The days’ sales uncollected ratio measures the liquidity of receivables.

All items of plant and equipment, including land, eventually wear out or lose their

usefulness.

In preparing financial statements from the trial balance, the balance sheet is prepared

first.

Before adjusting for accrued revenues, both assets and equity are understated.

The statement of cash flows measures the net effect of revenues and expenses for a

specified period.

TechCom had net sales of $480,000 and average accounts receivable of $64,000. Its

accounts receivable turnover was 7.5.

Receivables can be converted to cash by either selling them or using them as security

for a loan.

Sellers offer a purchase discount to buyers for prompt payment for purchases on

account.

Verifiability ensures that information is complete, neutral and free from error.

Merchandising sales and costs reported on the income statement usually differ from

cash receipts and payments for the period.

The decline in merchandise inventory from cost to NRV is recorded in an adjusting

entry at the end of the period.

The days’ sales in inventory ratio is calculated by dividing ending inventory by cost of

goods sold and multiplying the result by 365.

The amount of the month-end adjusting entry for Insurance Expense is $1,000. If the

entry is not made then expenses are understated by $1,000 and net income is overstated

by $1,000.

The cost of an inventory item includes its invoice price plus any added or incidental

costs necessary to put it in a place and condition for sale.

Equity is increased when cash is received from customers in payment of a previously

recorded accounts receivable.

The accounts receivable approach uses income statement relationships to estimate bad

debts.

A loss arises when revenues are higher than expenses.

If all columns balance upon completion of a work sheet, you can be sure that no errors

were made in preparing the work sheet.

Credits to accounts are always increases.

A characteristic of assets is their ability to provide current benefits to the business.

EFT is the use of electronic communication to transfer cash from one party to another.

A credit to Income Summary of $231,000 and a debit to Income Summary of $216,250

results in profit of $14,750 transferred to Owner’s Capital.

A characteristic of liabilities is their capacity to reduce future assets.

When a business sends a bill for $200 to a customer for services rendered, the journal

entry to record this transaction will include a $200 credit to Accounts Receivable.

The retail amount of inventory refers to its dollar amount measured using selling prices

of inventory items.

When a single goods and services tax (GST) or Harmonized Sales Tax (HST) account is

used, a credit balance in the account means that the government owes money to the

business.

Financial statements prepared from a work sheet offer more information than if it is not

used and statements are just prepared from an adjusted trial balance.

Withdrawals are a type of transaction that affects equity.

Banks normally use a flat rate fee for the processing of debit card transactions and a

percentage fee for the processing of credit card transactions.

The current ratio is calculated by dividing current liabilities by current assets.

The amount of gross profit for a merchandising business will be the same under both

the accrual basis and the cash basis of accounting.

To credit an expense account means to decrease it.

The two main accounting principles used in the adjusting process are matching and full

disclosure.

The consistency principle allows companies to use different inventory valuation

methods period to period as long as the changes are fully disclosed.

The Accounting Standards Board (AcSB), is the body that developed accounting

standards for private enterprises (ASPE).

A business that has inventory items that are ordinarily interchangeable is required to use

the specific identification method of assigning costs to inventory.

Under the perpetual system cash sales are recorded at the point of sale.

The adjusted trial balance must be prepared before the adjusting entries are made.

A merchandiser earns net income by buying and selling merchandise.

The allowance method complies with the generally accepted accounting principle of

matching.

The accounting principle that requires financial statements to reflect the assumption that

the business will continue operating instead of being closed or sold, unless evidence

shows that it will not continue, is the:

A. Cost principle.

B. Business entity principle.

C. Going concern principle.

D. Monetary unit principle.

E. Revenue recognition principle.

Prepaid expenses, depreciation, accrued expenses, unearned revenues, and accrued

revenues are all examples of:

A. Items that require contra accounts.

B. Items that require adjusting entries.

C. Classified balance sheet accounts.

D. Assets.

E. Income statement accounts.

Which of the following items does not appear on the balance sheet?

A. Cash.

B. Notes payable.

C. Accounts receivable.

D. Withdrawals.

E. Accounts payable.

During a period of steadily falling prices, which inventory cost flow assumption results

in reporting the lowest net income?

A. Specific identification.

B. Average cost.

C. Weighted-average.

D. FIFO.

E. Retail method.

Classified balance sheets commonly include the following categories.

(a) Current assets

(b) Investments

(c) Property, plant and equipment

(d) Intangible assets

(e) Current liabilities

(f) Long-term liabilities

(g) Equity

Indicate the typical classification of each item listed below by placing the letter of the

correct balance sheet category in the blank space next to the item.

(1) ______ Margarita Acosta, capital

(2) ______ Cash

(3) ______ Office supplies

(4) ______ Accounts receivable

(5) ______ Prepaid expenses

(6) ______ Merchandise inventory

(7) ______ Buildings used in business operations

(8) ______ Wages payable

(9) ______ Long-term note payable

(10) ______ Accounts payable

(11) ______ Patents

(12) ______ Land held for future plant expansion

A partnership:

A. Is also called a sole proprietorship.

B. Has unlimited liability.

C. Has to have a written agreement in order to be legal.

D. Is a legal organization separate from its owners.

E. Is a non-business organization.

Coronado Company sells two types of inventory, MP3 players and Blu Ray players.

The MP3 players originally cost $2,250 and have a net realizable value $1,075 while

the Blu Ray players had an original cost of $500 and have a net realizable value of

$700. Calculate the year end adjustment to inventory when applying the lower of cost

and net realizable value on an item by item basis.

A. $375.

B. $1,175.

C. $1,112.

D. $1,575.

E. $2,950.

The adjusted trial balance contains information pertaining to:

A. Asset accounts only.

B. Balance sheet accounts only.

C. Income statement accounts only.

D. All general ledger accounts.

E. Revenue accounts only.

The internal functions of a business include:

A. Research and development.

B. Purchasing.

C. Marketing.

D. Servicing.

E. All of these answers are correct.

A subsidiary ledger that contains a separate account for each party that grants credit on

account to the business is called a(n):

A. Controlling account.

B. Accounts Receivable Ledger.

C. Accounts Payable Ledger.

D. Merchandise Inventory Ledger.

E. Accounts Payable.

Double-entry accounting is:

A. An accounting system that disregards the accounting equation, A = L + E.

B. An accounting system that records the effects of transactions and other events in at

least two accounts with equal debits and credits.

C. An accounting system in which each transaction affects and is recorded in two or

more accounts with unequal debits and equal credits.

D. An accounting system in which the sum of the debit account balances never equals

the sum of the credit account balances.

E. An accounting system in which errors never occur.

Days’ sales in inventory:

A. Is a ratio that estimates how many days it will take to convert inventory on hand to

accounts receivable or cash.

B. Is a ratio that tells us how much inventory a firm has on hand in terms of days’ sales.

C. Is the number of days we can sell from inventory if no new items are purchased.

D. All of these answers are correct.

E. Is a ratio that estimates how many days it will take to convert inventory on hand to

accounts receivable or cash and is a ratio that tells us how much inventory a firm has on

hand in terms of days’ sales.

Principles of internal control include:

A. Establish responsibilities.

B. Maintain adequate records.

C. Insure assets.

D. Bond key employees.

E. All of these answers are correct.

The Income Summary account is:

A. The account from which the amount of the net income or loss is transferred to the

owners’ capital accounts in a partnership.

B. A temporary account.

C. Used in the closing process to summarize the amounts of revenues and expenses.

D. Not a permanent account.

E. All of these answers are correct.

Economic events that affect an entity’s accounting equation, but that are not transactions

between the entity and outside parties are called:

A. Internal transactions.

B. Liabilities.

C. Source documents.

D. External transactions.

E. Prepaid expenses.

Which of the following is the final step in the accounting cycle?

A. Journalizing.

B. Preparing an adjusted trial balance.

C. Preparing a post-closing trial balance.

D. Preparing the statements.

E. Preparing a work sheet.

If the Debit and Credit column totals of a trial balance are equal, then:

A. All transactions have been recorded correctly.

B. All entries from the journal have been posted to the ledger correctly.

C. All ledger account balances are correct.

D. The total debit entries and total credit entries in the ledger are equal.

E. No sliding or transposition errors have been made.

A $130 credit to Office Equipment was credited to Sales by mistake. By what amounts

are the accounts under- or overstated as a result of this error?

A. Office Equipment, understated $130; Sales, overstated $130.

B. Office Equipment, understated $260; Sales, overstated $130.

C. Office Equipment, overstated $130; Sales, overstated $130.

D. Office Equipment, overstated $130; Sales, understated $130.

E. Office Equipment, overstated $260; Sales, understated $130.

The FastForward Company balance sheet shows cash $5,000, accounts receivable

$7,000, office equipment $3,000, and accounts payable $4,000. What is the amount of

equity?

A. $1,000.

B. $11,000.

C. $12,000.

D. $15,000.

E. $19,000.

An income statement on which the cost of goods sold and operating expenses are added

together and subtracted from net sales in one step to get net income is a(n):

A. Balanced income statement.

B. Single-step income statement.

C. Multiple-step income statement.

D. Merchandise income statement.

E. Unclassified income statement.

Accounts receivable turnover measures:

A. How long it takes to sell inventory on credit.

B. How often a company converts its average accounts receivable balance into cash

during the period.

C. Measures the relationship of cash sales to credit sales.

D. How long it takes to sell inventory on credit and how often a company converts its

average accounts receivable balance into cash during the period.

E. How often a company converts its average accounts receivable balance into cash

during the period and measures the relationship of cash sales to credit sales.

When a business has more than one credit customer, a separate account receivable for

each customer must be designed to show all of the following except:

A. How much each customer has paid.

B. How much each customer has purchased.

C. How much sales tax each customer has paid.

D. How much remains to be collected from each customer.

E. All of these should be included.

The value of assets exchanged for goods or services provided to customers as part of

the main operations of a business are called:

A. Assets.

B. Revenues.

C. Liabilities.

D. Equity.

E. Expenses.

In January, Denton Mabrey College received $120,000 in Unearned Tuition Revenue

from its students for the spring semester, which lasts four months. On January 31, the

college should recognize which amount for tuition revenue?

A. $30,000.

B. $60,000.

C. $80,000.

D. $90,000.

E. $120,000.

Which of the following statements is

TRUE about assets?

A. They are the properties or economic resources owned by the business.

B. They are available to provide future benefits to the business.

C. They can be intangible rights.

D. Ownership is shared between creditors and owners.

E. All of these answers are correct.

Because an inventory error causes an offsetting error in the next period:

A. Managers can ignore the error.

B. It is sometimes said to be self-correcting.

C. It affects only income statement accounts.

D. If affects only balance sheet accounts.

E. Managers can ignore the error and it is sometimes said to be self-correcting.

Match each of the following items with the appropriate internal control principle(s).

(a) Establish responsibility.

(b) Maintain adequate records.

(c) Insure assets and bond employees.

(d) Separate recordkeeping from custody of assets.

(e) Divide responsibility for related transactions.

(f) Apply technological controls.

(g) Perform regular and independent reviews.

_____ (1) The cashier does not have access to the cash register record tape and file.:

_____ (2) Z-Mart uses a voucher system.

_____ (3) Two clerks share the same cash drawer.

_____ (4) The bookkeeper prepares and signs cheques.

_____ (5) Z-Mart uses a computerized point of sale system.

_____ (6) Z-Mart hires Nelson and McGuire, CAs, to perform an audit.

_____ (7) Z-Mart buys an insurance policy to protect against employee theft.

_____ (8) Z-Mart has separate departments for purchasing, receiving, and accounts

payable.

_____ (9) Z-Mart has an internal auditor on staff.

_____ (10) Z-Mart uses a cheque protector.

A trial balance prepared after adjustments have been recorded is called a(n):

A. Balance sheet.

B. Adjusted trial balance.

C. Unadjusted trial balance.

D. Summary trial balance.

E. Income statement.

Z-Mart had sales of $498,100. Cost of goods sold was $143,400. What is the gross

profit?

A. $214,600.

B. $215,100.

C. $354,700.

D. $501,900.

E. 40%.

Source documents include all of the following except:

A. Sales invoices.

B. Financial statements.

C. Cheques.

D. Purchase orders.

E. Bank statements.

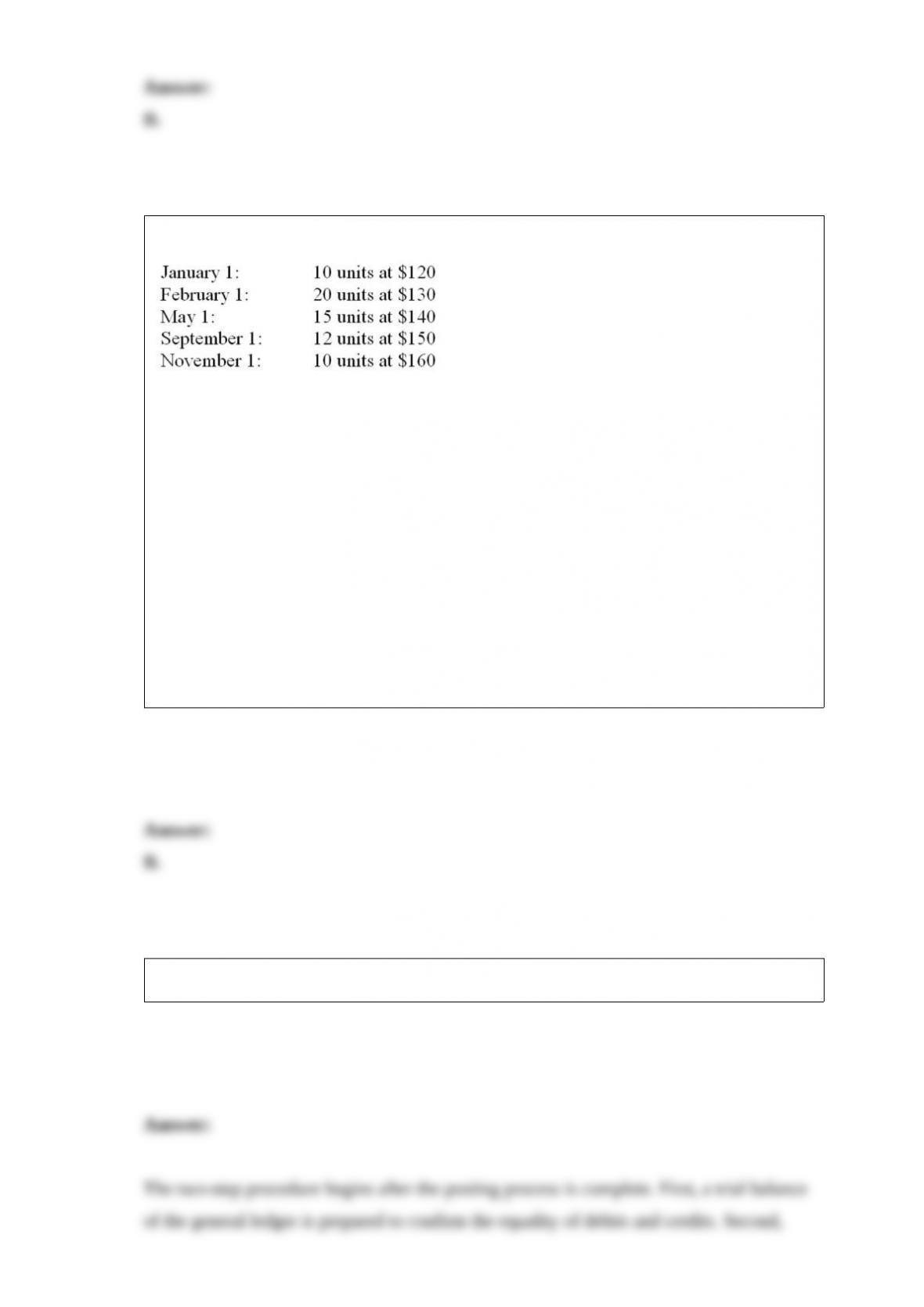

Trekking Company had the following purchases during the year:

On December 31, there were 26 units in ending inventory. These 26 units consisted of 2

from January, 4 from February, 6 from May, 4 from September, and 10 from November.

Using the specific identification method, what is the cost of the ending inventory?

A. $3,500.

B. $3,800.

C. $3,960.

D. $3,280.

E. $3,640.

Explain how the balances in the subsidiary accounts are tested for accuracy.

A(n) __________________ journal is used in recording and posting transactions of

similar type.

Why should assets be recorded at historical cost?

Discuss the purpose of an adjusted trial balance.

The cost of an asset less its accumulated depreciation is called the _____________.