Which of the following has the least impact upon the integrity of financial statements

issued by publicly owned corporations?

A. Federal securities laws.

B. Professional judgment of the accountants who prepare the financial statements.

C. Audits of the financial statements by the Internal Revenue Service.

D. Competence and integrity of the CPAs who perform audits.

The comparative balance sheets of Apollo Rocket, Inc. show a net increase in inventory

of $79,000 and a net decrease in accounts payable of $42,000 during 2015. In

computing net cash flow from operating activities under the indirect method, net

income for 2015 should be:

A. Increased by $37,000.

B. Reduced by $37,000.

C. Increased by $121,000.

D. Reduced by $121,000.

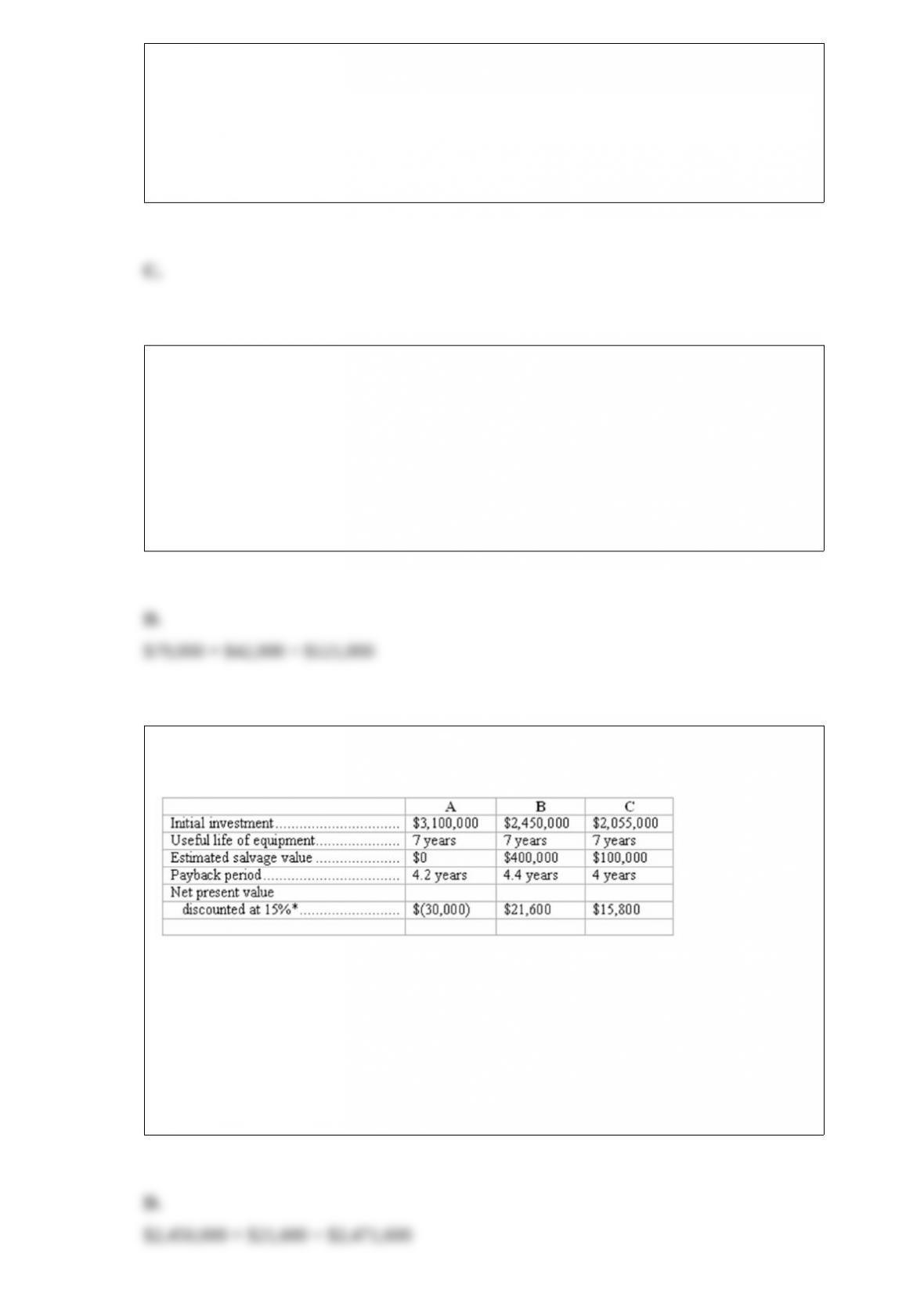

The management of Ortega Manufacturing has three different proposals under

consideration. The Accounting Department has prepared the following information:

*Management’s required rate of return is 15%.

Refer to the information above. The above data indicate that:

A. After considering the timing of future cash flows, each of the three proposals is

expected to provide a rate of return in excess of 15%.

B. Proposal A will generate net losses annually.

C. If the salvage value of proposal A were $52,000 instead of zero, proposal A would

have the highest net present value.

D. The present value of proposal B’s future cash flows is $2,471,600.

Cost-volume-profit relationships

Spotless, Inc., sells only one product. The sales price per unit is $50, with variable cost

per unit of $40. Fixed costs are $60,000 per month. Maximum capacity is 34,000 units

per month. Answer the following questions:

(a) To break-even, how many units must Spotless, sell per month? _______________

units

(b) If Spotless, Inc., sold 25,000 units, what would be its operating income for the

month? $________________

(c) At present capacity, what is the maximum operating income Spotless, can expect to

earn per month? $________________

(d) Assuming that direct labor cost can be reduced by $2 per unit, what would the

maximum operating income be per month? $_______________

Which of the following activities is not a category into which cash flows are classified?

A. Marketing activities.

B. Operating activities.

C. Financing activities.

D. Investing activities.

Refer to the information above. At the beginning of October, owners’ equity in Waldorf

was $480,000. Given the transactions of October, 2014, what will be the owners’ equity

at the end of the month?

A. $480,000.

B. $484,000.

C. $502,500.

D. $580,500.

If the end of the fiscal year is not a payroll date, the Direct Labor account normally has:

A. A debit balance, representing prepaid labor costs.

B. A credit balance, representing accrued wages payable.

C. Either a debit or a credit balance, depending upon whether the end of the fiscal year

falls before or after the end of the pay period.

D. A zero balance, because the Direct Labor account is closed along with the other

expense accounts.

Which of the following has no effect on the computation of earnings per share for the

current period?

A. The amount of cash dividends declared or paid to preferred stockholders.

B. The amount of cash dividends declared or paid to common stockholders.

C. Net income.

D. The number of shares of common stock issued.

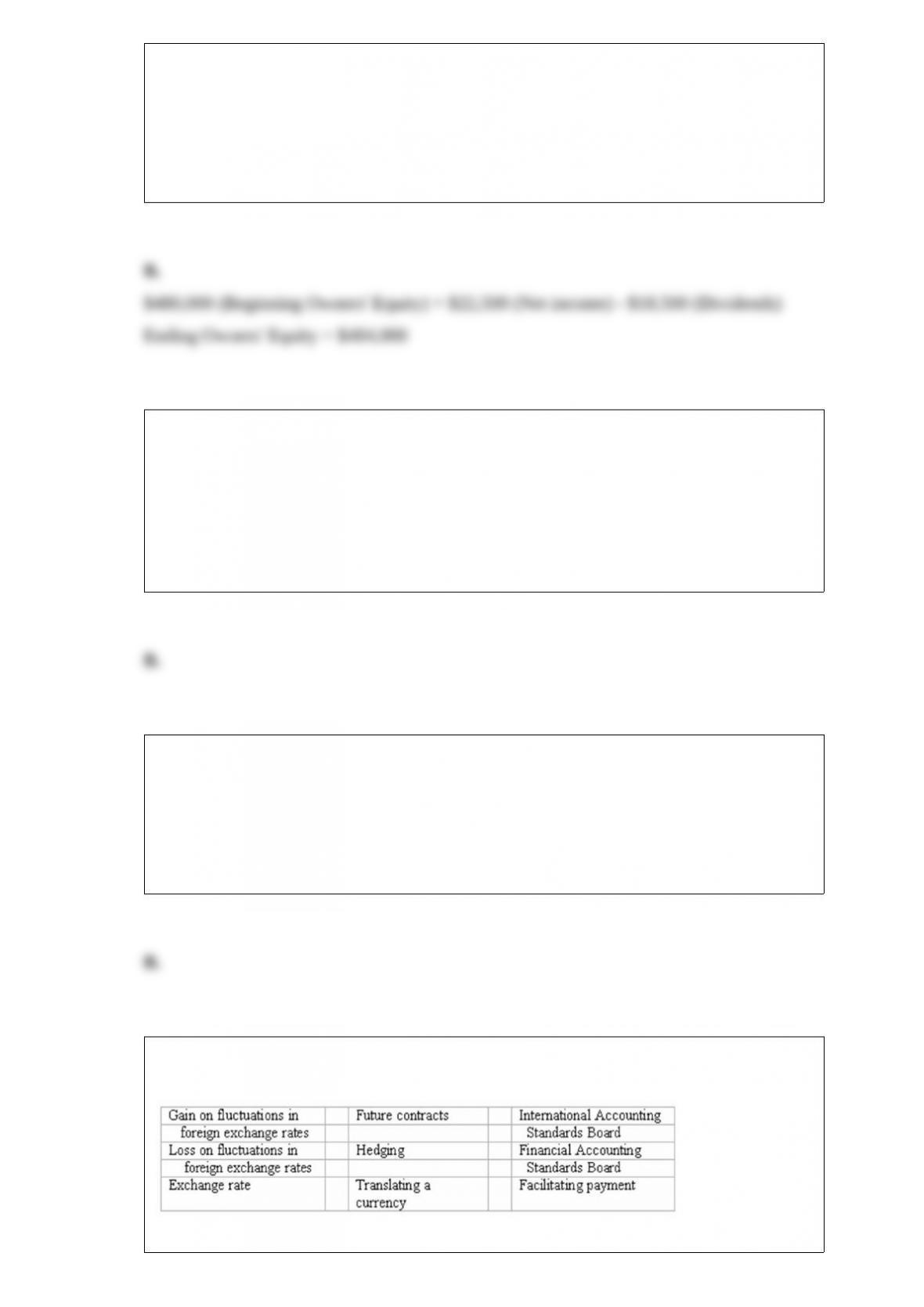

Accounting terminology

Listed below are nine technical accounting terms introduced in this chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided below each statement, indicate the accounting term

described, or answer “None” if the statement does not correctly describe any of the

terms.

_____ (a) The strategy of creating offsetting positions so that losses from currency

fluctuations will be offset by gains resulting from the same fluctuations.

_____ (b) The price of foreign currency, stated in terms of the domestic currency.

_____ (c) An item likely to appear in the income statements of American-based

importers when foreign exchange rates are rising.

_____ (d) The organization responsible for developing uniform worldwide accounting

standards.

_____ (e) Payments made to foreign officials to expedite paperwork.

_____ (f) The process of restating an amount of foreign currency in terms of the

equivalent number of U.S. dollars.

_____ (g) An item likely to appear in the income statements of American-based

exporters when foreign exchange rates are falling.

Assets contributed to a partnership by a partner would be recorded at:

A. Historical cost.

B. Fair market value.

C. Cost less depreciation.

D. Potential value.

The accounting standards and concepts used in the preparation of financial statements

are called:

A. Certified principles of accounting (CPA).

B. Generally accepted accounting principles (GAAP).

C. Federal accounting standards and bylaws (FASB).

D. Standards enforcing consistency (SEC).

Which of the following is not true about post-retirement benefits?

A. Post-retirement costs should be recognized as expense as the workers earn the right

to receive the benefits.

B. Most corporations have fully funded their post-retirement benefits.

C. Unfunded post-retirement costs are a non-cash expense.

D. A corporation’s liability for post-retirement benefits is equal to the present value of

estimated future payments.

Patterson’s Department Store prepares monthly income statements by sales

departments. These income statements are organized to show contribution margin,

performance margin, and responsibility margin for each sales department, as well as

operating income for the store as a whole.

Refer to the information above. Depreciation of the fixtures and equipment used

exclusively in a particular sales department should be classified as a:

A. Common fixed cost.

B. Variable cost.

C. Controllable fixed cost.

D. Committed fixed cost.

Which of the following accounting system characteristics cannot generate motivation?

A. Creating and setting goals.

B. Measuring progress towards those goals.

C. Allocating rewards towards goal achievement.

D. Balancing debits and credits.

Residual income can be defined as:

A. Income remaining after dividends are paid out.

B. Operating earnings minus return on investment.

C. Operating earnings plus a minimum acceptable return times average invested capital.

D. Operating earnings minus a minimum acceptable return times average invested

capital.

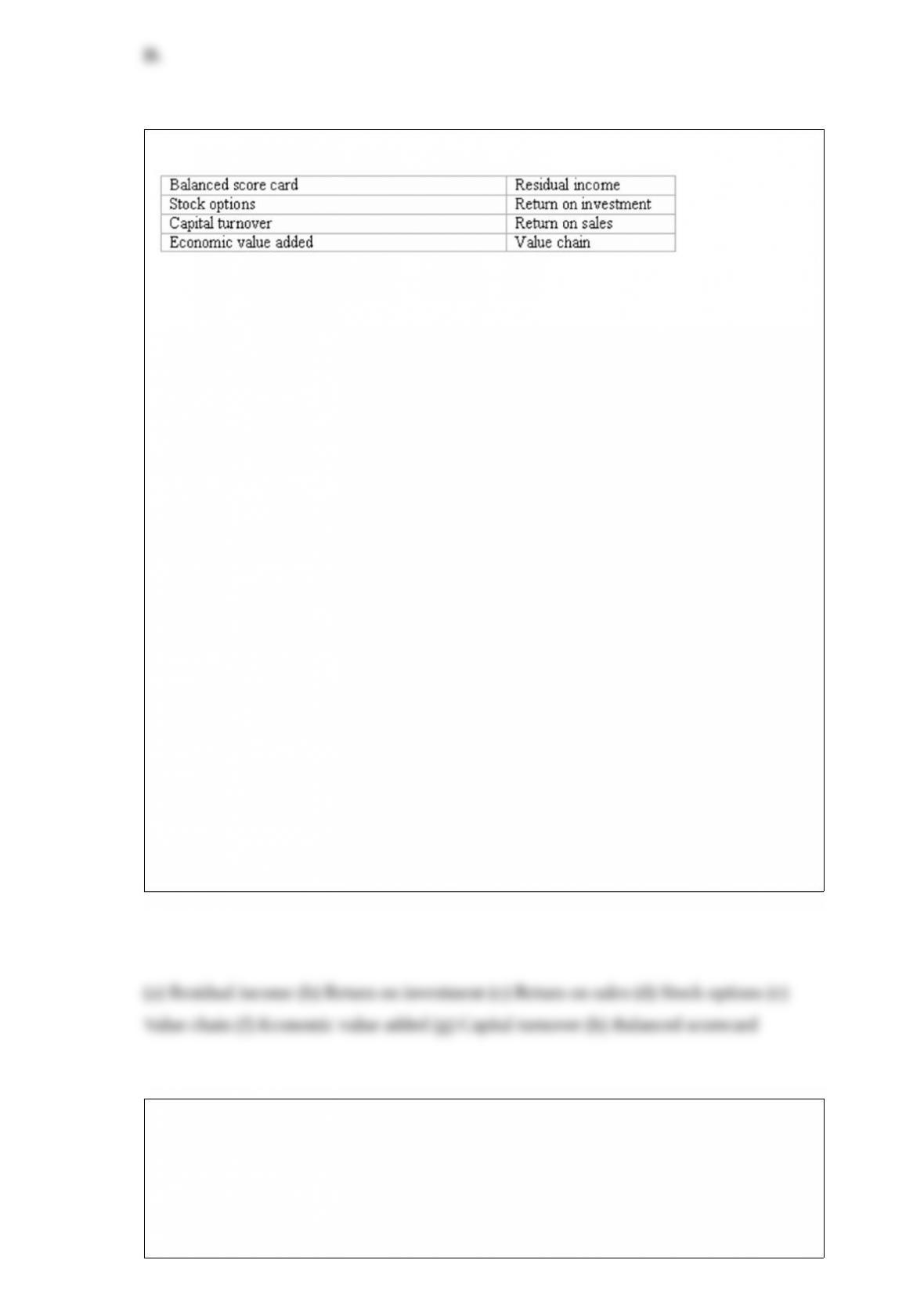

Listed below are eight accounting terms introduced or emphasized in this chapter:

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided, indicate the accounting term described, or answer “none”

if the statement does not correctly describe any of the terms.

(a) _______ is the amount by which operating earnings exceeds a minimum acceptable

return on the average invested capital. The minimum rate of return represents the

opportunity cost of using the invested capital.

(b) ______ is the operating income divided by the average invested capital associated

with the generation of that income.

(c) _______ is computed by dividing the operating income by the total sales for a

particular business segment or product line. It tells managers the amount of earnings

generated from a dollar of sales.

(d) _______ give an employee the right to purchase a pre-specified number of shares at

a pre-specified price within a certain future time period. They provide incentives for

managers to increase stock prices.

(e) _______ is the set of activities necessary to create and distribute a desirable product

or service to a customer.

(f) _______ is a specific type of residual income. It is computed by multiplying

weighted average cost of capital by total assets minus current liabilities, and subtracting

that product from the after-tax operating income.

(g) _______ is a measure created by dividing sales by the average invested capital to

generate those sales. It tells managers the amount of sales generated by a dollar of

invested capital.

(h) _______ is a system for performance measurement that links a company’s strategy

to specific goals, assesses progress towards those goals, and measures specific

initiatives to achieve those goals. It is a systematic attempt to create a business

performance measurement process that integrates objectives across four business lenses

to achieve the organization’s strategic goals.

Which of the following is not a generally accepted accounting principle relating to the

valuation of assets?

A. The cost principle – in general, assets are valued at cost, rather than at estimated

market values.

B. The objectivity principle – accountants prefer to use objective, rather than subjective,

information as the basis for accounting information.

C. The safety principle – assets are valued at no more than the value for which they are

insured.

D. The going-concern assumption – one reason for valuing assets such as buildings and

equipment at cost rather than at their current market values is the assumption that the

business will use these assets rather than sell them.

Gross profit rate is equal to:

A. Net sales divided by gross profit.

B. Gross sales divided by gross profit.

C. Gross profit divided by net sales.

D. Gross profit divided by gross sales.

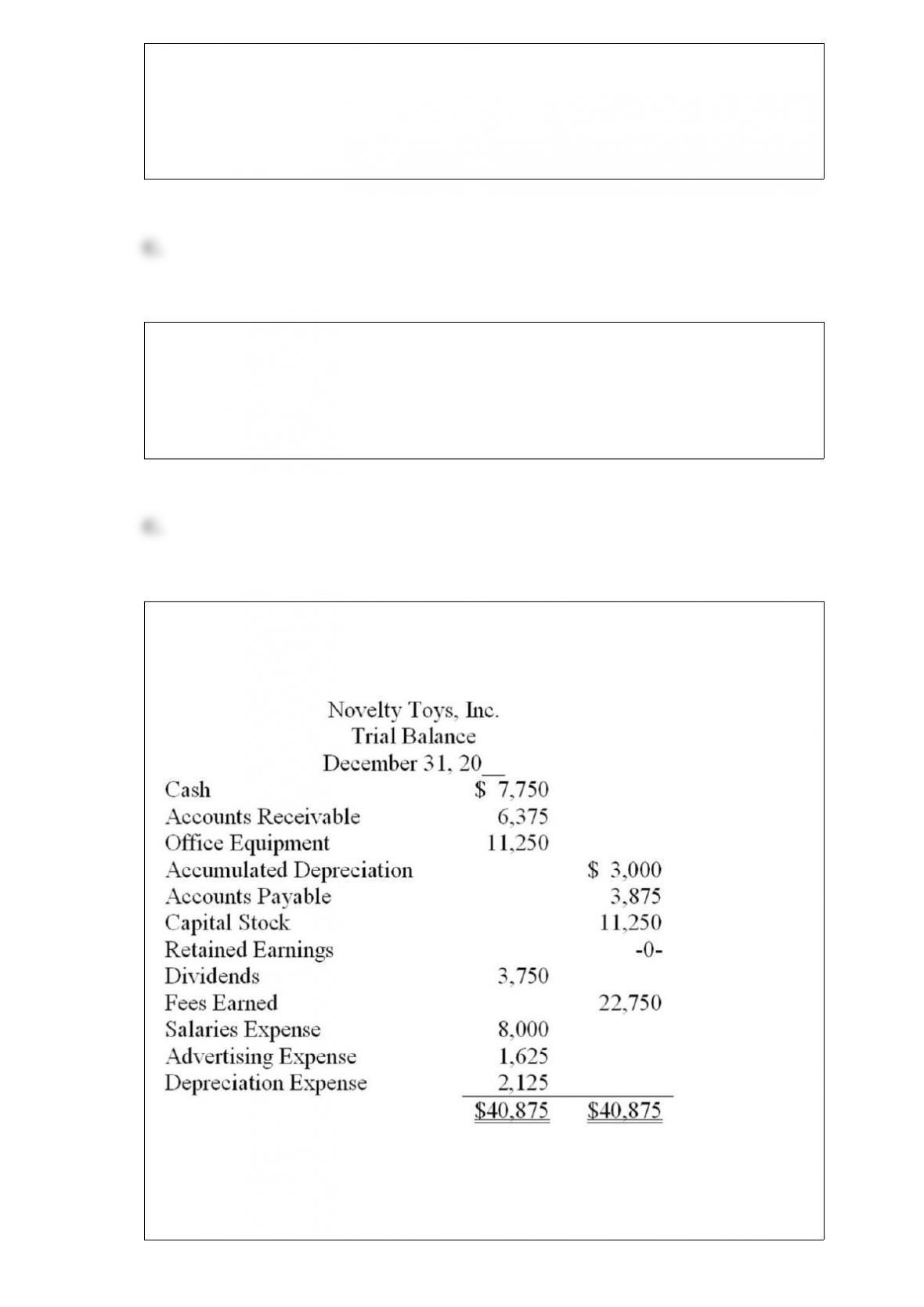

Shown below is a trial balance for Novelty Toys Inc., on December 31, after adjusting

entries:

Refer to the information above. Net income for the period equals:

A. $18,375.

B. $11,000.

C. $5,800.

D. $11,250.

Harris Corporation’s inventory of a particular product includes 200 units purchased at a

per-unit cost of $50, and another 100 units purchased at a unit cost of $60. If Harris

sells 10 units of this product, the cost of goods sold will be:

A. $500.

B. $550.

C. $660.

D. The answer will depend upon the inventory cost flow assumption in use.

Soriano Company had net sales of $300,000 for the month (after returns and allowances

of $1,500 and sales discounts of $3,250). Beginning inventory for the month was

$60,000; purchases for the month were $175,000; and gross profit was 43%.

Refer to the information above. What was the ending inventory for the month?

A. $60,000.

B. $64,000.

C. $129,000.

D. $175,000.

The principal difference between managerial accounting and financial accounting is that

managerial accounting information is:

A. Prepared by managers.

B. Intended primarily for use by decision makers inside the business organization.

C. Prepared in accordance with a set of accounting principles developed by the Institute

of Certified Managerial Accountants.

D. Oriented toward measuring solvency rather than profitability.

Refer to the information above. Supreme’s price-earnings ratio at year end was:

A. 25.

B. 22.

C. 100.

D. 4.

Refer to the information above. By how much would Terme’s annual gross profit

increase if the investment is undertaken?

A. $750,000.

B. $84,375.

C. $187,500.

D. $103,125.

Barter Corp. sold American telecommunications equipment to a British company for

650,000 pounds. On the sale date, the exchange rate was $1.65 per British pound, but

when Barter received payment from its customer, the exchange rate was $1.60 per

pound. When the foreign receivable was collected, Barter Enterprises:

A. Credited Sales for $32,500.

B. Debited Cash for $1,040,000.

C. Credited Gain on Fluctuation of Foreign Currency for $32,500.

D. Debited Loss on Fluctuation of Foreign Currency for $32,500.

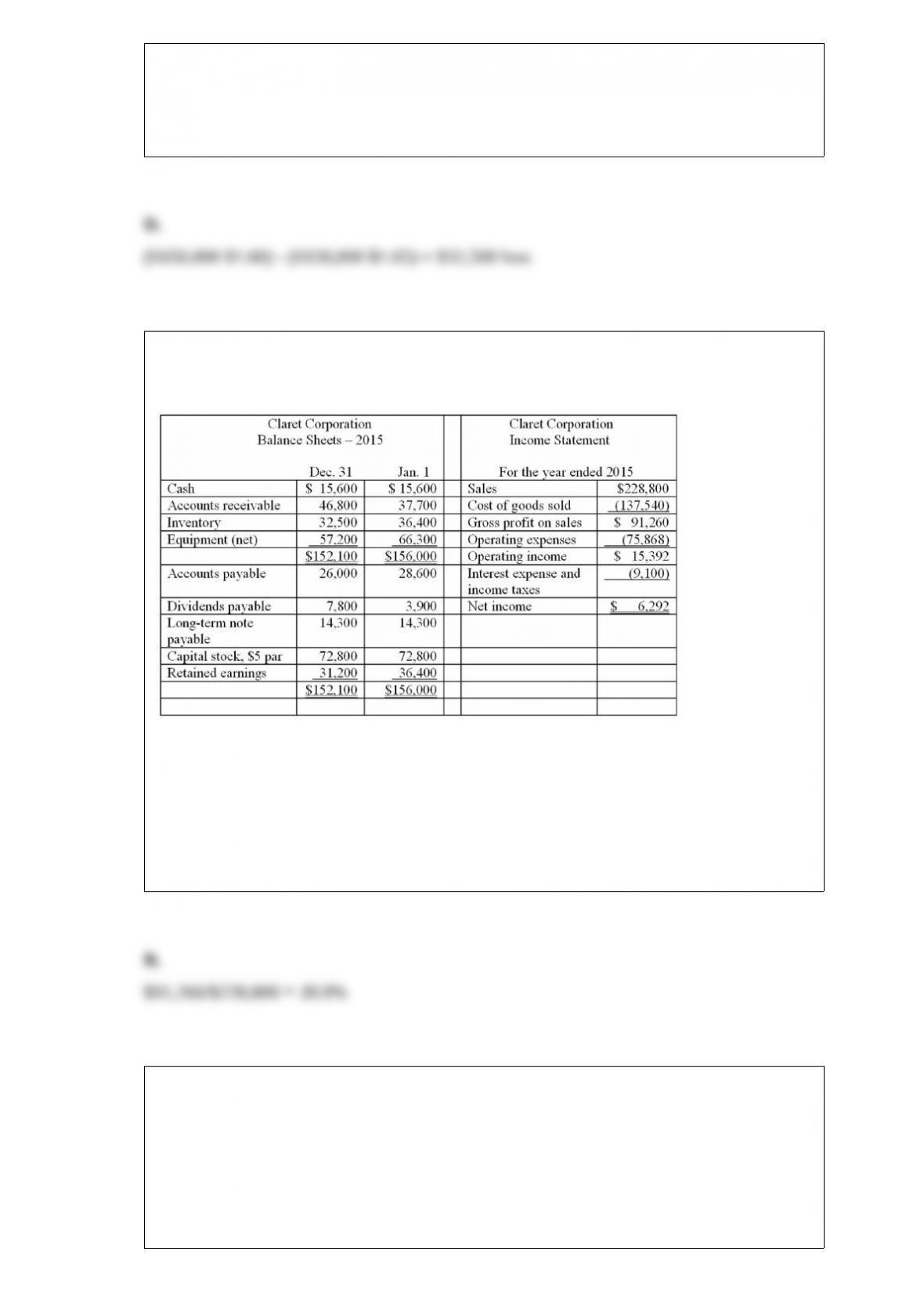

Given below are comparative balance sheets and an income statement for Claret

Corporation.

All sales were made on account. Cash dividends declared during the year totaled

$11,492.

Refer to the information above. Claret Corporation’s gross profit rate for 2015 is:

A. 60.1%.

B. 39.9%.

C. 33%.

D. 68%.

Samson Corporation buys a foreign currency future contract as a hedging strategy to

protect against possible losses from fluctuations in a particular foreign exchange. This

strategy suggests that Samson Corporation has:

A. Foreign accounts payable and expects the exchange rate to fall.

B. Foreign accounts receivable and expects the exchange rate to rise.

C. Foreign accounts payable and expects the exchange rate to rise.

D. Foreign accounts receivable and expects the exchange rate to fall.

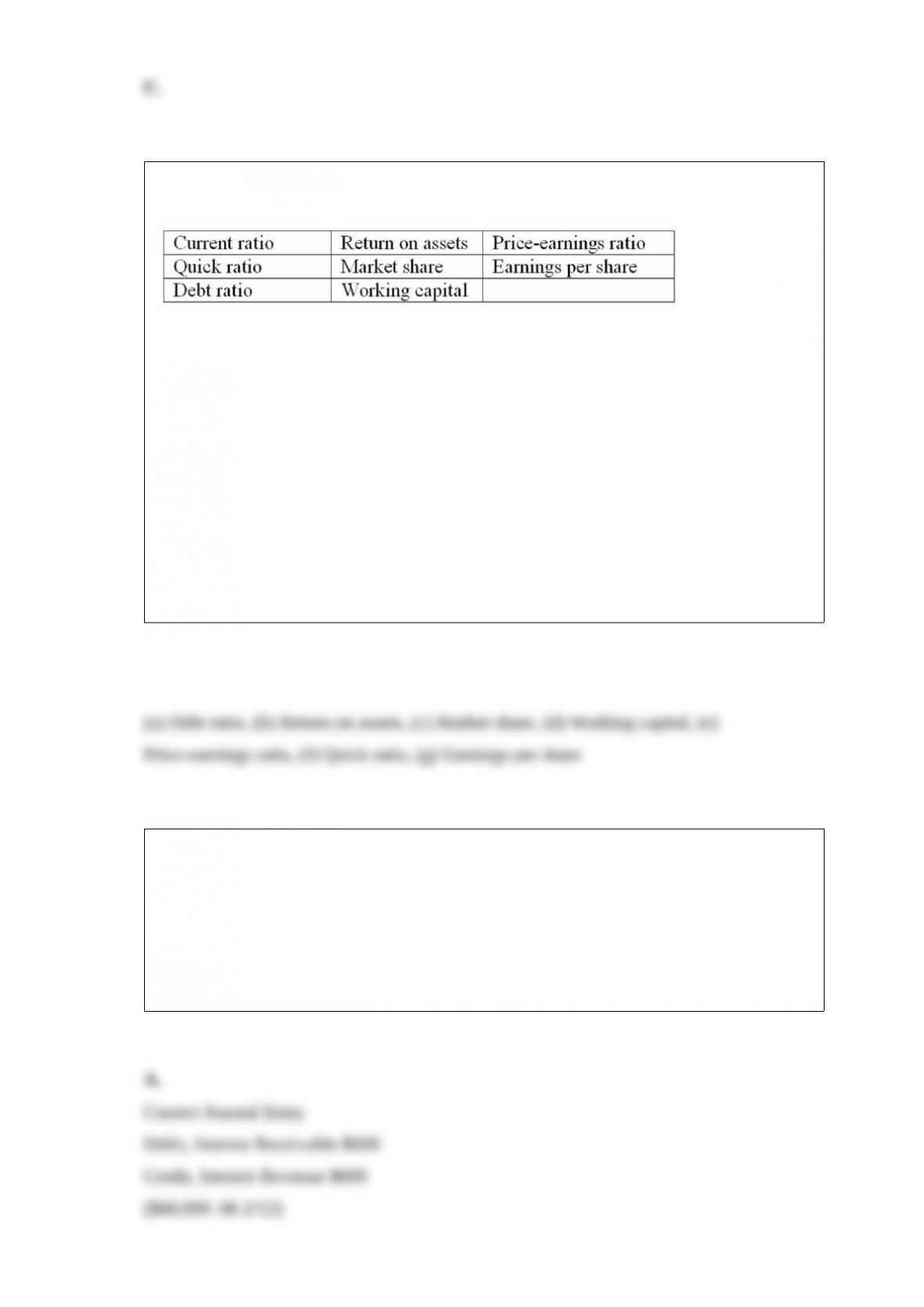

Accounting terminology

Listed below are eight technical accounting terms introduced in this chapter:

Each of the following statements may (or may not) describe one of these technical

terms. For each statement, indicate the term described, or answer “None” if the

statement does not correctly describe any of the terms.

____ (a) The percentage of total assets financed by creditors.

____ (b) A measure of the effectiveness with which management utilizes a company’s

resources, regardless of how those resources are financed.

____ (c) A company’s percentage share of total dollar sales within its industry.

____ (d) Current assets less current liabilities.

____ (e) A measure reflecting investors’ expectations of future profitability.

____ (f) A measure of short-term solvency often used when a company has large

inventories that cannot be quickly converted into cash.

____ (g) A ratio that helps individual stockholders relate the net income of a large

corporation to their equity investment.

On November 1, Willis Corporation sold merchandise in return for a 6%, three-month

note receivable in the amount of $60,000. The proper adjusting entry at December 31

(end of Willis’s fiscal year) includes a:

A. Credit to Interest Revenue of $600.

B. Debit to Cash of $600.

C. Debit to Interest Receivable of $300.

D. Credit to Notes Receivable of $900.

Development of generally accepted accounting principles

(A.) What is meant by the phrase “generally accepted accounting principles”?

(B.) Explain the concept of the business entity and how it relates to generally accepted

accounting principles.

The statement “This business produced net income of $520,000” is unclear because it

failed to specify:

A. The accounting method, that is, accrual or cash basis.

B. Whether the amount earned is before or after expenses.

C. The time period.

D. The amount of cash withdrawn from the business by the owner.

Publicly traded companies must file audited financial statements with the:

A. AICPA.

B. IRS.

C. SEC.

D. AAA.

A customer purchased merchandise for $400 which cost the seller $200. The customer

was dissatisfied with some of the goods and thus returned $100 worth and received a

cash refund.

(a) What journal entries should the seller make when the merchandise is sold and at the

time of the return? Assume that the seller uses a perpetual inventory system.

(b) If the seller uses a periodic inventory system, what entries would be made?

Family Fashions Corporation discontinued Kid-Choice, its entire line of children’s

clothing, in November of 2015. Prior to the disposal, Kid-Choice generated a loss of

$600,000 (net of tax) for the period from January through the sale date. Because of the

value of the real estate and machinery, there was a gain of $850,000 (net of tax) on the

actual sale. How should this situation be reported in the financial statements of Family

Fashions for 2015?

A. A $250,000 gain should be included in the 2015 income statement as an

extraordinary item.

B. A $600,000 loss should be included in income from operations and a $850,000 gain

should be reported in the “discontinued operations” section of the income statement.

C. A $250,000 adjustment to beginning retained earnings should be in the statement of

retained earnings.

D. A $250,000 gain should be in the “discontinued operations” section of the income

statement.

A worksheet should be viewed as:

A. A financial statement to be distributed to investors.

B. A financial statement to assist managers in making managerial decisions.

C. A tool to assist accountants in making end-of-period adjustments and in preparing

financial statements.

D. A tool to assist auditors in determining that all transactions have been properly

recorded throughout the period.