Traditional product costing systems (e.g., job and process costing) are designed

primarily to accumulate cost information for financial reporting.

Answer:

In general, and holding all other things constant, an unfavorable variance decreases

operating profits.

Answer:

If a transfer has no effect on divisional profit, risk-neutral managers will be indifferent

between making the transfer or not.

Answer:

Cost behavior is the most important characteristic for managerial decision making.

Answer:

The differential analysis approach to pricing for special orders could lead to

under-pricing in the long-run because fixed costs are not included in the analysis.

Answer:

One question that an organization’s mission statement should answer is how the

organization will evaluate its performance relative to its competitors.

Answer:

If materials are only added at the beginning of the production process, then the degree

of completion for materials in the ending Work-in-Process Inventory will be the same as

the degree of completion for the conversion costs.

Answer:

One advantage of centralization is better use of top management’s time on strategic

decisions.

Answer:

The range within which fixed costs remain constant as volume of activity varies is

known as the relevant range.

Answer:

In general, weighted-average costing is simpler to use while first-in, first-out (FIFO)

costing provides greater decision-making benefits to managers.

Answer:

Before using activity-based costing (ABC), managers must apply the cost-benefit

principle to the additional recordkeeping costs associated with ABC.

Answer:

Overapplied overhead occurs when the actual overhead costs incurred during a period

are greater than the overhead costs applied during the period.

Answer:

The estimated net realizable value for a product is its estimated selling price after

processing the product beyond the split-off point.

Answer:

The sales quantity variance is the same as the sales activity variance on a flexible

budget performance report.

Answer:

The account analysis method is more subjective than other cost estimation methods

because it relies heavily on the personal judgment and experience of accountants.

Answer:

Budgeting is primarily used to determine year-end bonuses based on managerial and

organizational performance.

Answer:

Activity-based costing (ABC) is a management tool that focuses on the continuous

improvement of all dimensions of a business.

Answer:

In general, the capacity-level costs in an activity-based costing (ABC) system are

variable costs.

Answer:

Activity-based costing (ABC) is a two-stage cost allocation system that (1) allocates

costs to activities and (2) then to products based on their use of the activities.

Answer:

Some variances are the result of accounting errors and omissions, including timing

differences.

Answer:

Properly designed management control systems can totally eliminate the inherent

conflict between individual behavior and organizational goals.

Answer:

Total work-in-process during the period is the sum of the beginning work-in-process

inventory and the total manufacturing costs incurred during the period.

Answer:

The use of residual income reduces, but does not eliminate, the suboptimization

problem.

Answer:

Tax avoidance is unethical when inflated transfer prices are used in international

transactions to shift profits from a division in one country to a division in another

country.

Answer:

From an organization’s viewpoint, transfer prices have no effect on total profits

assuming the transfer occurs between the two responsibility centers.

Answer:

The first step in determining whether a cost is direct or indirect is to specify the cost

allocation rule.

Answer:

The cost driver rate is computed by dividing the total cost per activity by the estimated

number of units produced.

Answer:

The value chain comprises activities from research and development through the

production process, but does not include activities related to the distribution of products

or services.

Answer:

The market share variance is more controllable by the marketing department than the

industry volume variance.

Answer:

Properly designed management control systems will eliminate fraudulent behavior by

maximizing goal congruence within the organization.

Answer:

A transfer made at cost does not motivate the selling division to transfer its goods or

services internally.

Answer:

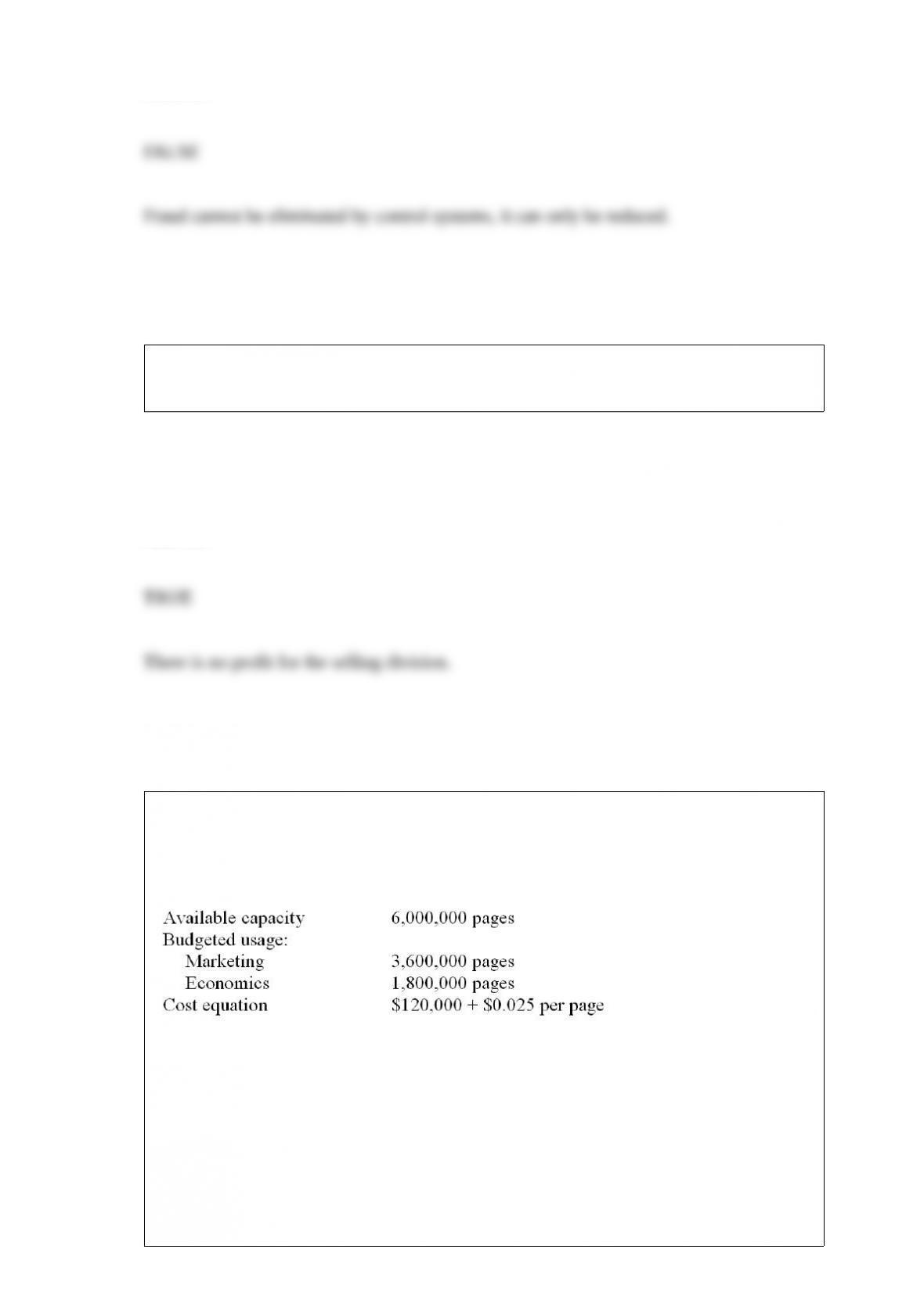

The Copy Department in the College of Business at State University provides

photocopying service for both the Marketing and Economics Department. The

following budget has been prepared for the year.

If the Copy Department uses a dual-rate for allocating its costs, how much cost will be

allocated to the Economics Department, assuming the Economics Department actually

made 2,100,000 copies during the year?

A. $85,000

B. $92,500

C. $132,500

D. $112,500

Answer:

Multiple (departmental) manufacturing overhead rates are considered preferable to a

single (plant wide) overhead rate when (CMA adapted)

A. manufacturing is limited to a single product flowing through identical departments in

a fixed sequence.

B. various products are manufactured that do not pass through the same departments or

use the same manufacturing techniques.

C. individual cost drivers cannot accurately be determined with respect to

cause-and-effect relationships.

D. the single or plant wide rate is related to several identified cost drivers.

Answer:

Scottso Corporation applies overhead using a normal costing approach based upon

machine-hours. Budgeted factory overhead was $232,750, budgeted machine-hours

were 17,500. Actual factory overhead was $227,830, actual machine-hours were

16,150. How much is the over- or underapplied overhead?

A. $13,035 overapplied

B. $13,035 underapplied

C. $4,920 overapplied

D. $4,920 underapplied

Answer:

What is the allocation rate for the upcoming year assuming Boxes-2-Go uses the

single-rate method and allocates common costs based on the time on the network?

A. $10.98

B. $10.00

C. $8.00

D. $7.14

Answer:

When managers are held responsible for costs and the input-output relationship is well

specified, a(n) ________________________ is established.

A. standard cost center

B. revenue center

C. discretionary cost center

D. asset center

Answer:

The Scottso Corporation has budgeted fixed costs of $225,000 and an estimated selling

price of $24 per unit. The variable cost ratio is 40% and the company plans to sell

48,000 units in 2010.

Required:

(a) Compute the break-even point in units.

(b) Compute the margin of safety (in units) for 2010.

(c) Compute the expected operating profit for 2010.

Answer:

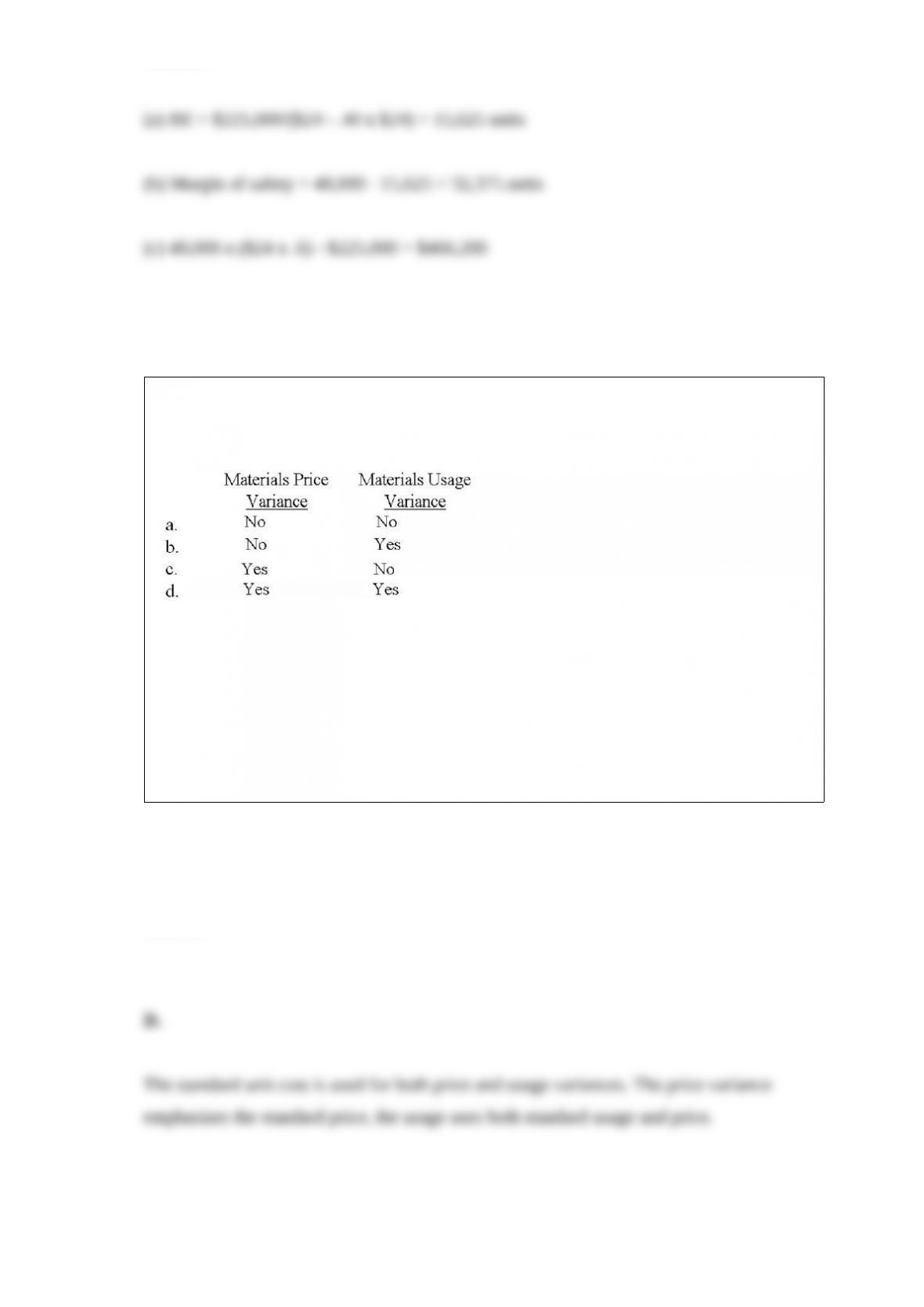

The standard unit cost is used in the calculation of which of the following variance?

(CPA adapted)

A. a

B. b

C. c

D. d

Answer:

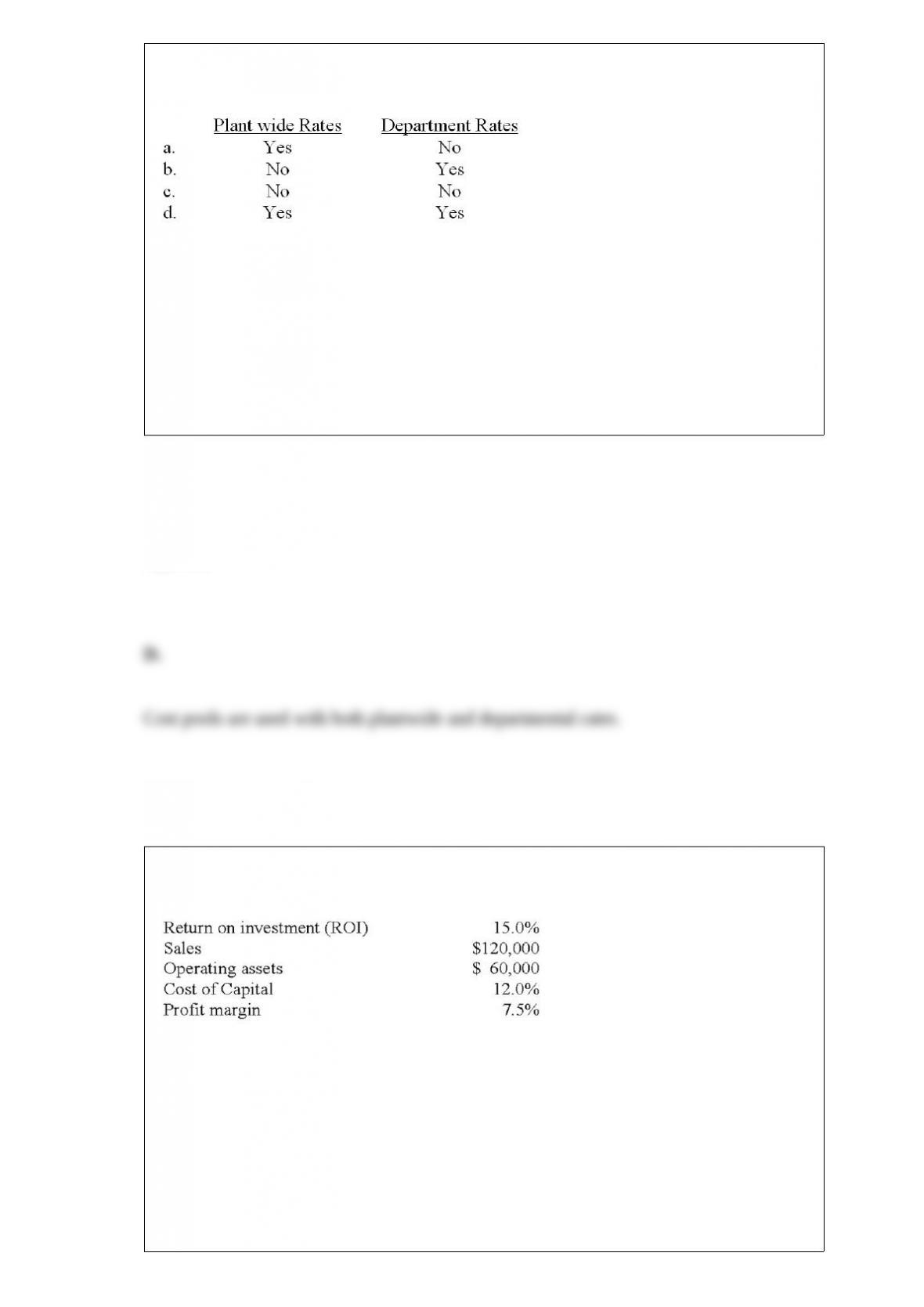

Cost pools are used with

A. a

B. b

C. c

D. d

Answer:

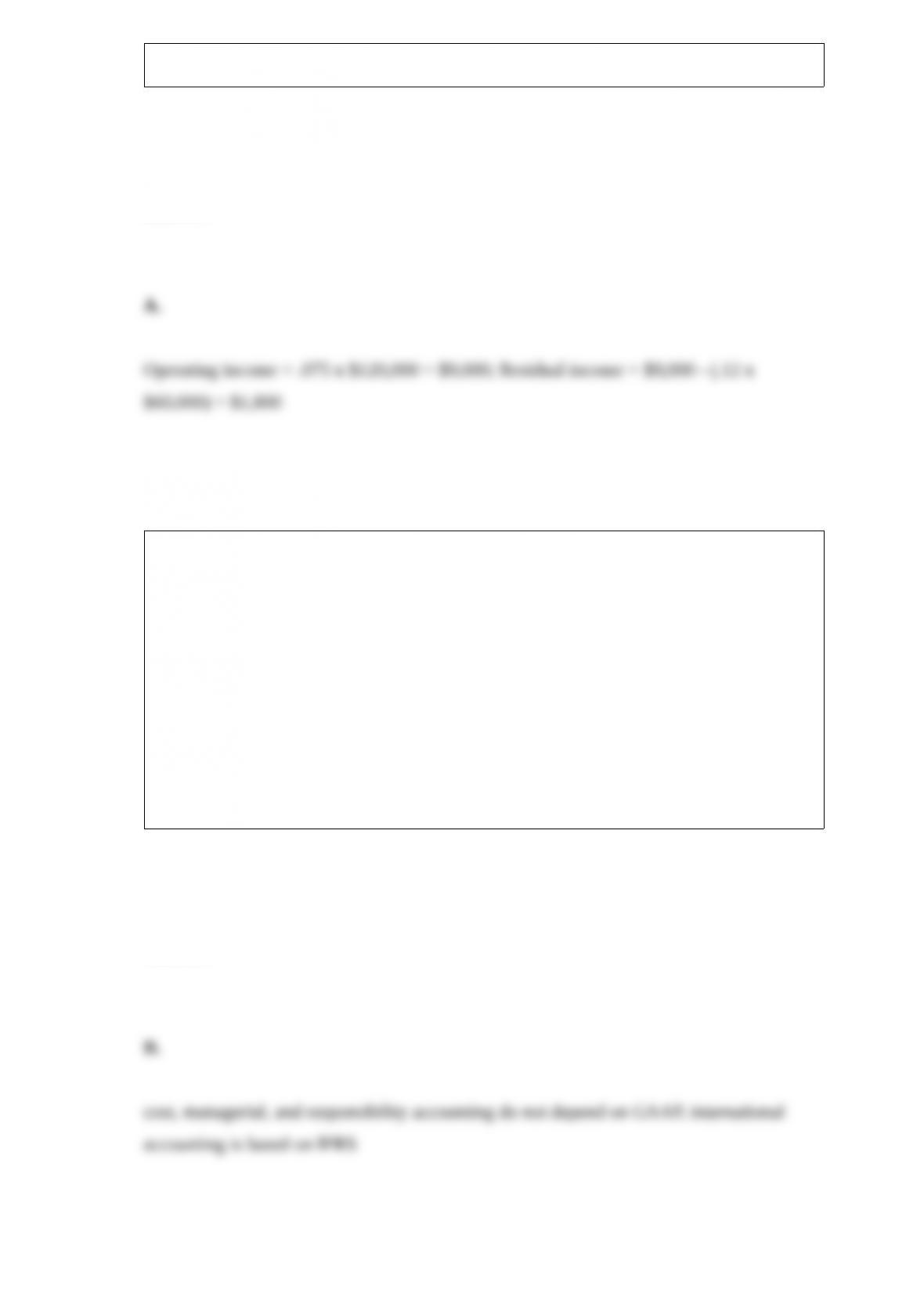

The following information has been gathered for the Green Division:

Compute the Green Division’s residual income.

A. $1,800

B. $2,700

C. $3,600

D. $5,400

Answer:

The field of accounting that depends on generally accepted accounting principles

(GAAP) is called

A. cost accounting.

B. financial accounting.

C. managerial accounting.

D. responsibility accounting.

E. international accounting.

Answer:

Fleury Inc has 9,600 machine hours available each month. The following information

on the company’s three products is available:

a) What production schedule will maximize the company’s profits?

b) What will be the maximum possible contribution margin?

Answer:

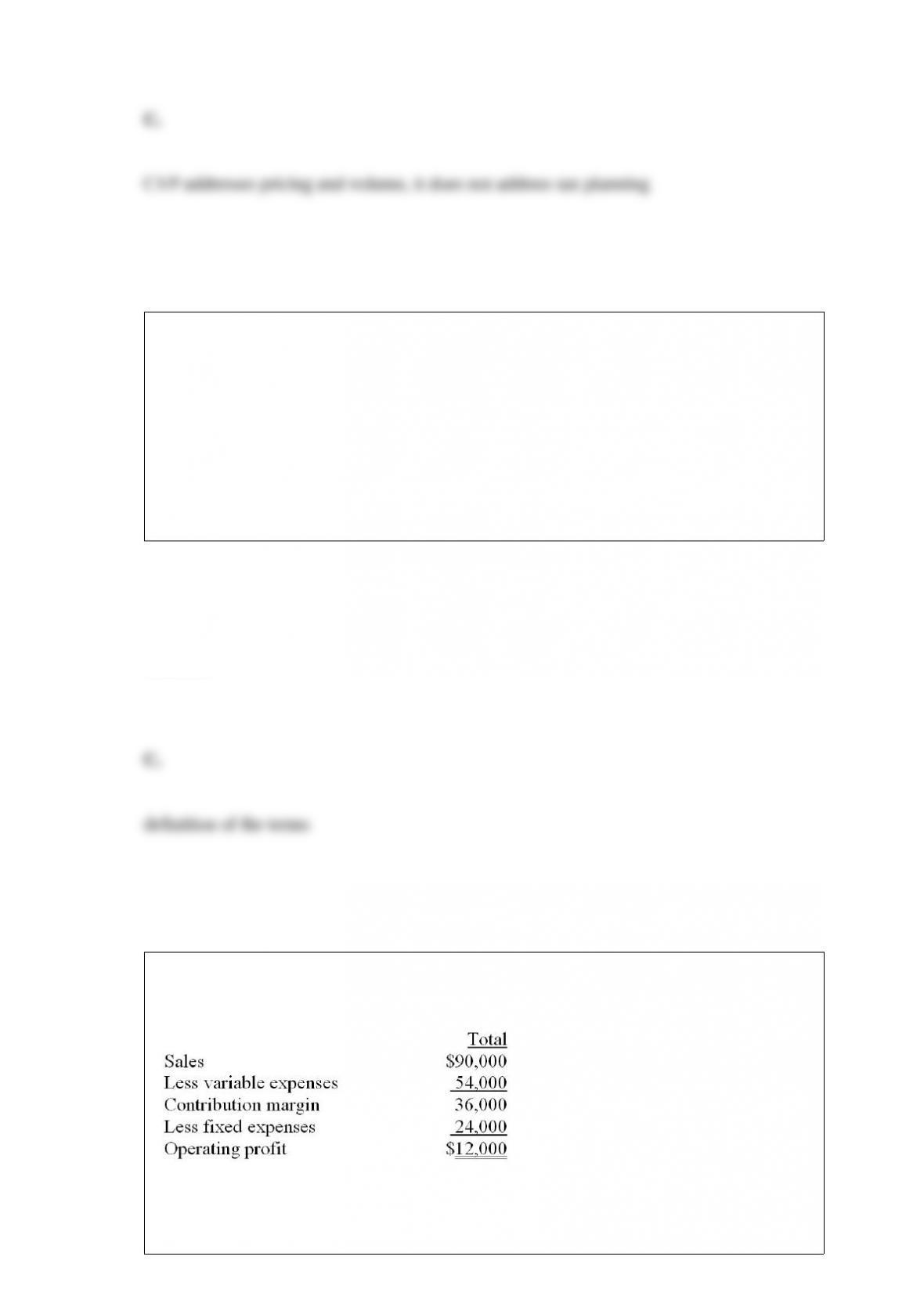

Cost-volume-profit (CVP) analysis is a simple but powerful tool to assist management

make operating decisions. Which of the following does not represent a potential use of

CVP analysis?

A. Ability to compute the break-even point.

B. Ability to determine optimal sales volumes.

C. Aids in evaluating tax planning alternatives.

D. Aids in determining optimal pricing policies.

Answer:

In the cost equation TC = F + VX, V is best described as the:

A. costs that do not vary with changes in the activity level.

B. intercept of the cost equation.

C. slope of the cost equation.

D. activity level used to estimate the dependent variable.

Answer:

You have been provided with the following information:

If sales decrease by 10%, what level of fixed expenses will maintain the current

operating profit?

A. $12,000.

B. $20,400.

C. $21,600.

D. $24,000.

Answer:

According to the Institute of Management Accountants (IMA), the first step in

resolving an ethical dilemma is to

A. resign from the organization.

B. call the IMA’s ethics hotline.

C. report the circumstances to a local newspaper.

D. consult with an objective, independent advisor.

E. discuss the situation with an immediate supervisor.

Answer:

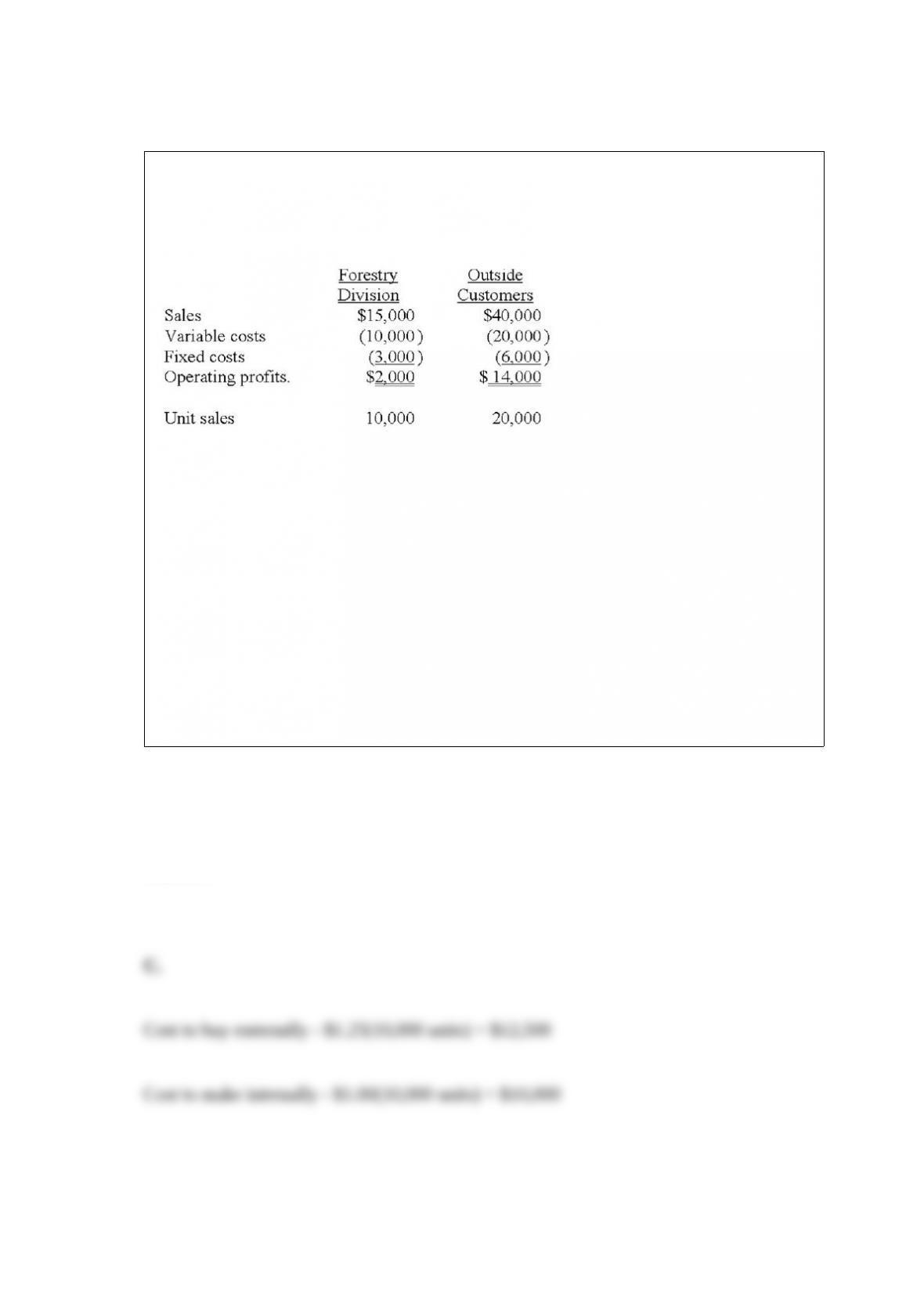

The Blade Division of Axe Company produces hardened steel blades. One-third of

Blade’s output is sold to the Forestry Products Division of Axe; the remainder is sold to

outside customers. Blades’ estimated operating profit for the year is:

The Forestry Division has an opportunity to purchase 10,000 blades of the same quality

from an outside supplier on a continuing basis. The Blade Division cannot sell any

additional products to outside customers. Should the Axe Company allow its Forestry

Division to purchase the blades from the outside supplier at $1.25 per unit?

A. No; making the blades will save Axe $1,500.

B. Yes; buying the blades will save Axe $1,500.

C. No; making the blades will save Axe $2,500.

D. Yes; buying the blades will save Axe $2,500.

Answer:

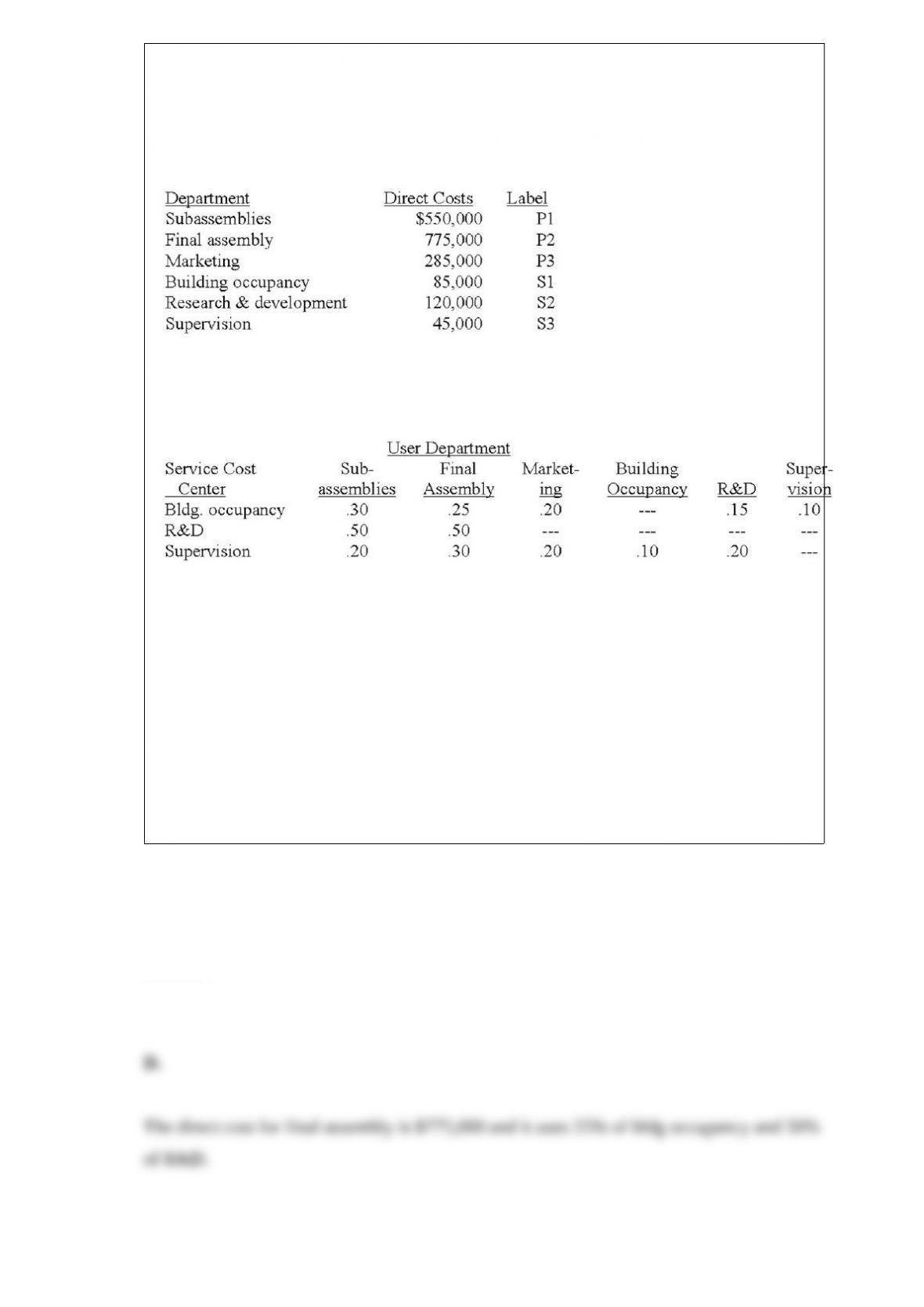

The following set up is a system of simultaneous linear equations to allocate costs

using reciprocal method. Matrix algebra is not required.

The following costs were incurred in three operating departments and three service

departments in Reality Company.

Use of services by other departments is as follows.

The equation for department P2 (final assembly) is

A. P2 = .25S1 + .50S2 + .30S3.

B. P2 = $775,000 + .25P2 + .20P3 + .15S2 + .10S3.

C. P2 = $775,000 + .30S1 + .50S2 + .20S3.

D. P2 = $775,000 + .25S1 + .50S2 + .30S3.

Answer:

Which of the following elements is not part of a management control system?

A. delegated decision authority

B. performance evaluation system

C. knowledge of local conditions

D. compensation and reward system

Answer:

Becker Company applies overhead at a rate of $26 per direct labor hour. Budgeted

labor hours were 25,000; actual labor hours exceeded the budget by 1,600 hours.

Overhead was overapplied by $3,758.

Required:

(a) Compute the budgeted overhead for the year.

(b) Compute actual overhead for the year.

Answer:

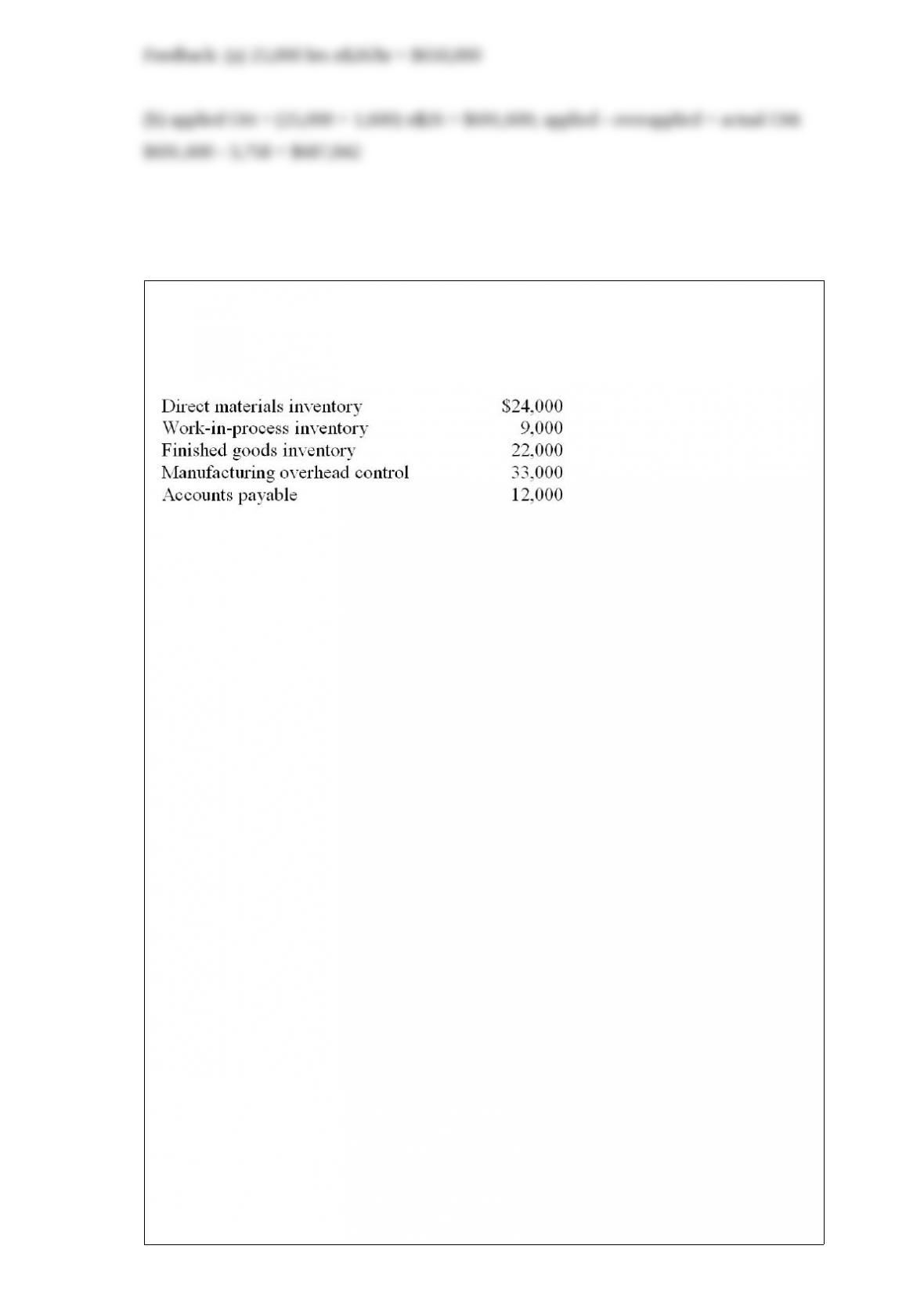

The Cedar Company does not maintain backup documents for its computer files. In

June, some of the current data were lost, and you have been asked to help reconstruct

the data. The following beginning balances are known:

Reviewing old documents and interviewing selected employees have generated the

following additional information:

The production superintendent’s job cost sheets indicated that materials of $5,200 were

included in the June 30 Work-in-Process Inventory. Also, 300 direct labor hours had

been paid at $12.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk

remembers clearly that the balance in the Accounts Payable on June 30 was $16,000.

An analysis of canceled checks indicated payments of $80,000 were made to suppliers

during June.

Payroll records indicate that 5,200 direct labor hours were recorded for June. It was

verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $32,000 on

June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled

$168,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor hours

for the year and an estimated $360,000 in manufacturing overhead costs.

Required:

(a) Compute the Cost of Goods Manufactured.

(b) Compute the ending Work-in-process inventory balance.

(c) Compute the ending Direct Materials Inventory balance.

Answer:

The WISCO Company uses a weighted-average process costing system. The following

data are available:

Total cost of the 4,000 units of the ending inventory

A. $15,840.

B. $14,520.

C. $9,240.

D. $8,910.

Answer:

In the balanced scorecard, the learning and growth perspective addresses which of the

following questions?

A. “To achieve our mission, how will we sustain our ability to change and improve?”

B. “To succeed financially, how should we appear to our shareholders?”

C. “To satisfy our shareholders and customers, in what business process must we

excel?”

D. “To achieve our mission, how should we appear to our customers?”

Answer:

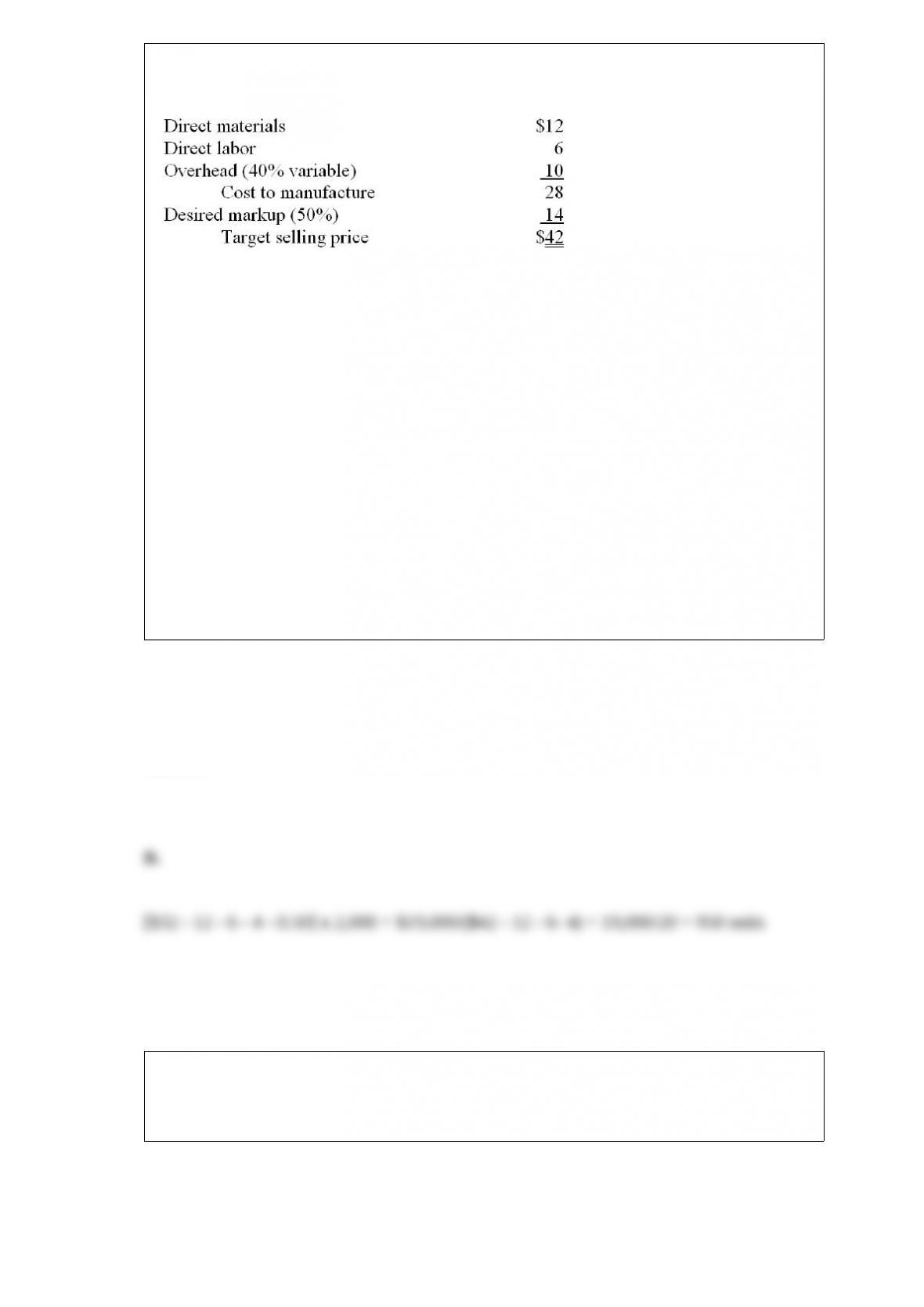

The Buchanan Company has gathered the following information for a unit of its most

popular product:

The above cost information is based on 10,000 units. A distributor has offered to buy

2,000 units at a price of $32 per unit. The distributor claims this special order would not

disturb regular sales at $42. Special packaging and other selling expenses would be an

additional $0.50 per unit for the special order. How many units of regular sales could be

lost before this contract is not profitable?

A. 0 units.

B. 950 units.

C. 1, 000 units.

D. 2,000 units.

E. 10,000 units.

Answer:

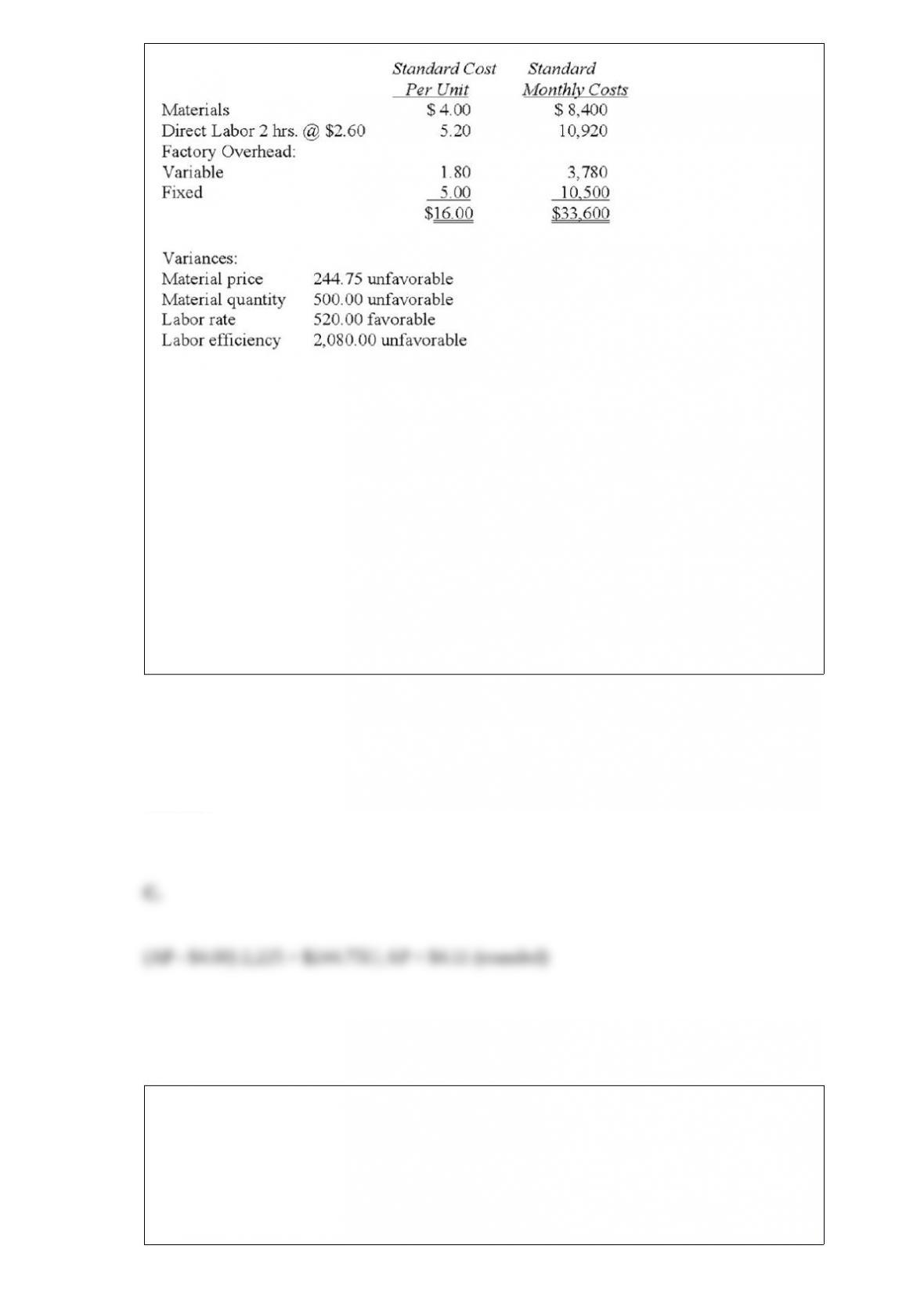

The following information summarizes the standard cost for producing one metal

tennis racket frame. In addition, the variances for one month’s production are given.

Assume that all inventory accounts have zero balances at the beginning of the month.

What was the actual price paid for the direct material during the month, assuming all

materials purchased were put into production?

A. $4.34.

B. $4.22.

C. $4.11.

D. $4.00.

E. $3.90.

Answer:

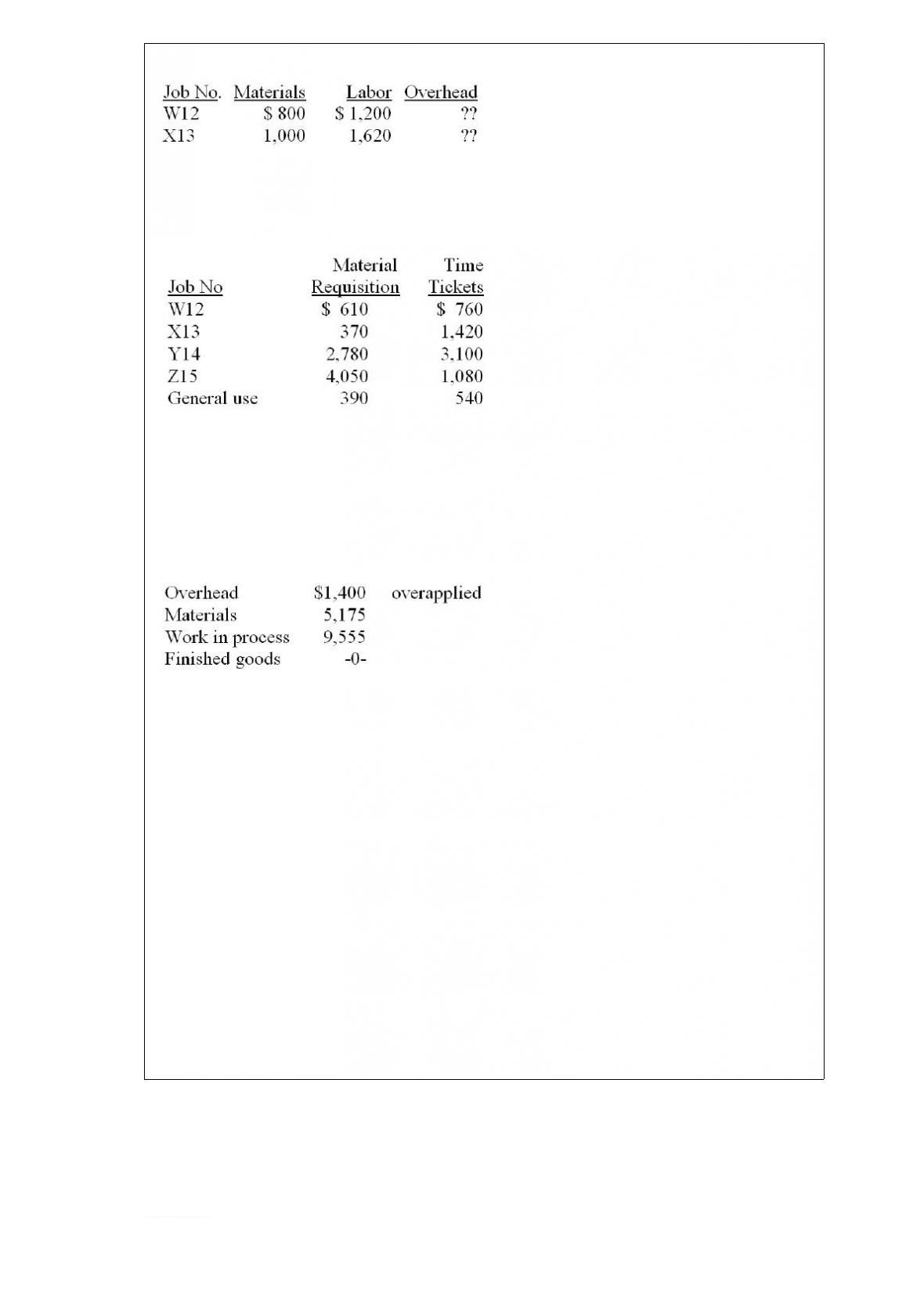

The following selected data were taken from the records of the Bixby Box Company.

The company uses a job costing system to account for its manufacturing costs. Bixby’s

fiscal year runs from January 1 to December 31; manufacturing overhead is closed out

only at the end of the fiscal year. The following information relates to August

operations.

(1) Jobs in process on August 1.

(2) Jobs completed during August: W12, X13, Y14.

(3) Material requisitions and labor time tickets indicated the following:

(4) Jobs sold during August: W12, X13.

(5) Bixby applies overhead to production based upon labor costs.

(6) Selected account balances on August 1 were:

(7) Various overhead incurred (excluding indirect materials and indirect labor) during

August, $13,500.

(8) Materials (direct and indirect) purchased during August, $10,905.

Required:

(a) What is the balance in the Material Inventory account on August 31?

(b) Is the manufacturing overhead account over-or underapplied on August 31? By how

much?

(c) Compute the cost of goods manufactured for August.

(d) Compute the cost of goods sold for August.

(e) What is the balance of the Work-in-Process Inventory account on August 31?

Answer:

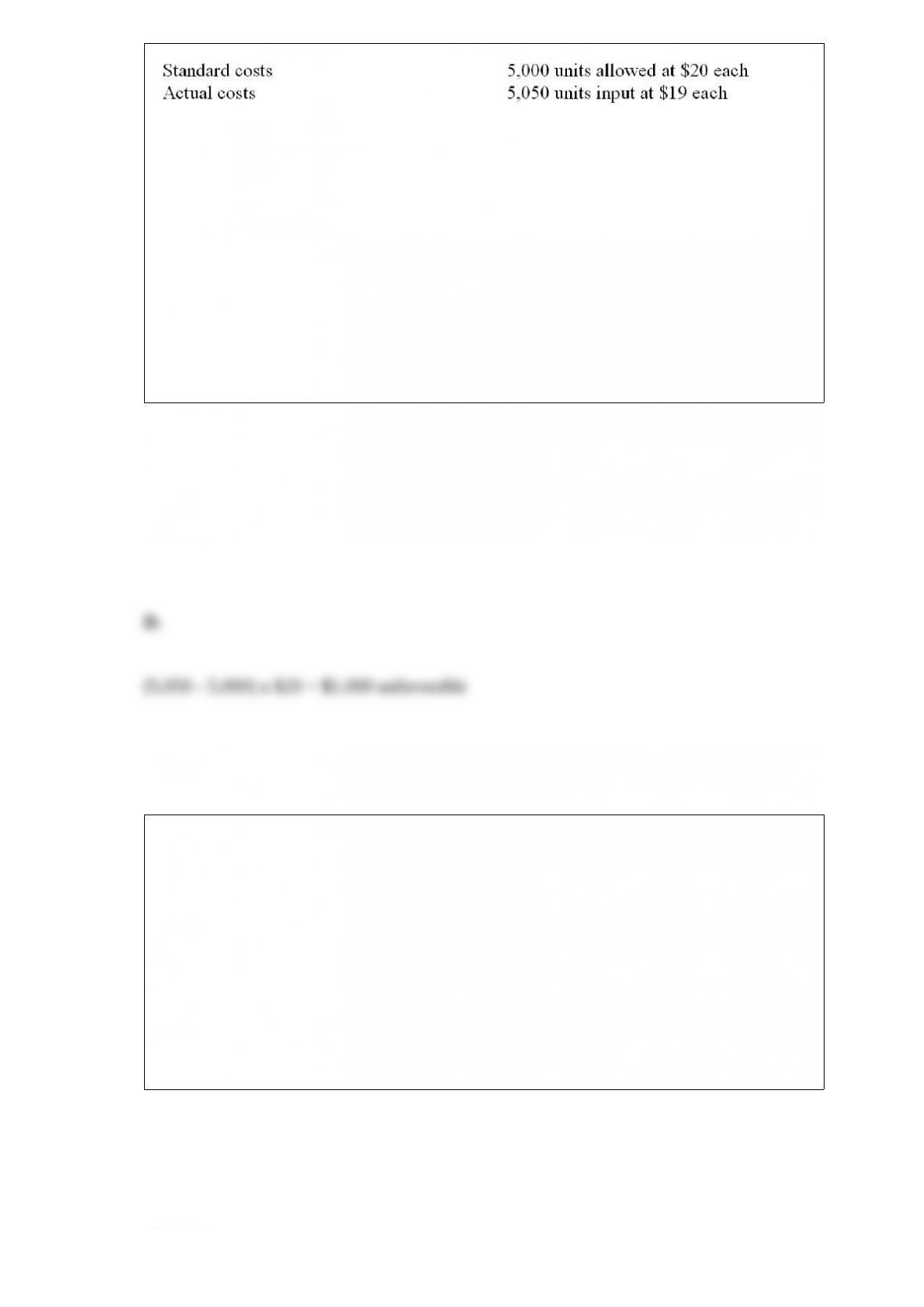

The following data pertains to the direct materials cost for the month of October:

What is the direct materials efficiency (quantity) variance?

A. $950 favorable

B. $950 unfavorable

C. $1,000 favorable

D. $1,000 unfavorable

E. $50 unfavorable

Answer:

In general, the first budget prepared is the

A. production budget.

B. direct labor budget.

C. sales budget.

D. overhead budget.

E. capital expenditures budget.

Answer:

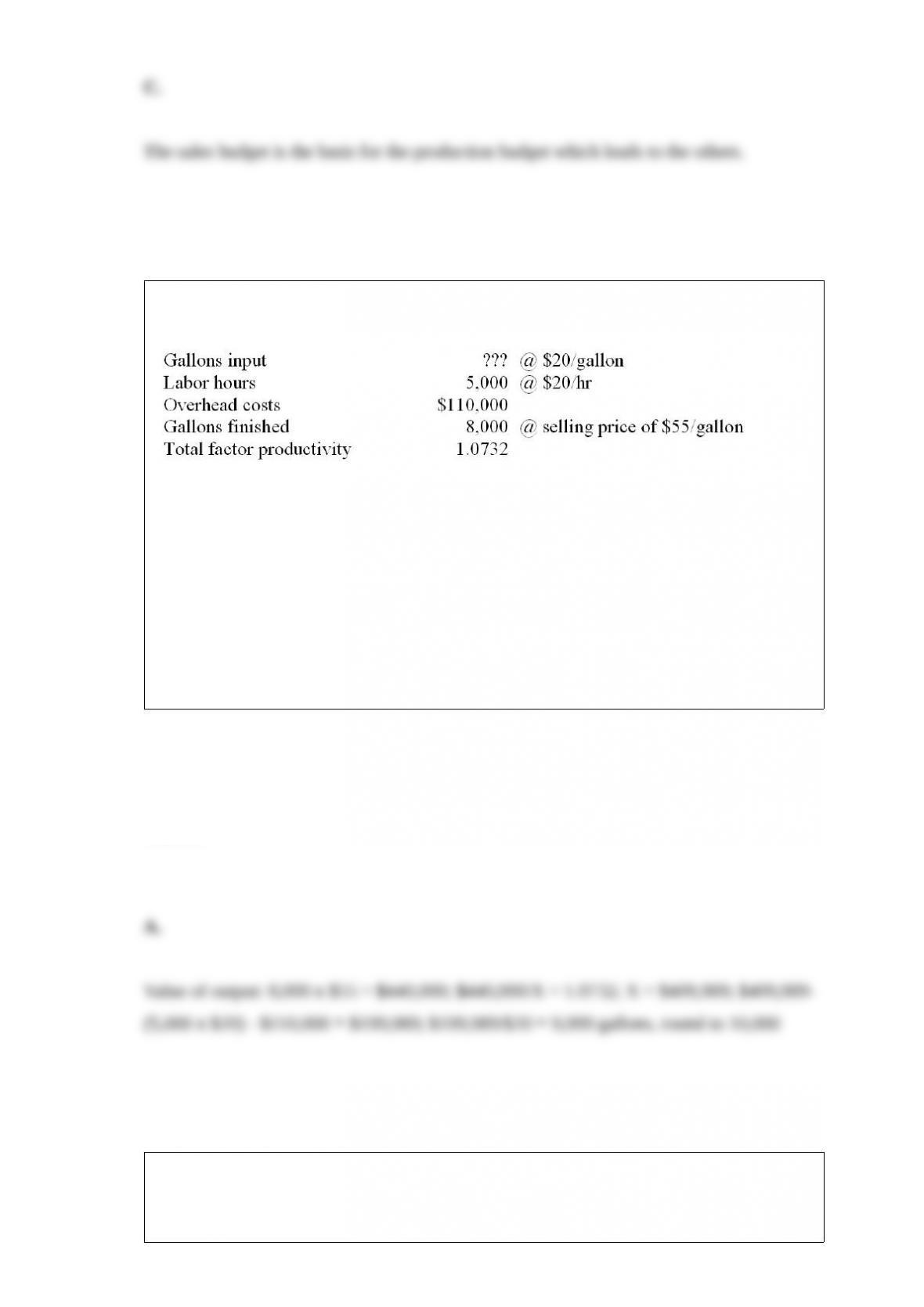

Cezanne Co. has provided the following information for last year:

The total number of gallons input (rounded) is:

A. 10,000 gallons

B. 8,600 gallons

C. 7,450 gallons

D. 200,000 gallons

Answer:

The Speedy Delivery Service is considering the expansion of its business into

afternoon retail delivery service. This would require an additional $25,000 in labor

costs per month. Company-owned vehicles now used to make morning deliveries to

local manufacturers could be used in the afternoons to make retail deliveries. However,

it is estimated that an additional $10,000 would be required per month for gas, oil, and

maintenance. It is further estimated that the retail delivery use of the trucks would be

allocated 45% of the existing $13,000 fixed vehicle costs. What is the differential

delivery cost per month for expanding into the retail delivery market?

A. $25,000

B. $35,000

C. $39,500

D. $40,850

Answer:

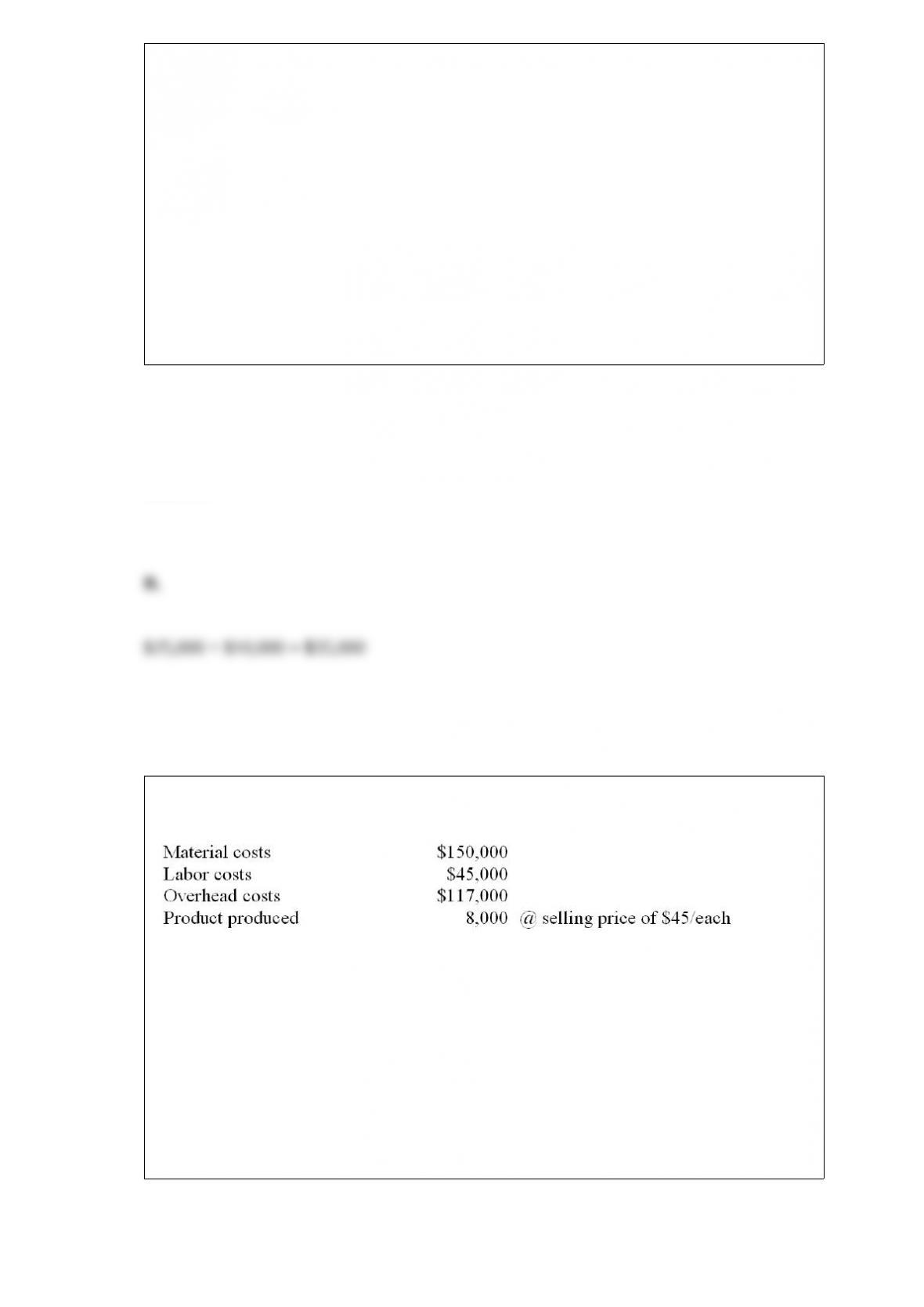

Paro Products Co. has provided the following information for last year:

The total factor productivity measure is:

A. $150,000

B. $312,000

C. 1.154

D. 0.832

Answer:

Which of the following items would be classified as a batch-level cost in an

activity-based cost management (ABM) system?

A. Indirect labor

B. Production supervisor’s salary

C. Depreciation on factory building

D. Machinery set-up costs

Answer: