1) The decision to accept an additional volume of business should be based on a

comparison of the revenue from the additional business with the sunk costs of

producing that revenue.

2) A dishonored note receivable is usually reclassified as an account receivable.

3) Revenue expenditures are additional costs of plant assets that materially increase the

assets’ life or productive capabilities.

4) A department can never be considered to be a profit center.

5) Organization expenses of a corporation often include legal fees and promoter fees.

6) An activity-based costing system usually involves a fewer number of allocations

compared with a traditional cost allocation system.

7) Book value per common share is calculated by dividing stockholders’ equity

applicable to common shares by the number of common shares outstanding.

8) Investments in trading securities are accounted for using the equity method with

consolidation.

9) In a job order cost accounting system, any immaterial underapplied overhead at the

end of the period can be charged entirely to Cost of Goods Sold.

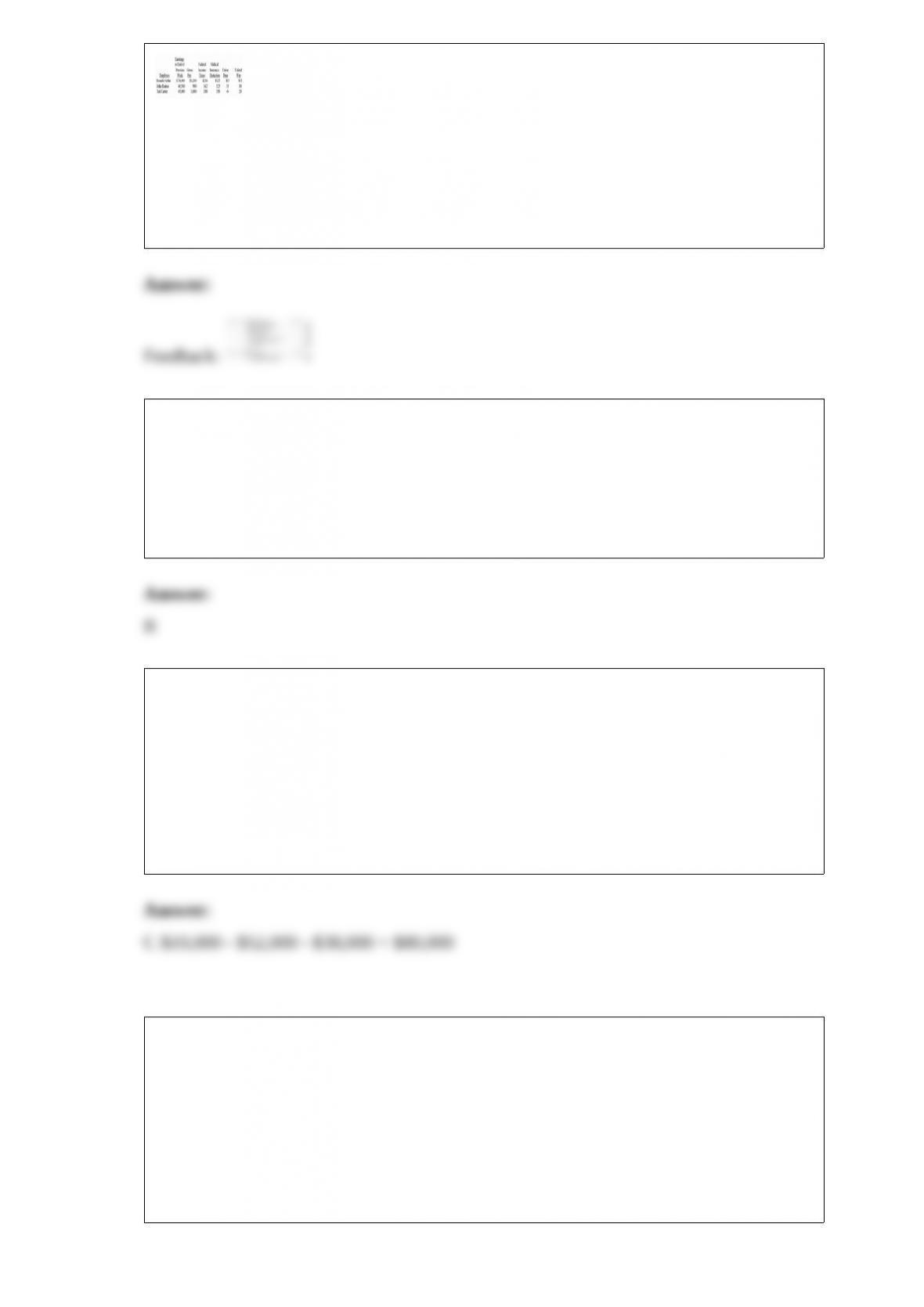

10) The amount of federal income tax withheld depends on the employee’s annual

earnings rate and the number of withholding allowances claimed by the employee.

11) When time ticket information is entered into the accounting system, the journal

entry is a debit to Factory Payroll and a credit to Goods in Process Inventory.

12) Curvilinear costs are also known as nonlinear costs.

13) A flexible budget expresses all costs on a per unit basis.

14) Ratios, like other analysis tools, are only historically oriented.

15) Accounting for contingent liabilities covers three possibilities. (1) The future event

is probable and the amount cannot be reasonably estimated. (2) The future event is

remote or unlikely to recur. (3) The likelihood of the liability to occur is impossible.

16) Relevant benefits refer to the additional or incremental revenue generated by

selecting a particular course or action over another.

17) The present value of $5,000 per year for three years at 12% compounded annually

is $12,009.

18) The cost of all materials issued to production are debited to Goods in Process

Inventory.

19) Accounting procedures for all items are the same for both C corporations and S

corporations in all aspects.

20) The statement of owner’s equity:

A.Reports how equity changes at a point in time

B.Reports how equity changes over a period of time

C.Reports on cash flows for operating, financing, and investing activities over a period

of time

D.Reports on cash flows for operating, financing, and investing activities at a point in

time

E.Reports on amounts for assets, liabilities, and equity at a point in time

21) When a company’s activities include income-related events not part of normal,

continuing operations, the complete income statement could potentially have the

following sections:

A.Items from continuing operations and earnings per share for a corporation

B.Income or loss from operating a discontinued segment for the current period

C.The loss from disposing of the discontinued segment’s net assets

D.Extraordinary items

E.Continuing operations, discontinued segments, extraordinary items, changes in

accounting principles, and earnings per share for a corporation

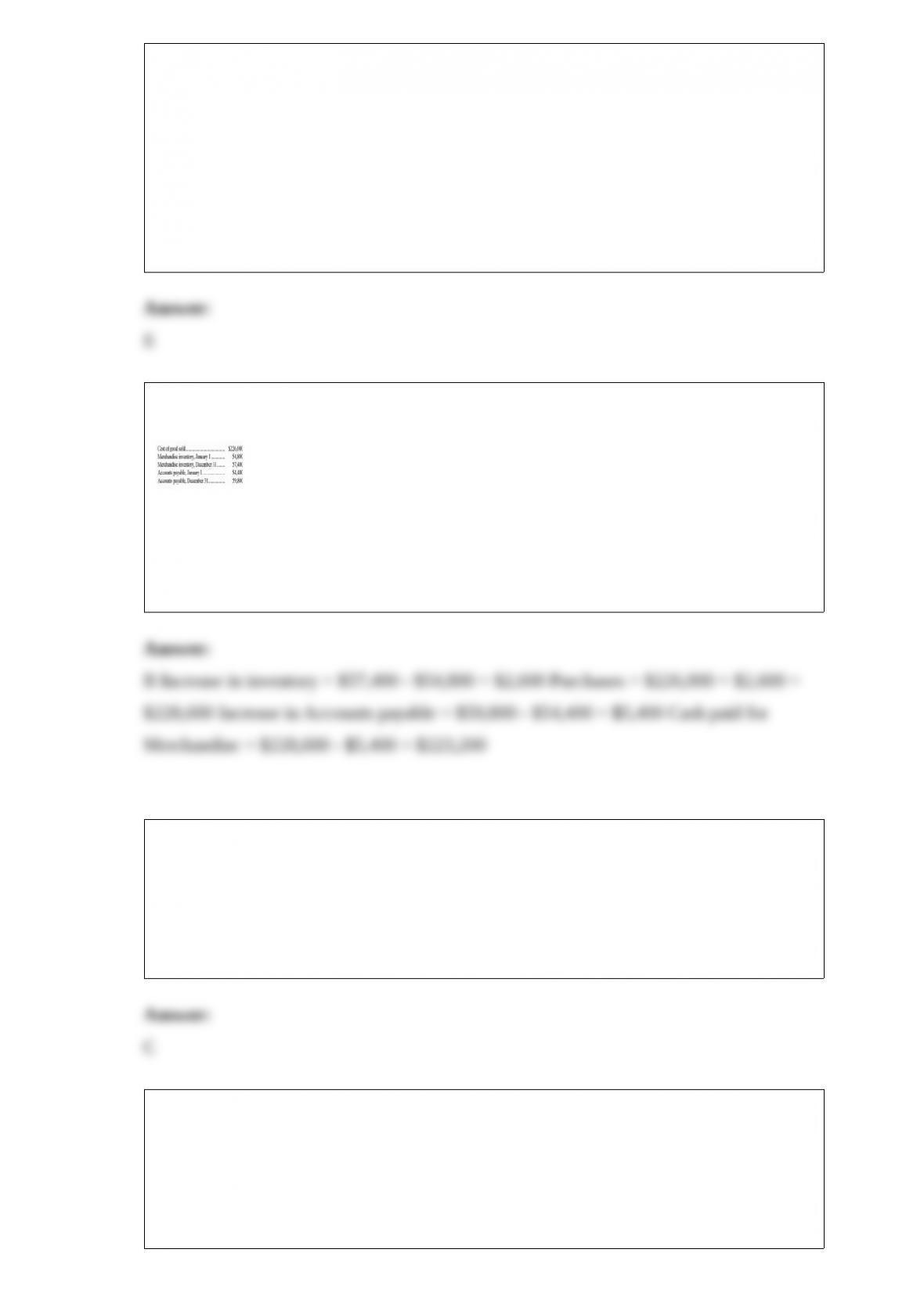

22) Use the following information about the current year’s operations of a company to

calculate the cash paid for merchandise.

A.$218,000

B.$223,200

C.$220,000

D.$228,800

E.$234,000

23) The least-squares regression method is:

A.A graphical method to identify cost behavior

B.An algebraic method to identify cost behavior

C.A statistical method to identify cost behavior

D.The only identify cost estimation method allowed by GAAP

E.A cost estimation method that only uses the two extreme values

24) An investor purchased at par value $75,000 of Cort’s 8% bonds, that mature in

three-years. The bonds pay interest semiannually on June 1 and December 1. The

investor plans to hold the bonds until they mature. When the bonds mature, the investor

should prepare the following journal entry:

A.debit Long-Term Investments-HTM, $75,000; credit Cash, $75,000

B.debit Cash, $6,000; credit, Unrealized Gain-Equity, $6,000

C.debit Cash, $75,000; credit Long-Term InvestmentsHTM, $75,000

D.debit Unrealized Gain-Equity, $6,000; credit Cash, $6,000

E.debit Cash, $75,000; credit Long-Term InvestmentsTrading, $75,000

25) The Haskins Company manufactures and sells radios. Each radio sells for $23.75

and the variable cost per unit is $16.25. Haskin’s total fixed costs are $25,000, and

budgeted sales are 8,000 units. What is the contribution margin per unit?

A.$7.50

B.$16.25

C.$23.75

D.$60,000

E.$1.25

26) ABC Corporation’s total quick assets were $5,888,000, its current assets were

$11,700,000 and its current liabilities were $8,000,000. Its acid-test ratio equals:

A.0.50.

B.0.68.

C.0.74.

D.1.50.

E.2.20.

27) A company had inventory on November 1 of 5 units at a cost of $20 each. On

November 2, they purchased 10 units at $22 each. On November 6 they purchased 6

units at $25 each. On November 8, 8 units were sold for $55 each. Using the LIFO

perpetual inventory method, what was the value of the inventory on November 8 after

the sale?

A.$304

B.$296

C.$288

D.$280

E.$276

28) When factory payroll costs for labor are allocated in a job cost accounting system:

A.Factory Payroll is debited and Goods in Process Inventory is credited

B.Goods in Process Inventory and Factory Overhead are debited and Factory Payroll is

credited

C.Cost of Goods Manufactured is debited and Direct Labor is credited

D.Direct Labor and Indirect Labor are debited and Factory Payroll is credited

E.Goods in Process Inventory is debited and Factory Payroll is credited

29) Assets, liabilities, and equity accounts are not closed; these accounts are called:

A.Nominal accounts

B.Temporary accounts

C.Permanent accounts

D.Contra accounts

E.Accrued accounts

30) On January 1, Alco Company purchases manufacturing equipment costing $95,000

that is expected to have a five-year life and an estimated salvage value of $5,000. Alco

uses the straight-line depreciation method to allocate costs. The adjusting entry needed

on December 31 is:

A.Debit Depreciation Expense, $9,000; credit Accumulated Depreciation, $9,000

B.Debit Depreciation Expense, $18,000; credit Accumulated Depreciation, $18,000

C.Debit Depreciation Expense, $90,000; credit Accumulated Depreciation, $90,000

D.Debit Depreciation Expense, $18,000; credit Equipment, $18,000

E.Debit Depreciation Expense, $9,000; credit Equipment, $9,000

31) During March, the production department of a process manufacturing system

completed a number of units of a product and transferred them to finished goods. Of the

units transferred, 25,000 were in process at the beginning of March and 110,000 were

started and completed in March. March’s beginning inventory units were 100%

complete with respect to materials and 55% complete with respect to labor. At the end

of March, 30,000 additional units were in process in the production department and

were 100% complete with respect to materials and 30% complete with respect to labor.

Compute the number of units transferred to finished goods.

A.110,000

B.135,000

C.105,000

D.165,000

E.144,000

32) Dividing accounts receivable, net by net sales and multiplying the result by 365 is

the:

A.Profit margin

B.Days’ sales uncollected

C.Accounts receivable turnover ratio

D.Average accounts receivable ratio

E.Current ratio

33) A company manufactures and sells a product for $120 per unit. The company’s fixed

costs are $68,760, and its variable costs are $90 per unit. The company’s break-even

point in units is:

A.2,292

B.573

C.764

D.327

E.840

34) Carmel Company acquires a mineral deposit at a cost of $5,900,000. It incurs

additional costs of $600,000 to access the deposit, which is estimated to contain

2,000,000 tons and is expected to take 5 years to extract. What journal entry would be

needed to record the expense for the first year assuming 418,000 tons were mined?

A.Debit Depletion Expense $1,233,100; credit Accumulated Depletion $1,233,100

B.Debit Amortization Expense $1,358,500; credit Accumulated Amortization

$1,358,500

C.Debit Depreciation Expense $1,358,500; credit Accumulated Depreciation

$1,358,500

D.Debit Depletion Expense $1,358,500; credit Accumulated Depletion $1,358,500

E.Debit Depreciation Expense $1,233,100; credit Accumulated Depreciation

$1,233,100

35) A company purchased $4,000 worth of merchandise. Transportation costs were an

additional $350. The company later returned $275 worth of merchandise and paid the

invoice within the 2% cash discount period. The total amount paid for this merchandise

is:

A.$3,725.00.

B.$3,925.00.

C.$3,900.

D.$4,000.50.

E.$4,075.00.

36) An estimate of an asset’s value to the company, calculated by discounting the future

cash flows from the investment at an appropriate rate and then subtracting the initial

cost of the investment, is known as:

A.Annual net cash flows

B.Rate of return on investment

C.Net present value

D.Payback period

E.Unamortized carrying value

37) The cost of labor that is not clearly associated with specific units or batches of

product is called:

A.Unspecified labor

B.Direct labor

C.Indirect labor

D.Basic labor

E.Joint labor

38) The payroll records of a company provided the following data for the weekly pay

period ended December 7:

The FICA social security tax rate is 6.2% and the FICA Medicare tax rate is 1.45% on

all of this week’s wages paid to each employee. The federal and state unemployment tax

rates are 0.8% and 5.4%, respectively, on the first $7,000 paid to each employee.

Prepare the journal entries to (a) accrue the payroll and (b) record payroll taxes

expense.

39) Secured bonds:

A.Are called debentures

B.Have specific assets of the issuing company pledged as collateral

C.Are backed by the issuer’s bank

D.Are subordinated to those of other unsecured liabilities

E.Are the same as sinking fund bonds

40) Stojko Corporation had a net decrease in cash of $10,000 for the current year. Net

cash used in investing activities was $52,000 and net cash used in financing activities

was $38,000. What amount of cash was provided (used) in operating activities?

A.$100,000 provided

B.$(100,000) used

C.$80,000 provided

D.$(80,000) used

E.$(10,000) used

41) If the credit balance of the Allowance for Doubtful Accounts account exceeds the

amount of a bad debt being written off, the entry to record the write-off against the

allowance account results in:

A.An increase in the expenses of the current period

B.A reduction in current assets

C.A reduction in equity

D.No effect on the expenses of the current period

E.A reduction in current liabilities

42) A company bought a new display case for $42,000 and was given a trade-in of

$2,000 on an old display case, so the company paid $40,000 cash with the trade-in. The

old case had an original cost of $37,000 and accumulated depreciation of $34,000. If

the transaction has commercial substance, the company should record the new display

case at:

A.$2,000

B.$3,000

C.$40,000

D.$42,000

E.$43,000

43) Sellers allow customers to use credit cards:

A.To avoid having to evaluate a customer’s credit standing for each sale

B.To lessen the risk of extending credit to customers who cannot pay

C.To speed up receipt of cash from the credit sale

D.To increase total sales volume

E.All of these

44) Ethical behavior requires:

A.That auditors’ pay not depend on the success of the client’s business

B.Auditors to invest in businesses they audit

C.Analysts to report information favorable to their companies

D.Managers to use accounting information to benefit themselves

E.That auditors’ pay depend on the success of the client’s business

45) Decreases in equity that represent costs of assets or services used to earn revenues

are called:

A.Liabilities

B.Equity

C.Withdrawals

D.Expenses

E.Owner’s Investment

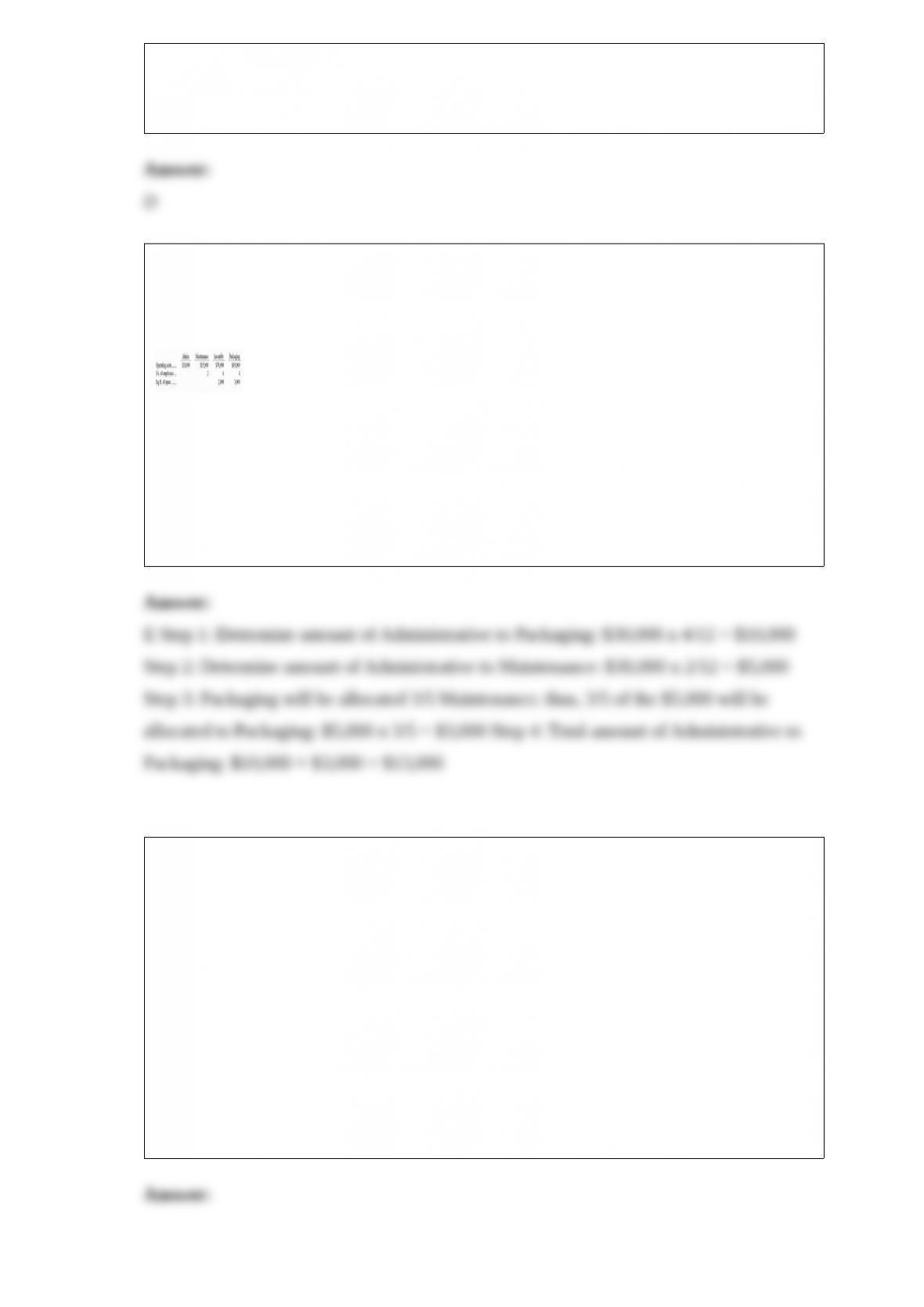

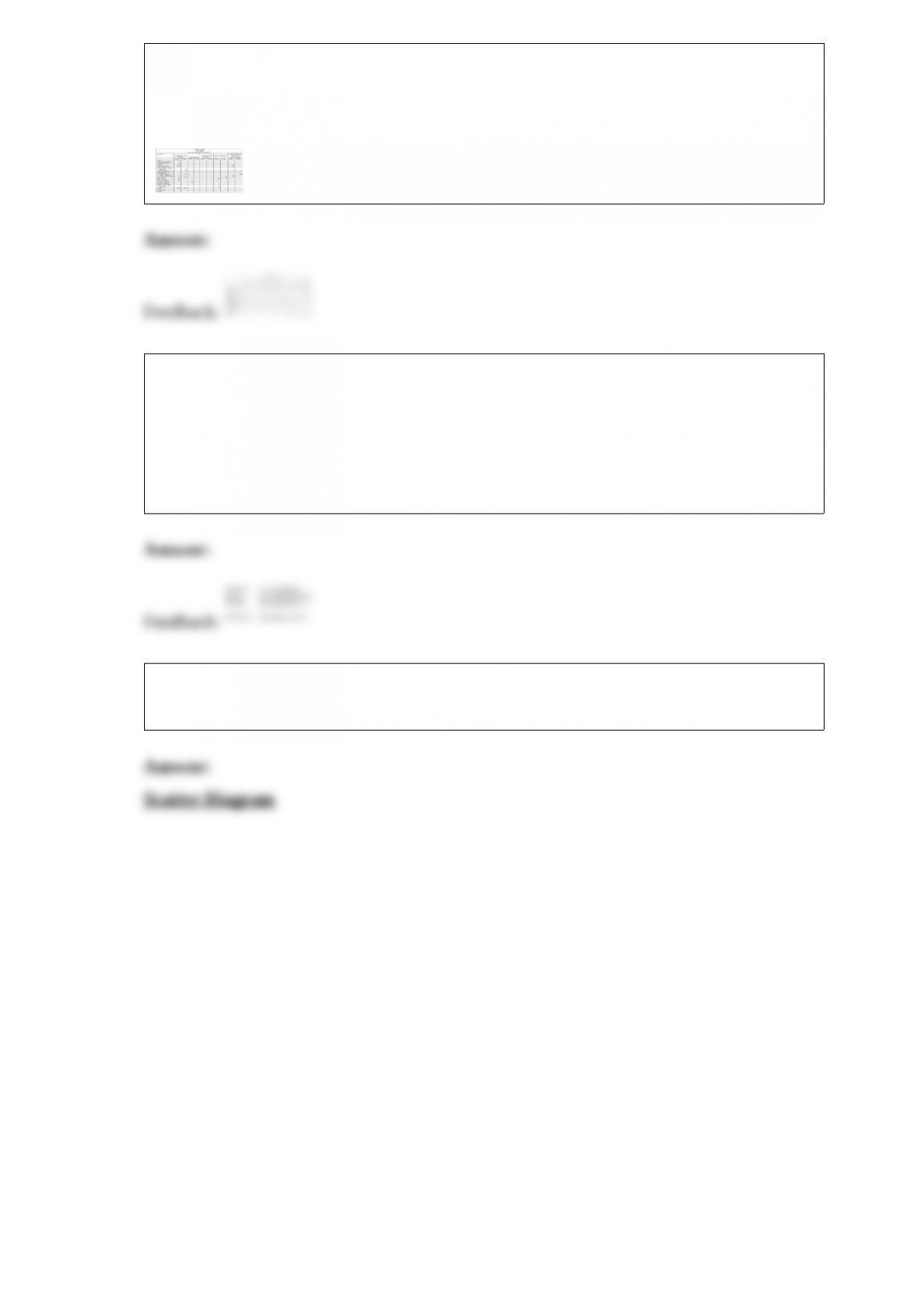

46) Farber, Inc., has four departments. The Administrative Department costs are

allocated to the other three departments based on the number of employees in each and

the Maintenance Department costs are allocated to the Assembly and Packaging

Departments based on their occupied space. Data for these departments follows:

The total amount of the Administrative Department’s cost that would eventually be

allocated to the Packaging Department is:

A.$4,800

B.$12,000

C.$10,000

D.$18,000

E.$13,000

47) Jane, Castle, and Sean are dissolving their partnership. Their partnership agreement

allocates each partner an equal share of all income and losses. The current period’s

ending capital account balances are Jane, $54,000; Castle, $42,000; and Sean, $(6,000).

After all assets are sold and liabilities are paid, there is $90,000 in cash to be

distributed. Sean is unable to pay the deficiency. The journal entry to record the

distribution should be:

A.Debit Jane, Capital $54,000; debit Castle, Capital $36,000; credit Cash $90,000

B.Debit Jane, Capital $54,000; debit Castle, Capital $42,000; credit Cash $96,000

C.Debit Jane, Capital $51,000; debit Castle, Capital $39,000; credit Cash $90,000

D.Debit Cash $90,000, debit Sean, Capital $6,000, credit Jane, Capital $54,000, credit

Castle, Capital $42,000

E.Debit Cash $90,000; credit Jane, Capital $30,000; credit Castle, Capital $30,000;

credit Sean, Capital $30,000

48) The use of an Accounts Payable controlling account:

A.Reduces the number of accounts in the subsidiary ledger

B.Reduces the total number of accounts maintained

C.Reduces the number of entries in the general journals

D.Reduces the number of accounts in the general ledger

E.Increases the number of columns in the journals

49) A company’s current assets were $17,980, its quick assets were $11,420 and its

current liabilities were $12,190. Its quick ratio equals:

A.0.94.

B.1.07.

C.1.48.

D.1.57.

E.2.40.

50) In the preparation of departmental income statements, the preparer completes the

following steps in the following order:

A.Identify direct expenses; allocate indirect expenses; allocate service department

expenses

B.Identify indirect expenses; allocate direct expenses; allocate service department

expenses

C.Identify service department expenses; allocate direct expenses; allocate indirect

expenses

D.Identify direct expenses, allocate service department expenses, allocate indirect

expenses

E.Allocate all expenses

51) J. Awn, the proprietor of Awn Services, withdrew $8,700 from the business during

the current year. The entry to close the withdrawals account at the end of the year is:

A.Debit J. Awn, Withdrawals $8,700; credit Cash, $8,700

B.Debit J. Awn, Capital $8,700; credit J. Awn, Withdrawals $8,700

C.Debit J. Awn, Withdrawals $8,700; credit J. Awn, Capital $8,700

D.Debit J. Awn, Capital $8,700, credit Salary Expense $8,700

E.Debit Income Summary $8,700; credit J. Awn, Capital $8,700

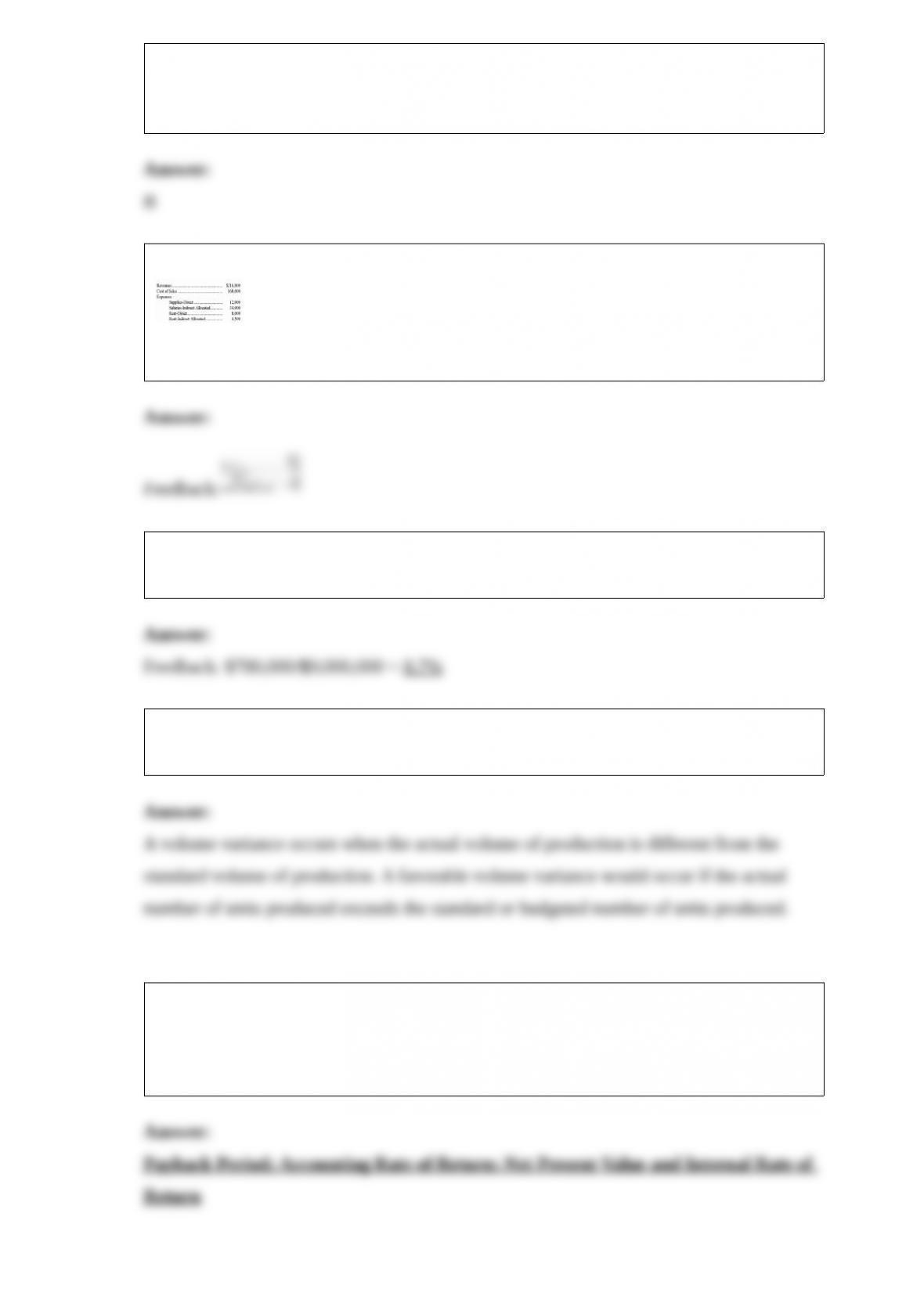

52) The following data is available for the Cleaning Services Department of Amitol Co.

Required: Calculate departmental contribution to overhead for the Cleaning Services

Department, including the department’s contribution as a percentage of revenues.

53) Ned’s net income was $780,000; its net assets were $5,200,000; and its net sales

were $9,000,000. Calculate its profit margin ratio.

54) What is the overhead volume variance? What would be the cause of a favorable

volume variance?

55) In evaluating capital budgeting alternatives, there are two primary methods that do

not consider the time value of money. These methods are _______________ and

_________________. There are also two primary methods that consider the time value

of money; these are ___________________ and ______________________.

56) A partially completed work sheet is shown below. The unadjusted trial balance

columns are complete. Complete the adjustments, adjusted trial balance, income

statement, and balance sheet and statement of owner’s equity columns.

57) A machine was purchased for $37,000 and depreciated for five years on a

straight-line basis under the assumption it would have a ten-year life and a $1,000

salvage value. At the beginning of the machine’s sixth year it was recognized the

machine had three years of remaining life instead of five and that at the end of the

remaining three years its salvage value would be $1,600. What amount of depreciation

should be recorded in each of the machine’s remaining three years?

58) One aid in measuring cost behavior involves creating a display of the data about

past costs in graphical form. Such a visual display is called a _____________________.