For 2016, Rahal’s Auto Parts estimates bad debt expense at 1% of credit sales. The

company reported accounts receivable and an allowance for uncollectible accounts of

$86,500 and $2,100, respectively, at December 31, 2015. During 2016, Rahal’s credit

sales and collections were $404,000 and $408,000, respectively, and $2,340 in accounts

receivable were written off.

Rahal’s 2016 bad debt expense is:

a. $2,100.

b. $2,340.

c. $4,080.

d. None of these answer choices are correct.

During the year, Hamlet Inc. paid $20,000 to have bond certificates printed and

engraved, paid $100,000 in legal fees, paid $10,000 to a CPA for registration

information, and paid $200,000 to an underwriter as a commission. What is the amount

of bond issue costs?

a. $330,000.

b. $300,000.

c. $120,000.

d. $ 20,000.

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term.

1> Notes receivable a. Insurance premiums paid in advance.

2> Short-term investments b. Goods to be sold in the ordinary course of business.

3> Inventories 4> Accounts receivable c. Due from customers in the ordinary course

of business.

5> Prepaid expensesd. Formal agreement that specifies customer’s payment terms.

e. Liquid investments not classified as cash equivalents.

On January 1, 2011, F Corp. issued 2,000 of its 10%, $1,000 bonds for $2,080,000.

These bonds were to mature on January 1, 2021, but were callable at 101 any time after

December 31, 2014. Interest was payable semiannually on July 1 and January 1. On

July 1, 2016, F called all of the bonds and retired them. The bond premium was

amortized on a straight-line basis. Before income taxes, F Corp.’s gain or loss in 2016

on this early extinguishment of debt was:

a. $16,000 gain.

b. $20,000 loss.

c. $24,000 gain.

d. $60,000 gain.

Which of the following was the first private-sector entity that set accounting standards

in the United States?

a. Accounting Principles Board.

b. Committee on Accounting Procedure.

c. Financial Accounting Standards Board.

d. AICPA.

Which of the following is one of the steps for recognizing revenue?

a. Identify the performance obligations of the contract.

b. Determine whether bad debts can be reasonably estimated.

c. Estimate the total transaction price of the contract based on fair value.

d. Allocate all revenue to the performance obligation with the largest stand-alone selling

price.

What is the total compensation cost for this plan?

Wall Drugs offered an incentive stock option plan to its employees. On January 1, 2016,

options were granted for 60,000 $1 par common shares. The exercise price equals the

$5 market price of the common stock on the grant date. The options cannot be exercised

before January 1, 2019, and expire December 31, 2020. Each option has a fair value of

$1 based on an option pricing model.

a. $0.

b. $60,000.

c. $240,000.

d. $300,000.

Pug Corporation has 10,000 shares of $10 par common stock outstanding and 20,000

shares of $100 par, 6% noncumulative, nonparticipating preferred stock outstanding.

Dividends have not been paid for the past two years. This year, a $150,000 dividend

will be paid. What are the dividends per share for preferred and common, respectively?

a. $7.50; $0.

b. $6; $3.

c. $6; $1.50.

d. None of these answer choices is correct.

In a statement of cash flows using the indirect method, an increase in available-for-sale

securities not due to an increase in their fair value should be reported as:

a. A deduction from net income in determining cash flows from operating activities.

b. An addition to net income in determining cash flows from operating activities.

c. A net cash outflow from investing activity.

d. A net cash inflow from investing activity.

The FASB’s conceptual framework’s qualitative characteristics of accounting

information include:

a. Historical cost.

b. Realization.

c. Faithful representation.

d. Full disclosure.

The financial reporting carrying value of Boze Music’s only depreciable asset exceeded

its tax basis by $150,000 at December 31, 2016. This was a result of differences

between straight-line depreciation for financial reporting purposes and MACRS for tax

purposes. The asset was acquired earlier in the year. Boze has no other temporary

differences. The enacted tax rate is 30% for 2016 and 40% thereafter. Boze should

report the deferred tax effect of this difference in its December 31, 2016, balance sheet

as:

a. A liability of $45,000.

b. A liability of $60,000.

c. An asset of $45,000.

d. An asset of $60,000.

A company’s postretirement health care benefit plan had an APBO of $265,000 on

January 1, 2016. During 2016, retiree benefits paid were $40,000. The discount rate for

the plan for this year was 10%. Service cost for 2016 was $80,000. Plan assets (fair

value) increased during the year by $45,000. The amount of the APBO at December 31,

2016, was:

a. $225,000.

b. $305,000.

c. $331,500.

d. $371,500.

Gore Inc. recorded a liability in 2016 for probable litigation losses of $2 million.

Ultimately, $5 million in legitimate warranty claims were filed by Gore’s customers.

a. Gore has made a change in accounting principle, requiring retrospective adjustment.

b. Gore needs to correct an accounting error.

c. Gore is required to adjust a change in accounting estimate prospectively.

d. Gore is not required to make any accounting adjustments.

Which of the following financial statements is prepared as of a particular point in time

rather than for a period of time?

a. Statement of cash flows.

b. Income statement.

c. Statement of shareholders’ equity.

d. Balance sheet.

Expenses in an income statement prepared under International Financial Reporting

Standards:

a. Must be classified by function.

b. Must be classified by natural description.

c. Can be classified either by function or by natural description.

d. None of the other answers is correct.

Portelli Services provides room-cleaning arrangements for hotels in Pennsylvania. On

April 1, Silvia Hotels & Resorts signed an agreement to outsource its room-cleaning

functions to Portelli. The contract specifies the service fee to be $15,000 per month, and

all payments are to be made shortly after the end of each quarter. It also specifies that

Portelli will receive an additional quarterly bonus of $3,000 if, during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Portelli estimated that there is a 75% chance

that it will earn the quarterly bonus.

– On May 5, Portelli learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Portelli revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Portelli that, for the quarter ended, there were four

complaints associated with room cleanliness, so Portelli would receive the bonus. Two

days later, Portelli received all payments due for all services rendered in the second

quarter, including the bonus. Portelli bases estimates of variable consideration on the

most likely amount it expects to receive.

Prepare Portelli’s June 30 and July 2 journal entries to record additional service revenue

earned, as well as any necessary adjustments to revenue and receipt of payment from

Silvia.

On January 1, 2016, an investor paid $291,000 for bonds with a face amount of

$300,000. The stated rate of interest is 8% while the current market rate of interest is

10%. Using the effective interest method, how much interest income is recognized by

the investor in 2016 (assume annual interest payments and amortization)?

a. $23,280.

b. $29,100.

c. $24,000.

d. $30,000.

GAAP requires that some lease agreements be accounted for as purchases. The

theoretical justification for this treatment is that a lease of this type:

a. Complies with the concept of form over substance.

b. Reflects the relationship of cause and effect.

c. Satisfies the concept of historical cost.

d. Conveys most of the risks and benefits of property ownership.

In its 2016 annual report to shareholders, Bare Sturns Group Inc. disclosed the

following:

On October 28, 2016, the Company issued $475,000,000 aggregate principal amount of

9-1/4% Senior Notes Due 2021 (“Senior Notes”) and $618,670,000 aggregate principal

amount at maturity of 10-1/4% Senior Discount Notes Due 2021 (“Senior Discount

Notes” and collectively the “Notes”) in a transaction not registered under the Securities

Act in reliance upon an exemption from the registration requirements of the Securities

Act. Gross proceeds from the offering amounted to $850,000,000. The discount on the

Senior Discount Notes is being accreted under the effective interest method.

Explain the last sentence of the disclosure to clarify what accounting was necessary and

why.

Use the following to answer questions 119-124: You are reviewing O’Brian Co.’s

adjusted trial balance for the year ended 12/31/16. You notice several omissions and

incorrect items during your review, some of which are noted below. For each one, you

are to determine what effect, if any, these items would have on the stated components of

O’Brian Co.’s 2016 Income Statement and 12/31/16 Balance Sheet if they are not

corrected or updated. Assume no income taxes. Use the following code for your

answers. You need not include any dollar amounts.

N = No Effect

O = Overstated

U = Understated

Lugar Company purchased a piece of machinery for $30,000 on January 1, 2014, and

has been depreciating the machine using the sum-of-the-years’-digits method based on a

five-year estimated useful life and no salvage value. On January 1, 2016, Lugar decided

to switch to the straight-line method of depreciation. The salvage value is still zero and

the estimated useful life is changed to a total of six years from the date of purchase.

Ignore income taxes.

List at least four operating activities that would be reported in the statement of cash

flows for Walmart. Assume the use of the direct method.

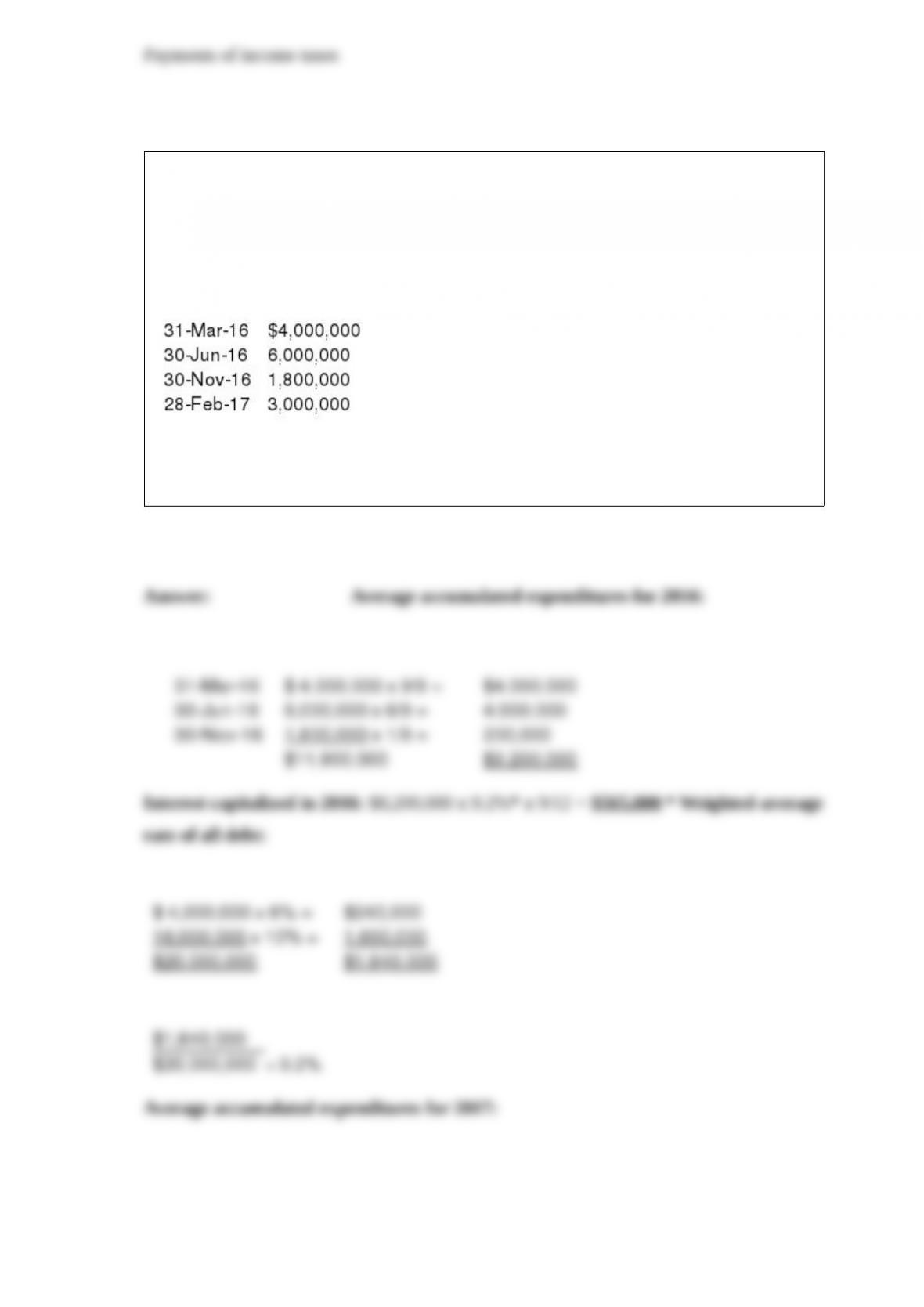

Hawkins Corporation began construction of a motel on March 31, 2016. The project

was completed on April 31, 2017. No new loans were required to fund construction.

Hawkins does have the following two interest-bearing liabilities that were outstanding

throughout the construction period: $ 4,000,000, 6% note

$16,000,000, 10% bonds Construction expenditures incurred were as follows:

The company’s fiscal year-end is December 31. Required:

Calculate the amount of interest capitalized for 2016 and 2017.

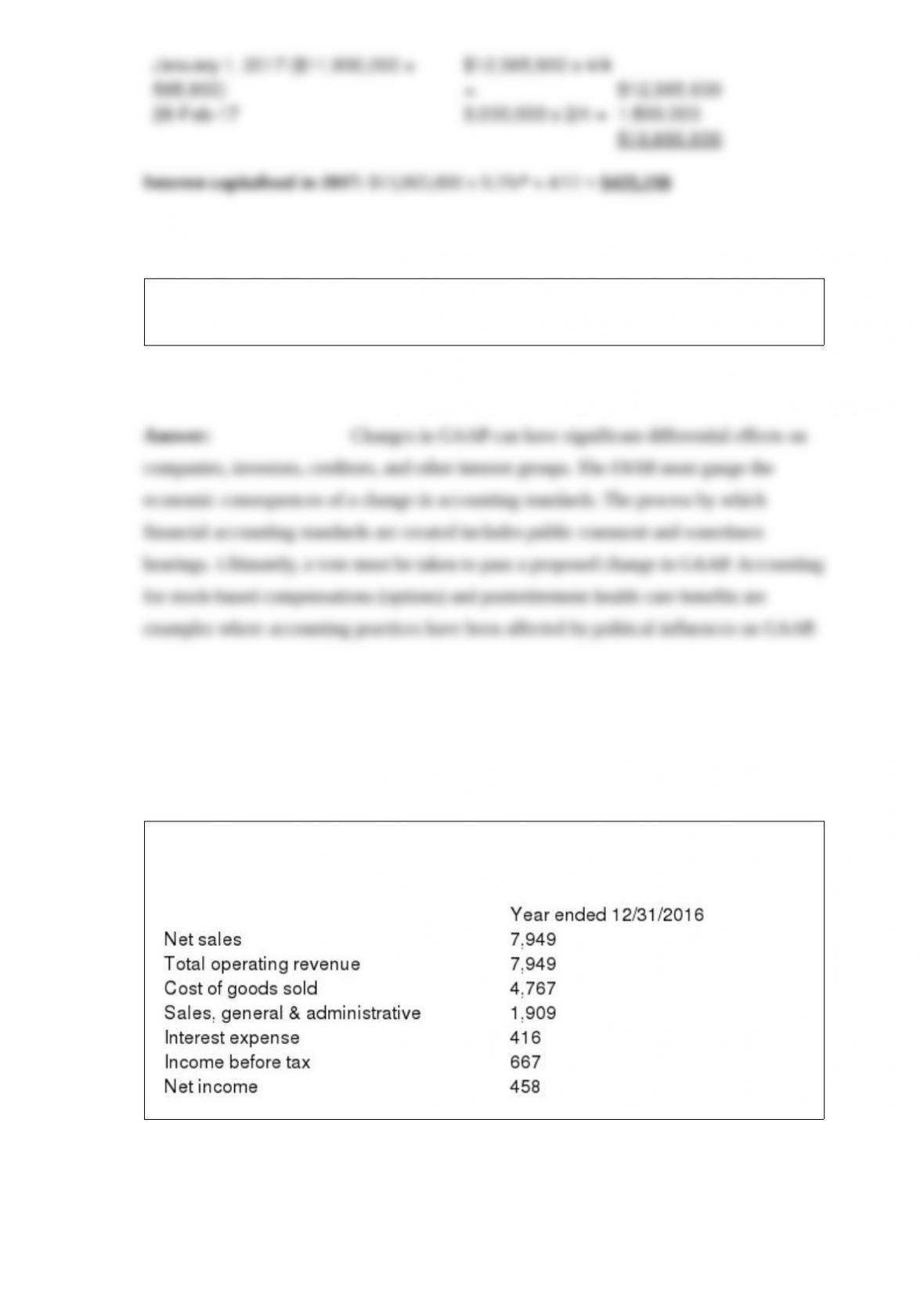

Accounting standard-setting has been characterized as a political process. Discuss this

proposition giving an example.

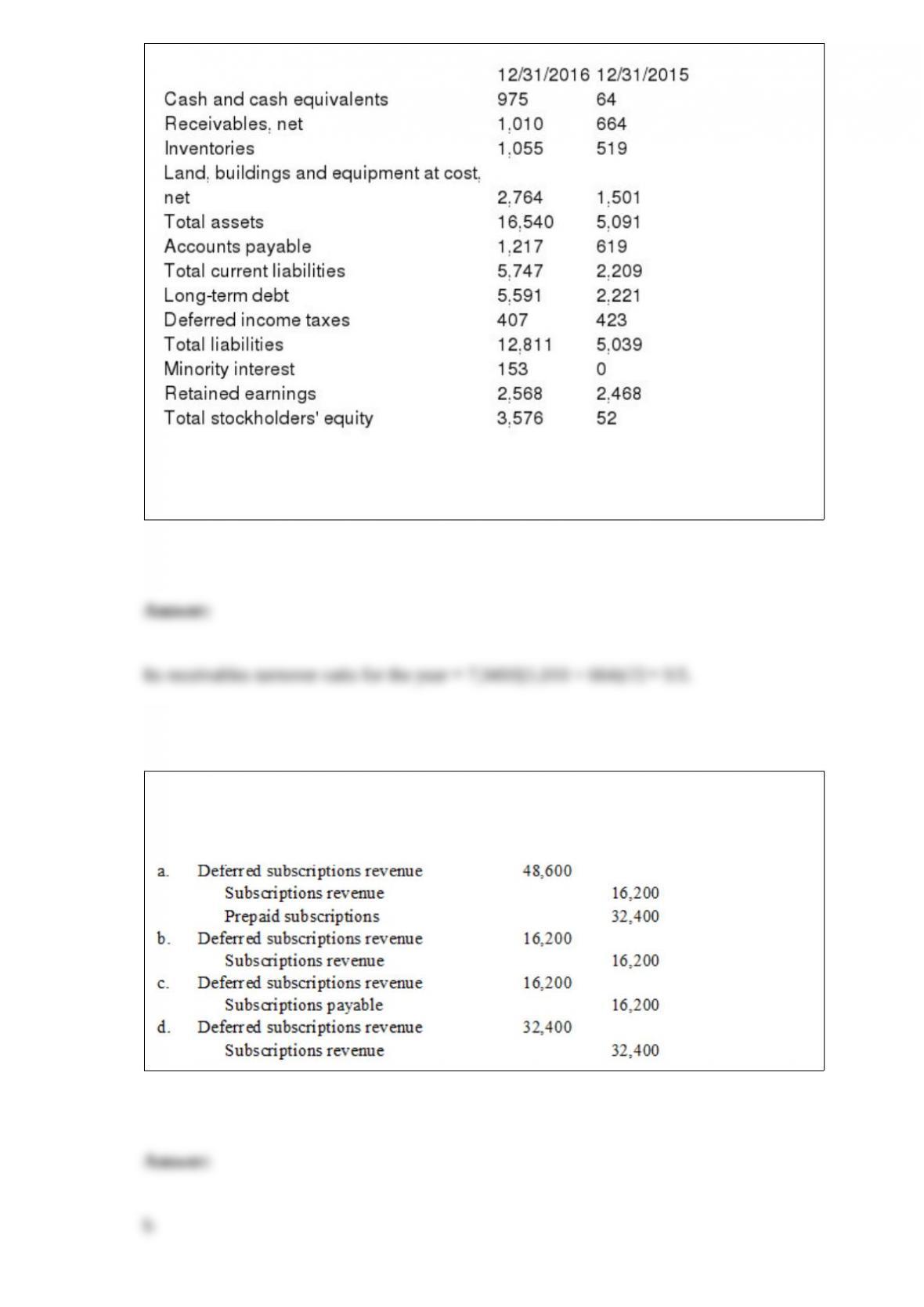

The following partial income statement and balance sheet information (in $ millions)

comes from the Annual Report of Saratoga Springs Co. for the year ending 12/31/2016:

Required: Compute the following amounts for Saratoga Springs Co.

Its receivables turnover ratio for 2016. Round your answer to one decimal place.

On September 1, 2016, Fortune Magazine sold 600 one-year subscriptions for $81 each.

The total amount received was credited to deferred subscriptions revenue. What is the

required adjusting entry at December 31, 2016?

Prepare the journal entry to record pension expense, gains or losses, past service cost,

funding, and payment of benefits for 2016.