Of the following, which typically would not be classified as a current liability?

a. Estimated liability from cash rebate program.

b. A long-term note payable maturing within the coming year.

c. Rent revenue received in advance.

d. A six-month bank loan to be paid with the proceeds from the sale of common stock.

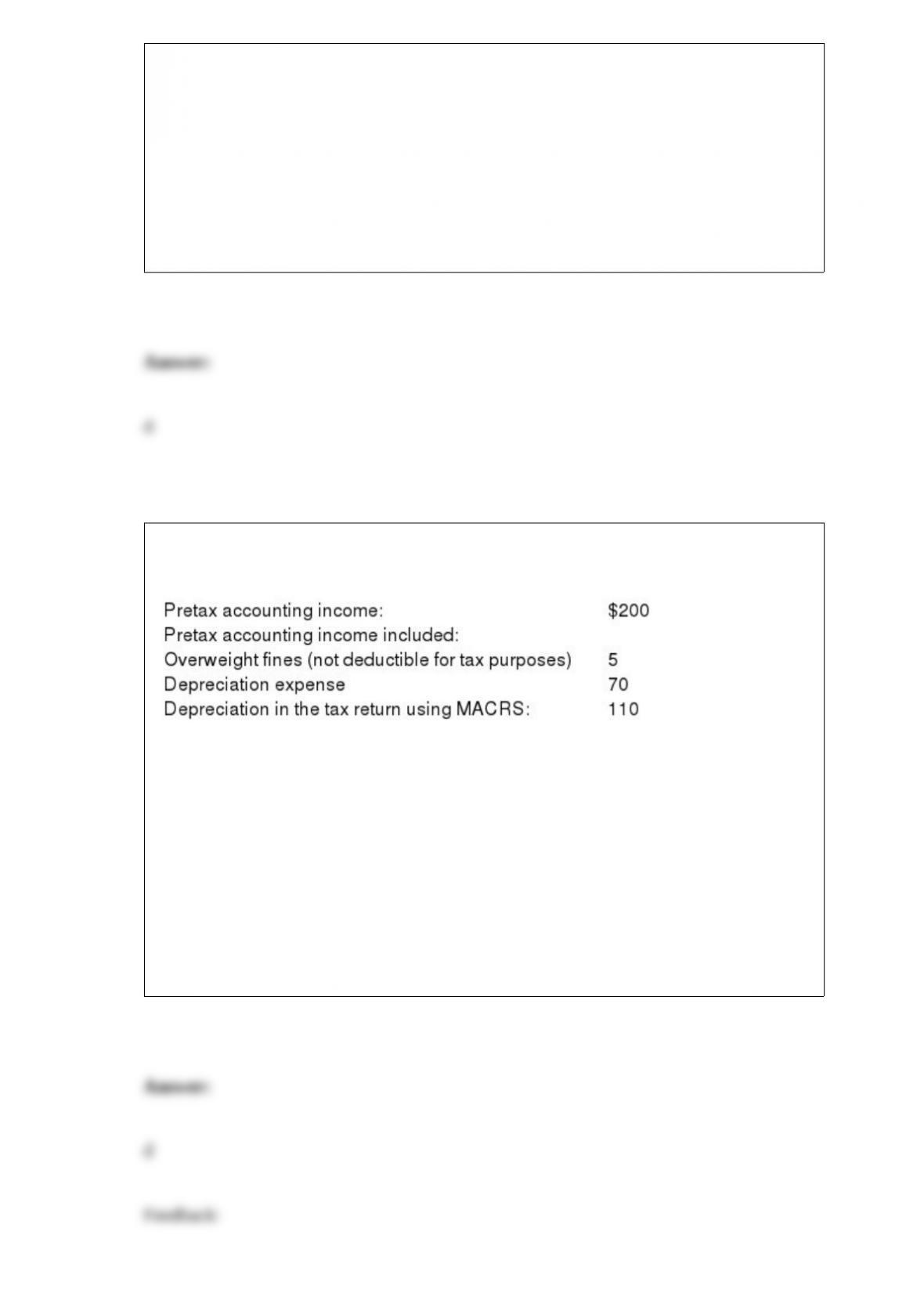

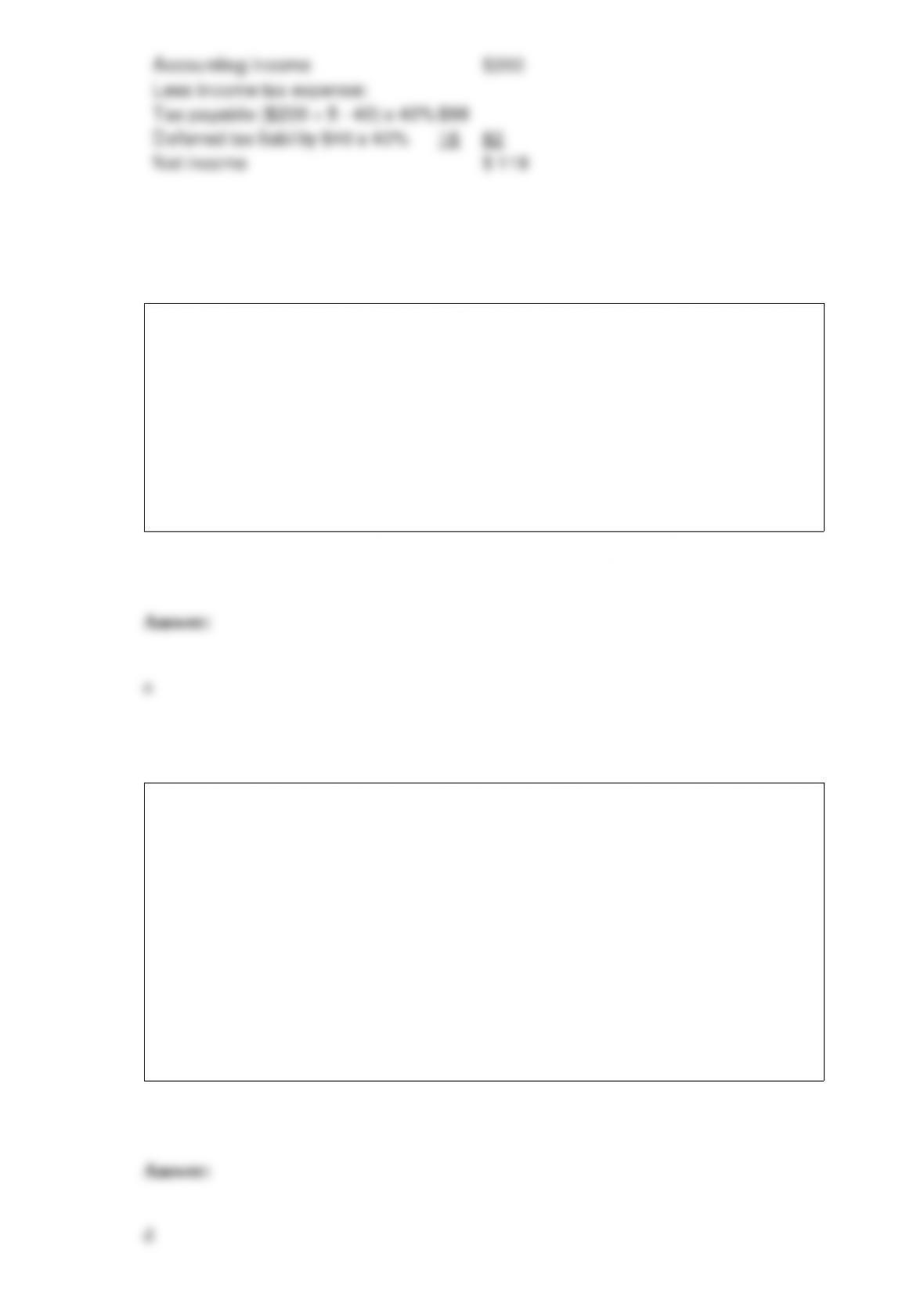

The following information relates to Franklin Freightways for its first year of

operations (data in millions of dollars):

The applicable tax rate is 40%. There are no other temporary or permanent differences.

Franklin’s net income ($ in millions) is:

a. $134.

b. $124.

c. $119.4.

d. $118.

The purchase of treasury stock is:

a. Reported as a financing activity in the statement of cash flows.

b. Reported as an investing activity in the statement of cash flows.

c. Reported as an operating activity in the statement of cash flows.

d. None of these answer choices is correct.

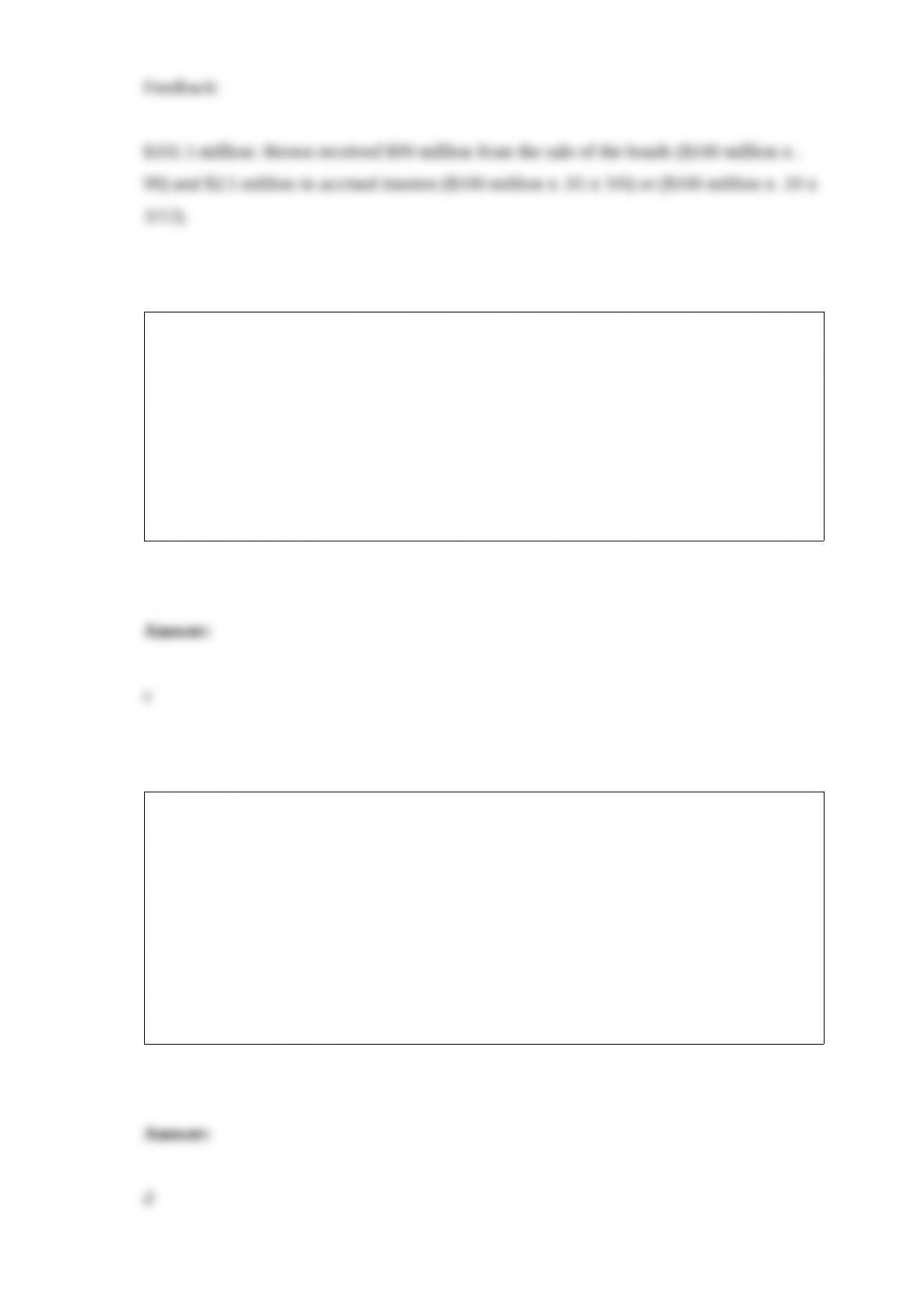

Brown Co. issued $100 million of its 10% bonds on April 1, 2016, at 99 plus accrued

interest. The bonds are dated January 1, 2016, and mature on December 31, 2035.

Interest is payable semiannually on June 30 and December 31. What amount did Brown

receive from the bond issuance?

a. $ 87.8 million

b. $ 99.0 million

c. $100.0 million

d. $101.5 million

Gains are:

a. Inflows from selling a product or service to a customer.

b. Increases in equity resulting from transfers of assets to the company from owners.

c. Increases in equity from peripheral transactions of an entity.

d. None of the above is correct.

A loss contingency should be accrued in a company’s financial statements only if the

likelihood that a liability has been incurred is:

a. At least remotely possible and the amount of the loss is known.

b. Reasonably possible and the amount of the loss is known.

c. Reasonably possible and the amount of the loss can be reasonably estimated.

d. Probable and the amount of the loss can be reasonably estimated.

When bonds include detachable warrants, what is the appropriate accounting for the

cash proceeds from the bond issue?

a. The proceeds from the bond issue are allocated between the bonds and the warrants

on the basis of their relative market values.

b. The proceeds from the bond issue are allocated between the bonds and the warrants

on the basis of their relative face values.

c. A nominal amount is allocated to the warrants.

d. All of the proceeds are allocated to the bonds.

When an accounting change is reported under the retrospective approach, account

balances in the general ledger:

a. Are not adjusted.

b. Are closed out and then updated.

c. Are adjusted net of the tax effect.

d. Are adjusted to what they would have been had the new method been used in

previous years.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment sales

method for revenue recognition. In 2015, Lake began operations and sold jet skis with a

total price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2015,

$300,000 in 2016, and $300,000 in 2017 associated with those sales. In 2016, Lake sold

jet skis with a total price of $1,500,000 that cost Lake $900,000. Lake collected

$500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated with those sales.

In 2018, Lake also repossessed $200,000 of jet skis that were sold in 2016. Those jet

skis had a fair value of $75,000 at the time they were repossessed.

Total cash collections on installment sales during 2016 would be:

a. $700,000.

b. $300,000.

c. $800,000.

d. $0

Which of the following is reported as an investing activity in the statement of cash

flows?

a. Sale of a subsidiary.

b. Issuance of a long-term promissory note.

c. Sale of treasury stock.

d. Purchase of highly liquid, short-term investments with excess cash.

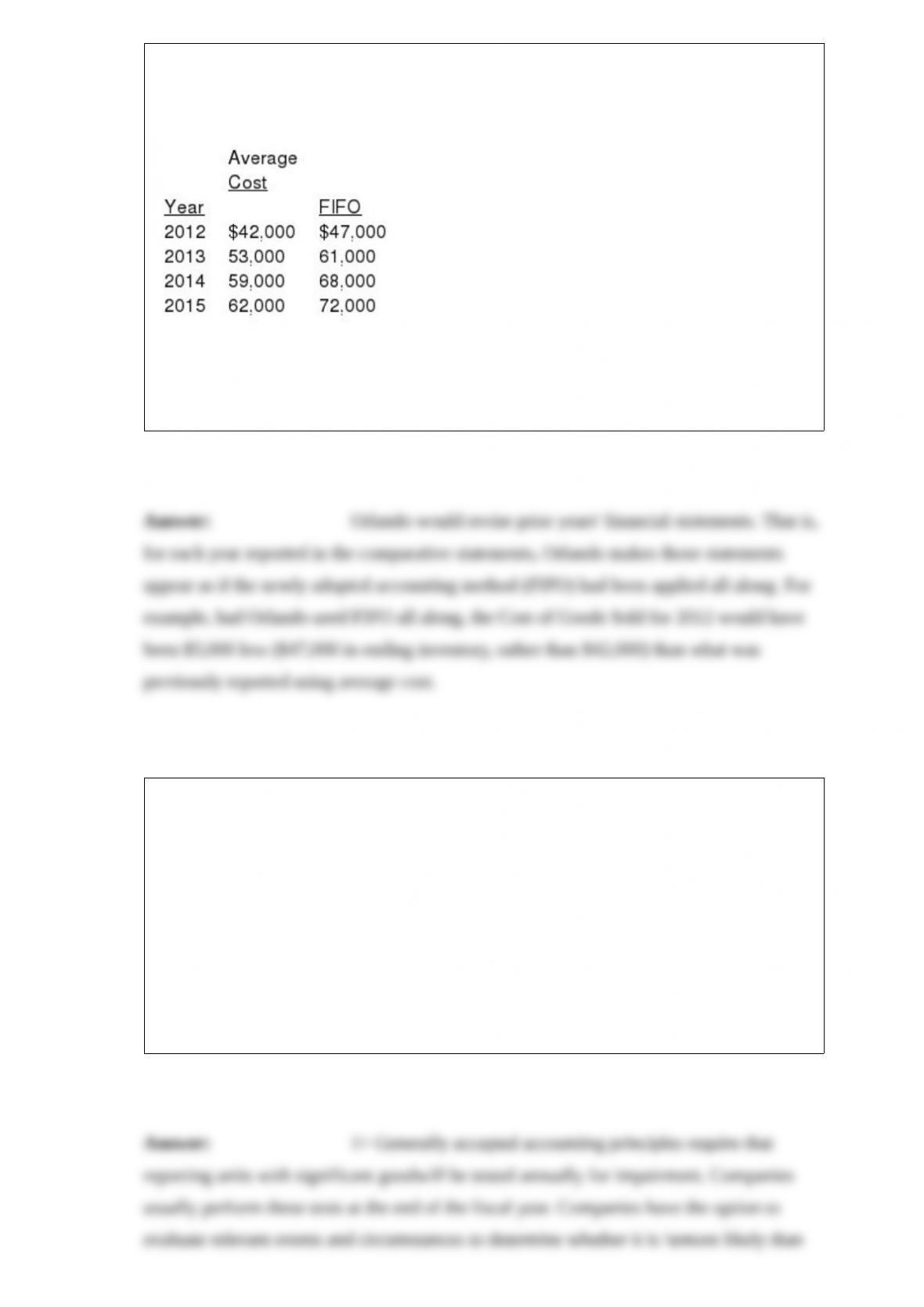

Orlando Company has used the average cost method for inventory valuation since it

began business in 2012, but has elected to change to the FIFO method starting in 2015.

Year-end inventory valuations under each method are shown below:

Required:

How would Orlando reflect the change in accounting principle in its financial

statements (ignore income taxes)?

Qualcomm Inc. engages in the development, design, manufacture, and marketing of

digital wireless telecommunications products and services. In a recent income statement

the company reported a $114 million goodwill impairment loss. The loss related to the

goodwill of its Firethorn reporting unit. Required:

1> Why did Qualcomm conduct an impairment test of the goodwill of this reporting

unit?

2> Describe the steps Qualcomm performed to conduct its impairment test.

3> Where would the impairment loss be shown in the company’s income statement?

3 Hardin Widget Manufacturing began operations in January 2016. 3 Hardin sells

widgets that carry a two-year manufacturer’s warranty against defects in workmanship.

3 Hardin’s management projects that 2% of the widgets will require repair during the

first year of the warranty while approximately 6% will require repair during the second

year of the warranty. The widgets sell for $400 each. The average cost to repair a

widget is $50. The company sells 60% of the widgets to retail customers who must pay

a 6% sales tax. Sales and warranty information for 2016 and 2017 are as follows:

2016: Sold 200 widgets on account; incurred warranty expenditures of $300.

2017: Sold 300 widgets on account; actual warranty expenditures were $500.

Required:

1> Prepare journal entries that summarize the sales and any aspects of the warranty for

2016.

2> Prepare journal entries that summarize the sales and any aspects of the warranty for

2017.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the correct term.

Briefly explain the financial reporting required when a company changes to or from the

LIFO inventory method.

What are the situations deemed to constitute a change in reporting entity? Describe the

way changes in reporting entity are reported.