1) The ________ of the term structure of interest rates states that the interest rate on a

long-term bond will equal the average of short-term interest rates that individuals

expect to occur over the life of the long-term bond, and investors have no preference for

short-term bonds relative to long-term bonds

A) segmented markets theory

B) expectations theory

C) liquidity premium theory

D) separable markets theory

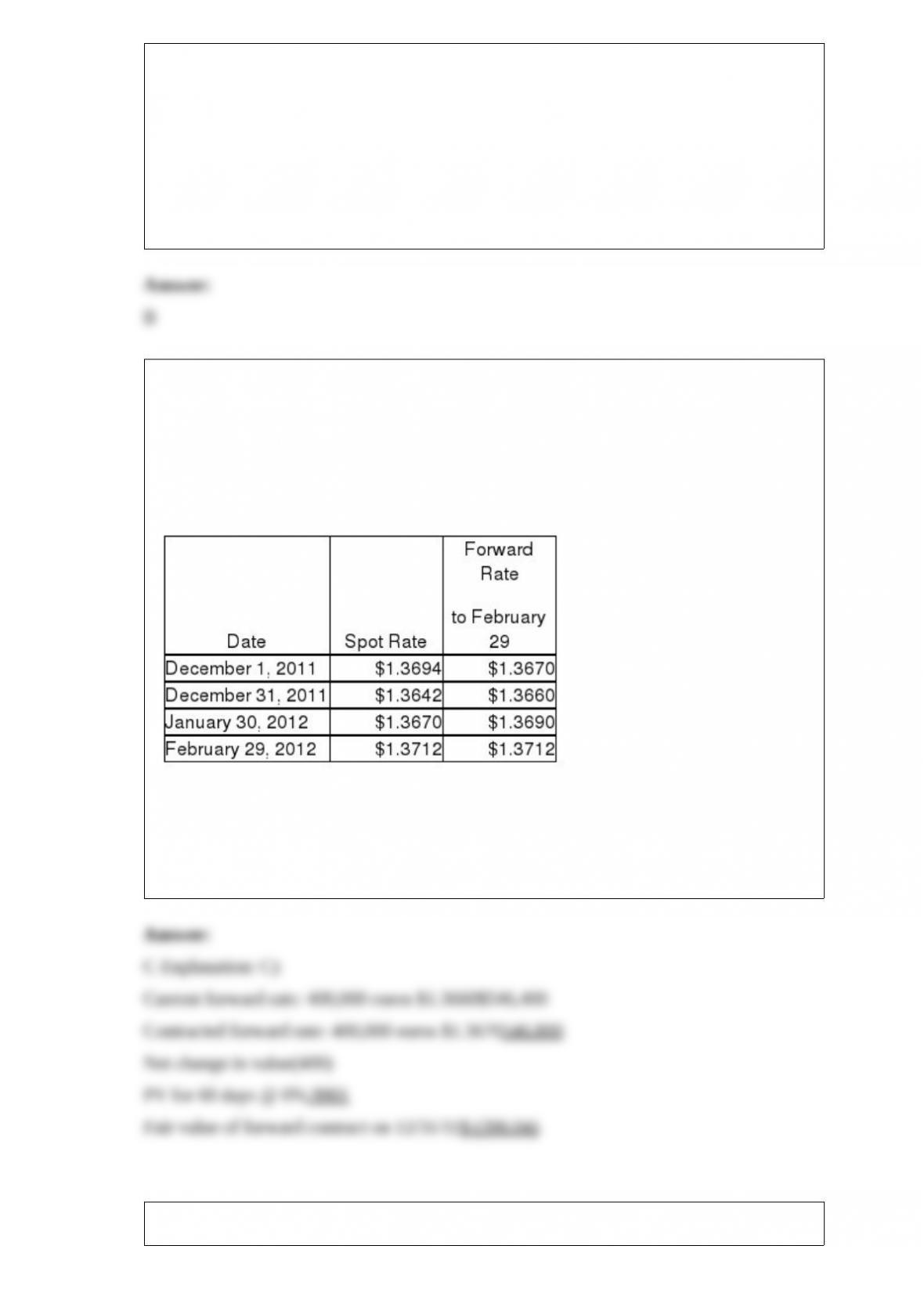

2) On December 1, 2011, Thomas Company, a U.S. corporation, purchases inventory

from a vendor in Italy for 400,000 euros. Payment is due in 90 days. To hedge the

transaction, Thomas signs a forward contract to buy 400,000 euros in 90 days at

$1.3670. Thomas uses a discount rate of 6% (present value factor for 30 days = .9950;

60 days = .9901; 90 days = .9851). Assume the forward contract will be settled net and

this is a cash flow hedge. Currency exchange rates are shown below:

What is the fair value of the forward contract at December 31, 2011?

A) $400.00 liability

B) $400.00 asset

C) $396.04 liability

D) $396.04 asset

3) Which of the following are entitled to the remainder of the estate after all other

rightful claims on the estate have been satisfied?

A) Remainder beneficiaries

B) Residual beneficiaries

C) Alternate beneficiaries

D) Secondary beneficiaries

4) Governmental accounting differs from corporate financial accounting primarily

because

A) the size of the government and the various levels would make it unreasonable to use

corporate GAAP

B) governments lack a profit motive and must focus on accountability to the public they

serve

C) the government has no stakeholders who require financial reporting

D) the government has too many types of organizations to use one type of corporate

GAAP

5) When yield curves are flat,

A) long-term interest rates are above short-term interest rates

B) short-term interest rates are above long-term interest rates

C) short-term interest rates are about the same as long-term interest rates

D) medium-term interest rates are above both short-term and long-term interest rates

6) A decrease in the riskiness of corporate bonds will ________ the yield on corporate

bonds and ________ the yield on Treasury securities, everything else held constant

A) increase; increase

B) decrease; decrease

C) increase; decrease

D) decrease; increase

7) Plenty Corporation issued six thousand, $1,000 par, 6% bonds on January 1, 2010, at

par. Interest is paid on January 1 and July 1 of each year; the bonds mature on January

1, 2015 . On January 2, 2012, Scrawn Corporation, a 75%-owned subsidiary of Plenty,

purchased 3,000 of the bonds on the open market at 102.50 . Plenty’s separate net

income for 2012 included the annual interest expense for all 3,000 bonds. Scrawn’s

separate net income for 2012 was $400,000, which included the bond interest received

on July 1 as well as the accrual of bond interest revenue earned on December 31 . Both

companies use straight-line amortization of bond discounts/premiums.

If the bonds were originally issued at 103, and 70% of them were purchased on January

2, 2014 at 104, the constructive gain or (loss) on the purchase was

A) $(142,800).

B) $( 42,000).

C) $ 42,000.

D) $ 142,800.

8) Jacana Company uses the LIFO inventory method. During the second quarter, Jacana

experienced a 100-unit liquidation in its LIFO inventory at a LIFO cost of $430 per

unit. Jacana considered the liquidation temporary and expects to replace the units in the

third quarter at an estimated replacement cost of $460 a unit. The cost of goods sold

computation in the interim report for the second quarter will

A) include the 100 liquidated units at the $460 estimated replacement unit cost

B) include the 100 liquidated units at the $430 LIFO unit cost

C) be understated by $3,000

D) be overstated by $3,000

9) If the possibility of a default increases because corporations begin to suffer losses,

then the default risk on corporate bonds will ________, and the bonds’ returns will

become ________ uncertain, meaning that the expected return on these bonds will

decrease, everything else held constant

A) increase; less

B) increase; more

C) decrease; less

D) decrease; more

10) Quincy has decided to retire from the partnership of Quincy, Robert, and Sam. The

partnership will pay Quincy $400,000. Total partnership capital should be revalued

based on the excess payment to Quincy. (Assume the book values of the assets listed

below equals fair values.) A summary balance sheet for the Quincy, Robert, and Sam

partnership appears below. Quincy, Robert, and Sam share profits and losses in a ratio

of 1:1:3, respectively.

Assets

Cash$ 150,000

Marketable securities76,000

Inventory164,000

Land300,000

Building-net510,000

Total assets$1,200,000

Equities

Quincy, capital320,000

Robert, capital280,000

Sam, capital600,000

Total equities$1,200,000

What goodwill will be recorded?

A) $ 80,000

B) $240,000

C) $320,000

D) $400,000

11) If a parent company has controlling interest in a subsidiary which has no potentially

dilutive securities outstanding, then in the calculation of consolidated diluted EPS, it

will be necessary to

A) only make an adjustment of subsidiary’s basic earnings

B) replace the parent’s equity in subsidiary earnings with the parent’s equity in

subsidiary’s diluted EPS

C) make a replacement calculation in the parent’s basic earnings for the EPS

D) only use the parent’s common shares and shares represented by the parent’s

potentially dilutive securities

12) If an affiliate purchases bonds in the open market, the book value of the

intercompany bond liability at the time of purchase is

A) always assigned to the parent company because it has control

B) the par value of the bonds less the unamortized discount or plus the unamortized

premium

C) par value

D) the par value of the bonds plus the unamortized discount or less the unamortized

premium

13) Chapter 7 bankruptcy cases differ from Chapter 11 bankruptcy cases because

Chapter 7 bankruptcy

A) is involuntary

B) requires a reorganization plan that is approved by the court

C) requires the debtor corporation to file a list of creditors, schedule of assets and

liabilities, and work with a trustee

D) leads to full liquidation of the bankrupt company

14) The Bush tax cut reduced the top income tax bracket from 39% to 35% over a

ten-year period Supply and demand analysis predicts the impact of this change was a

________ interest rate on municipal bonds and a ________ interest rate on Treasury

bonds

A) higher; lower

B) lower; lower

C) higher; higher

D) lower; higher

15) Which of the following is not an approach appropriate for hedge accounting?

A) Cash Flow Hedge Accounting

B) Critical Term Hedge Accounting

C) Fair Value Hedge Accounting

D) Hedge of Net Investment in Foreign Subsidiary

16) Everything else held constant, an increase in marginal tax rates would likely have

the effect of ________ the demand for municipal bonds, and ________ the demand for

US government bonds

A) increasing; increasing

B) increasing; decreasing

C) decreasing; increasing

D) decreasing; decreasing

17) In contrast with single entity organizations, consolidated financial statements

include which of the following in the calculation of cash flows from operating activities

under the indirect method?

A) Cash paid to employees

B) Noncontrolling interest dividends paid

C) Noncontrolling interest share

D) Proceeds from the sale of land

18) With regard to a variable interest entity (VIE), Ann Company may meet the

following two conditions:

Condition I

Ann Company has the power to direct VIE activities that significantly impact VIE’s

economic performance.

Condition II

Ann Company has an obligation to absorb losses and/or a right to receive significant

benefits from the VIE.

Ann Company must consolidate a VIE if

A) Condition I is met only

B) Condition II is met only

C) either Condition I or Condition II is met

D) both Condition I and Condition II are met

19) On January 1, 2011, Bambi borrowed $500,000 from Lonni. The five-year term

note carries a variable rate interest, based on LIBOR, and interest is payable at

December 31 of each year, compounded annually. The first year’s rate of interest is 6%

and Bambi would like to assure that their rate does not increase. Bambi enters into a

pay-fixed, receive-variable interest rate swap agreement with Third National Bank,

under which Bambi will pay 6%, fixed. At December 31, 2011, it is determined that

Bambi’s interest rate to Lonni for the next year will be 5%. Treat as a cash flow hedge.

Required:

Determine the estimated fair value of the hedge at December 31, 2011, and prepare the

related journal entry required to document this hedge and the related interest payment at

December 31, 2011 . Assume the interest rate curve is flat.

20) Perry Instruments International purchased 75% of the outstanding common stock of

Standard Systems in 1997 when the book values and fair values of Standard’s assets and

liabilities were equal. The cost of Perry’s investment was equal to 75% of the book

value of Standard’s net assets. Separate company income statements for Perry and

Standard for the year ended December 31, 2011 are summarized as follows:

Perry Standard

Sales Revenue$2,400,000 $800,000

Investment income from Standard142,000

Cost of Goods Sold(1,600,000)(400,000)

Expenses(450,000)(200,000)

Net Income$492,000 $200,000

During 2011, the companies began to manage their inventory differently, and worked

together to keep their inventories low at each location. In doing so, they agreed to sell

inventory to each other as needed at a markup of 10% of cost. Perry sold merchandise

that cost $100,000 to Standard for $110,000, and Standard sold inventory that cost

$80,000 to Perry for $88,000. Half of this merchandise remained in each company’s

inventory at December 31, 2011 .

Required:

Prepare a consolidated income statement for Perry Corporation and Subsidiary for 2011

21) Prepare journal entries to record the following grant-related transactions of an

Enterprise Fund.

1>Received an operating grant in cash from the state, $2,500,000.

2>Incurred and paid qualifying operating expenses on the state grant program,

$1,600,000.

3>Received a federal grant to finance construction of a plant, $4,500,000 (cash received

in advance).

4>Incurred and paid construction costs on the plant, $3,000,000. The plant is not

completed.

22) Balance sheet information for Sphinx Company at January 1, 2011, is summarized

as follows:

Current assets$230,000Liabilities$300,000

Plant assets450,000Capital stock $10 par200,000

Retained earnings 180,000

$680,000$680,000

Sphinx’s assets and liabilities are fairly valued except for plant assets that are

undervalued by $50,000. On January 2, 2011, Pyramid Corporation issues 20,000

shares of its $10 par value common stock for all of Sphinx’s net assets and Sphinx is

dissolved. Market quotations for the two stocks on this date are:

Pyramid common:$28.00

Sphinx common:$19.50

Pyramid pays the following fees and costs in connection with the combination:

Finder’s fee$10,000

Legal and accounting fees6,000

Required:

1>Calculate Pyramid’s investment cost of Sphinx Corporation.

2>Calculate any goodwill from the business combination.

23) Oceana Corporation is being liquidated under Chapter 7 of the Bankruptcy Act. The

trustee has determined that the unsecured claims will receive $.35 on the dollar.

Loans-R-Us holds a $1,000,000 mortgage note receivable from Oceana that is secured

by building and equipment with a $1,200,000 book value and a $900,000 fair value.

Required:

How much of the mortgage receivable will Loans-R-Us recover?

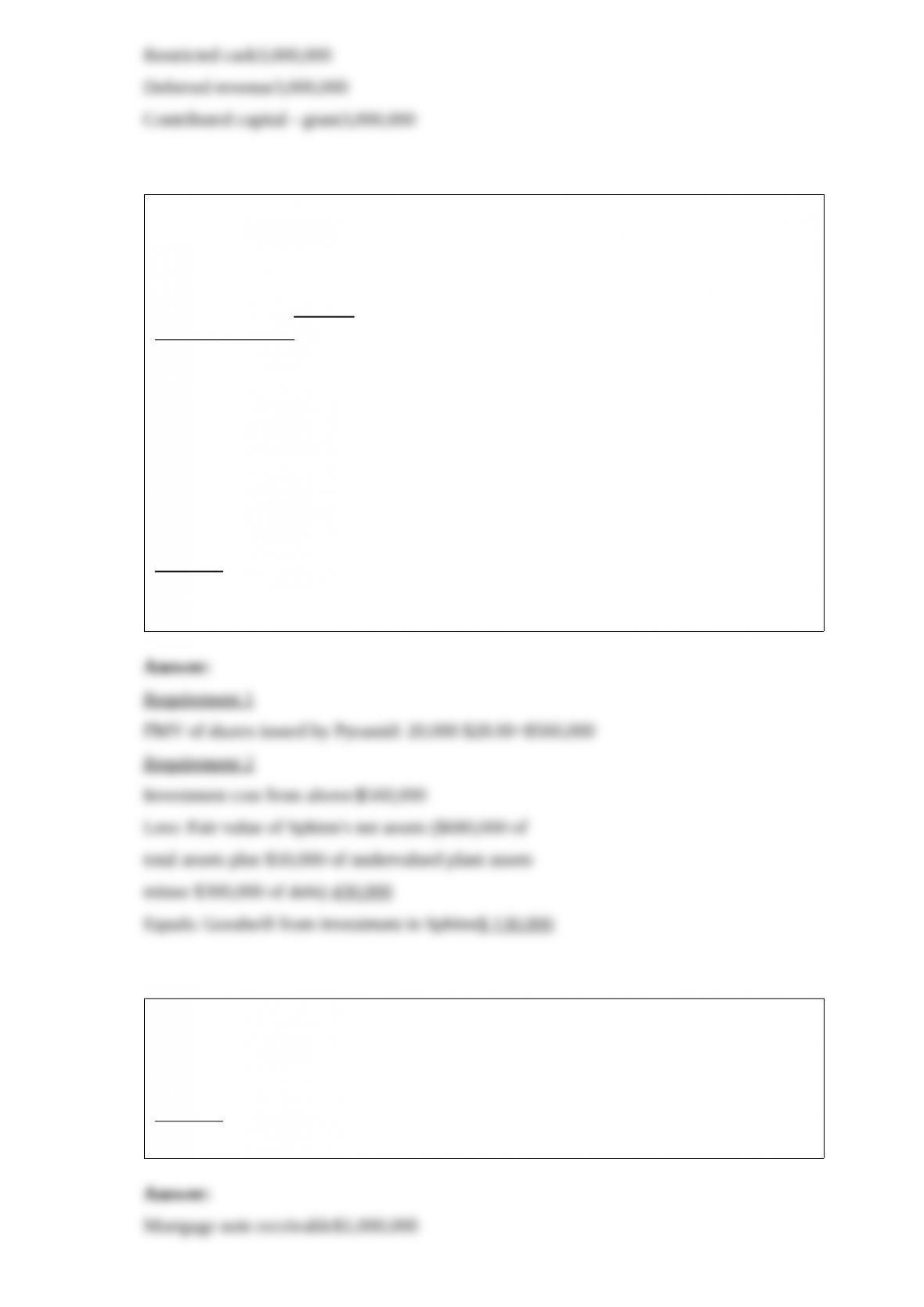

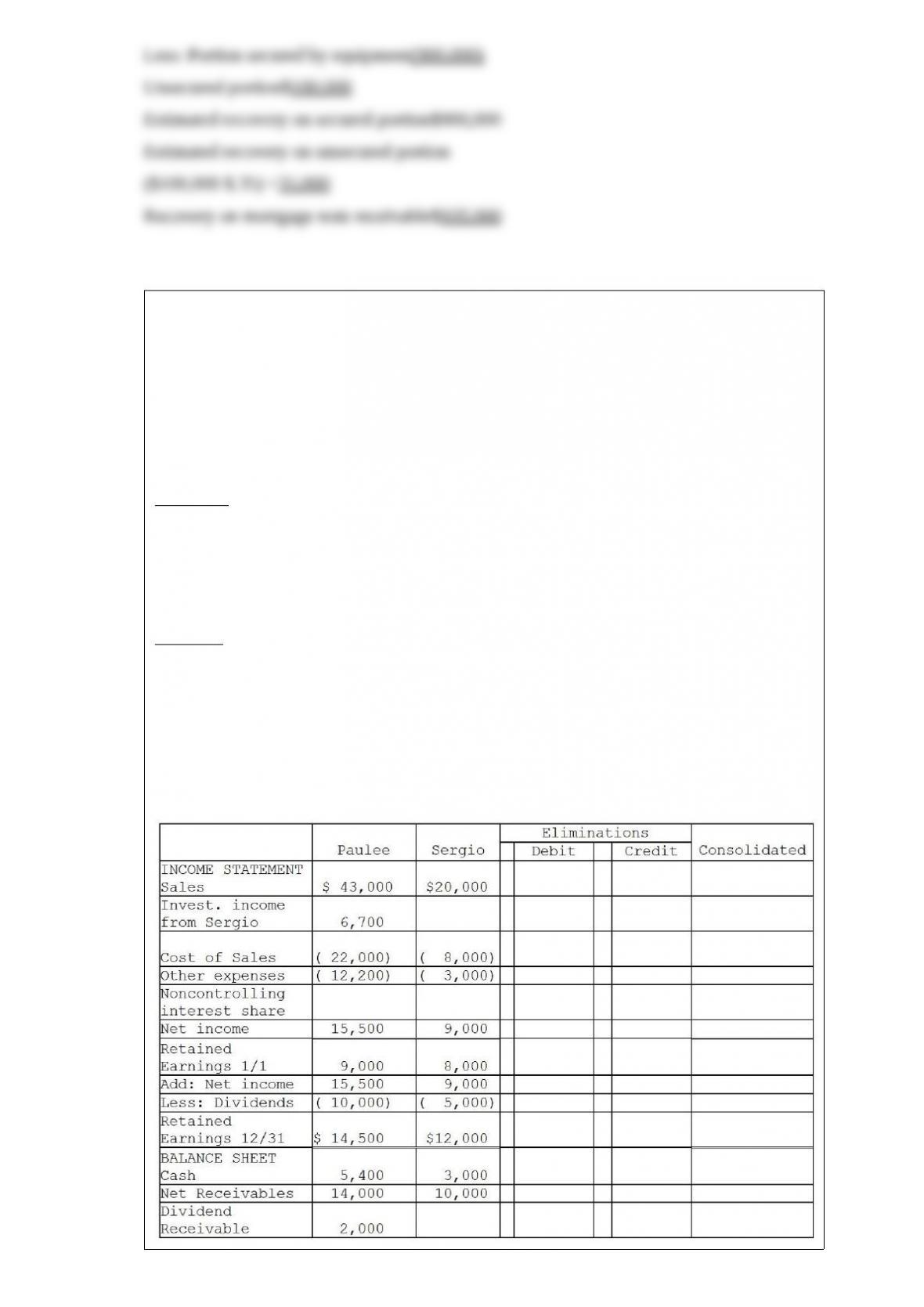

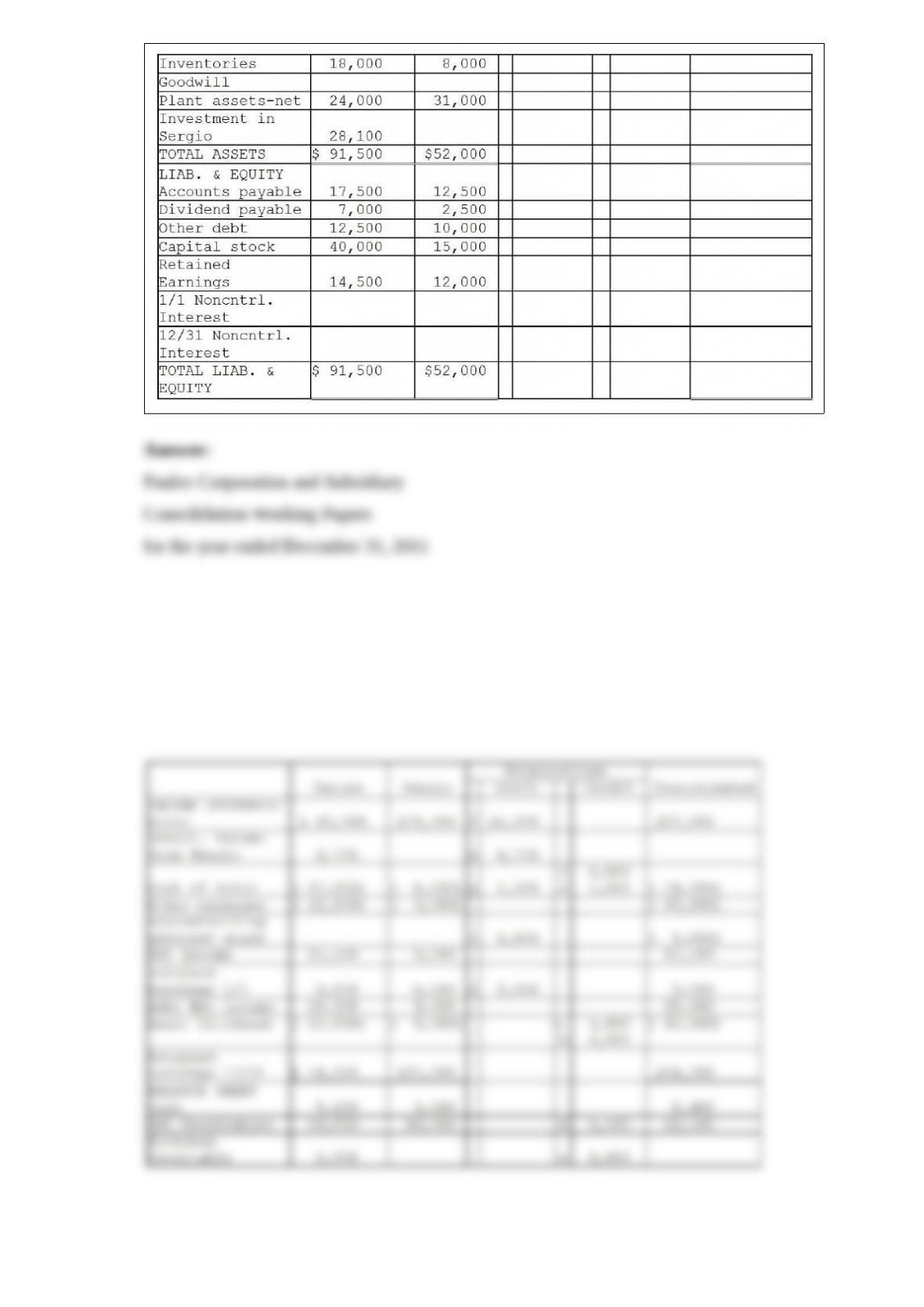

24) Paulee Corporation paid $24,800 for an 80% interest in Sergio Corporation on

January 1, 2010, at which time Sergio’s stockholders’ equity consisted of $15,000 of

Common Stock and $6,000 of Retained Earnings. The fair values of Sergio

Corporation’s assets and liabilities were identical to recorded book values when Paulee

acquired its 80% interest.

Sergio Corporation reported net income of $4,000 and paid dividends of $2,000 during

2010 .

Paulee Corporation sold inventory items to Sergio during 2010 and 2011 as follows:

20102011

Paulee’s sales to Sergio$5,000$6,000

Paulee’s cost of sales to Sergio3,0003,500

Unrealized profit at year-end1,0001,500

At December 31, 2011, the accounts payable of Sergio include $1,500 owed to Paulee

for inventory purchases.

Required:

Financial statements of Paulee and Sergio appear in the first two columns of the

partially completed working papers. Complete the consolidation working papers for

Paulee Corporation and Subsidiary for the year ended December 31, 2011 .

Paulee Corporation and Subsidiary

Consolidation Working Papers

for the year ended December 31, 2011

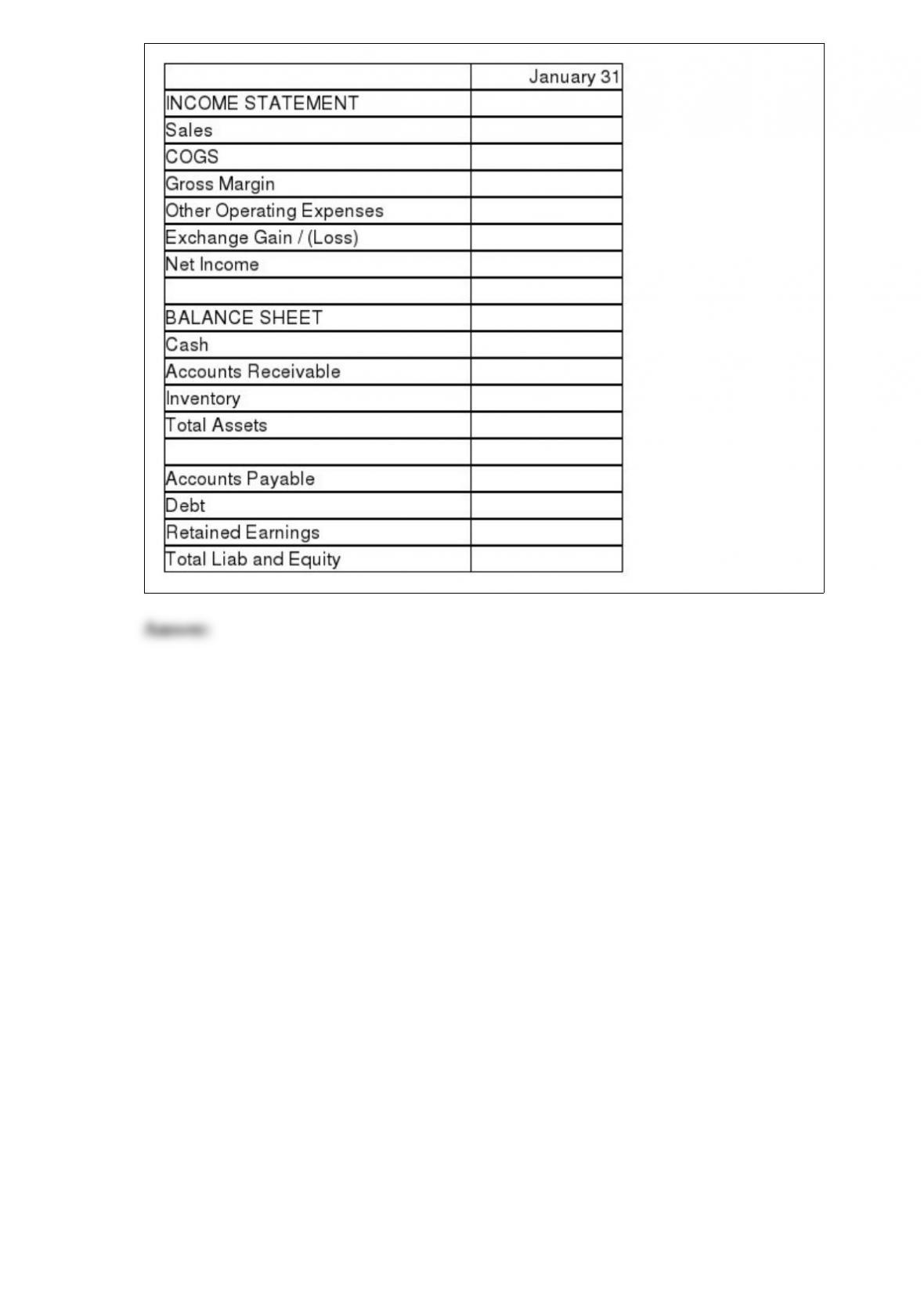

25) Meric Corporation (a U.S. company) began operations on January 1, 2011, when

the owner borrowed $150,000 to start the company. In the first month of operations,

Meric had the following transactions:

January 3, 2011Bought inventory for 100,000 Brazilian real on account. Must be paid

with Brazilian real.

January 8, 2011Sold 60% of inventory acquired on 1/3/11 for 32,000 British pounds on

account. Invoice denominated in British pounds.

January 10, 2011Paid $3,000 in other operating expenses

January 23, 2011Acquired and paid half of the Brazilian real owed to the Brazilian

supplier

January 28, 2011Collected half of the 32,000 pounds from the customer in Great Britain

and immediately converted them into U.S. dollars

The following exchange rates apply:

DateRateRate

January 3$.6260 = 1 real$1.5950 = 1 pound

January 8$.6230 = 1 real$1.5760 = 1 pound

January 10$.6210 = 1 real$1.5880 = 1 pound

January 23$.6250 = 1 real$1.5610 = 1 pound

January 28$.6330 = 1 real$1.5570 = 1 pound

January 31$.6180 = 1 real$1.5720 = 1 pound

Required: Complete the summary income statement and balance sheet for the month

ended January 31, 2011 assuming there were no other transactions.

26) Marshfield Hospital is a private, not-for-profit hospital. The following transactions

occurred:

1>Unrestricted cash gifts that were received last year, but designated for use in the

current year, totaled $180,000. The cash gifts were used in the current year in

accordance with restrictions.

2>Unrestricted pledges of $800,000 were received. Ten percent of the pledges typically

prove uncollectible. Additional cash contributions during the year totaled $300,000.

3>Gifts in kind were received that were sold at a silent auction for $23,000. The fair

value of the donated gifts in kind could not be reasonably determined.

4>Expenses were incurred and paid as follows: Salary of doctor, $190,000; facility

rental, $36,000; purchases of supplies, $8,000; and utility costs, $10,000.

5>Marketable securities with a fair value of $650,000 were received as a donation with

a stipulation that the hospital use the funds to purchase suitable land for the hospital.

Required:

Prepare journal entries for the aforementioned transactions.

27) Rusty Nail died in the summer of 2011 . The following transactions occurred

relating to Rusty’s estate.

1>Rusty’s estate included a $50,000 Certificate of Deposit. When Rusty died, there was

$250 accrued but unpaid interest. When the check was received for the normal

semiannual interest payment, it was in the amount of $1,250.

2>Rusty’s will requested a specific transfer to the local playhouse in the amount of

$20,000. Avery’s estate should be adequate to cover all obligations and devises, and the

amount is paid.

3>A fee for probate court is paid amounting to $1,400.

4>Funeral expenses are paid amounting to $13,000.

5>A bill is received from the anesthesiologist relating to Rusty’s last hospital stay for

$22,000. The bill is not covered by insurance, and was not included in the estate

inventory. The bill is verified and paid.

Required:

Prepare the journal entries for the listed transactions. Disregard the impact of estate and

income taxes.

28) Old West City had the following transactions in fiscal 2011 . Assume that all

expenditures were properly appropriated in the fiscal 2011 budget.

1>A six-month loan was made to the special revenue fund from the general fund

amounting to $28,000.

2>A purchase order for landscaping maintenance services was issued in the amount of

$43,000.

3>A $10,000 nonreciprocal transfer was made to the debt service fund to pay interest

amounts outstanding.

4>The final invoice for landscaping maintenance was received in the amount of

$39,000, and it was scheduled to be paid in 30 days.

5>The city enters into a capital lease of fixed assets for the general government. The

present value of the minimum lease payments equals $70,000.

Required:

Prepare the journal entries for the General Fund.