If an available-for-sale investment is sold for which there are unrealized losses in

accumulated other comprehensive income (AOCI), the total effect on total

comprehensive income is:

a. An increase.

b. A decrease.

c. No effect.

d. Cannot be determined given this information.

According to International Financial Reporting Standards (IFRS), the impairment loss

for property, plant, and equipment is the difference between book value and:

a. The undiscounted sum of estimated future cash flows.

b. The present value of future cash flows.

c. Fair value less costs to sell.

d. The higher of the present value of estimated future cash flows and the fair value less

costs to sell.

When a company accrues federal income taxes at the end of the accounting period:

a. Its acid-test ratio increases.

b. Its current ratio increases.

c. Its debt to equity ratio decreases.

d. Its debt to equity ratio increases.

Which of the following is not a characteristic of a distinct good or service?

a. It can be used on its own or in combination with other goods or services the seller

could obtain elsewhere

b. It is not highly dependent on other goods or services in the contract

c. It has a stand-alone selling price

d. It is not interrelated with other goods or services in the contract

Which of the following is not an example of a derivative?

a. Interest rate swap.

b. Cash.

c. Stock option.

d. Forward contract.

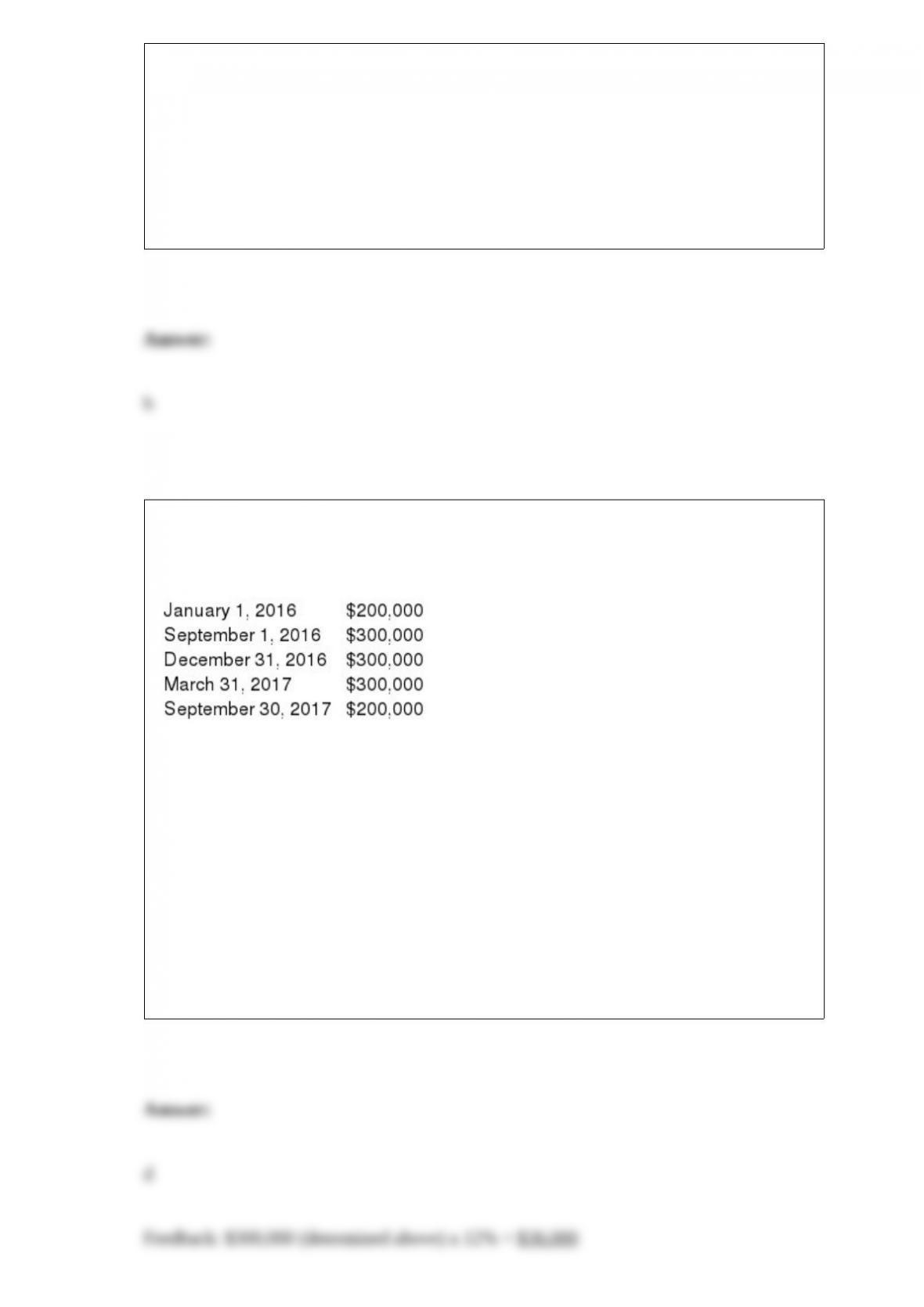

On January 1, 2016, Kendall Inc. began construction of an automated cattle feeder

system. The system was finished and ready for use on September 30, 2017.

Expenditures on the project were as follows:

Kendall borrowed $750,000 on a construction loan at 12% interest on January 1, 2016.

This loan was outstanding throughout the construction period. The company had

$4,500,000 in 9% bonds payable outstanding in 2016 and 2017. Interest capitalized for

2016 was:

a. $48,000.

b. $42,000.

c. $60,000.

d. $36,000.

Change in equity from nonowner sources is:

a. Comprehensive income.

b. Revenues.

c. Expenses.

d. Gains and losses.

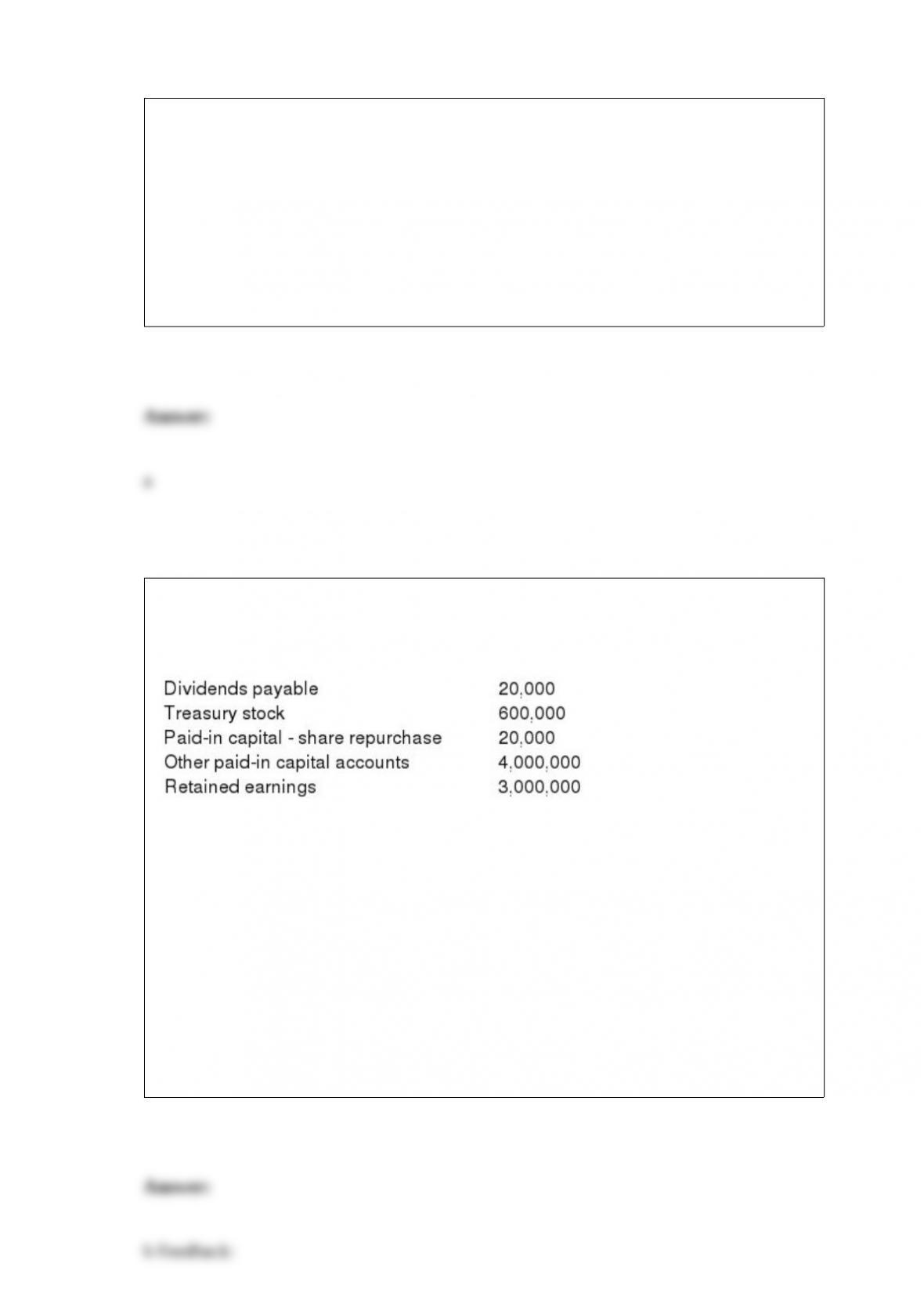

What would shareholders’ equity be as of December 31, 2017?

As of December 31, 2016, Warner Corporation reported the following:

During 2017, half of the treasury stock was resold for $240,000; net income was

$600,000; cash dividends declared were $1,500,000; and stock dividends declared were

$500,000.

a. Amount is not shown.

b. $5,760,000.

c. $5,820,000.

d. $6,760,000.

Accounting for costs of incentive programs for customer purchases:

a. Requires probability estimation.

b. Follows the matching principle.

c. Is a loss contingency situation.

d. All of these answer choices are correct.

Garland Inc. offers a new employee a lump-sum signing bonus at the date of

employment, June 1, 2016. Alternatively, the employee can take $39,000 at the date of

employment plus $10,000 each June 1 for five years, beginning in 2020. Assuming the

employee’s time value of money is 9% annually, what lump sum at employment date

would make him indifferent between the two options?

a. $44,035.

b. $40,855.

c. $69,035.

d. $65,855.

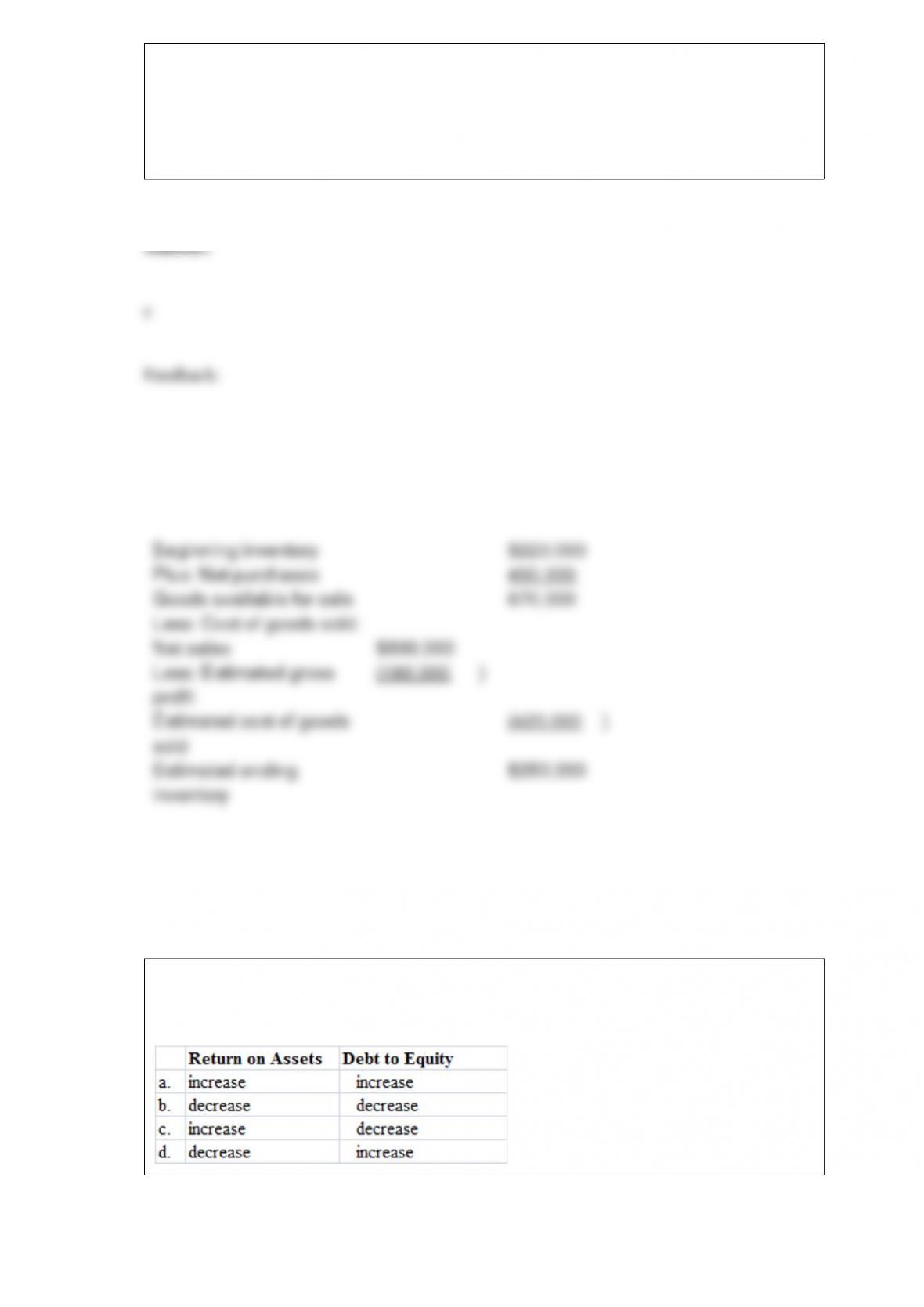

Howard’s Supply Co. suffered a fire loss on April 20, 2016. The company’s last physical

inventory was taken January 30, 2016, at which time the inventory totaled $220,000.

Sales from January 30 to April 20 were $600,000 and purchases during that time were

$450,000. Howard’s consistently reports a 30% gross profit. The estimated inventory

loss is:

a. $490,000.

b. $238,000.

c. $250,000.

d. None of these answer choices are correct.

Red Corp. has a rate of return on assets of 10% and a debt to equity ratio of 2 to 1. Not

including any indirect effects on earnings, the immediate impact of retiring debt on

these ratios is a(n)

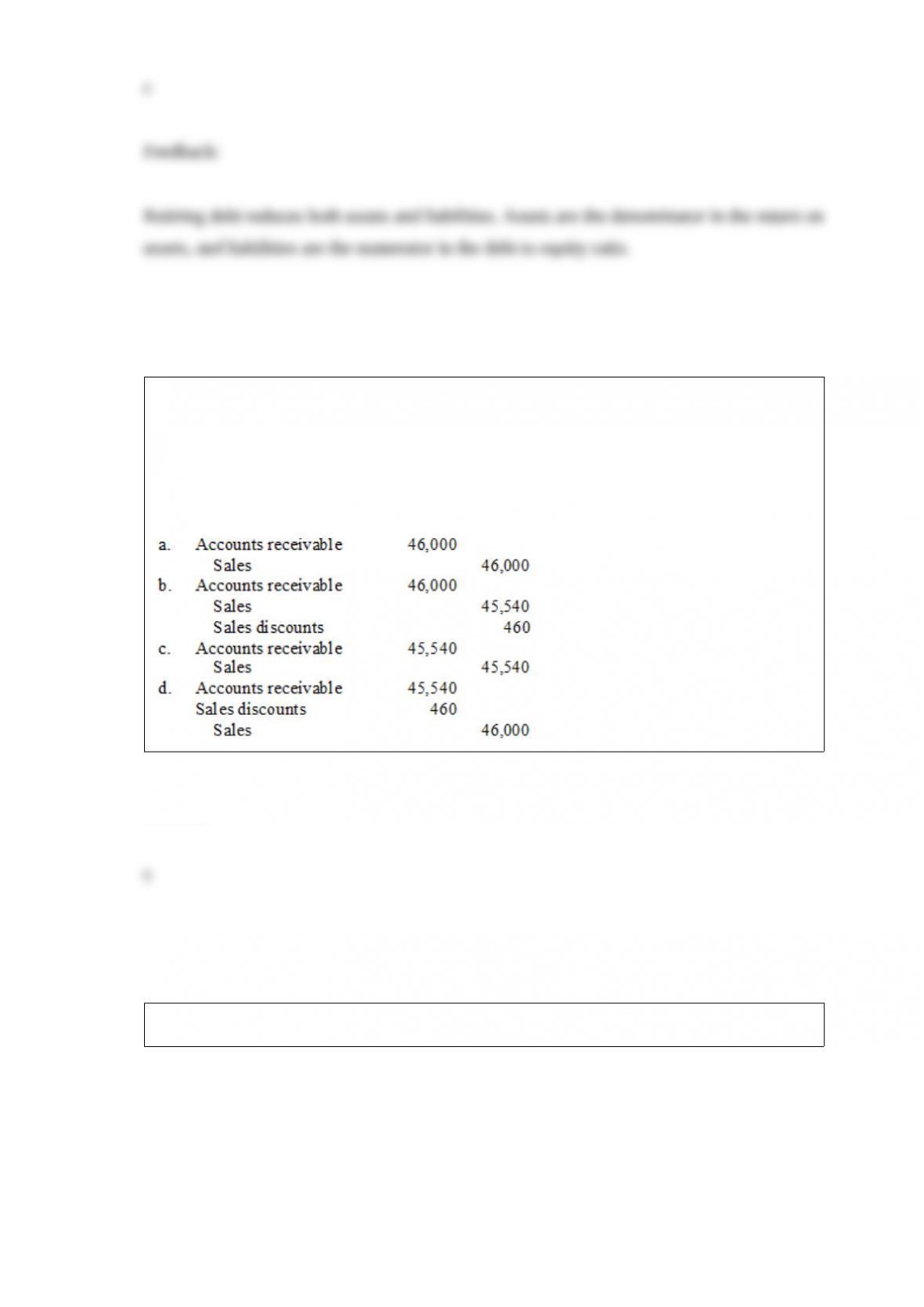

Harvey’s Wholesale Company sold supplies of $46,000 to Northeast Company on April

12 of the current year, with terms 1/15, n/60. Harvey uses the net method of accounting

for cash discounts.

What entry would Harvey’s make on April 12?

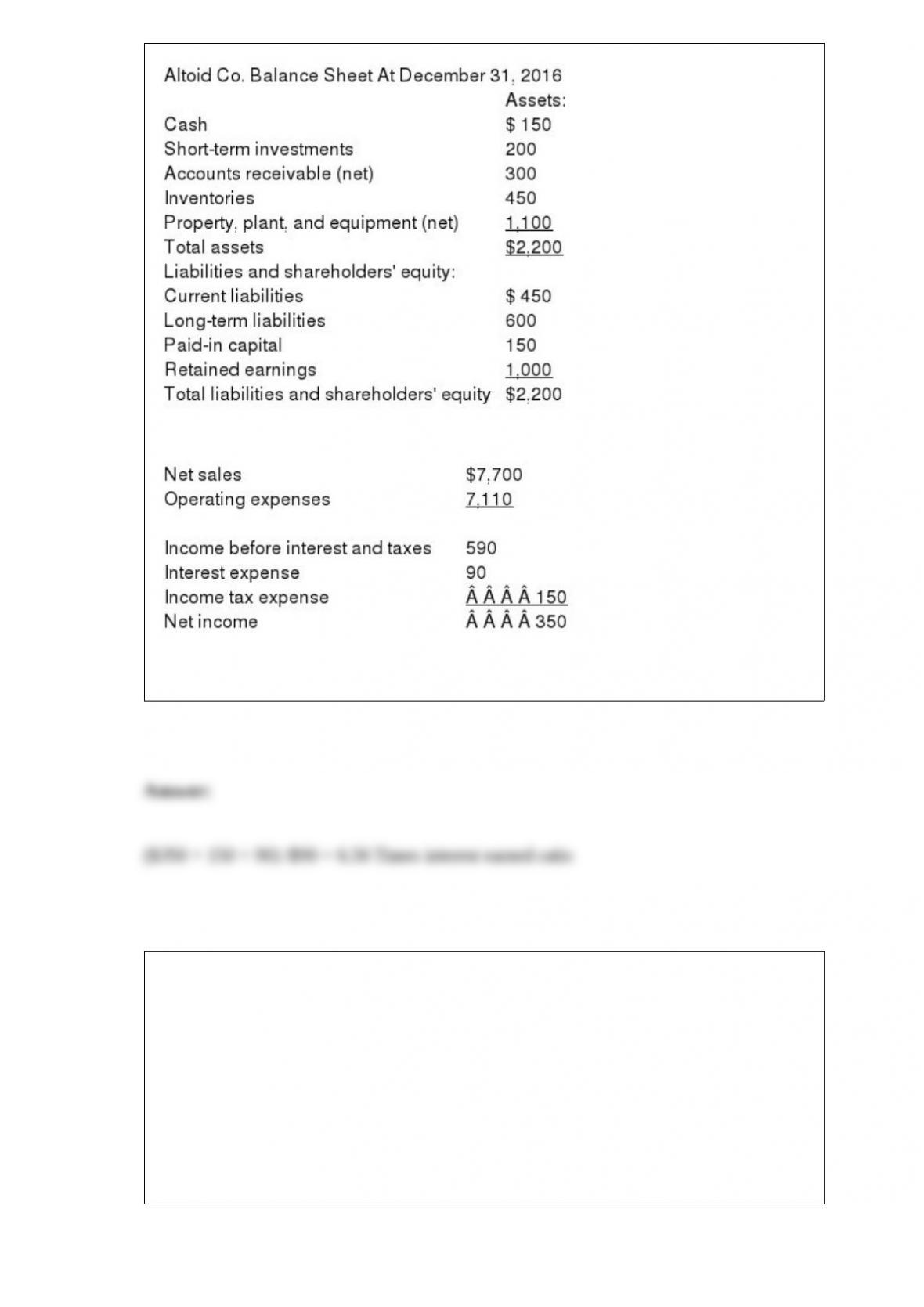

The balance sheet for Altoid Co. is shown below.

Selected 2016 income statement information for Altoid Co. includes:

Required: Compute the following financial statement ratios for 2016: Altoid Co.’s

times interest earned ratio. Round your answer to two decimal places.

Albatross Company purchased a piece of machinery for $60,000 on January 1, 2014,

and has been depreciating the machine using the sum-of-the-years’-digits method based

on a five-year estimated useful life and no salvage value. On January 1, 2016, Albatross

decided to switch to the straight-line method of depreciation. The salvage value is still

zero and the estimated useful life did not change. Ignore income taxes.

Required:

(1.) Prepare the appropriate journal entry, if any, to record the accounting change.

(2.) Prepare the journal entry to record depreciation for 2016.

On September 1, 2016, Jacob Furniture Mart enters into a tentative agreement to sell

the assets of its office equipment division. This division qualifies as a component of the

entity according to GAAP regarding discontinued operations. The division’s

contribution to Jacob’s operating income for 2016 was a $3 million loss before taxes.

Jacob has an average tax rate of 30%. Required: Consider independently the

appropriate accounting by Jacob under the three scenarios below.

Scenario 1: Assume that Jacob sold the division’s assets on December 31, 2016, for $24

million. The book value of the division’s assets was $19 million at that date. Under

these assumptions, what would Jacob report in its 2016 income statement regarding the

office equipment division? Explain where this information would be presented.

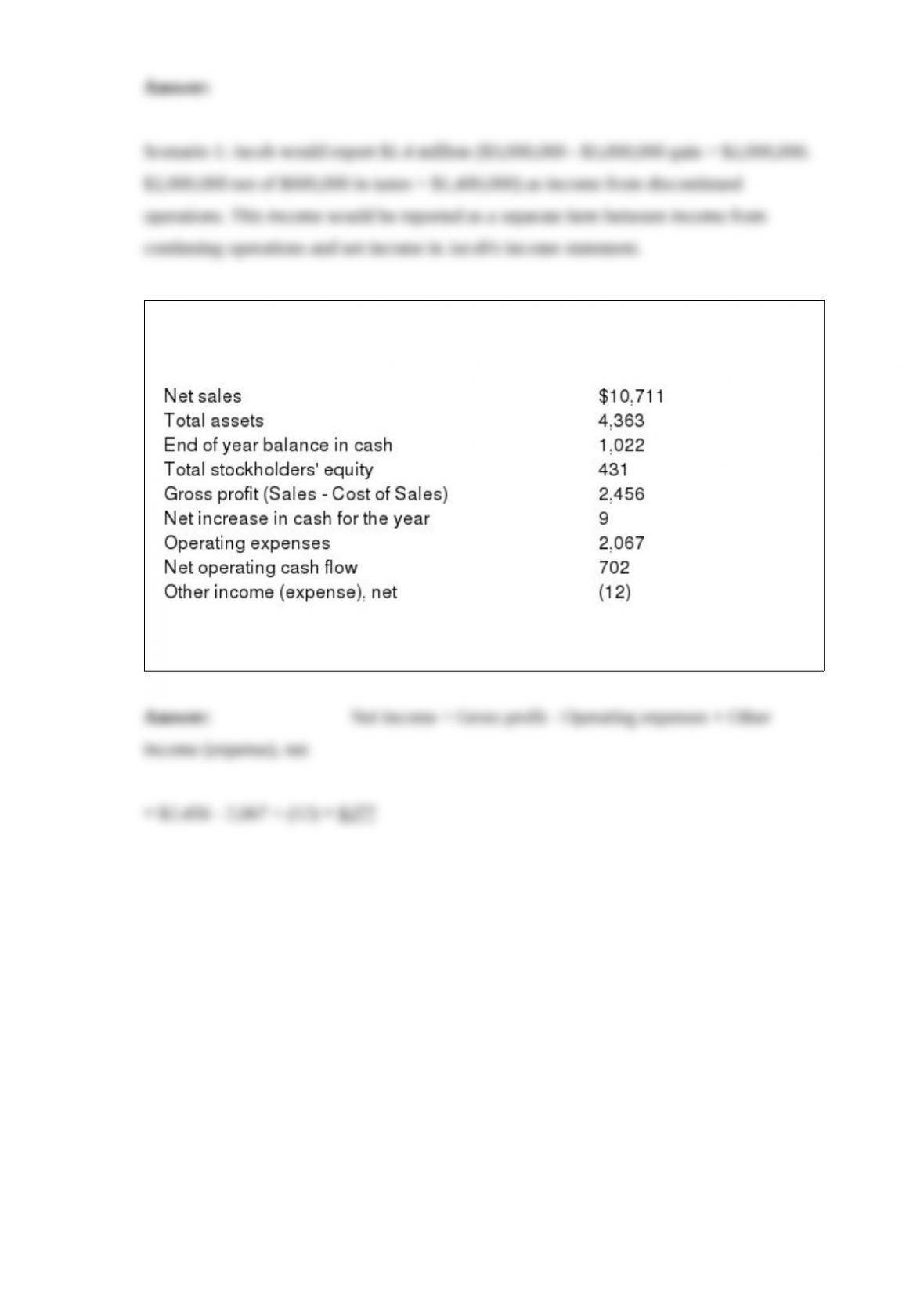

The following information ($ in millions) comes from a recent annual report of

Amazon.com, Inc.:

Compute the income before income tax for Amazon.