Which of the following does not apply to a seller who is a principal?

a. Has control over goods or services

b. Primarily responsible for providing goods or services to customer

c. Exposed to risks associated with holding inventory

d. Primary performance obligation is to facilitate the transfer of goods or services

An argument against use of the lower of cost and net realizable value rule is its lack of:

a. Relevance.

b. Reliability.

c. Consistency.

d. Objectivity.

The shareholders’ ‘equity of Green Corporation includes $200,000 of $1 par common

stock and $400,000 par value of 6% cumulative preferred stock. The board of directors

of Green declared cash dividends of $50,000 in 2016 after paying $20,000 cash

dividends in each of 2015 and 2014. What is the amount of dividends common

shareholders will receive in 2016?

a. $18,000.

b. $26,000.

c. $28,000.

d. $32,000.

Which of the following is not among the criteria for classifying a lease as a capital

lease?

a. The agreement specifies that ownership of the asset transfers to the lessee.

b. The agreement contains a bargain purchase option.

c. The noncancelable lease term is equal to 90% or more of the expected economic life

of the asset.

d. The present value of the minimum lease payments is equal to or greater than 90% of

the fair value of the asset.

The appropriate asset value reported in the balance sheet by the lessee for an operating

lease is:

a. Present value of the minimum lease payments.

b. Sum of the minimum lease payments.

c. Fair value of the asset at the inception of the lease.

d. Zero, unless a prepayment or accrual is involved.

The amortization of a net gain has what effect on pension expense?

a. Decreases it.

b. Has no effect on it.

c. Increases it (but only by the amount over 10% of the PBO).

d. Increases it (regardless of the amount).

What is Rudyard’s diluted EPS (rounded)?

Rudyard Corporation had 100,000 shares of common stock and 10,000 shares of 8%,

$100 par convertible preferred stock outstanding during the year. Net income for the

year was $400,000 and dividends were paid to both common and preferred

shareholders. Rudyard’s effective tax rate is 40%. Each share of preferred stock is

convertible into five shares of common.

a. $2.13.

b. $2.67.

c. $3.20.

d. $4.80.

The balance sheets of Davidson Corporation reported net fixed assets of $320,000 at the

end of 2016. The fixed-asset turnover ratio for 2016 was 4.0, and sales for the year

totaled $1,480,000. Net fixed assets at the end of 2015 were:

a. $470,000.

b. $370,000.

c. $420,000.

d. None of these answer choices are correct.

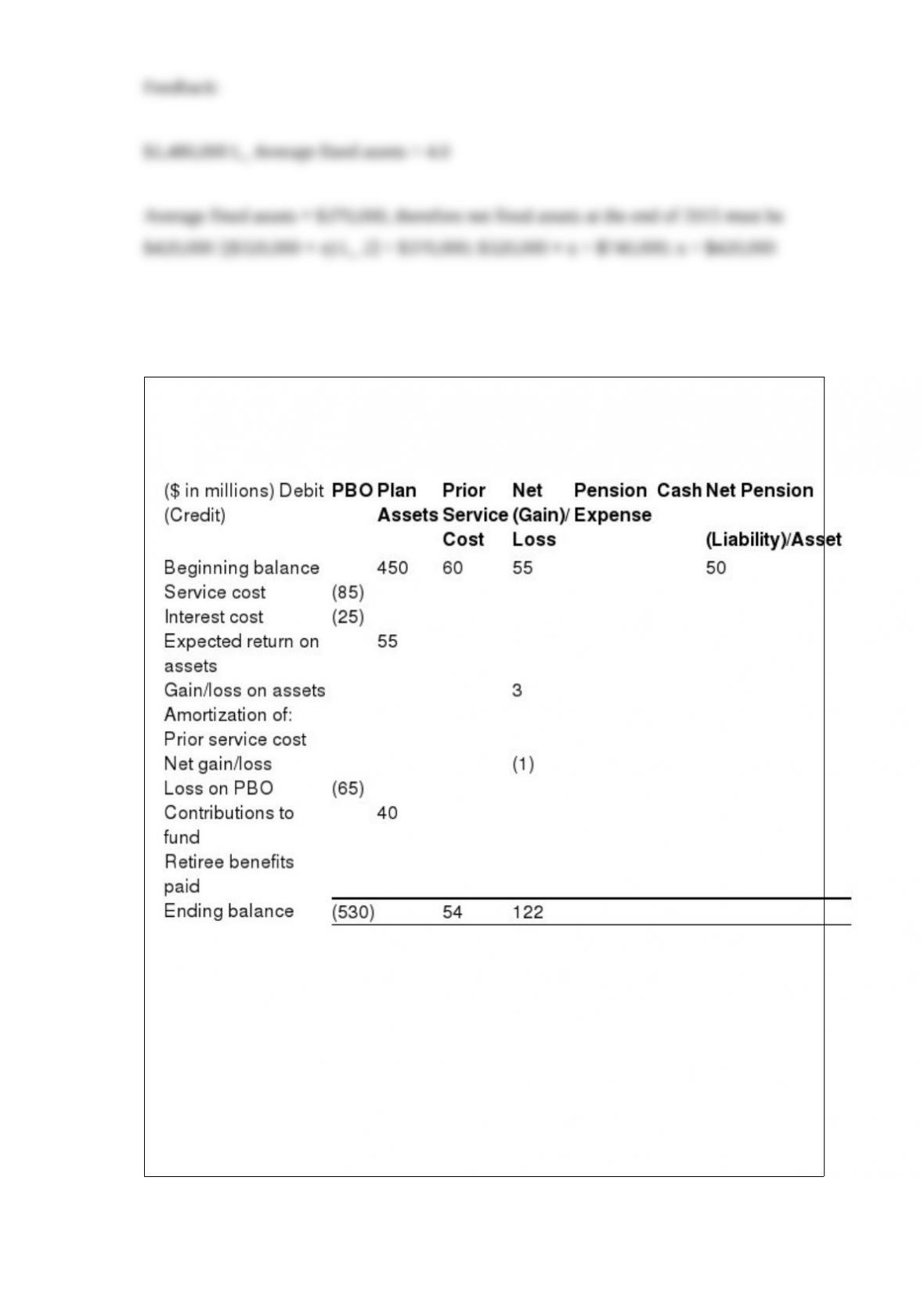

The following refers to the pension spreadsheet (columns have missing amounts) for

the current year for Pancho Villa Enterprises (PVE).

What was the PBO at the beginning of the year?

a. $160.

b. $400.

c. $500.

d. $610.

The largest expense on a retailer’s income statement is typically:

a. Salaries and wages.

b. Cost of goods sold.

c. Income tax expense.

d. Depreciation expense.

Current liabilities are normally recorded at the amount expected to be paid rather than

at their present value. This practice can be supported by GAAP according to the concept

of:

a. Matching.

b. Consistency.

c. Materiality.

d. Conservatism.

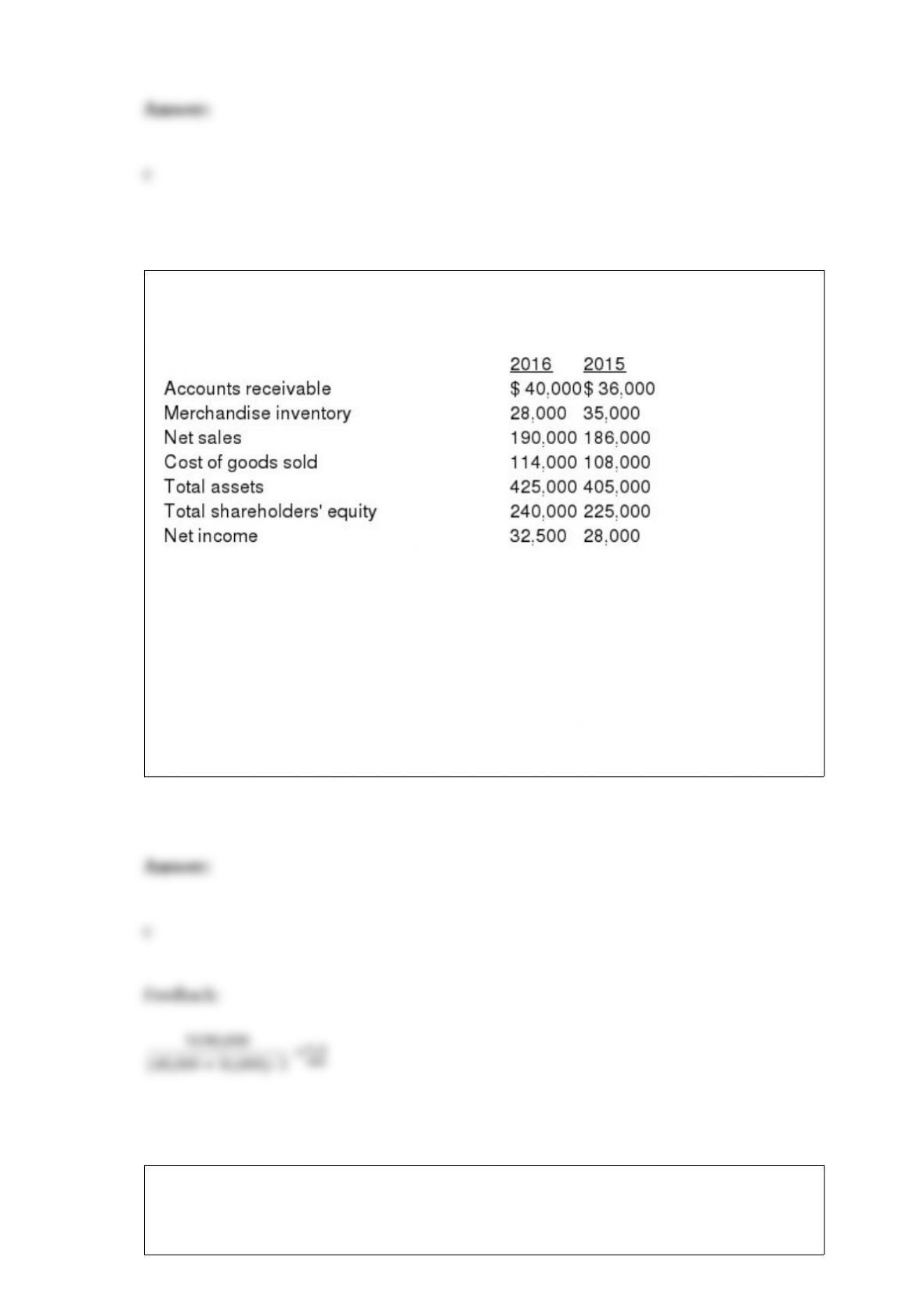

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Hulkster’s 2016 receivables turnover is:

a. 2.85.

b. 4.70.

c. 5.00.

d. 10.63.

Jane’s Donut Co. borrowed $200,000 on January 1, 2016, and signed a two-year note

bearing interest at 12%. Interest is payable in full at maturity on January 1, 2018. In

connection with this note, Jane’s should report interest expense at December 31, 2016,

in the amount of:

a. $0.

b. $24,000.

c. $48,000.

d. $50,880.

Which of the following groups is not among financial intermediaries?

a. Mutual fund managers.

b. Financial analysts.

c. CPAs.

d. Credit rating organizations.

What is the expense that Holyoakshould report for its promotional rebates in its 2016

income statement?

a. $142,000.

b. $152,000.

c. $170,000.

d. $200,000.

According to International Financial Reporting Standards (IFRS), the revaluation of

equipment when fair value exceeds book value, results in:

a. An increase in net income.

b. A decrease in net income.

c. An increase in other comprehensive income.

d. A decrease in other comprehensive income.

Recognition of impairment for property, plant, and equipment is required if book value

exceeds:

a. Fair value.

b. Present value of expected cash flows.

c. Undiscounted expected cash flows.

d. Accumulated depreciation.

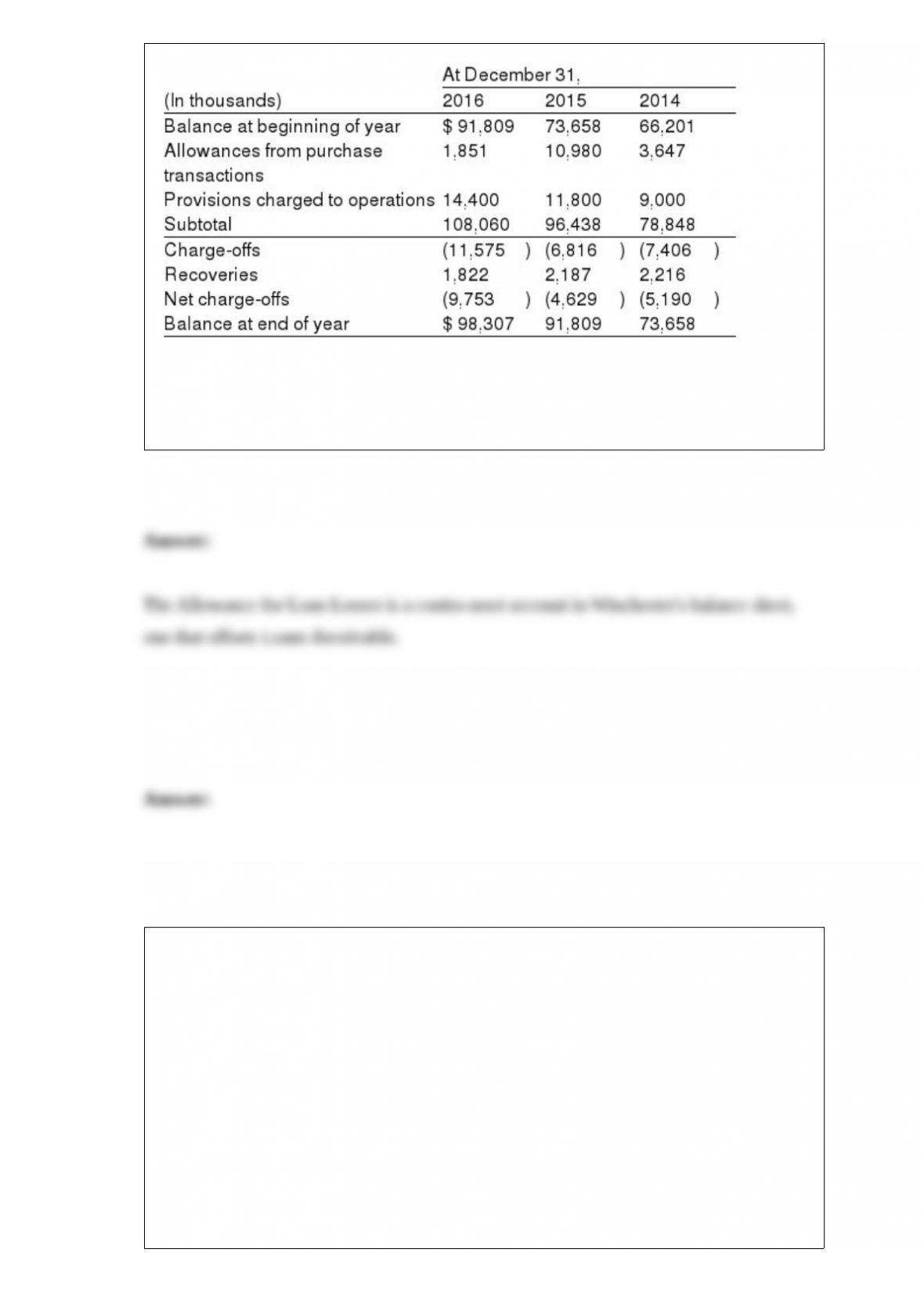

Topic Area:

The following note disclosure is taken from the 2016 annual report to shareholders of

Winchester International Corporation. NOTE 5: ALLOWANCE FOR LOAN LOSSES

The allowance for loan loss is maintained at a level to absorb probable losses inherent

in the loan portfolio. This allowance is increased by provisions charged to operating

expense and by recoveries on loans previously charged off, and reduced by charge-offs

on loans. The following is a summary of the changes in the allowances for loan losses

for three years:

Winchester also reported (in thousands) in its comparative balance sheet that it held

Loans receivable, net, of $6,869,911 and $6,819,209 at December 31, 2016, and

December 31, 2015, respectively. What kind of account is the Allowance for Loan

Losses in Winchester’s financial statements?

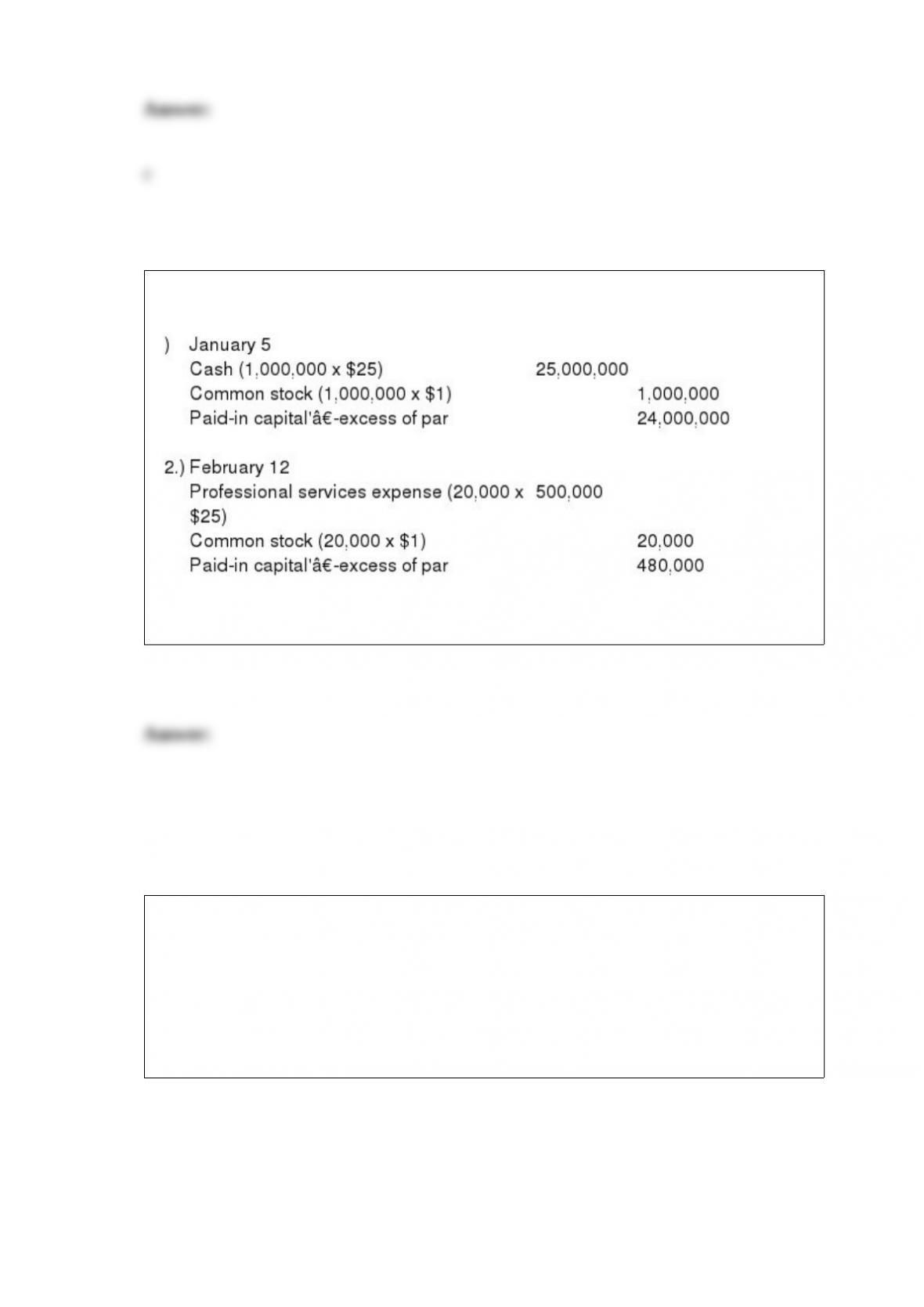

During its first year of operations, Cole’s Electronics Inc. completed the following

transactions relating to shareholders’ equity.

January 5: Issued 1,000,000 shares of common stock for $25 per share.

February 12: Issued 20,000 shares of common stock to accountants for $500,000 of

professional services.

The articles of incorporation authorize 5,000,000 shares of common stock with a par

value of $1 per share and 1,000,000 preferred shares with a par value of $100 per share.

Required:

Record the above transactions in general journal form.

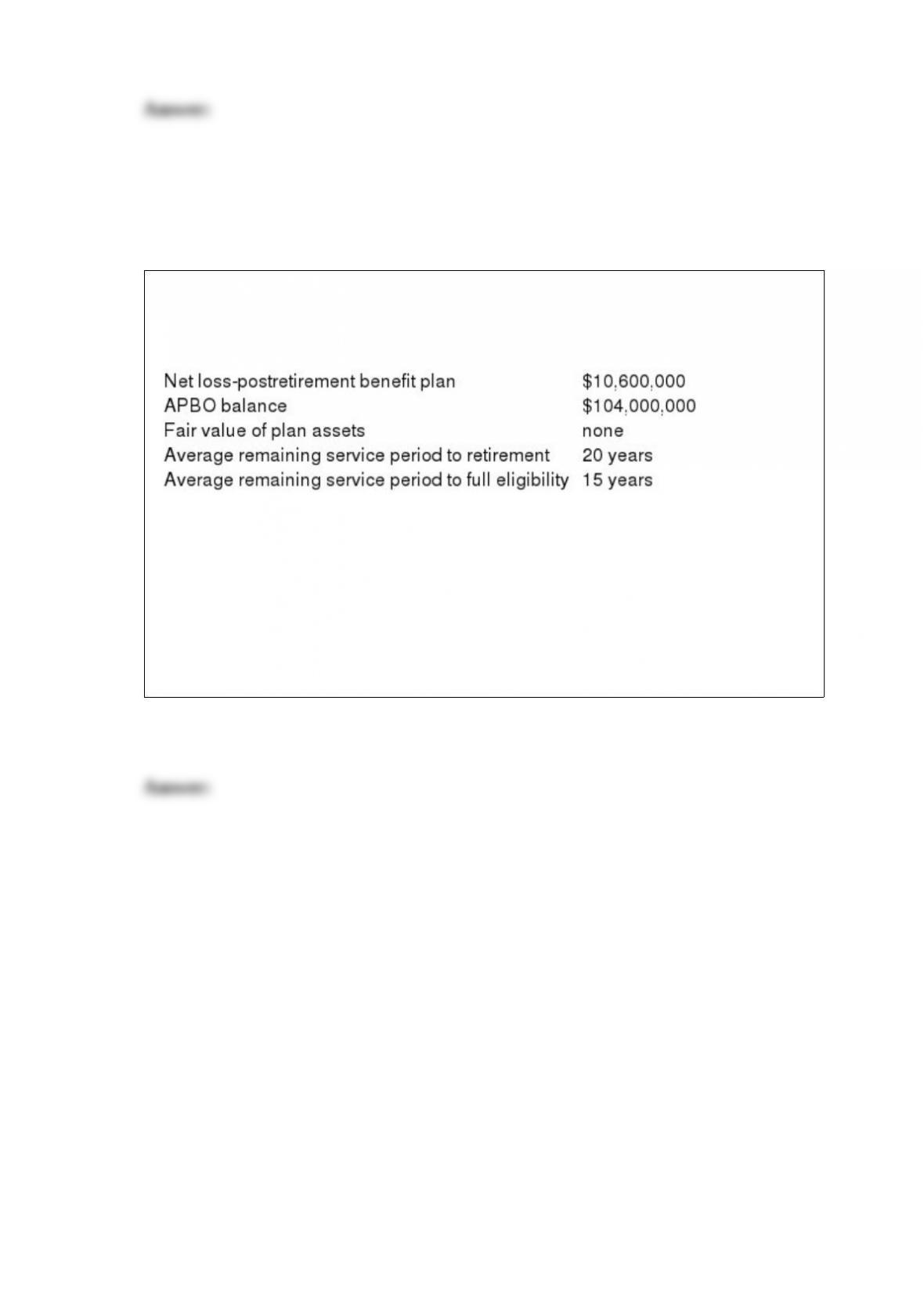

Oberon Company provides postretirement health care benefits to employees who

provide at least 10 years of service and reach the age of 65 while in service. On January

1 of the current year, the following plan-related data were available.

On January 1 of the current year, Oberon amended the plan to provide dental benefits.

The actuary determines that the cost of making the amendment increases the APBO by

$10,000,000. Management chooses to amortize this amount on a straight-line basis. The

service cost is $60,000,000. The appropriate interest rate is 10%.

Required:

Calculate the postretirement benefit expense for the current year.

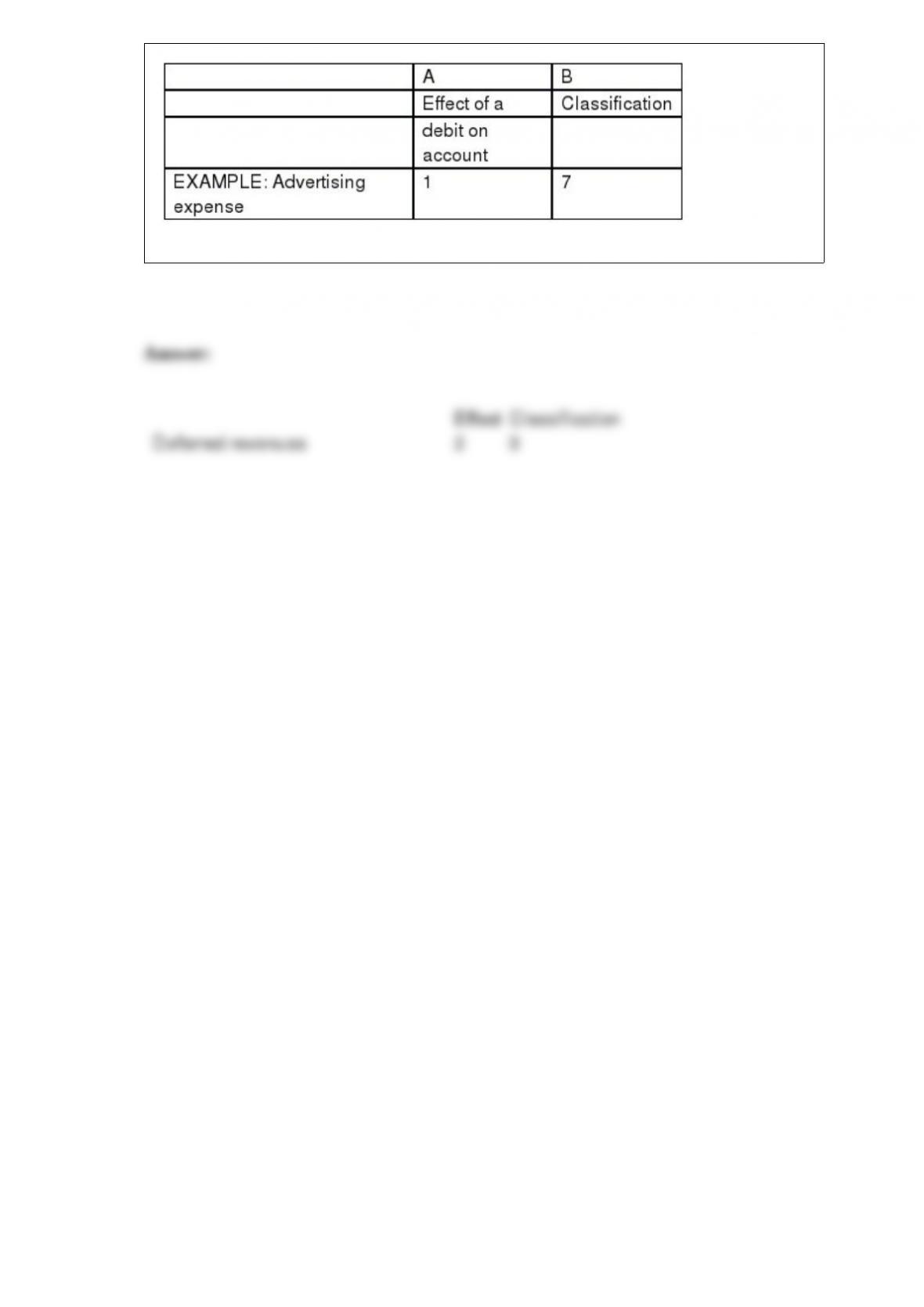

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Deferred revenues