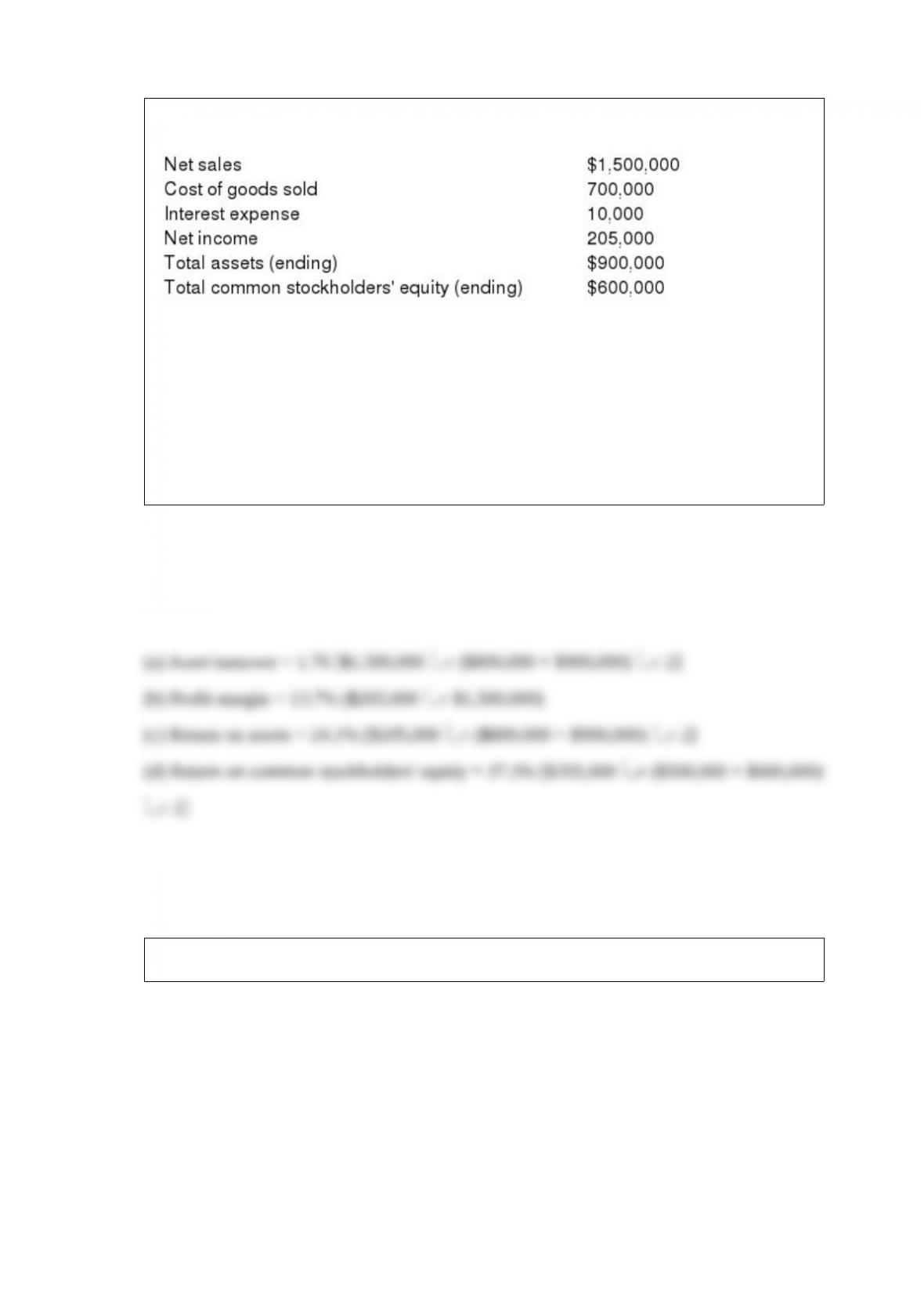

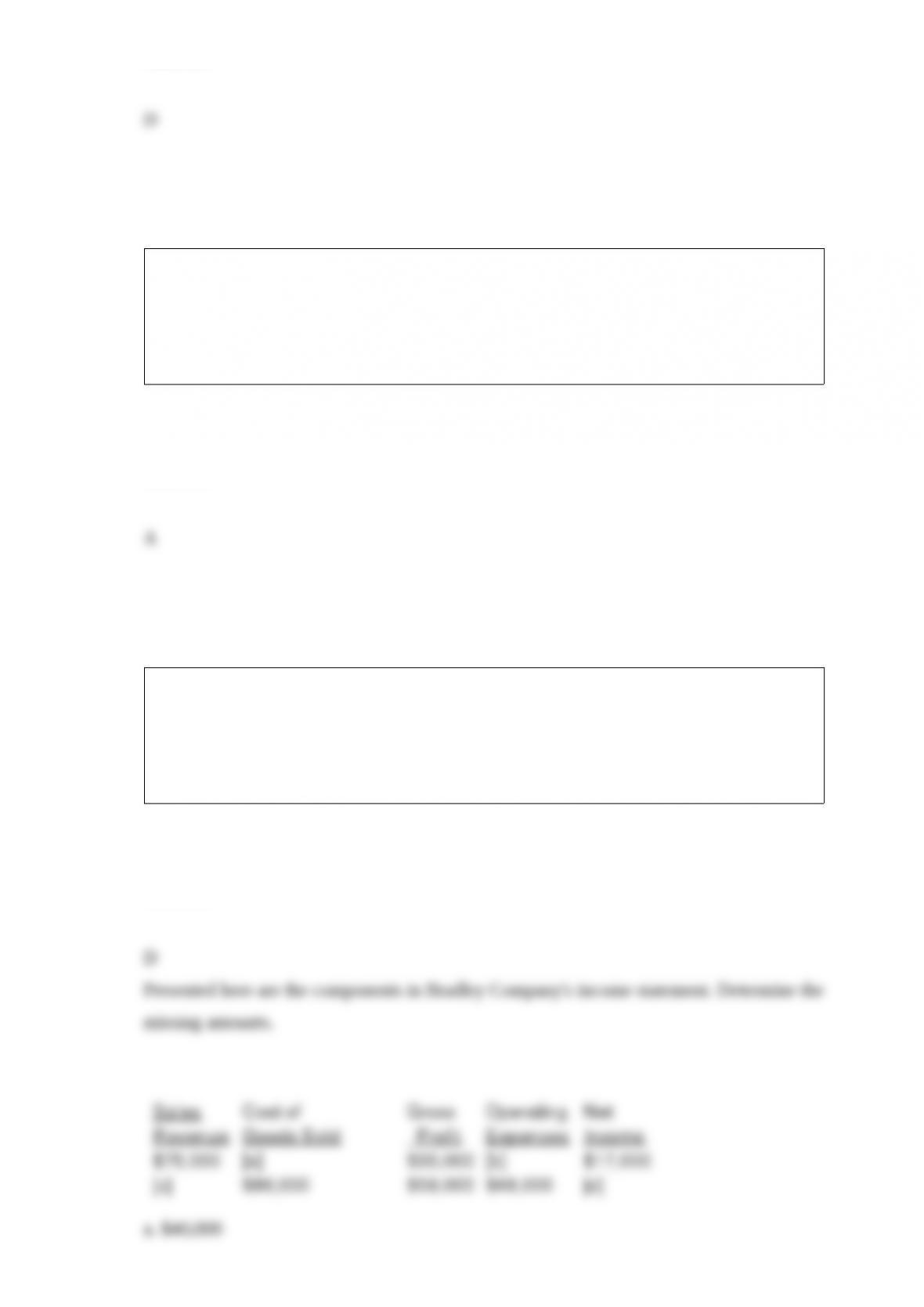

Selected financial statement data for Homer Company are presented below.

Total assets at the beginning of the year were $800,000; total common stockholders’

equity was $500,000 at the beginning of the period.

Instructions

Compute each of the following:

(a) Asset turnover

(b) Profit margin

(c) Return on assets

(d) Return on common stockholders’ equity

Answer:

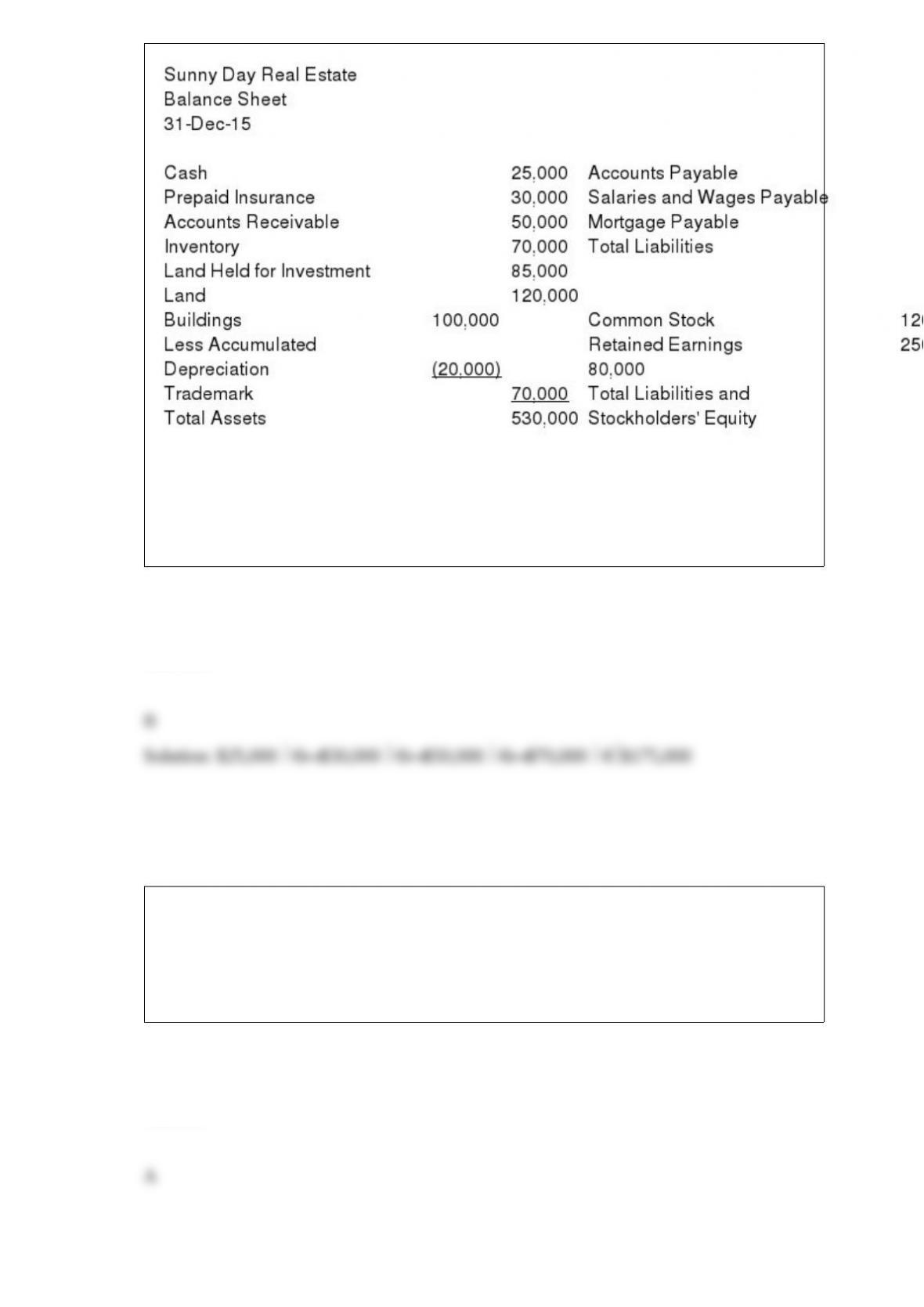

The following information is for Sunny Day Real Estate:

The total dollar amount of assets to be classified as current assets is

a. $105,000.

b. $175,000.

c. $190,000.

d. $260,000.

Answer:

If a company sells its accounts receivables to a factor,

a. the seller pays a commission to the factor.

b. the factor pays a commission to the seller.

c. there is a gain on the sale of the receivables.

d. the seller defers recognition of sales revenue until the account is collected.

Answer:

On November 30, Thatcher Company issued a $15,000, 6%, 4-month note to the

National Bank. The entry on Thatcher’s books to record the payment of the note at

maturity will include a credit to Cash for

a. $15,000.

b. $15,900.

c. $15,300

d. $15,600

Answer:

The principle of establishing responsibility does not include

a. one person being responsible for one task.

b. authorization of transactions.

c. independent internal verification.

d. approval of transactions.

Answer:

The journal entry to record a return of merchandise purchased on account under a

periodic inventory system would be

a. Accounts Payable

Purchase Returns and Allowances

b. Purchase Returns and Allowances

Accounts Payable

c. Accounts Payable

Inventory

d. Inventory

Accounts Payable

Answer:

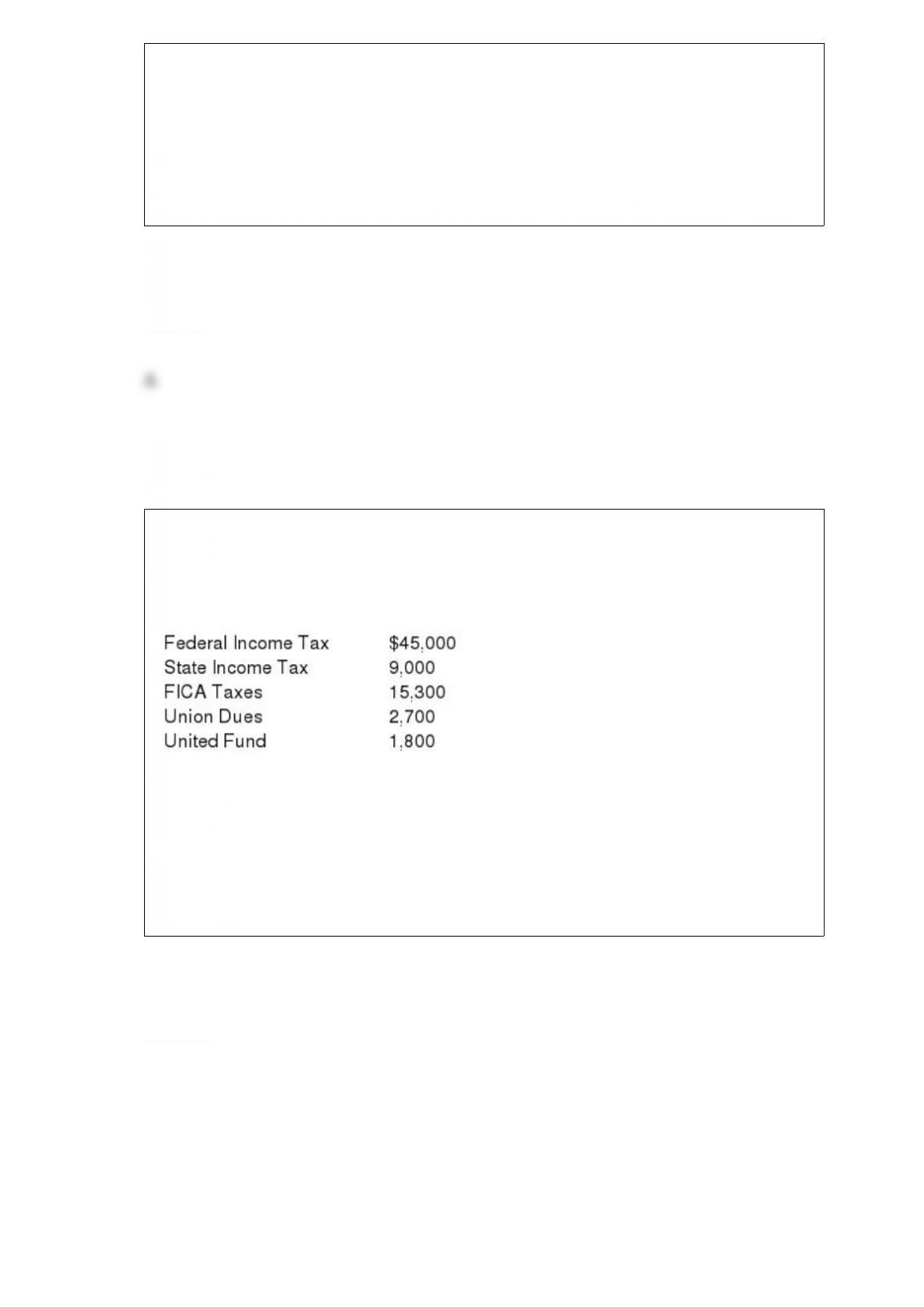

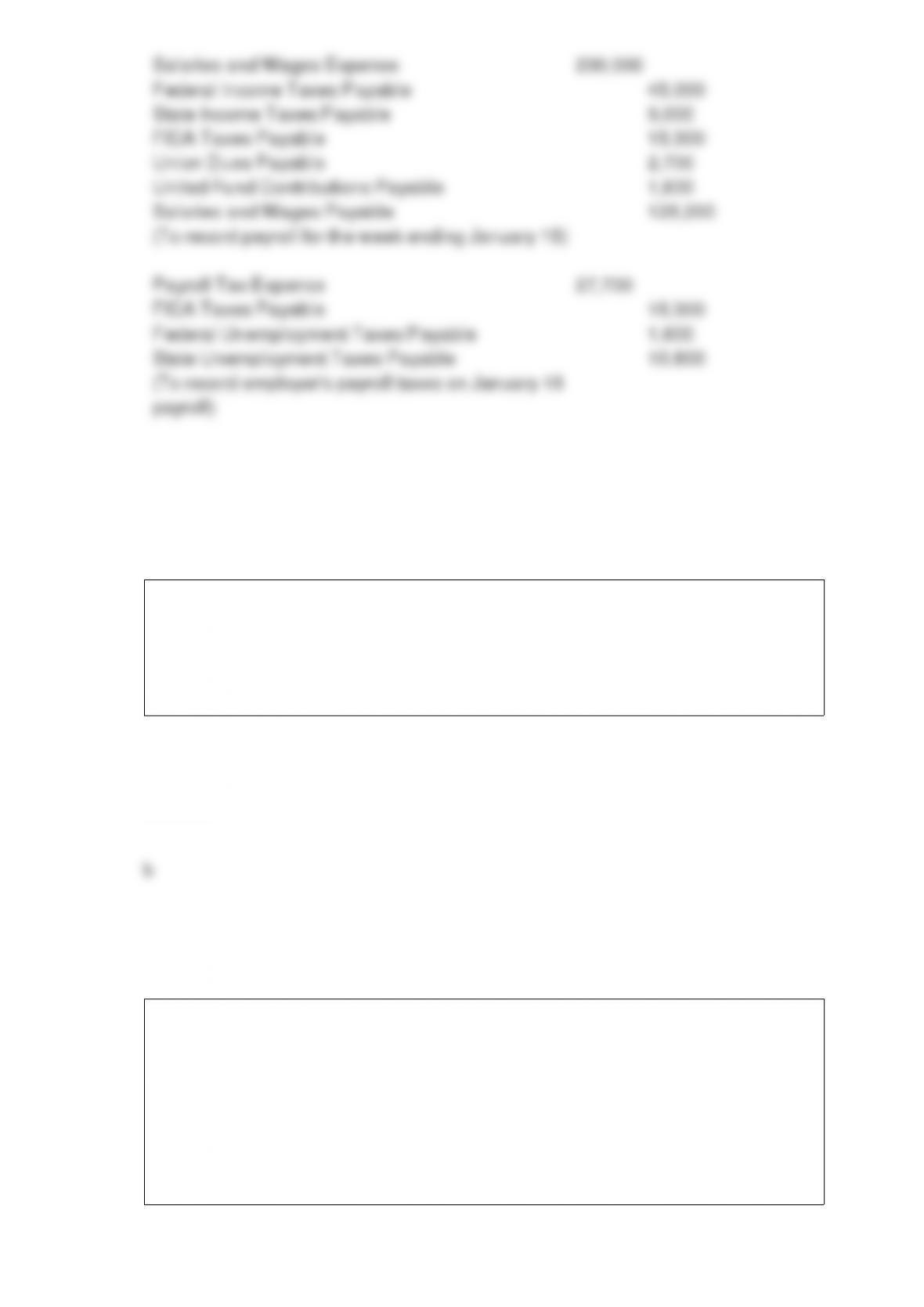

Warren Company’s payroll for the week ending January 15 amounted to $200,000 for

salaries and wages. None of the employees has reached the earnings limits specified for

federal or state employer payroll taxes. The following deductions were withheld from

employees’ salaries and wages:

Federal unemployment tax (FUTA) rate is 6.2% less a credit equal to the rate paid for

state unemployment taxes. The state unemployment tax (SUTA) rate is 5.4%.

Instructions

Prepare the journal entries to record the weekly payroll ending January 15 and also the

employer’s payroll tax expense on the payroll.

Answer:

The future value of an annuity factor for 2 periods is equal to

a. 1 plus the interest rate.

b. 2 plus the interest rate.

c. 2 minus the interest rate.

d. 2.

Answer:

Schwartzman Co., makes a credit card sale to a customer for $800. The credit card sale

has a grace period of 30 days and then an interest charge of 1.5% per month is added to

the balance. If the unpaid balance on the above sale is $640 at the end of the grace

period, the interest charge is

a. $6.40.

b. $9.60.

c. $11.00.

d. $16.00.

Answer:

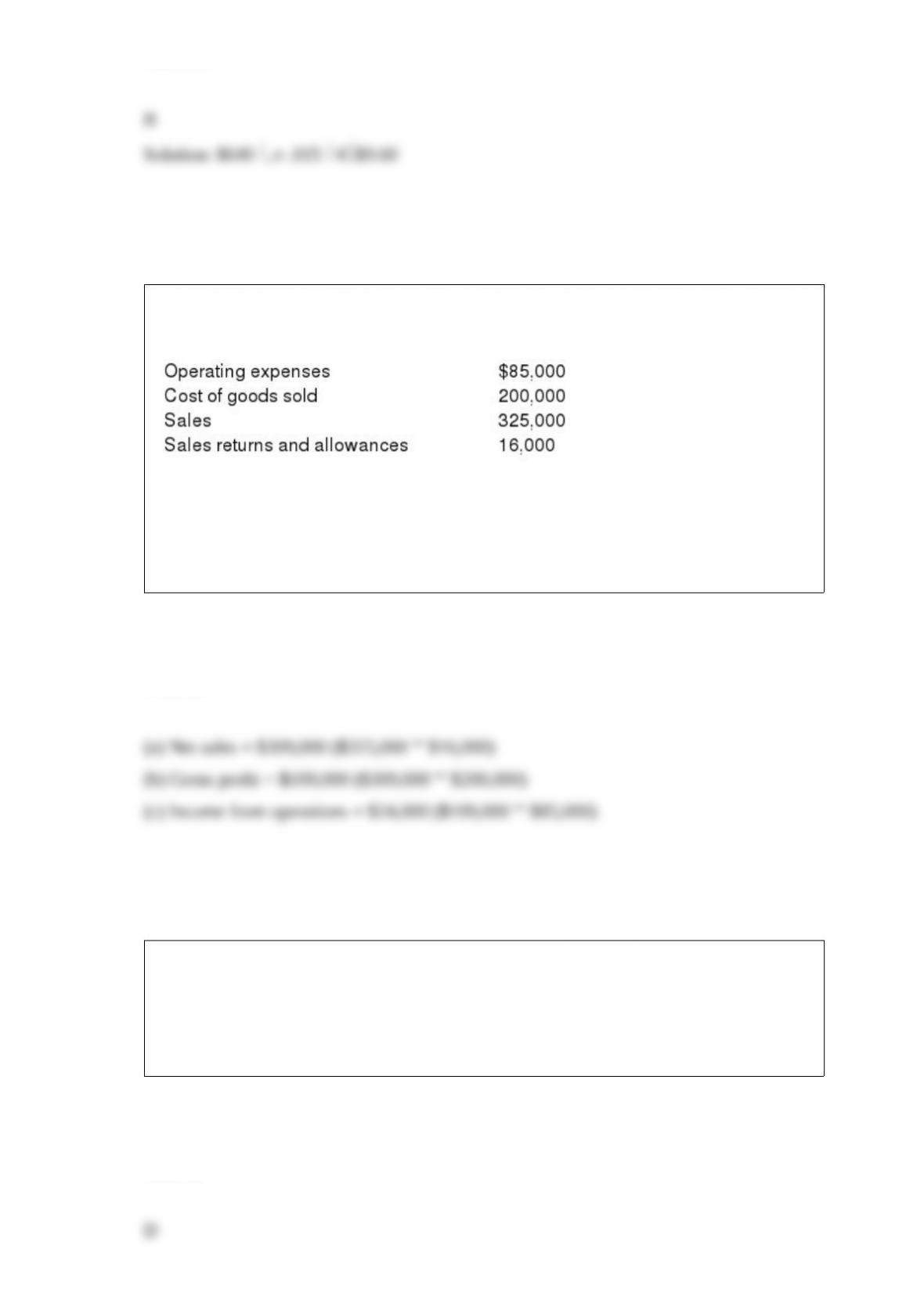

The following information is available for Sheldon Leonard Company:

Instructions

Compute each of the following:

(a) Net sales

(b) Gross profit

(c) Income from operations

Answer:

Closing entries are

a. an optional step in the accounting cycle.

b. posted to the ledger accounts from the worksheet.

c. made to close permanent or real accounts.

d. journalized in the general journal.

Answer:

Vision Company purchased treasury stock with a cost of $16,000 during 2014. During

the year, the company paid dividends of $20,000 and issued bonds payable for proceeds

of $860,000. Cash flows from financing activities for 2014 total

a. $840,000 net cash inflow.

b. $856,000 net cash inflow.

c. $860,000 net cash outflow.

d. $824,000 net cash inflow.

Answer:

The effective-interest method for amortization of bond discounts is required under

a. GAAP only.

b. IFRS only.

c. Both GAAP and IFRS.

d. Neither GAAP or IFRS.

Answer:

Which of the following would require a compound journal entry?

a. To record merchandise returned that was previously purchased on account.

b. To record sales on account.

c. To record purchases of inventory when a discount is offered for prompt payment.

d. To record collection of accounts receivable when a cash discount is taken.

Answer:

In the balance sheet, ending inventory is reported

a. in current assets immediately following accounts receivable.

b. in current assets immediately following prepaid expenses.

c. in current assets immediately following cash.

d. under property, plant, and equipment.

Answer:

The number of years of income statement information to be presented is

a. 2 years under both GAAP and IFRS.

b. 3 years under both GAAP and IFRS.

c. 2 years under GAAP and 3 years under IFRS.

d. 3 years under GAAP and 2 years under IFRS.

Answer:

Entries are made to the Petty Cash account when

a. establishing the fund.

b. making payments out of the fund.

c. recording shortages in the fund.

d. replenishing the fund.

Answer:

The respective normal account balances of Sales Revenue, Sales Returns and

Allowances, and Sales Discounts are

a. credit, credit, credit.

b. debit, credit, debit.

c. credit, debit, debit.

d. credit, debit, credit.

Answer:

Maria Queen was reviewing her business activities at the end of the year (2015) and

decided to prepare a Retained Earnings Statement. At the beginning of the year her

assets were $700,000 and her liabilities were $210,000. At the end of the year the assets

had grown to $930,000 but liabilities had also increased to $340,000. Common Stock

was $200,000 in both years. The net income for the year was $220,000. The company

paid dividends of $120,000 during the year.

Prepare a Retained Earnings statement in good form.

Answer:

Net income of a corporation should be closed to retained earnings and net losses should

be closed to paid-in capital accounts.

Answer:

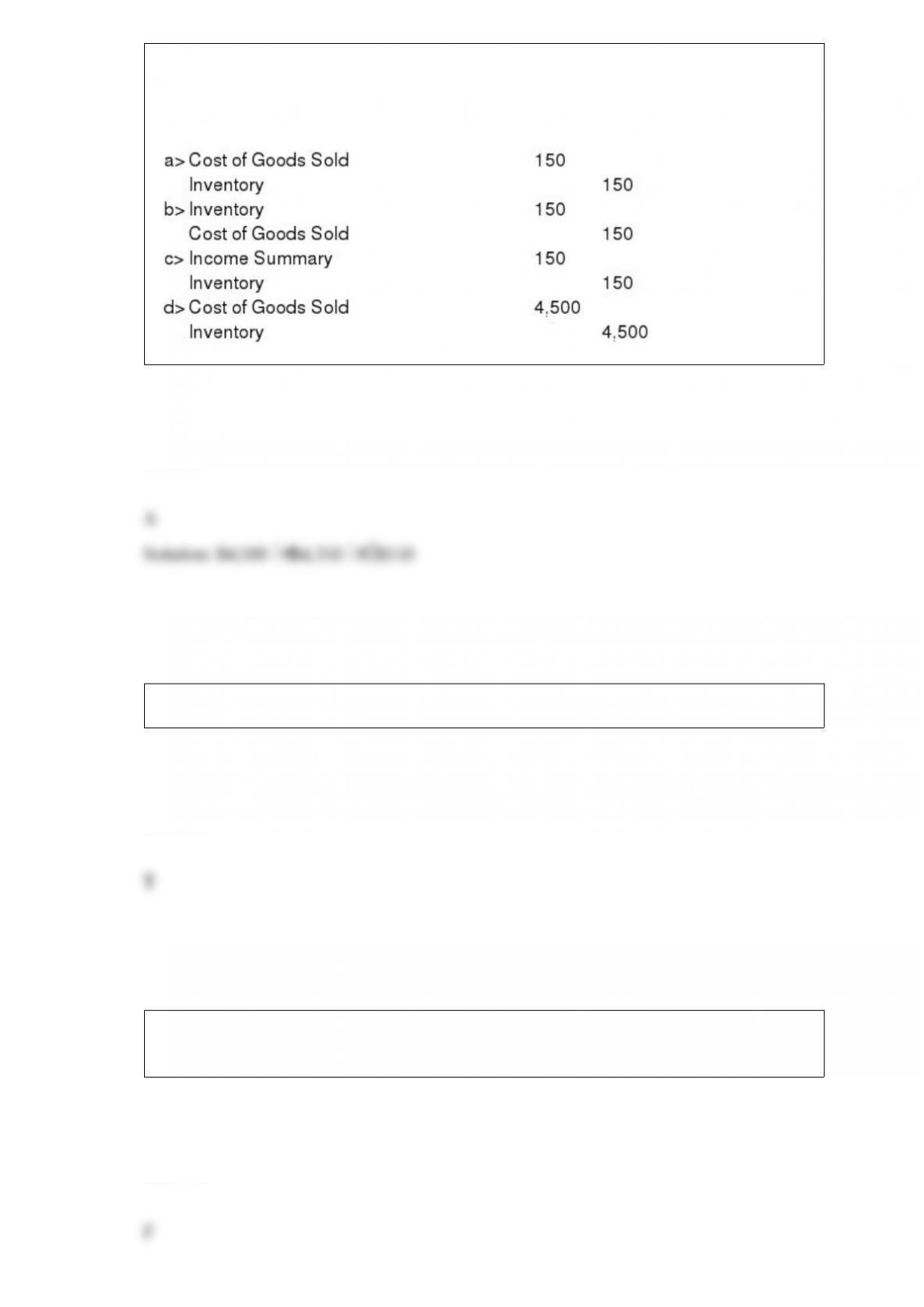

When the physical count of Rosanna Company inventory had a cost of $4,350 at year

end and the unadjusted balance in Inventory was $4,500, Rosanna will have to make the

following entry:

Answer:

Retailers and wholesalers are both considered merchandisers.

Answer:

Bonds that permit bondholders to convert them into common stock at their option are

known as callable bonds.

Answer:

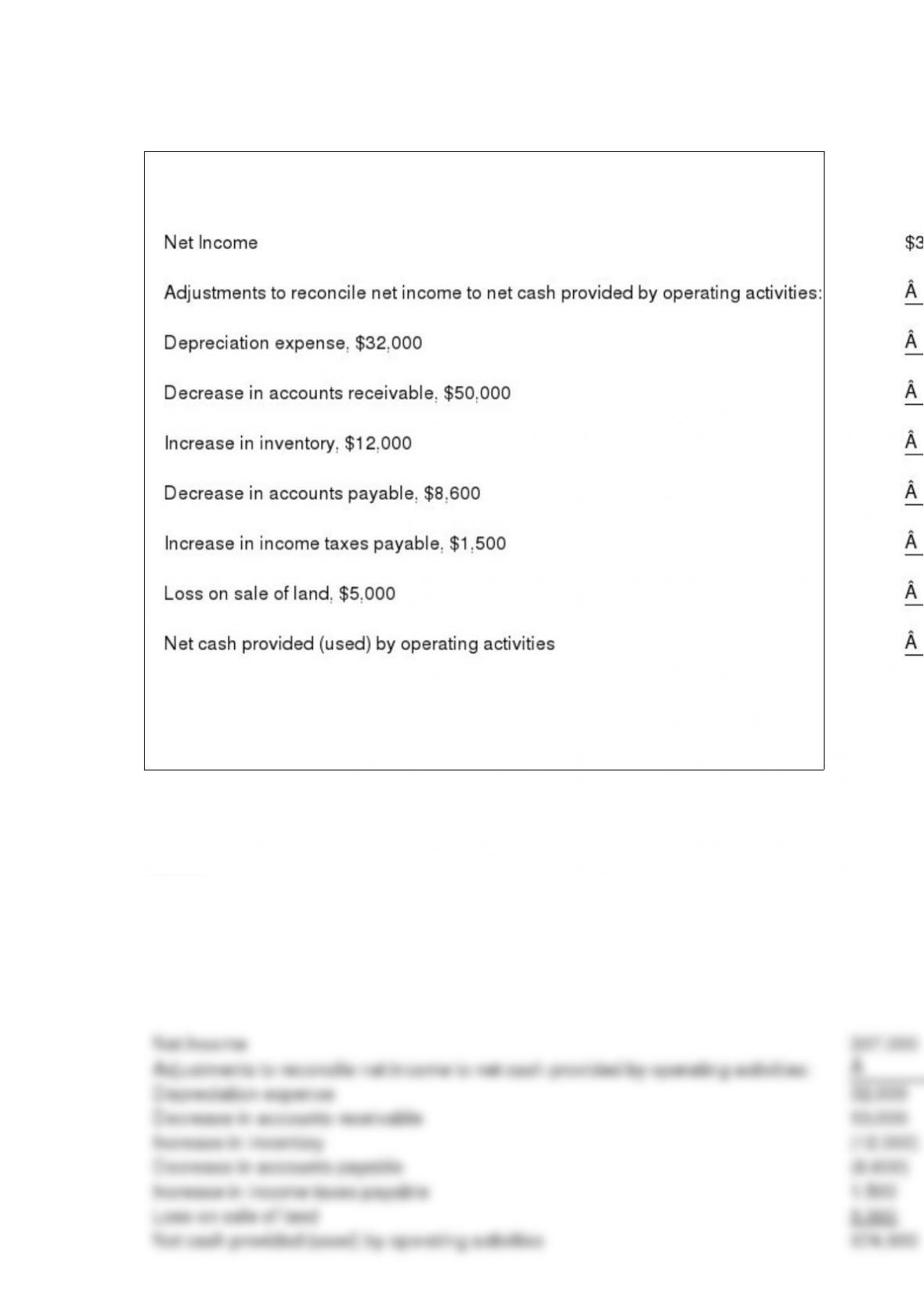

Doctor Company prepared the tabulation below at December 31, 2015.

Instructions

Show how each item should be reported in the statement of cash flows. Use parentheses

for deductions.

Answer:

Par value of stock represents the __________________ per share that must be retained

in the business for the protection of corporate ___________________.

Answer: