Which of the following is a correct statement?

A) The Sales Discounts account is a contra-asset account.

B) The Sales Returns & Allowances account is a contra-revenue account.

C) The Sales Returns & Allowances account is a credit balance account.

D) The Sales Discounts account is a contra-asset account.

A company started the year with a normal balance of $68,000 in the Inventory account.

During the year, debits totaling $45,000 and credits totaling $55,000 were posted to the

Inventory account. Which of the following statements about the Inventory account is

correct?

A) The normal balance of the Inventory account is a credit balance.

B) After these amounts are posted, the balance in the Inventory account is a credit

balance of $58,000.

C) The Inventory account is decreased by debits.

D) The debits and credits posted to the Inventory account caused it to decrease by

$10,000.

When bonds are retired at their maturity date, the balance in the Bonds Payable account

is equal to the bond’s:

A) face value minus any premium amortized.

B) face value plus interest to be paid.

C) face value plus any discount amortized.

D) face value.

A share of stock sells for $20. The company has $64 million in earnings and 200

million outstanding shares. The Price/Earnings ratio for the company is closest to:

A) 62.5

B) 200

C) 0.31

D) 6.4

Bearskin Inc. has recorded all the year-end adjustments. Its revenue accounts total

$190,000 and its expense accounts total $130,000. The closing entry to close the

income statement accounts for the year will debit the various:

A) expense accounts for a total of $130,000, debit Retained Earnings for $60,000, and

credit the various revenue accounts for a total of $190,000. .

B) revenue accounts for a total of $190,000, credit the various expense accounts for a

total of $130,000, and credit Retained Earnings for $60,000.

C) expense accounts for a total of $130,000, credit the various revenue accounts for a

total of $190,000, and credit Retained Earnings for $60,000.

D) revenue accounts for a total of $190,000, debit Retained Earnings for $60,000, and

credit the various expense accounts for a total of $130,000.

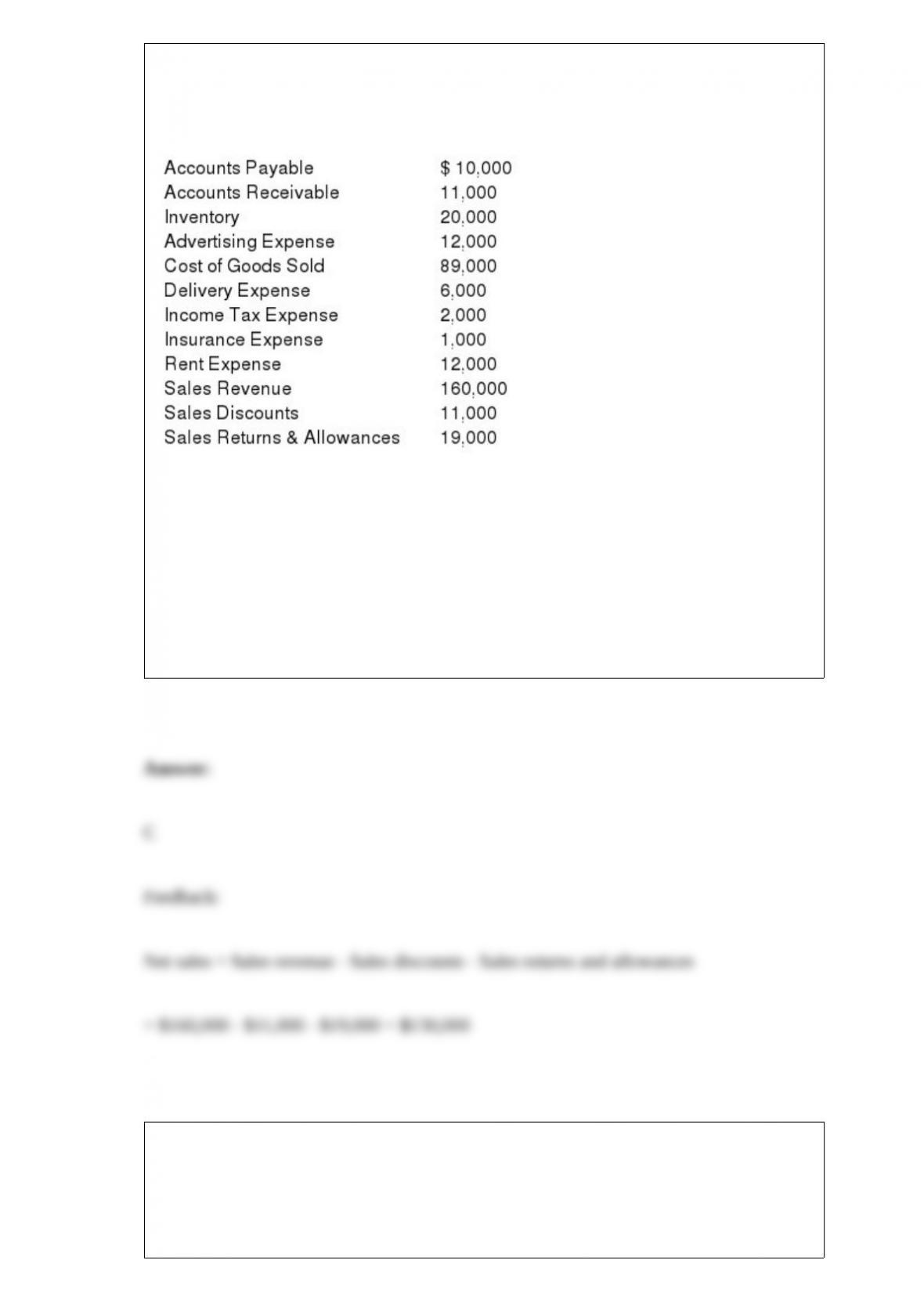

The following is a listing of some of the balance sheet accounts and all of the income

statement accounts for Aldine Inc. as they appear on the company’s adjusted trial

balance.

Use the information above to answer the following question. Net sales would be:

A) $30,000.

B) $124,000.

C) $130,000.

D) $160,000.

The adjusting entry to record the estimated bad debts in the period credit sales occur

would normally include a debit to:

A) Accounts Receivable and a credit to Allowance for Doubtful Accounts.

B) Bad Debt Expense and a credit to Allowance for Doubtful Accounts.

C) Allowance for Doubtful Accounts and a credit to Accounts Receivable.

D) Bad Debt Expense and a credit to Accounts Receivable.

Which of the following is an example of an error that would cause the trial balance to

be out of balance?

A) A journal entry was posted as a debit to Cash for $525 and a credit to Accounts

Receivable for $552.

B) A journal entry was posted as a debit to Cash and a credit to Sales Revenue when the

company received a $400 payment from a customer on account.

C) A purchase of supplies on account for $100 was posted as a debit to Supplies for $10

and a credit to Accounts Payable for $10.

D) A $350 transaction was not recorded at all.

On September 1, 2016, a company issued a $50,000, 6-month, 9% note payable to

purchase equipment. At December 31, 2016, the company records an adjusting entry to

accrue interest incurred by not paid. The company pays the note with interest at the

maturity date.

Use the information above to answer the following question. What is the entry to record

the payment of interest at the maturity date of the note?

A) Debit Notes Payable for $50,000, debit Interest Expense for $4,500, and credit Cash

for $54,500

B) Debit Interest Payable for $1,500, debit Interest Expense for $750, and credit Cash

for $2,250

C) Debit Interest Expense for $2,250, and credit Cash for $2,250

A) Debit Interest Expense for $2,000 debit Interest Payable for $2,500, and credit Cash

for $4,500

Current liabilities are expected to be:

A) converted to cash within one year.

B) settled within one year.

C) used in the business within one year.

D) acquired within one year.

An adjustment to ending inventory under the lower of cost or market (LCM) rule would

be least likely to be recorded by a company that sells:

A) a household staple like laundry detergent.

B) a fad product like Slap Wraps bracelets.

C) seasonal items like snow blowers.

D) high-tech goods like cell phones.

Lansing Company has a gross profit percentage of 61%, while Arbor Company has a

gross profit percentage of 37%. Which of the following statements is correct?

A) Lansing Company will report a higher net income than Arbor Company.

B) Arbor Company must have a greater sales volume than Lansing Company.

C) Lansing Company is more efficient at controlling selling, general, and administrative

expenses than Arbor Company.

D) Lansing Company and Arbor Company both earn enough on each sale to make a

contribution to their operating costs.