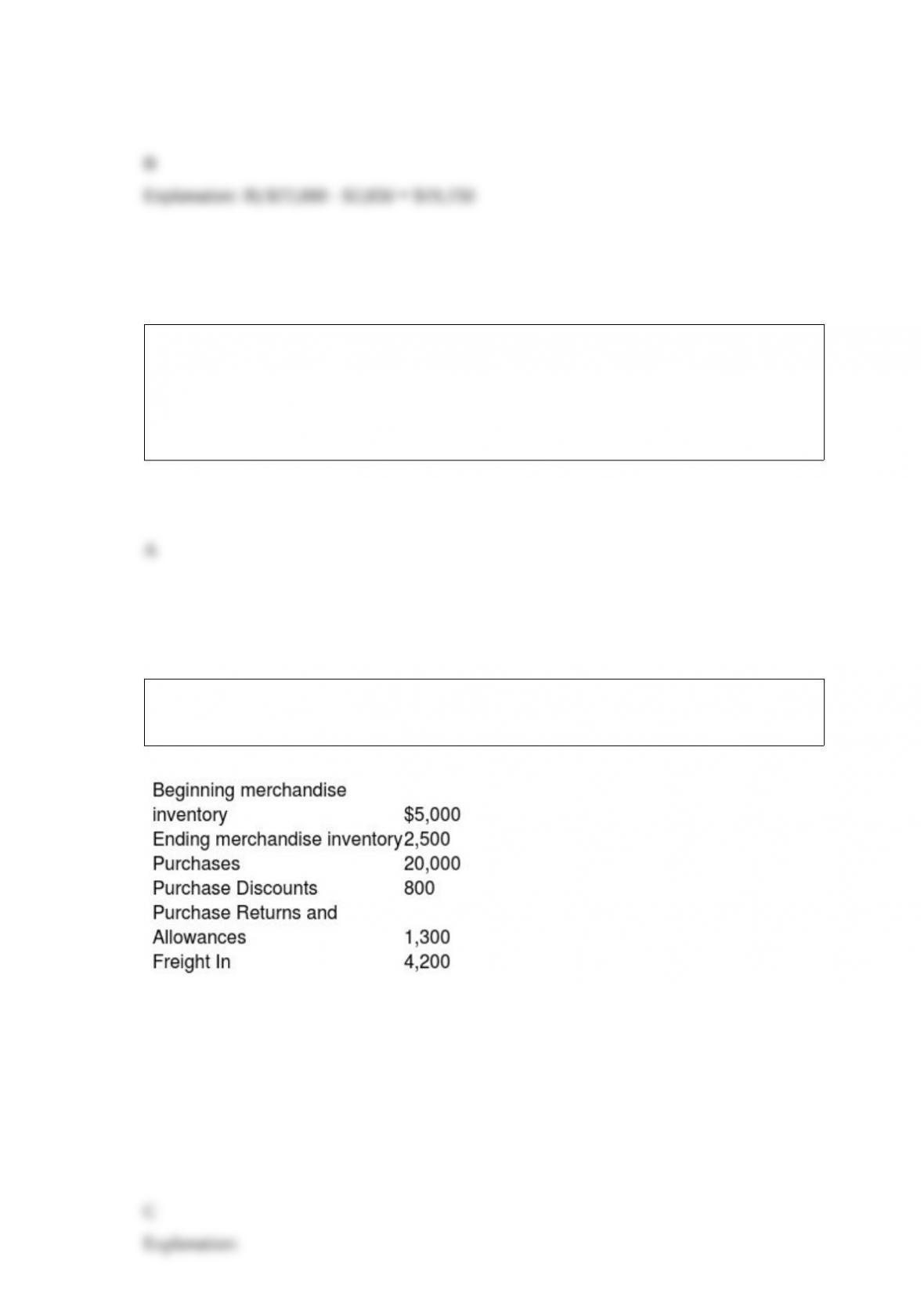

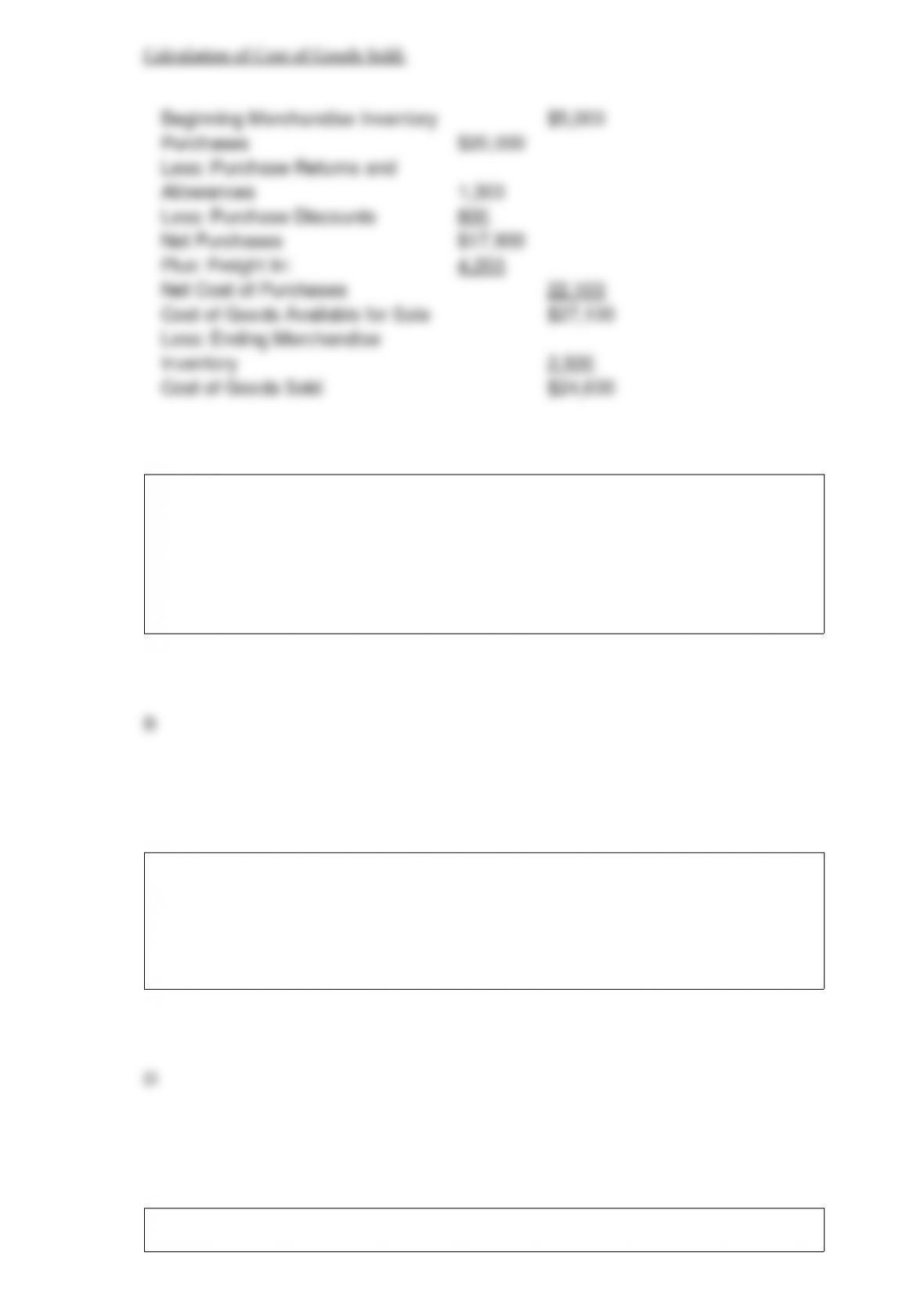

Robin, Inc. uses a periodic inventory system. Use the following details to calculate the

cost of goods sold.

A) $22,100

B) $17,900

C) $24,600

D) $27,100

Mars Electronic Company receives cash from a stockholder, John Tilden, and issues

common stock to him. The two accounts involved in this transaction are ________.

A) Accounts Payable and Cash

B) Cash and Common Stock

C) Common Stock and Accounts Payable

D) Common Stock and Accounts Receivable

Which of the following is NOT included as furniture and fixtures?

A) file cabinets

B) shelving

C) display racks

D) computers

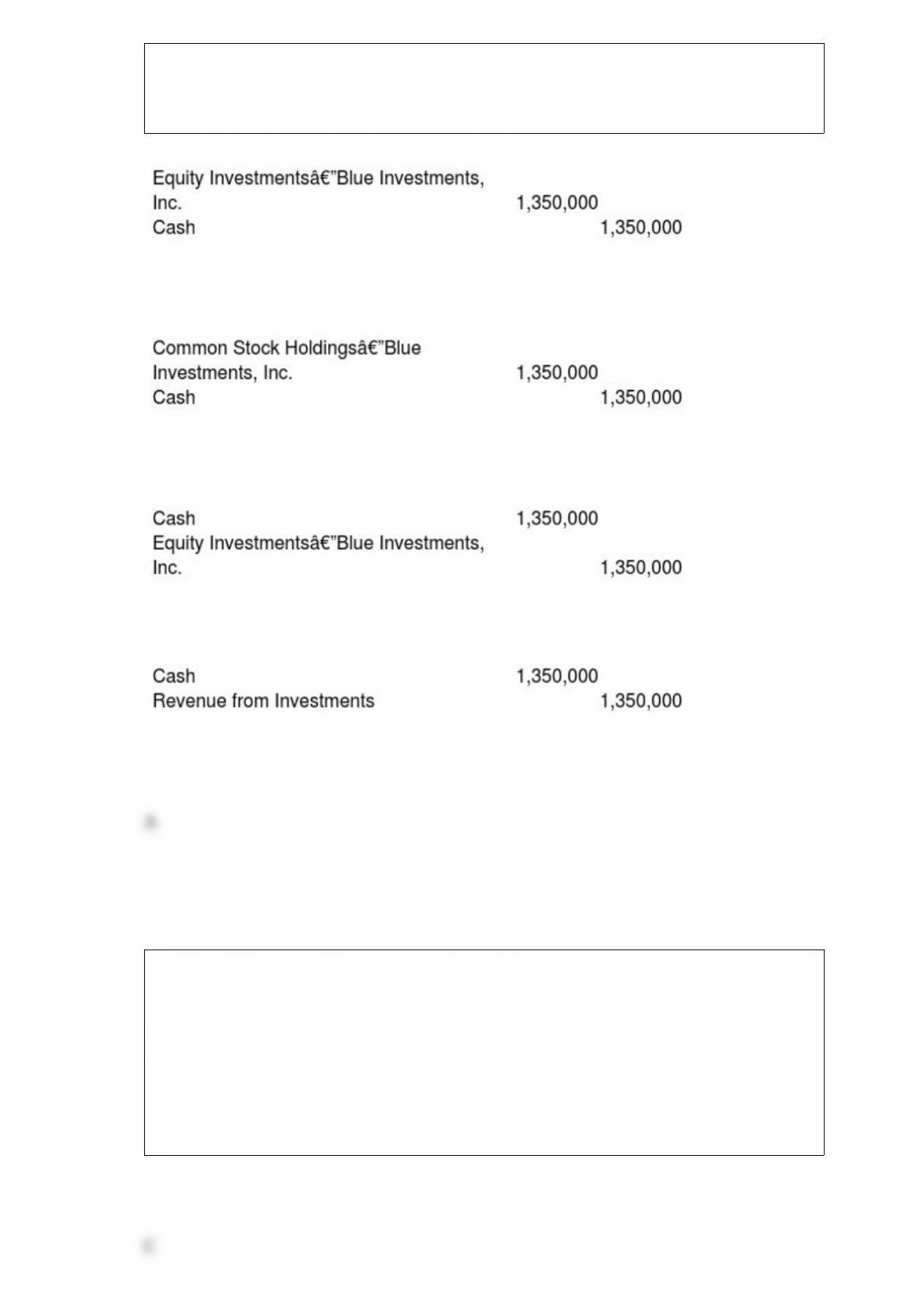

Premier Services, Inc. pays $1,350,000 to acquire 38% of voting stock of Blue

Investments, Inc. on March 5, 2019. Which of the following is the correct journal entry

for the transaction?

A)

B)

C)

D)

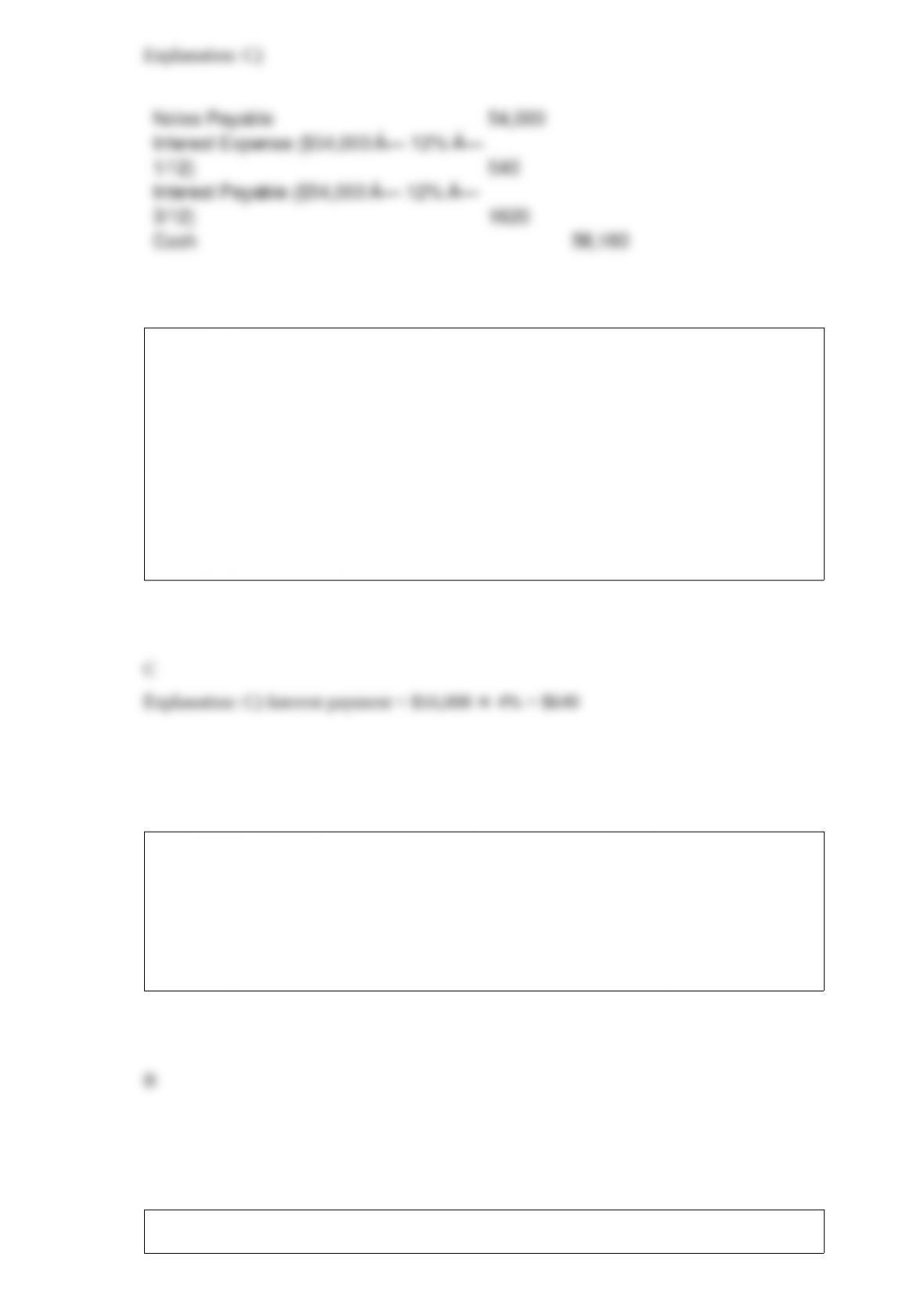

A $54,000, four-month, 12% note payable was issued on October 1, 2018. Which of the

following would be included in the journal entry required on the note’s maturity date by

the borrower? (Do not round any intermediate calculations, and round your final answer

to the nearest dollar.)

A) a credit to Note payable for $56,160

B) a credit to Cash for $54,000

C) a debit to Interest expense for $540

D) a debit to Interest payable for $540

On March 1, 2018, Everson Services issued a 4% long-term notes payable for $16,000.

It is payable over a 4-year term in $4000 annual principal payments on March 1 of each

year plus interest, beginning March 1, 2019. Each yearly installment will include both

principal repayment of $4000 and interest payment for the preceding one-year period.

On March 1, 2019, ________. The accounting period ends on December 31.

A) Everson must accrue $4000 of Interest Expense

B) Everson must accrue the next note payment of $4000 as the current portion of

principal payment

C) Everson must pay $640 of interest to the note holder

D) Everson will receive $4000 as an installment payment

IFRS permits the presentation of plant assets at their fair market value because

________.

A) U. S. GAAP requires this presentation

B) fair market value may be more relevant

C) fair market value is easier to compute than book value

D) financial statements users are indifferent as to how plant assets are presented

Unearned revenue is recorded when ________.

A) revenue will be both collected and earned in the future

B) the business has collected cash, but not yet earned the revenue

C) revenue has been collected and earned during the same accounting period

D) the business has earned, but not collected, cash for the revenue

Beverly Dalton incorporated her CPA practice in 2013. At that time, the corporation

purchased land for $29,000. The December 31, 2019 market value of the land is

$85,000. On the December 31, 2019 balance sheet, this asset should be reported at

________ under U.S. GAAP and at ________ under international reporting standards.

A) $29,000; $29,000

B) $85,000; $85,000

C) $29,000; $85,000

D) $85,000; $29,000

Provide definitions for the following types of investments.

a. Held-to-maturity debt investment

b. Significant influence equity investment

c. Trading debt investment

Mitchell Company receives a bill from one of its suppliers for advertising services

received and will pay the supplier next month. How does the receipt of the bill from the

supplier affect the accounting equation of Mitchell?

A) Assets and equity decrease.

B) Liabilities increase and equity decreases.

C) Assets and liabilities increase.

D) Liabilities and equity increase.

In which of the columns of a worksheet would a net loss be found?

A) in the balance sheet credit column and the income statement debit column

B) in the balance sheet debit column and the income statement credit column

C) in the unadjusted trial balance credit column, the adjusted trial balance credit

column, and the balance sheet credit column

D) in the unadjusted trial balance debit column, the adjusted trial balance debit column,

and the balance sheet debit column