1) A company issued long-term notes payable for cash during the year under audit. To

ascertain that this transaction was properly recorded, the auditor’s best course of action

is to:

A) trace the cash received from the issuance to the accounting records

B) confirm the results of the issuance with the underwriter or investment banker

C) verify that the new cash received is credited to an account entitled “Bonds Payable”

D) request a statement from the bond trustee as to the amount of bonds issued and

outstanding

2) Which of the following auditor’s defenses usually means non-reliance on the

financial statements by the user?

A) Lack of duty

B) Non-negligent performance

C) Absence of causal connections

D) Contributory negligence

3) ________ inquiry is used when the auditor seeks responses from the interviewee

about his or her knowledge of an event or circumstance.

A) Assessment

B) Declarative

C) Interrogative

D) Informational

4) Because of the importance of tests of controls and substantive tests of transactions

for acquisitions and cash disbursements, it is common in this audit area to use:

A) block sampling

B) variables sampling

C) attributes sampling

D) probability proportional to size sampling

5) The effectiveness of automated controls depends solely on the competence of the

personnel performing the controls.

A) True

B) False

6) Because of the requirements of Rule 201 of the

A) True

B) False

7) A CPA’s financial interests in nonclients may have an effect on independence if the

nonclients are investors in or investees of the client. Which situation would not impair a

CPA’s independence?

A) The client has an immaterial investment in a nonclient investee in which the CPA

has an immaterial investment

B) The CPA has a material indirect financial interest in a nonclient in which the client

has a material investment

C) The client investor has a nonmaterial investment in the nonclient investee in which

the CPA has a material investment

D) The CPA has a joint closely held investment with the client in a nonclient that is

material to the client as well as the CPA

8) For most audits, a proper cash receipts cutoff is less important than either the sales or

the sales returns and allowances cutoff.

A) True

B) False

9) Which of the following statements best describes the enforceability of the

Interpretations of the Rules of Conduct?

A) The Interpretations are not enforceable

B) The Interpretations are enforceable

C) The Interpretations may be enforceable if they have been reviewed and approved by

the

D) The Interpretations are not enforceable, but a practitioner must justify departure

from them

10) Lewis Corporation has a few large accounts receivable that total one million dollars

whereas

Clark Corporation has many small accounts receivable that total one million dollars.

Misstatement in any one account is more significant for Lewis corporation because of

the concept of:

A) Materiality

B) Audit risk

C) Reasonable assurance

D) Comparative analysis

11) Most public companies’ audited financial statements are available on the SEC’s

EDGAR database.

A) True

B) False

12) When performing compilation services, the accountant is not required to obtain an

understanding of the client’s internal control.

A) True

B) False

13) Most practitioners allocate the preliminary judgment about materiality to balance

sheet accounts.

A) True

B) False

14) According to the Code of Professional Conduct which of the following is true with

respect to records in a CPA’s possession?

A) Extensive analyses of inventory prepared by the client at the auditor’s request are

working papers that belong to the auditor and need not be furnished to the client upon

request

B) The auditor who returns client records must comply with any subsequent requests to

again provide such information

C) A corporation’s consolidating worksheets of their multinational conglomerate belong

to the auditor and need not be furnished to the client upon request

D) An auditor may retain client records if fees due with respect to a completed

engagement have not been paid

15) A nonaudit engagement in which the accountant undertakes to present, in the form

of financial statements, information that is the representation of management, without

undertaking to express any assurance on the statements is called a review engagement.

A) True

B) False

16) Which of the following must be set prior to testing a sample?

A) Sample exception rate

B) Achieved upper precision limit

C) Computed exception rate

D) Tolerable exception rate

17) The tolerable rate of exceptions for tests of controls is generally:

A) lower than the expected rate of errors in the related accounting records

B) higher than the expected rate of errors in the related accounting records

C) identical to the expected rate of errors in the related accounting records

D) unrelated to the expected rate of errors in the related accounting records

18) The audit of year-end physical inventories should include steps to verify that the

client’s purchases and sales cutoffs were adequate. The audit steps should be designed

to detect whether merchandise included in the physical count at year-end was not

recorded as a:

A) sale in the current period

B) sale in the subsequent period

C) purchase in the current period

D) purchase return in the subsequent period

19) Companies with non-complex IT environments often rely on desktops and

networked servers to perform accounting system functions. Which of the following is

not an audit consideration in such an environment?

A) limited reliance on automated controls

B) unauthorized access to master files

C) vulnerability to viruses and other risks

D) excess reliance on automated controls

20) Which of the following is likely to be determined first when performing tests of

details for accounts receivable?

A) Recorded accounts receivable exist

B) Accounts receivable in the aged trial balance agree with related master file amounts,

and the total is correctly added and agrees with the general ledger

C) Accounts receivable are owned

D) Existing accounts receivable are included

21) When part of the client’s inventory is in a public warehouse or in the possession of

other outside custodians, the auditor does not need to observe a physical count of the

inventory if a written confirmation is obtained directly from the inventory custodians.

A) True

B) False

22) One of the ways to eliminate nonsampling risk is through:

A) proper supervision and instruction of the client’s employees

B) proper supervision and instruction of the audit team

C) the use of attributes sampling rather than variables sampling

D) controls which ensure that the sample drawn is random and representative

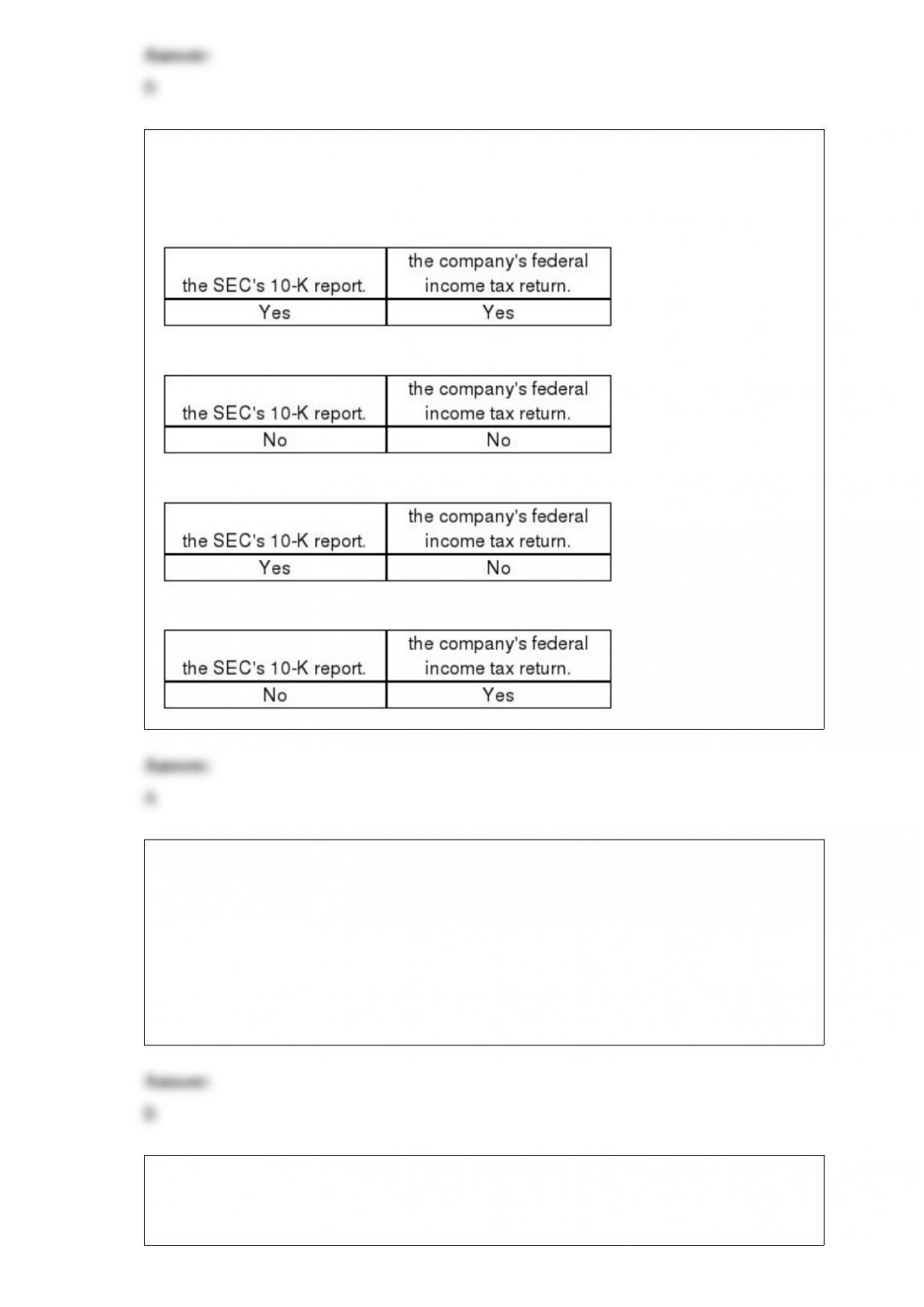

23) The usual audit test for a public company’s officer compensation is to obtain the

authorized salary of each officer from the minutes of the board of directors and compare

it with:

A)

B)

C)

D)

24) Which of the following would have the least amount of importance regarding

controls over the processing of payroll?

A) The person authorized to sign paychecks should not be otherwise involved in the

preparation of the payroll

B) A check-signing machine should not be used to replace a manual signature

C) Distribution of pay checks should be performed by someone who is not involved in

the other payroll functions

D) Unclaimed paychecks should be immediately returned for redeposit

25) The auditor’s responsibility for uncovering direct-effect illegal acts is the same as

for fraud.

A) True

B) False

26) Which of the following is least likely to impair a CPA firm’s independence with

respect to an audit client in the Oklahoma City office of a national CPA firm?

A) A partner in the Oklahoma City office owns an immaterial amount of stock in the

client

B) A partner in the Jersey City office owns 25% of the client’s stock

C) A partner in the Oklahoma City office, who does not work on the audit engagement,

previously served as controller for the audit client

D) A partner in the Chicago office previously served as vice president of finance for the

audit client

27) When auditors apply MUS to a sample, the sample is selected using random

sampling techniques.

A) True

B) False

28) The reliability of evidence refers to the degree to which evidence is considered

believable or trustworthy. There are six factors that affect the reliability of audit

evidence. One factor is the independence of the provider; i.e., evidence obtained from a

source outside the client company is more reliable than that obtained within. Identify

and discuss any two of the remaining five factors:

29) An important concept in contract law for accountants to understand is the

“third-party beneficiary doctrine”. Explain and give an example.

30) Discuss the two circumstances under which auditors would extend their procedures

considerably in the audit of payroll.

31) Discuss the five SSARS requirements that must be met when an accountant is

performing a compilation of financial statements.

32) Discuss each of the following primary documents and records used in the personnel

and employment function in the payroll and personnel cycle: personnel records,

deduction authorization form, and the rate authorization form.