1) The accountant’s report on the examination of prospective financial statements

should include a caveat that the prospective results may not be achieved.

A) True

B) False

2) An auditor using nonstatistical sampling cannot:

A)

B)

C)

D)

3) Changes in reporting entities, such as the inclusion of an additional company in

combined financial statements, affect comparability but not consistency, and therefore

do not require an explanatory paragraph in the audit report.

A) True

B) False

4) When auditing the year-end cash balance, one of the areas of focus is on the accuracy

objective.

A) True

B) False

5) Which of the following is not one of the three categories of assertions?

A) Assertions about classes of transactions and events for the period under audit

B) Assertions about financial statements and correspondence to GAAP

C) Assertions about account balances at period end

D) Assertions about presentation and disclosure

6) When performing price tests for purchased inventory, the auditor would not be

concerned with the most recent vendors’ invoices if the client uses the FIFO valuation

method.

A) True

B) False

7) A prior period adjustment may result in a debit or credit to a company’s retained

earnings account.

A) True

B) False

8) Audits are expected to provide a higher degree of assurance for the detection of

material frauds than is provided for an equally material error.

A) True

B) False

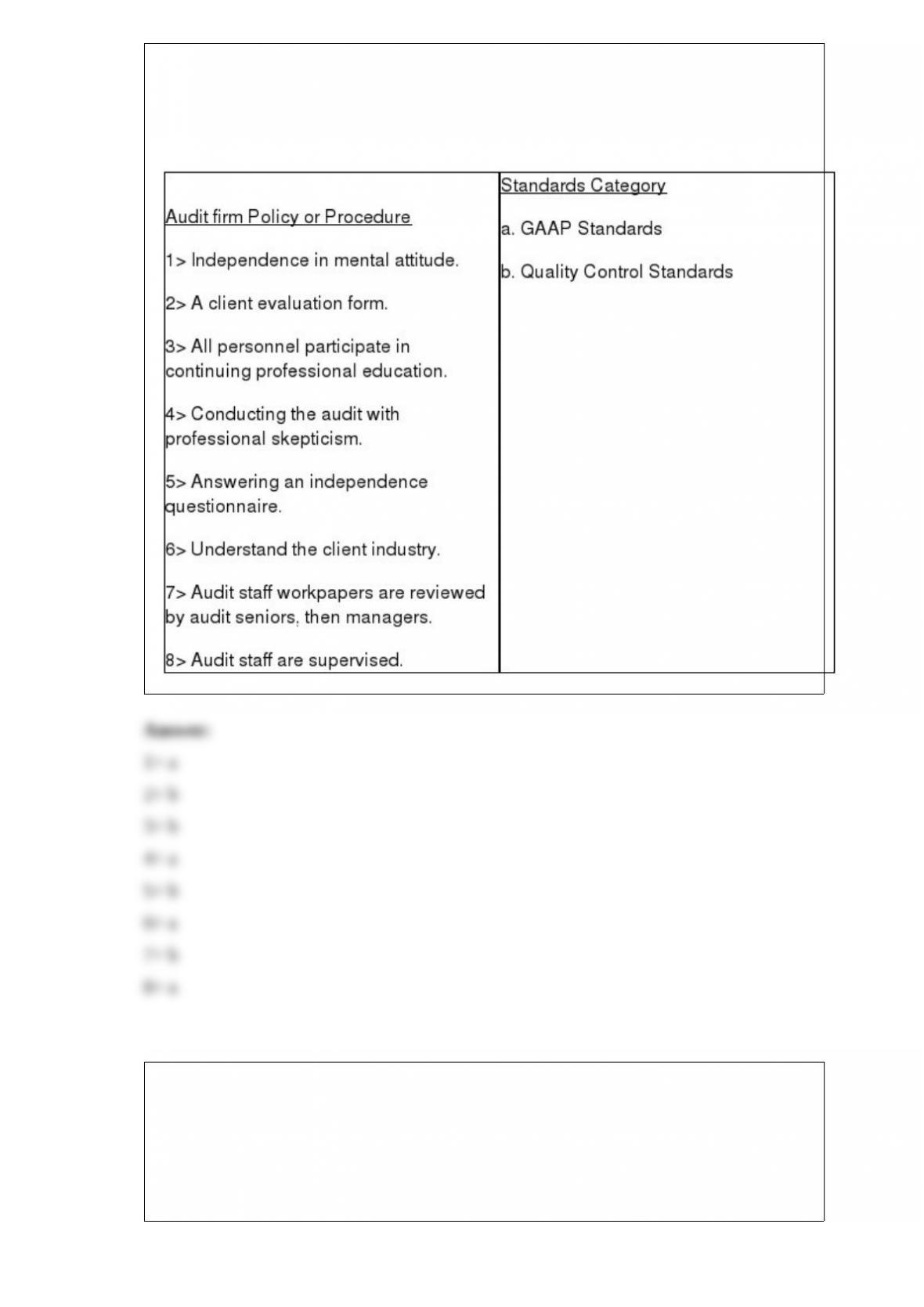

9) Listed below are policies or procedures that the Crystal Cove audit firm has in place.

For each identified policy or procedure state if it is a Generally Accepted Audit

Standard (GAAS) or a Quality Control Standard.

10) If a short-term note payable is included in the accounts payable balance on the

financial statement, there is a violation of the:

A) completeness assertion

B) existence assertion

C) cutoff assertion

D) classification and understandability assertion

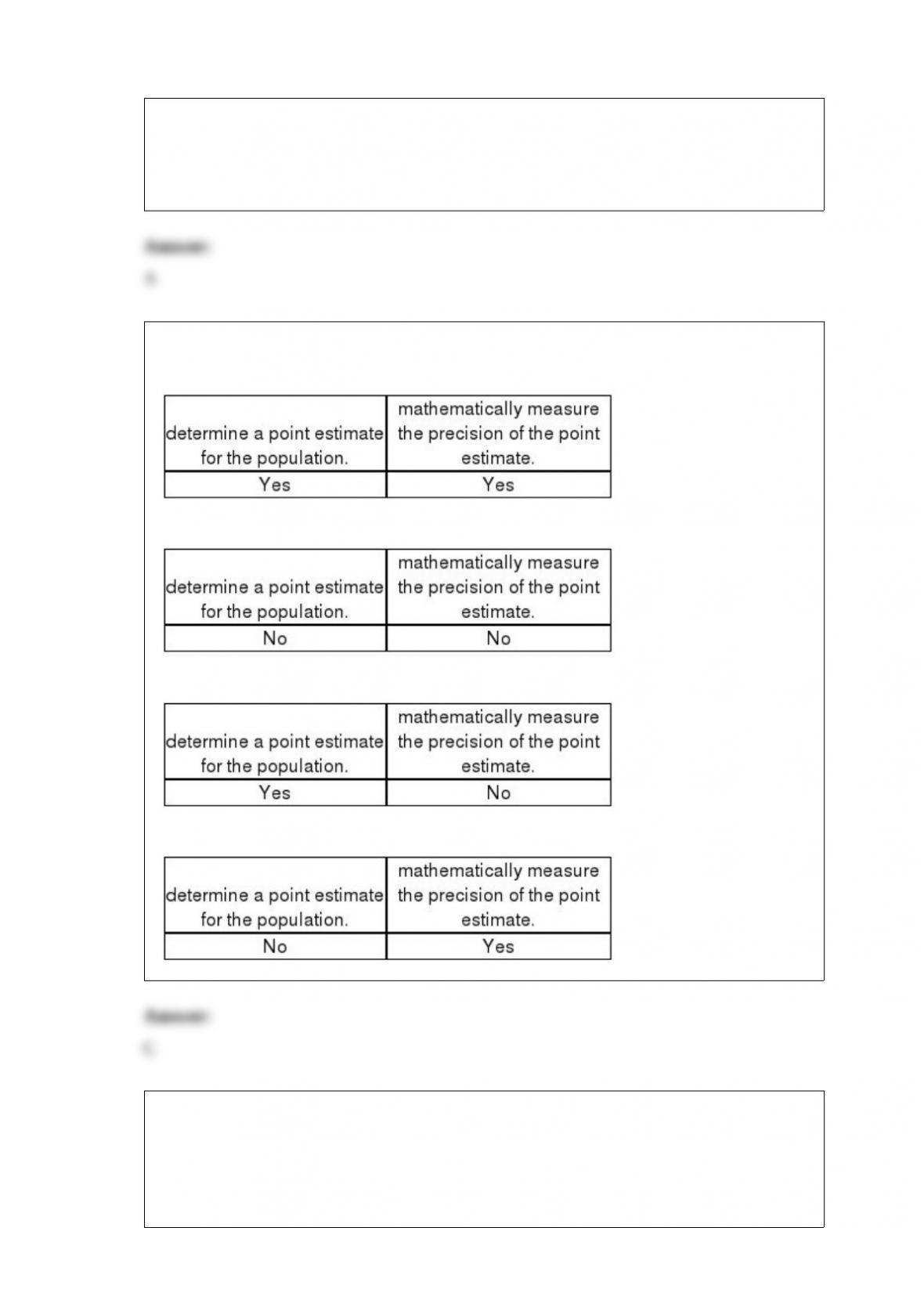

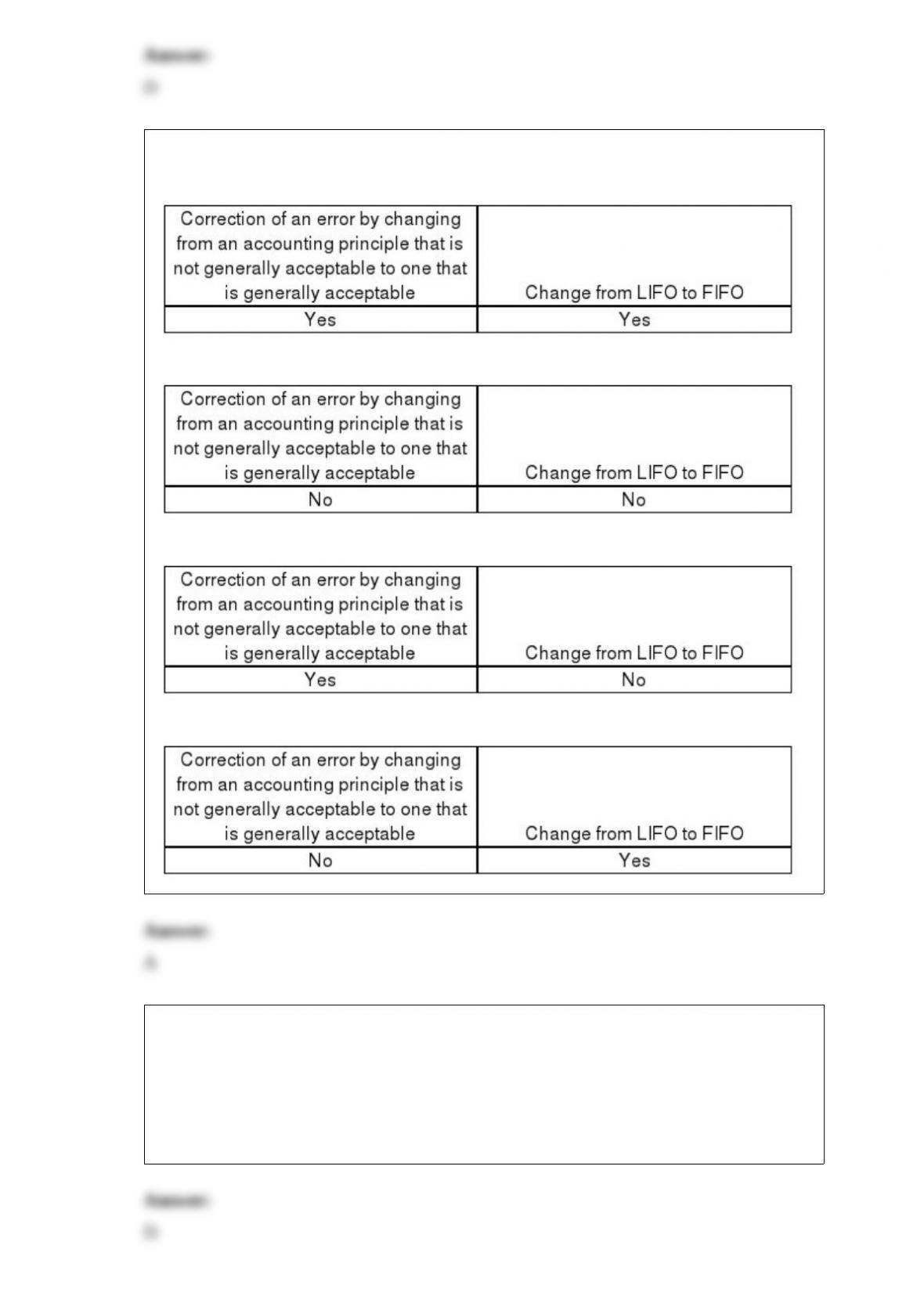

11) Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

12) Methods used to determine if there are legal encumbrances related to fixed assets

include all but which of the following?

A) Reading terms of loan and credit agreements

B) Reviewing loan confirmations received from banks

C) Having discussions with the client or sending letters to legal counsel

D) All of the above may be used to identify legal encumbrances

13) The audit tests to verify that the client is using an inventory method which is

generally accepted and to verify that physical counts were correctly summarized are

performed during the audit of the:

A) acquisition and payments cycle

B) payroll and personnel cycle

C) inventory and warehousing cycle

D) sales and collection cycle

14) Auditors are required to obtain a letter of representation that describes

management’s planned solutions to all internal control weaknesses identified during an

audit.

A) True

B) False

15) Which balance-related audit objective is not relevant to an audit of prepaid

expenses?

A) Rights

B) Accuracy

C) Detail tie-in

D) Realizable value

16) Which of the following statements is correct with respect to the auditor’s

responsibilities relative to the detection of indirect-effect illegal acts?

A) The auditor has no responsibility for searching for indirect-effect illegal acts

B) The auditor has the same responsibility for searching for indirect-effect illegal acts

as any other potential misstatement that may occur

C) Auditors have responsibility for searching for any illegal act, whether direct-effect or

indirect-effect

D) Discovery of indirect-effect illegal acts is usually easier than discovery of fraud

17) When determining whether independence is impaired because of an ownership

interest in a client company, materiality will affect ownership:

A) in all circumstances

B) only for direct ownership

C) only for indirect ownership

D) under no circumstances

18) Current professional auditing standards mandate the use of analytical procedures

during the testing phase of the audit.

A) True

B) False

19) Ordinarily, audit documentation can be provided to someone else only with the

express permission of the client.

A) True

B) False

20) The audit procedure “Perform tests of lower-of-cost-or-market, selling price, and

obsolescence” provides assurance mainly for the realizable value objective for

inventory pricing and compilation.

A) True

B) False

21) When the computed upper exception rate is greater than the tolerable exception rate

in attributes sampling, one possible appropriate course of action is to increase sample

size.

A) True

B) False

22) The audit objective to determine that notes payable in the schedule actually exist is

verified by the test of details of balances procedure to:

A) foot the notes payable list

B) confirm notes payable

C) recalculate interest expense

D) examine the balance sheet for proper disclosure of noncurrent portions

23) The Sarbanes-Oxley Act establishes standards related to the audits of privately held

companies.

A) True

B) False

24) The Code of Professional Conduct is established by the membership of the

A) Financial Accounting Standards Board

B) Securities and Exchange Commission

C) CPA licensing agencies within each state

D) Professional Ethics Executive Committee of the

25) These two conditions are generally present when material misstatements due to

fraud occurincentives and opportunities.

A) True

B) False

26) Which of the following tests determines that every field in a record has been

completed?

A) Validation

B) Sequence

C) Completeness

D) Programming

27) In phase 4 of the audit, complete the audit and issue an audit report, there are five

activities required. List below the activities.

28) Describe the methodology for designing tests of details of balances for notes

payable.

29) Describe the standard unqualified report to be issued for an audit of a private

company. Begin by specifying the seven parts of the report, and then discuss the

contents of each part.

30) Describe the differences between statistical and nonstatistical sampling in terms of

(1) the sample selection methods used, and (2) quantification of sampling risk.

31) Discuss the similarities and differences between financial statement audits,

operational audits, and compliance audits. Give an example of each type.

32) Discuss Rule 301Confidential Client Information, including the four exceptions to

the rule.

33) Define fraud and distinguish between the two main categories of fraud.

34) Discuss the differences and similarities between the roles of accountants and

auditors. What additional expertise must an auditor possess beyond that of an

accountant?

35) Describe purchase requisitions and purchase orders. What is a key difference

between the two documents?