When a company issues a stock dividend, which of the following would be affected?

a. Earnings per share.

b. Total assets.

c. Total liabilities.

d. Total shareholders’ equity.

Kunkle Company wishes to earn 20% annually on its investments. If it makes an

investment that equals or exceeds that rate, it considers it a success. Assume that it

invests $2 million and gets $500,000 in return at the end of each year for X years. What

is the minimum value of X for which it will consider the investment a success? Assume

that it can’t invest for fractional parts of a year.

a. 4 years.

b. 6 years.

c. 7 years.

d. 9 years.

A contract does not exist for purposes of applying the revenue recognition principle in

all of the following cases except for when:

a. The seller believes it is not probable that it will collect the amount it’s entitled to

receive under the contract.

b. The seller and buyer did not sign a formalized written contract.

c. The seller and buyer can terminate the contract without penalty and neither has

performed any obligations under the contract.

d. The seller believes it is highly likely but not certain that the buyer will agree to the

terms of the contract.

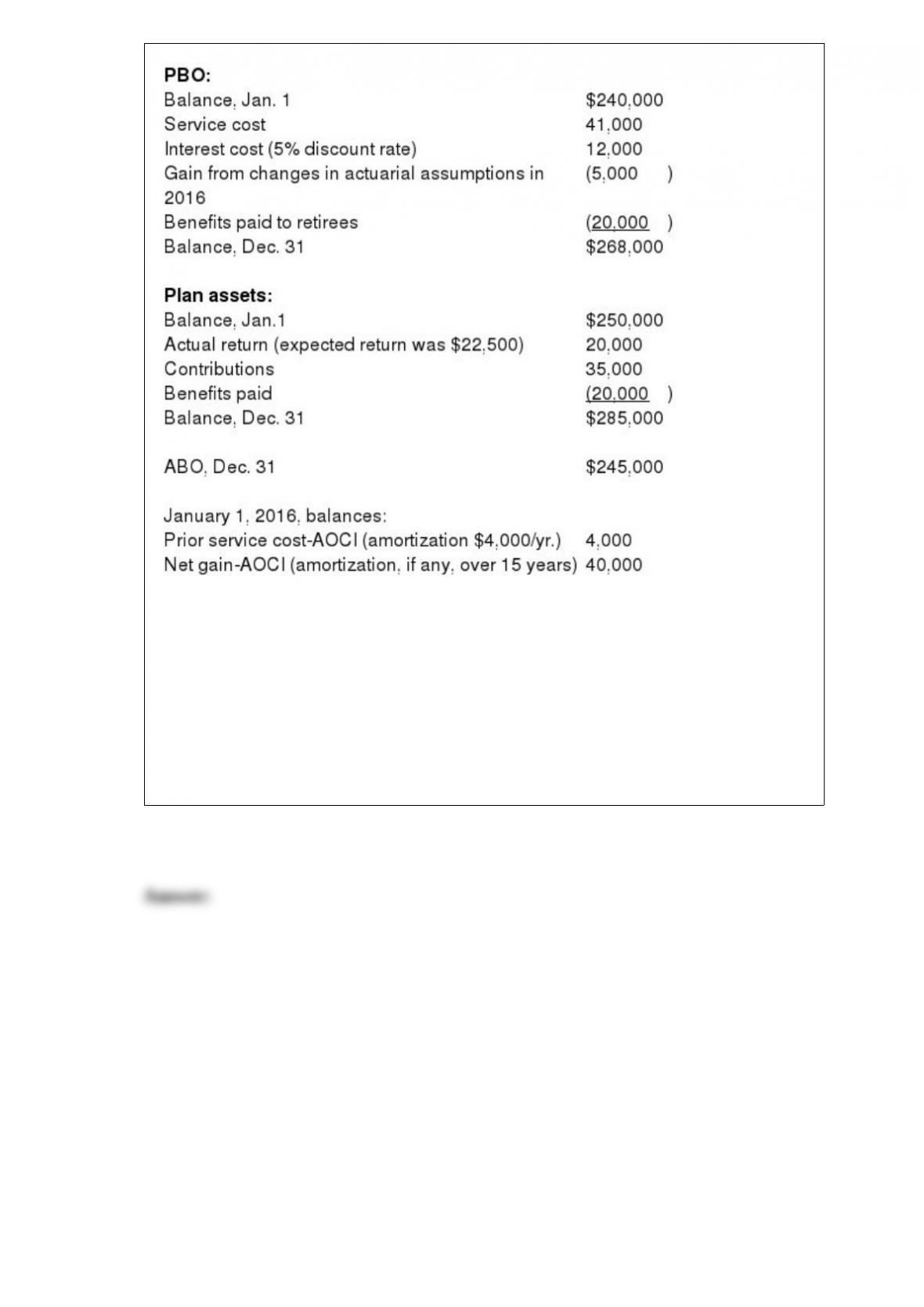

Carolina Consulting Company has a defined benefit pension plan. The following

pension-related data were available for the current calendar year:

There were no other relevant data.

Required:

1) Calculate the 2016 pension expense. Show calculations.

2) Prepare the 2016 journal entries to record pension expense and funding.

3) Prepare any journal entries to record any 2016 gains or losses.

Operating cash outflows would include:

a. Purchase of investments.

b. Purchase of equipment.

c. Payment of cash dividends.

d. Purchases of inventory.

Treasury shares are most often reported as:

a. A reduction of total shareholders’ equity.

b. A reduction of total paid-in capital.

c. A reduction of retained earnings.

d. An expense in the income statement.

In 2016, due to a change in marketing forecasts, Barney Corporation reduced the

projected life of its patent for producing round dice. The cumulative patent amortization

prior to 2016 would have been $10 million higher had the new life been used. Barney’s

tax rate is 30%. Barney’s retained earnings as of December 31, 2016, would be:

a. Overstated by $7 million.

b. Overstated by $3 million.

c. Overstated by $10 million.

d. Unaffected.

Which of the following is added to net income as an adjustment under the indirect

method of preparing the statement of cash flows?

a. Salaries payable decrease.

b. Gain on the sale of land.

c. Loss on the sale of equipment.

d. Accounts receivable increase.

The PBO is increased by:

a. An increase in the average life expectancy of employees.

b. Amortization of prior service cost.

c. An increase in the actuary’s assumed discount rate.

d. A return on plan assets that is lower than expected.

Which of the following is not a required segment reporting disclosure according to U.S.

GAAP?

a. Segment profit or loss.

b. Segment assets.

c. Segment liabilities.

d. General information about the operating segment.

Long-term assets generally include:

a. Inventory held for sale.

b. Prepaid rent.

c. Accounts receivable.

d. Land held for a possible future plant site.

Which of the following accounting changes should not be accounted for prospectively?

a. The correction of an error.

b. A change from declining balance to straight-line depreciation.

c. A change from straight-line to declining balance depreciation.

d. A change in the expected salvage value of a depreciable asset.

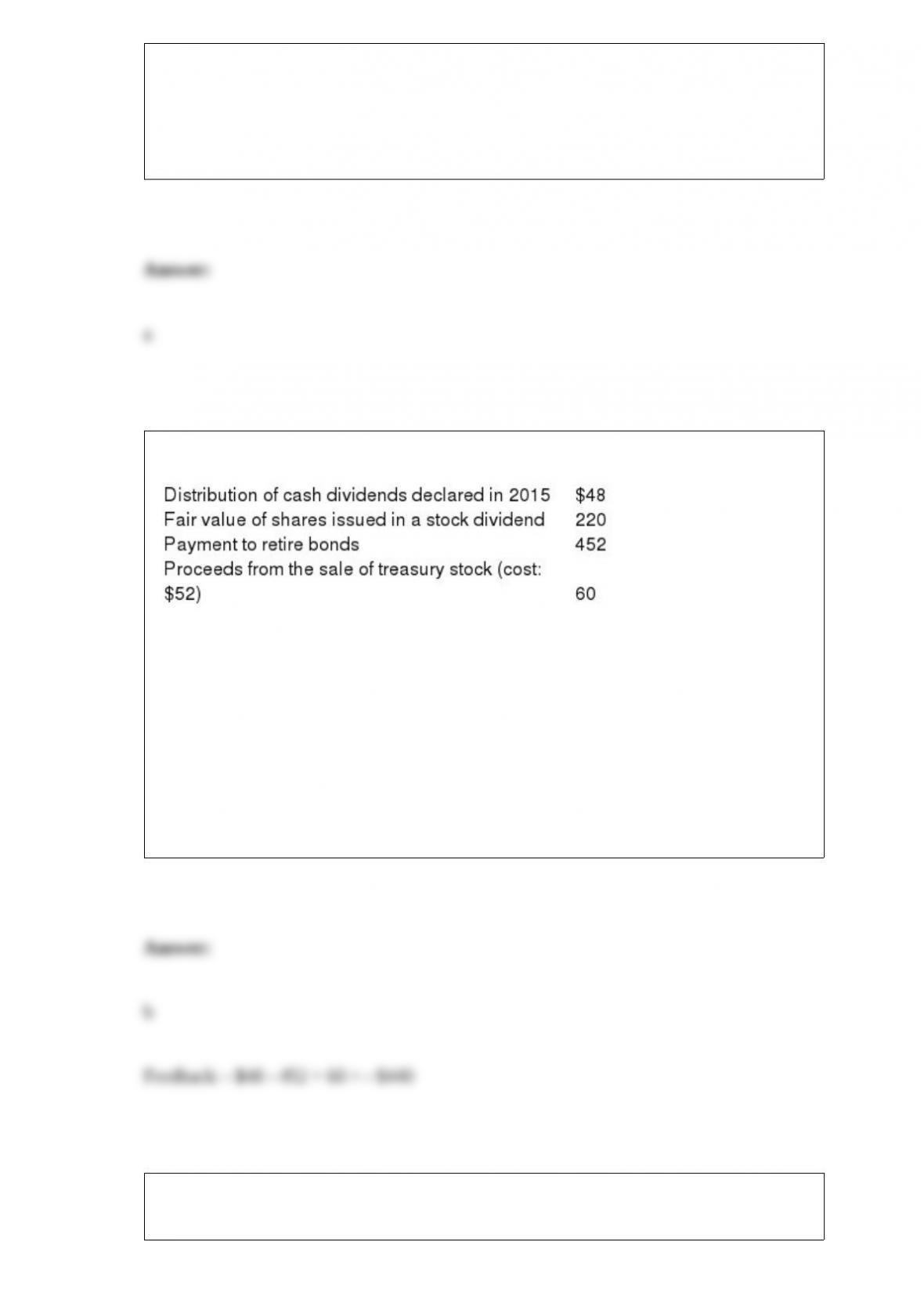

During 2016, T Company engaged in the following activities:

In T’s statement of cash flows, what were net cash outflows from financing activities for

2016?

a. $392.

b. $440.

c. $560.

d. $732.

XYZ Corporation receives $100,000 from investors for issuing them shares of its stock.

XYZ’s journal entry to record this transaction would include a:

a. Debit to investments.

b. Credit to retained earnings.

c. Credit to capital stock.

d. Credit to revenue.

GAAP regarding accounting for unrealized gains and losses on investments in equity

securities will apply to an investment when the percentage of ownership of another

company is:

a. Less than 20%.

b. 20% to 50%.

c. Over 50%.

d. Exactly 100%.

Which of the following is not a performance obligation?

a. A good that the seller could sell separately and that is separately identifiable from

other goods and services in the contract.

b. A right of return.

c. An option for a customer to purchase goods under terms that are more advantageous

than those enjoyed by other customers.

d. An extended warranty.

In deciding whether financing with receivables is a secured borrowing or a sale under

IFRS, the critical element is the extent to which:

a. The transferee has received substantially all the risks and rewards of ownership.

b. The age of the receivables transferred differs from the average age of the receivables.

c. The transferor of the receivable surrenders control over the assets transferred.

d. The transferee relies on funds from the transferor to maintain operations.

What would be the total interest expense recognized for the bond issue over its full

term?

a. $ 6,512,253.

b. $ 8,000,000.

c. $ 9,487,747.

d. $11,487,747.

If the fair value of a debt investment that is classified as an available-for-sale

investment declines for a reason that is viewed as “other than temporary” because the

company has incurred a credit loss on the investment:

a. The investment is written down to fair value, and only the noncredit-loss component

of the impairment loss is recognized in net income.

b. The investment is written down to fair value, and the entire impairment loss is

recognized in net income.

c. The investment is written down to fair value, and only the credit-loss component of

the impairment loss is recognized in net income.

d. The investment is written down to fair value, but none of the impairment loss is

recognized in net income.

Assuming the magnitude of the change is $7 million. Prepare the appropriate journal

entry to record any 2016 gain or loss. (Ignore income taxes.) If Open Arms prepares its

financial statements according to U.S. GAAP, how will the company report the gain or

loss?

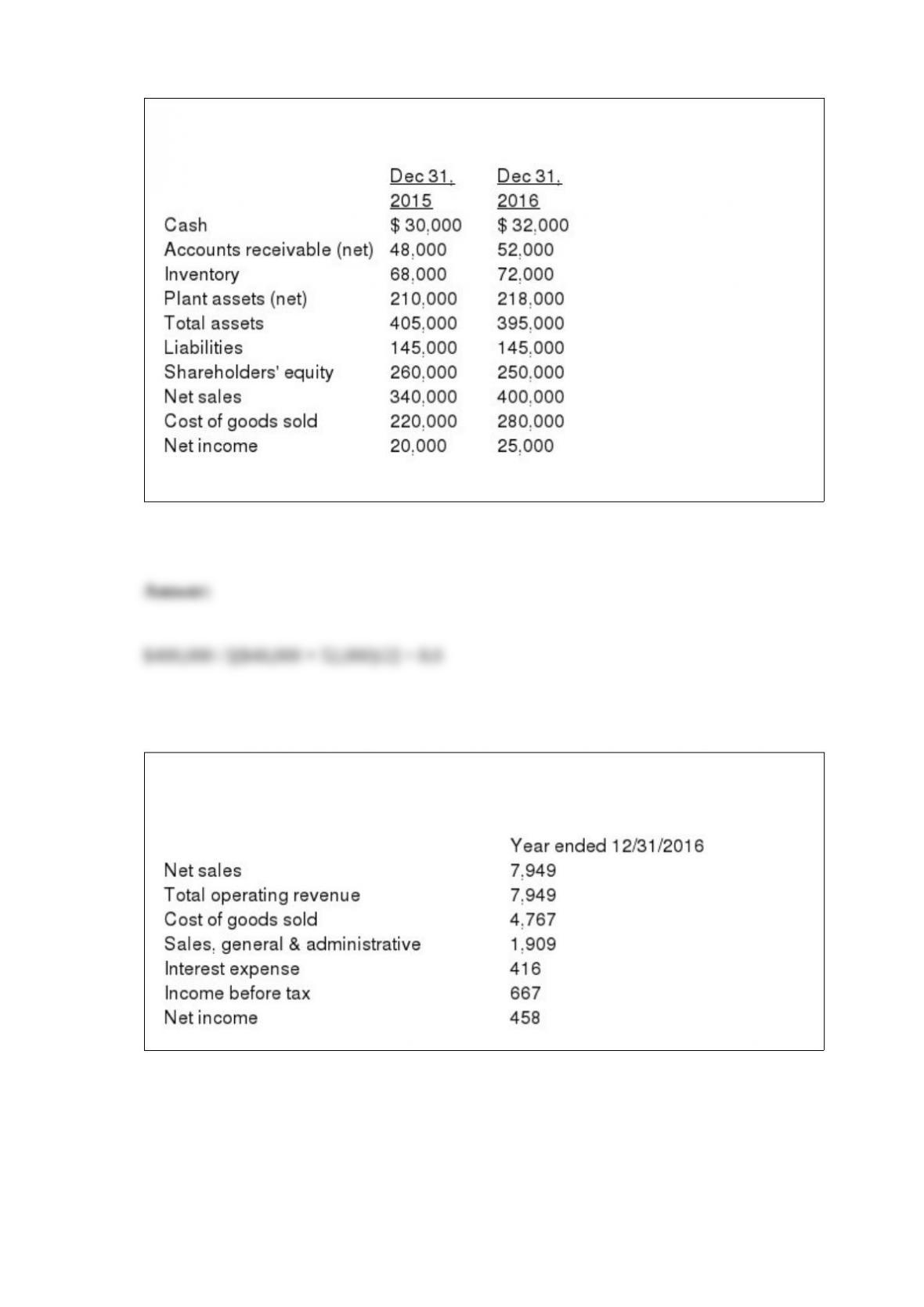

Missoula Inc. reported the following selected financial statement data:

Required: Compute the receivables turnover ratio for 2016.

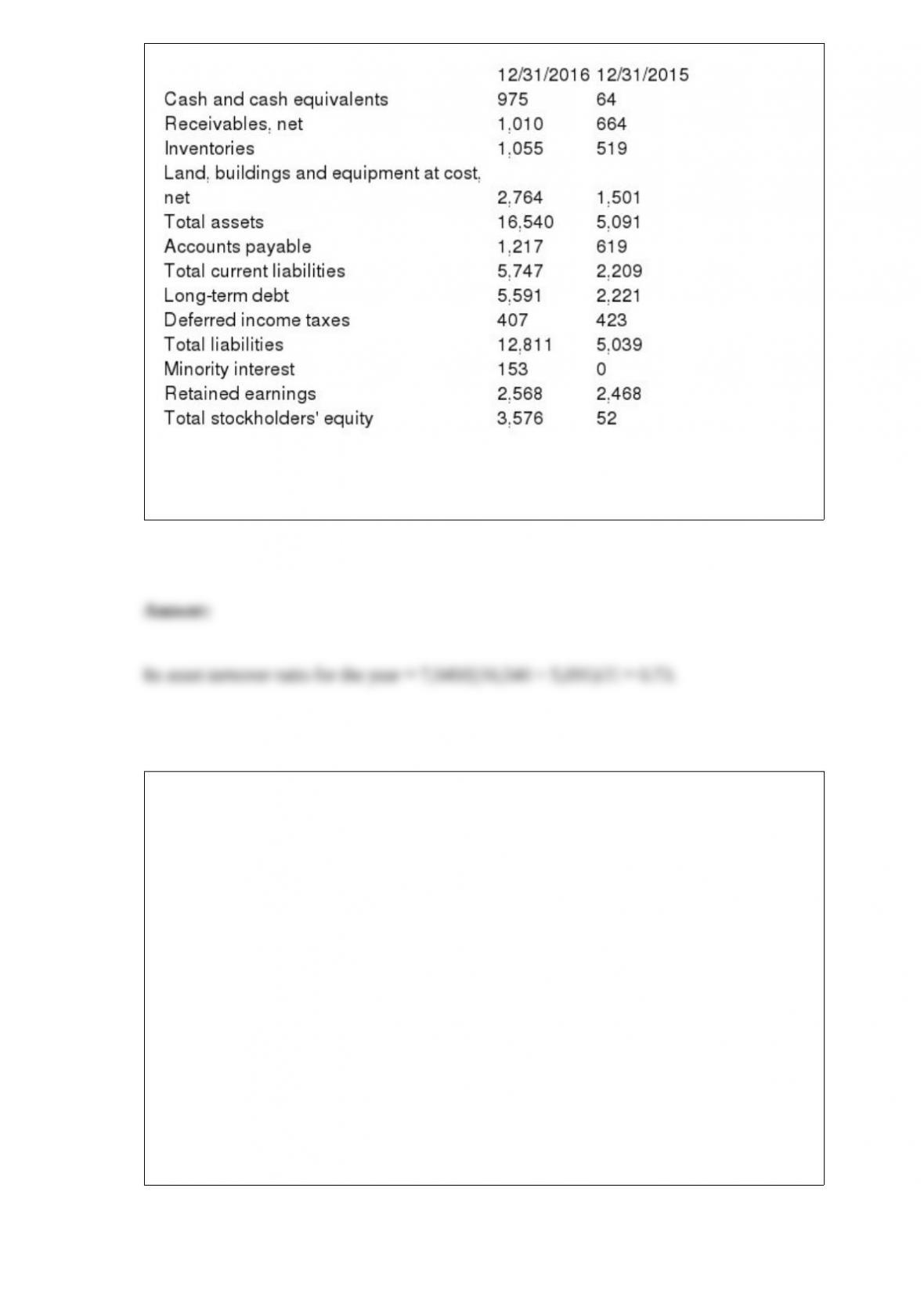

The following partial income statement and balance sheet information (in $ millions)

comes from the Annual Report of Saratoga Springs Co. for the year ending 12/31/2016:

Required: Compute the following amounts for Saratoga Springs Co.

Its asset turnover ratio for 2016. Round your answer to two decimal places.

On January 1, 2016, BBX issued $400,000 of its 8% bonds for $368,000. The bonds

were priced to yield 10%. Interest is payable semiannually on June 30 and December

31. BBX records interest at the effective rate and elected the option to report these

bonds at their fair value. On December 31, 2016, the fair value of the bonds was

$370,000 as determined by their market value on the NYSE. $1,000 of the change in

fair value was due to a change in the general (risk-free) rate of interest.

Required:

1> Prepare the journal entry to record interest on June 30, 2016 (the first interest

payment).

2> Prepare the journal entry to record interest on December 31, 2016 (the second

interest payment).

3> Prepare the journal entry to adjust the bonds to their fair value for presentation in the

December 31, 2016, balance sheet.

Explain the differences between how a principal and agent would show a sale of a

product that has gross revenues of $1,000, cost of goods sold of $750, and a

commission paid by the principle of 10% of gross sales on their respective income

statements.