Baldwin Company had 40,000 shares of common stock outstanding on January 1,

2016. On April 1, 2016, the company issued 20,000 shares of common stock. The

company had outstanding fully vested incentive stock options for 10,000 shares

exercisable at $10 that had not been exercised by its executives. The average market

price of common stock for the year was $12. What number of shares of stock (rounded)

should be used in computing diluted earnings per share?

a. 65,000.

b. 56,667.

c. 55,000.

d. 46,667.

Yamaha Inc. hires a new chief financial officer and promises to pay him a lump-sum

bonus four years after he joins the company. The new CFO insists that the company

invest an amount of money at the beginning of each year in a 7% fixed rate investment

fund to insure the bonus will be available. To determine the amount that must be

invested each year, a computation must be made using the formula for:

a. The future value of a deferred annuity.

b. The future value of an ordinary annuity.

c. The future value of an annuity due.

d. None of these answer choices is correct.

Which of the following would not be accounted for using the prospective approach?

a. A change to LIFO from FIFO for inventory costing.

b. A change in price indexes used under the LIFO method of inventory costing.

c. A change in estimate.

d. A change from the cash basis to accrual accounting.

The fair value of debt securities not regularly traded can be most reasonably

approximated by:

a. Calculating the discounted present value of the principal and interest payments.

b. Determining the value using similar securities in the NASDAQ market.

c. Using the relative fair value method.

d. Calling a licensed and registered stockbroker.

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2015. Collections on this sale were $20,000 in 2015, $15,000 in

2016, and $20,000 in 2017.

In its 2015 year-end balance sheet, Reliable would report installment receivables (net)

of:

a. $20,000.

b. $35,000.

c. $25,909.

d. $10,000.

All else equal, a large increase in deferred revenue in the current period would be

expected to produce what effect on revenue in a future period?

a. Large increase, because deferred revenue becomes revenue when the seller has

satisfied its performance obligations.

b. Large decrease, because deferred revenue implies that less revenue has been earned,

which reduces future revenue.

c. No effect, because deferred revenue is a liability, so payment will use assets rather

than providing revenue.

d. Large decrease, because deferred revenue indicates collection problems that will

reduce net revenues in future periods.

Alamos Co. exchanged equipment and $18,000 cash for similar equipment. The book

value and the fair value of the old equipment were $82,000 and $90,000, respectively.

Assuming that the exchange lacks commercial substance, Alamos would record a gain/

(loss) of:

a. $26,000.

b. $ 8,000.

c. $(8,000).

d. $ 0.

Prior to 2016, Trapper John Inc. used sum-of-the-years’-digits depreciation on its store

equipment. Beginning in 2016, Trapper John decided to use straight-line depreciation

for these assets. The equipment cost $3 million when it was purchased at the beginning

of 2014, had an estimated useful life of five years and no estimated residual value. To

account for the change in 2016, Trapper John:

a. Would retrospectively report $600,000 in depreciation expense annually for 2014 and

2015, and report $600,000 in depreciation expense for 2016.

b. Would adjust accumulated depreciation and retained earnings for the excess charges

made in 2014 and 2015.

c. Would report depreciation expense of $400,000 in its 2016 income statement.

d. None of these answer choices is correct.

Productive assets that are physically consumed in operations are:

a. Equipment.

b. Land.

c. Land improvements.

d. Natural resources.

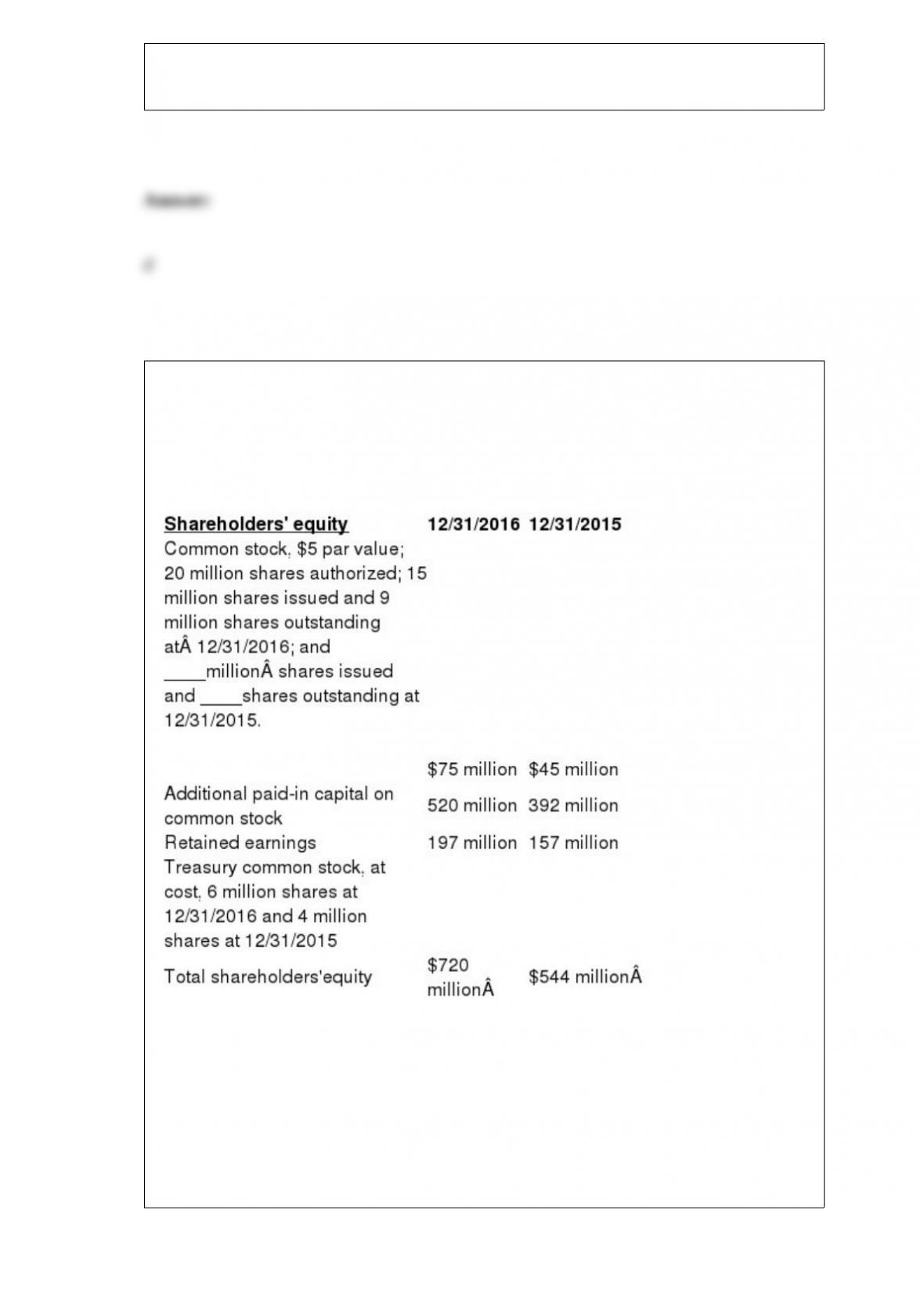

What was the amount of net income earned by Levi during 2016?

The following partial information is taken from the comparative balance sheet of Levi

Corporation:

a. $0.

b. $40 million.

c. $62 million.

d. Cannot be determined from the given information.

In the statement of cash flows, inflows and outflows of cash from buying and selling

trading securities typically are considered:

a. Investing activities.

b. Operating activities.

c. Financing activities.

d. Noncash financing activities.

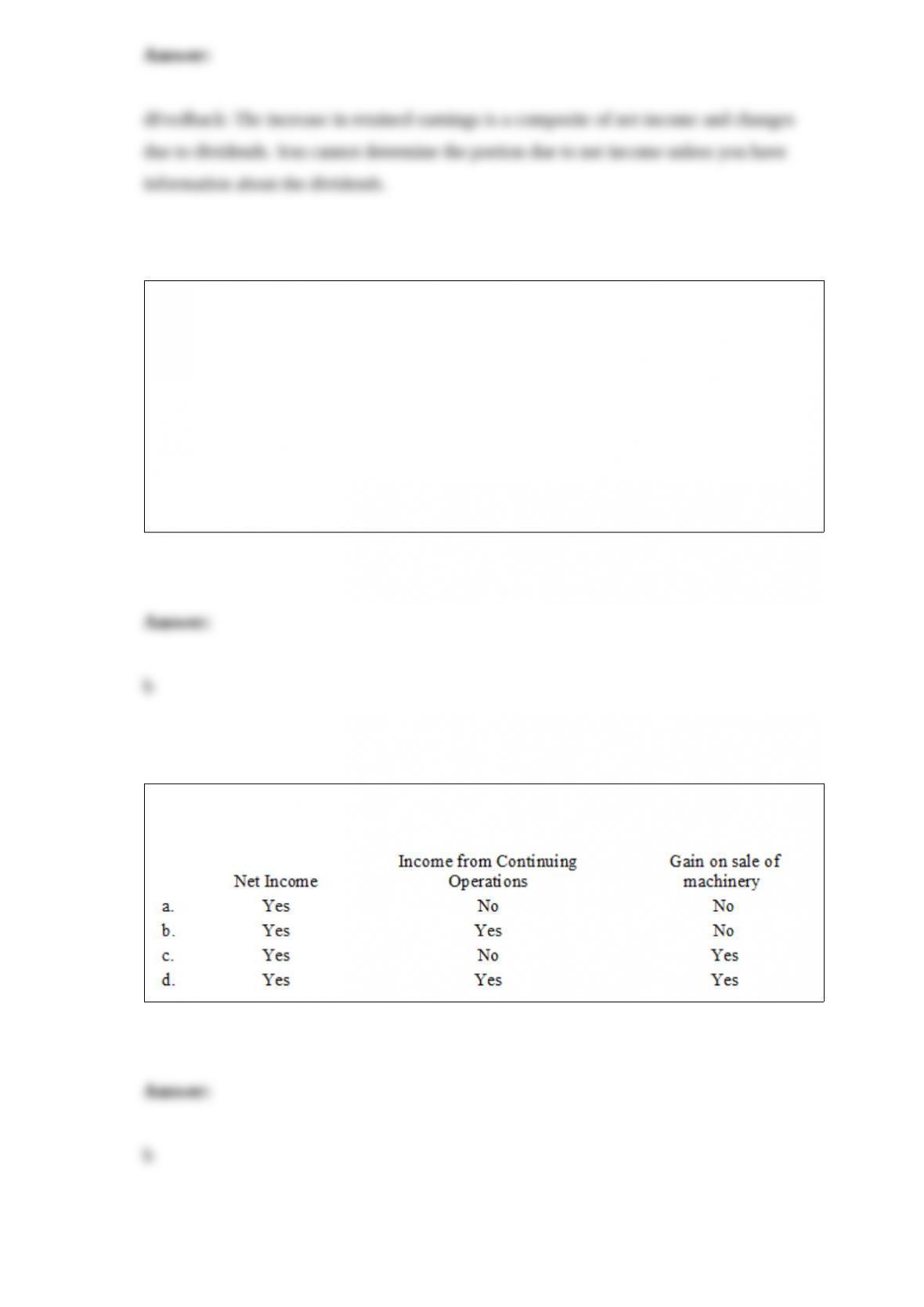

When a company’s income statement includes discontinued operations and a gain on

the sale of machinery, the company should report per share information on:

What is the effect on a company’s cash flows and reported profit from accounting for an

investment as a trading security as compared to accounting for it as an

available-for-sale security?

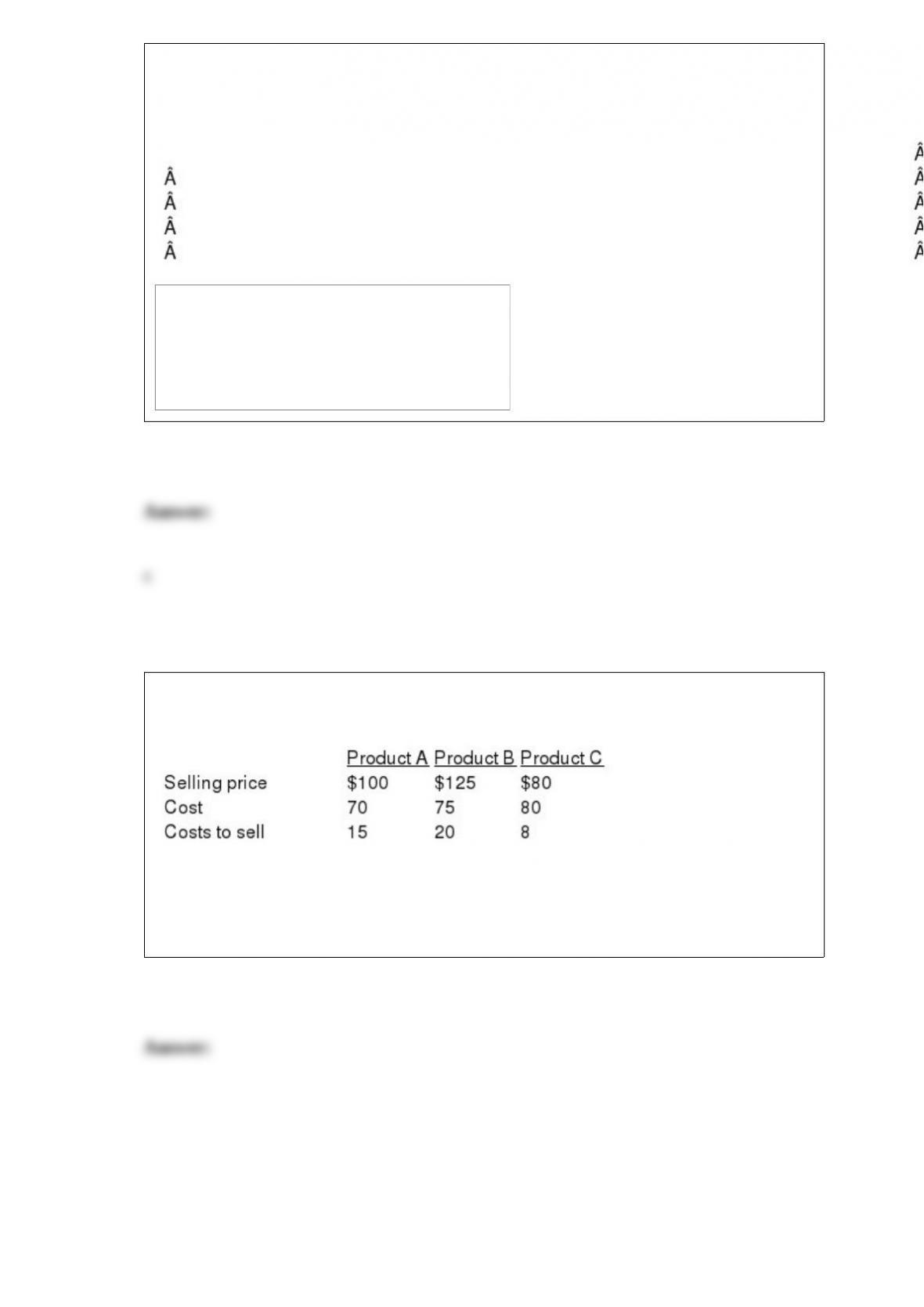

Memphis Wholesale Market applies the lower of cost and net realizable valuation to

individual products and has collected the following data:

Determine the inventory book value for Products A, B, and C assuming that Memphis

Wholesale Market prepares its financial statements according to International Financial

Reporting Standards (IFRS).

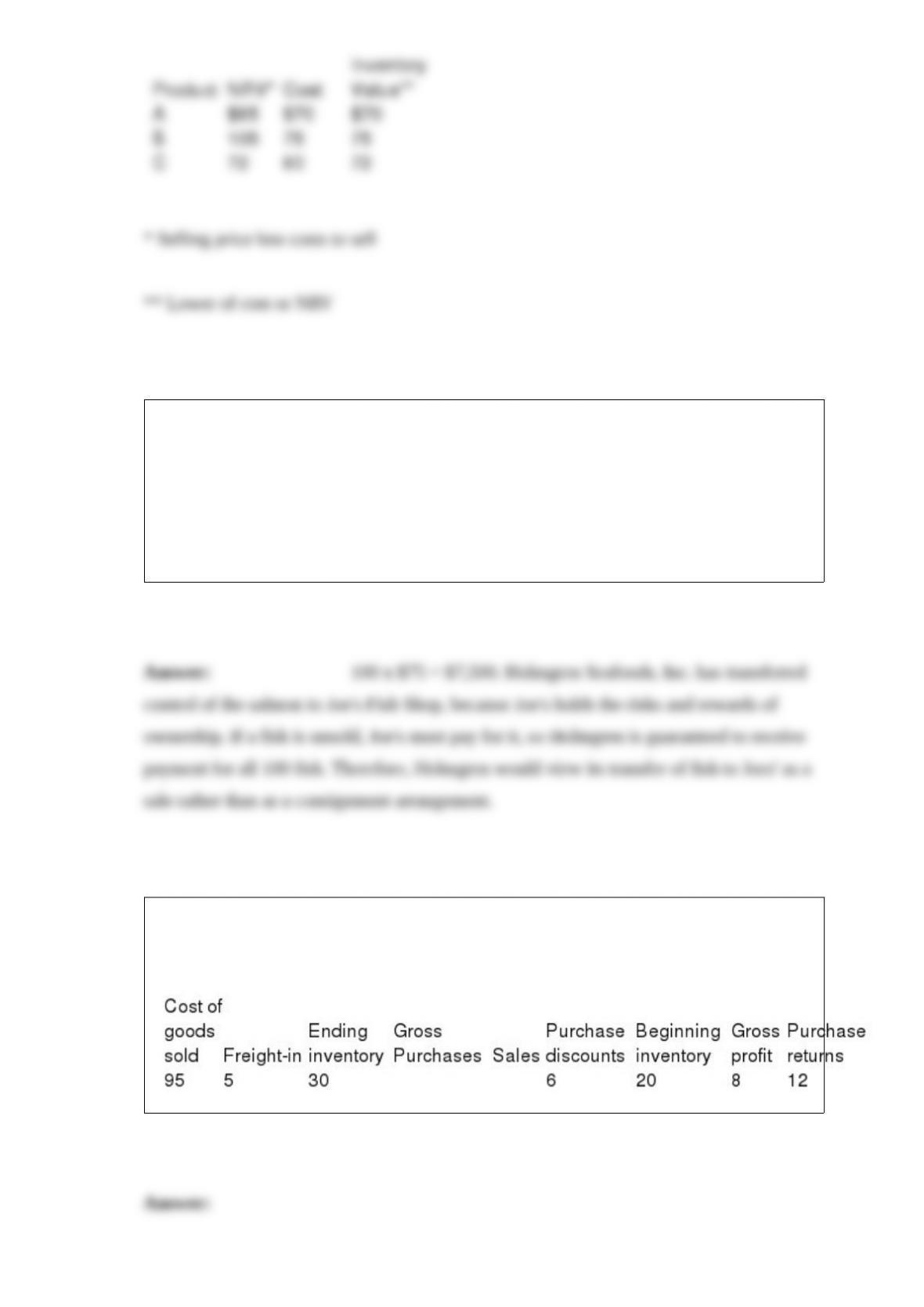

Holmgren Seafoods, Inc. catches and processes salmon and tuna caught off the coast of

Maine. In May 2016, it placed 100 freshly caught wild salmon with a retail price of $75

each in Joe’s Fish Shop. Holmgren’s contract with the shop stipulates that the shop will

earn a 15% commission on each salmon sold. Joe’s is responsible for purchasing any

fish that remain unsold at the end of a three-day period. Required: During the three-day

period, Joe’s Fish Shop was able to sell 88 of the 100 salmon. How much revenue

should Holmgren recognize with respect to this transaction?

The following information is taken from the accounting records of Rapid Runner Inc.

for the year 2016. Missing information has been left blank. Required: Compute the

missing amounts.