Just-in-time inventory systems are characterized by extremely large inventories of

materials, work in process, and finished goods.

As the discount rate required by an investor increases, the present value of an

investment decreases.

Annuities may provide equal amounts to an investor at fixed periods of time over the

life of an investment.

The return on equity ratio may be either higher or lower than the return on assets ratio.

When an adjusting entry is made to record inventory shrinkage, the Inventory account

is debited and the Cost of Goods Sold account is credited.

A favorable materials price variance indicates that actual prices paid in acquiring

materials were more than standard prices.

The expropriation (seizure of) of a multinational company’s assets by a government is

an example of a discontinued operation item.

Opportunity costs are recorded in the accounting records.

The amortization of bond discount by the issuing company decreases the carrying value

of its bonds payable.

Liabilities are usually listed in order of magnitude, from smallest dollar amount to

largest dollar amount.

The purpose of the after-closing trial balance is to give assurance that the accounts are

in balance and ready for the new accounting period.

The preparation of a budgeted balance sheet requires consideration of the budgeted

capital expenditures and budgeted net income.

Supervisor salaries, equipment repairs, depreciation of machinery, and indirect

materials are all examples of manufacturing overhead.

A corporation, as well as a partnership, must file a corporate income tax return and pay

tax on its earnings.

If the total quality management approach is employed to determine the level at which

budgeted amounts are set, then absolute efficiency is assumed.

Capital turnover is equal to sales divided by average invested capital.

The statement of cash flows helps investors and creditors assess both the cash and

noncash aspects of a company’s investing and financing activities.

The responsibility margin is the contribution margin less common fixed costs.

In order to obtain the maximum tax benefit, companies that use a perpetual inventory

system can restate their year-end inventory at costs indicated by periodic LIFO costing

procedures.

The realization principle underlies the accounting practices of depreciating plant assets

and amortizing the cost of unexpired insurance policies.

Ding Company traded in one of its automobiles for a newer model. This transaction

may result in a gain or a loss being recorded on Ding’s financial statements.

An unrealized holding gain on available for sale securities will increase shareholders’

equity.

Any rational, systematic method of depreciation is acceptable, as long as costs are

allocated to expense in a reasonable manner.

The operating cycle of a merchandiser is longer and more complex than the operating

cycle of a manufacturer.

The income summary account appears on the statement of retained earnings.

The retail inventory method requires a company to state inventory on the year-end

balance sheet at its retail value.

Net Sales is computed as total sales revenue less sales returns and allowances less sales

discounts.

In general, the longer an account receivable is outstanding, the greater the likelihood it

will be collected.

The date on a statement of retained earnings is at a point in time; such as, at December

31, 2015.

The income statement approach used to estimate uncollectible receivables uses a

percentage of net sales without considering the current balance in the Allowance

account.

A revenue expenditure is recorded in an expense account.

When interest is collected, it is debited to the Interest Revenue account and credited to

the Notes Receivable account.

A clothing store would logically have a higher inventory turnover rate than would a

doughnut shop.

General ledgers contain information about specific control accounts in the company’s

subsidiary ledger.

A revenue account is closed by debiting Income Summary and crediting Service

Revenue.

Marketable securities include investments in bonds and in the capital stocks of publicly

traded corporations.

Decision makers outside the organization base their credit decisions on weekly, or even

daily, financial statements.

A good standard cost system should always generate unfavorable variances.

An expenditure that benefits year one but is paid for in year two should not be recorded

until year two.

In a single-step income statement, all revenue items are listed, then all expense items

are combined and deducted from total revenue.

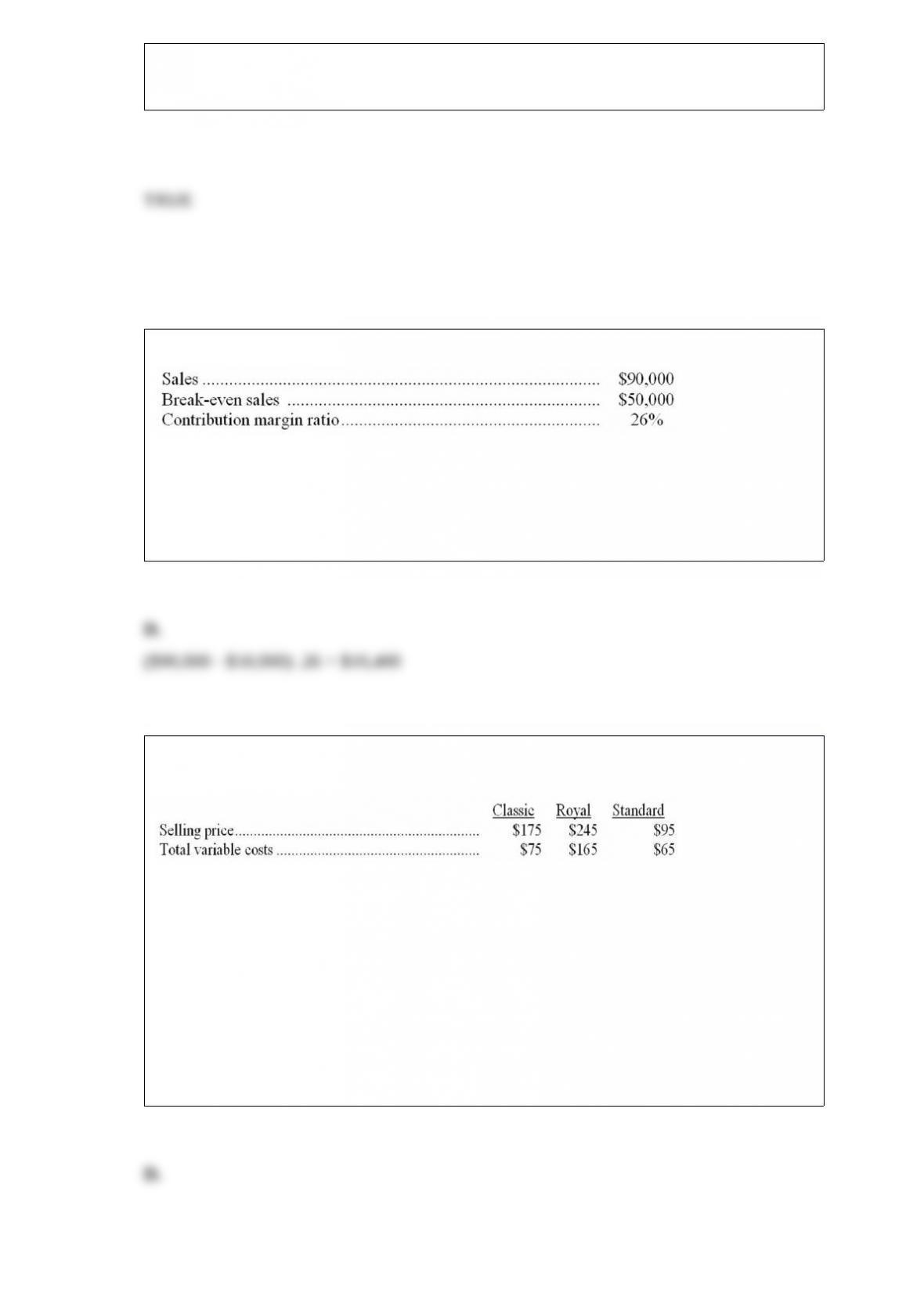

The following information is available:

What is the operating income?

A. $40,000.

B. $50,000.

C. $8,000.

D. $10,400.

Creative Star Corporation produces three lines of desks from wood: Classic, Royal, and

Standard. Cost and revenue data pertaining to each product are shown below:

Classic desks require five square yards of wood, Royal requires ten square yards, and

Standard requires three square yards. High demand for each product line far exceeds the

company’s production capacity.

Refer to the information above. If Creative Star Corporation has a limited supply of

wood available, which products should it produce?

A. Royal only.

B. Classic and Royal.

C. Royal and Standard.

D. Classic only.

Refer to the information above. If Capital Stock is $320,000, total assets of Braun

Corporation at December 31, 2014, amounts to:

A. $686,000.

B. $926,000.

C. $726,000.

D. $106,000.

A/P ($16,000) + N/P ($190,000) + Capital Stock ($320,000) + R.E. ($160,000) =

$686,000

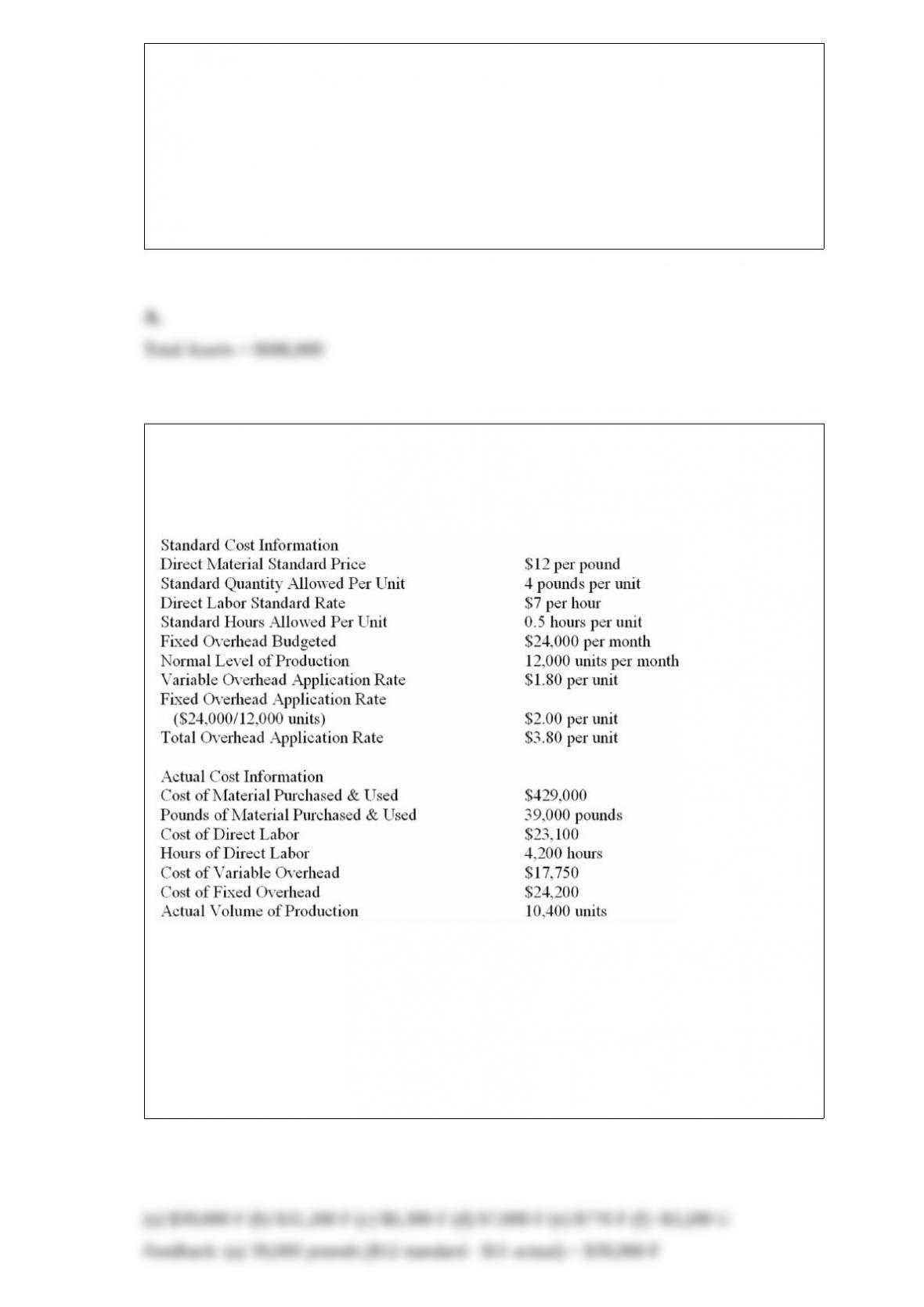

Standard cost systems variance computations

Livingston Corporation recently implemented a standard cost system. The company’s

cost accountant has provided the following data to perform a variance analysis for May:

Compute the following variances. Indicate whether each variance is favorable (F) or

unfavorable (U):

(a) Materials price variance: $__________

(b) Materials quantity variance: $__________

(c) Labor rate variance: $__________

(d) Labor efficiency variance: $__________

(e) Overhead spending variance: $__________

(f) Overhead volume variance: $__________

If the volume of output of a factory for the month of June is 50,000 units, while the

budgeted output was 40,000 units:

A. Comparison of budgeted results and actual results will be misleading unless the

company uses a flexible budget.

B. Actual fixed costs per unit may be expected to exceed budgeted levels.

C. Actual cost per unit will be higher than standard cost per unit.

D. Both total production costs and unit production costs should be approximately 25%

above budgeted levels.

Refer to the information above. On January 6, 2015, total liabilities are:

A. $901,000.

B. $579,000.

C. $1,399,000.

D. $1,721,000.

Steel Fabricating, Inc. manufactures furniture at its plants in Akron, Greensboro, and

Schenectady. The company prepares monthly income statements segmented by plant.

These income statements are organized to disclose contribution margin, performance

margin, and responsibility margin for each plant, in addition to operating income for the

company as a whole.

Refer to the information above. The Akron factory employs two quality control

inspectors at an annual salary of $70,000 each. These salaries should be classified as:

A. Common fixed cost.

B. Variable cost.

C. Committed fixed cost.

D. Controllable fixed cost.

If sales are $270,000, expenses are $220,000 and dividends are $30,000, Income

Summary:

A. Will have a credit balance of $50,000.

B. Will have a debit balance of $50,000.

C. Will have a debit balance of $20,000.

D. Will have a credit balance of $20,000.

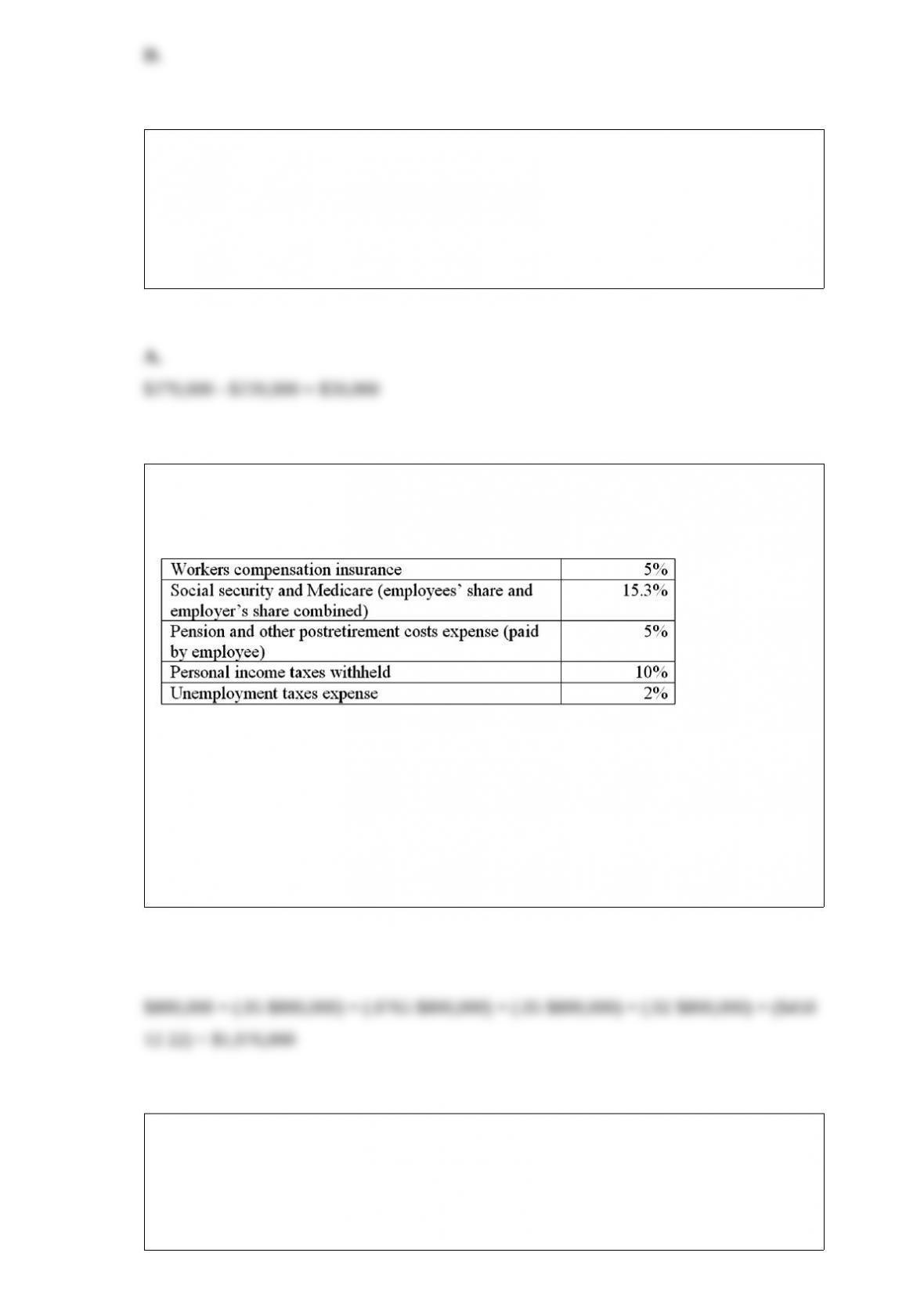

Rockland Corporation has 22 employees and incurs total wages and salaries expense of

$800,000 per year. The following table shows various payroll amounts as a percentage

of this annual wage and salaries expense:

In addition, Rockland provides group health insurance for its entire workforce. The cost

of this insurance is $450 per month for each employee.

Refer to the information above. The company’s annual payroll-related expenses amount

to approximately:

A. $1,137,200.

B. $1,076,000.

C. $980,000.

D. $800,000.

The contribution margin ratio is computed as:

A. Sales minus variable costs, divided by sales.

B. Fixed costs plus variable costs, divided by sales.

C. Sales minus fixed costs, divided by sales.

D. Sales divided by variable costs.

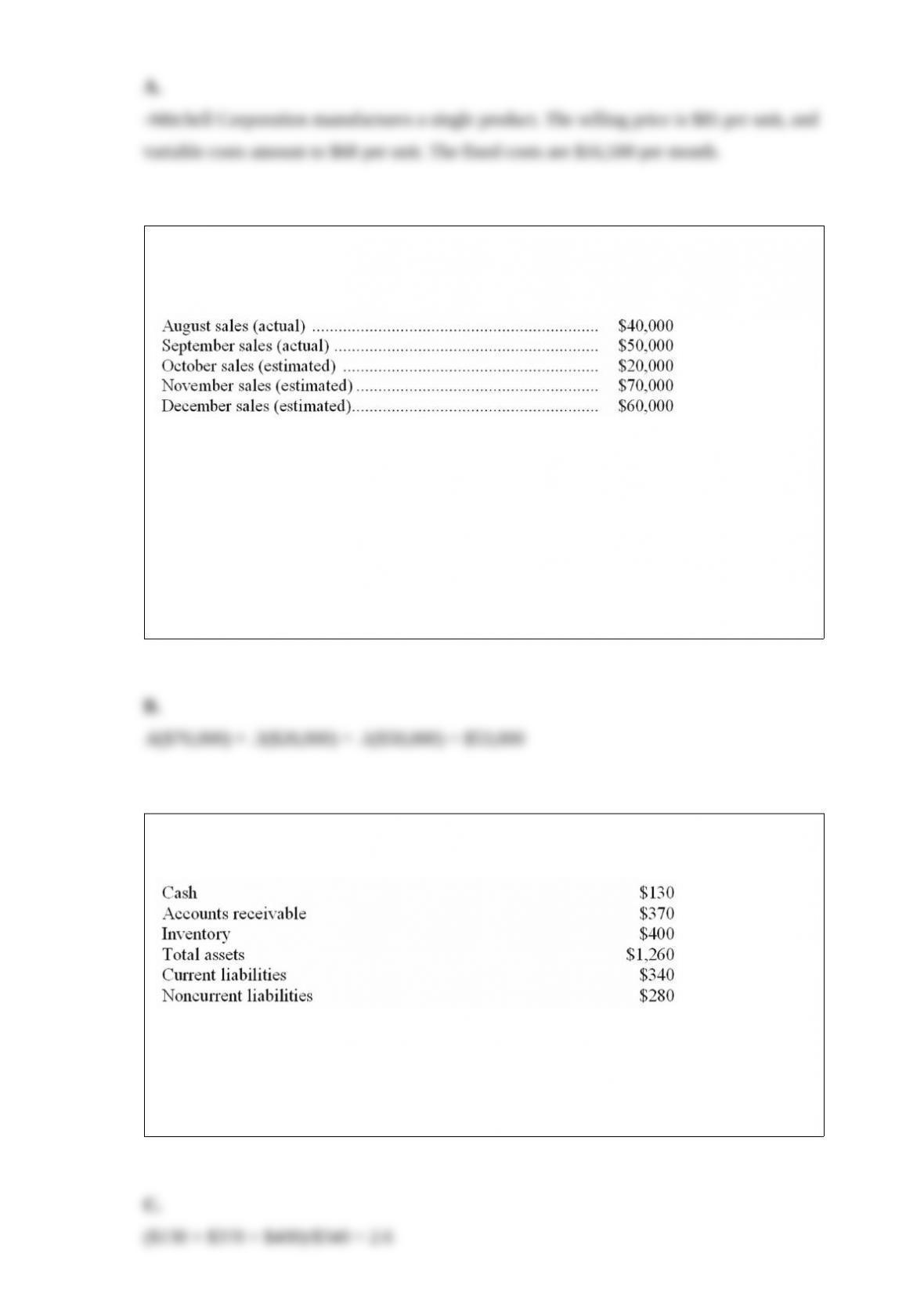

On October 1 of the current year, Molloy Corporation prepared a cash budget for

October, November, and December. All of Molloy’s sales are made on account. The

following information was used in preparing estimated cash collections:

Approximately 60% of all sales are collected in the month of the sale, 30% is collected

in the following month, and 10% is collected in the month thereafter.

Refer to the information above. Budgeted collections from customers in November

total:

A. $32,000.

B. $53,000.

C. $59,000.

D. $48,000.

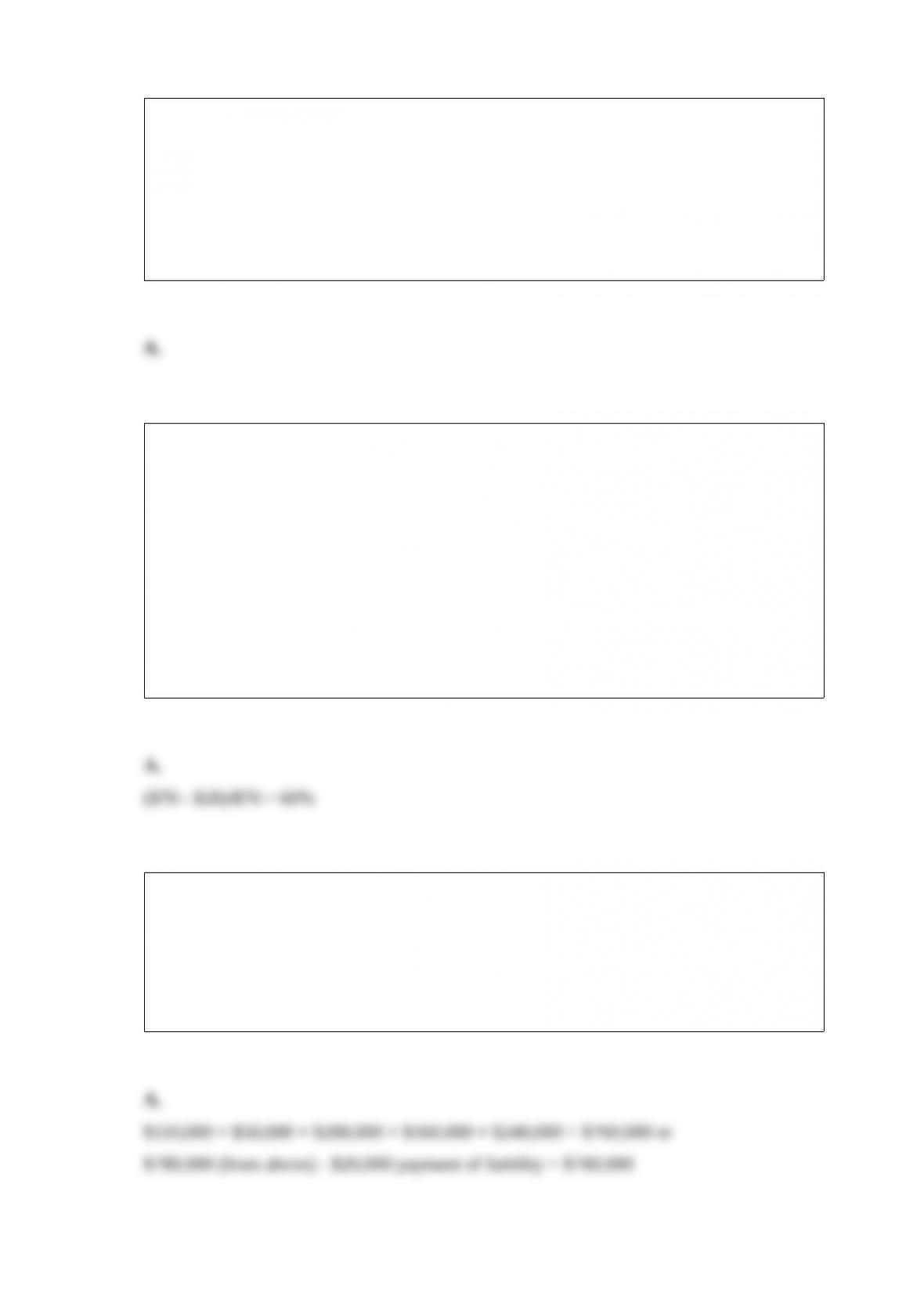

Shown below are selected data from the balance sheet of Bill’s Auto Parts, a retail store

(dollar amounts are in thousands):

Refer to the information above. What is the current ratio?

A. 1.2 to 1.

B. Less than 2 to 1, but not 1.2 to 1.

C. 2.6 to 1.

D. More than 2 to 1, but not 2.6 to 1.

The primary advantage of a just-in-time inventory system is:

A. The amount of money tied up in inventory is minimized.

B. Customers are afforded a wider selection of merchandise available for immediate

delivery.

C. The company is able to use the specific identification method of inventory pricing.

D. The risks of losing sales opportunities or of having to shut down manufacturing

operations because of inventory shortages are minimized.

Accents Associates sells only one product, with a current selling price of $70 per unit.

Variable costs are 40% of this selling price, and fixed costs are $12,000 per month.

Management has decided to reduce the selling price to $65 per unit in an effort to

increase sales. Assume that the cost of the product and fixed operating expenses are not

changed by this reduction in selling price.

Refer to the information above. At the current selling price of $70 per unit, the

contribution margin ratio is:

A. 60%.

B. 40%.

C. 67%.

D. 120%.

Refer to the information above. In a trial balance prepared at January 3, 2015, the total

of the debit column is:

A. $760,000.

B. $1,570,000.

C. $740,000.

D. $370,000.

Which of the following is generally not considered an external user of accounting

information?

A. Stockholders of a corporation.

B. Bank lending officers.

C. Financial analysts.

D. Factory managers.

Benefits derived from budgeting do not include:

A. Improved relationship with shareholders.

B. Enhanced management responsibilities.

C. Improved coordination of activities.

D. Enhanced performance evaluations.

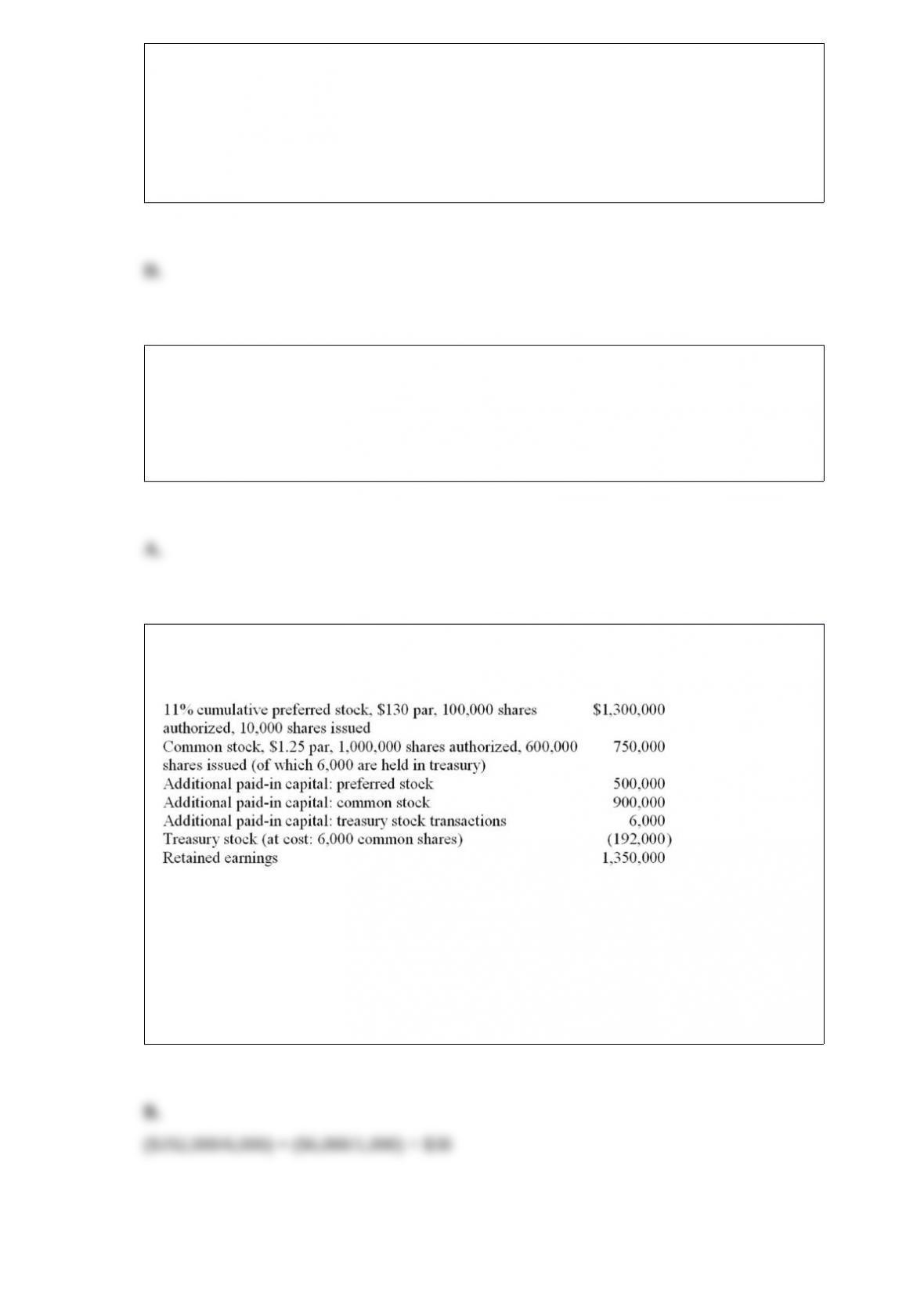

Shown below is information relating to the stockholders’ equity of Brookdale

Corporation at December 31, 2015:

Refer to the information above. If Brookdale Corporation had reacquired 7,000 shares

of treasury stock early in 2015, and this was the company’s only treasury stock

transaction, then some treasury stock must have been sold during 2015 for:

A. $32 per share.

B. $38 per share.

C. $27 per share.

D. $6 per share.

In the year-end financial statements, the Manufacturing Overhead account should have:

A. A debit balance, representing overhead on hand and available for use.

B. A credit balance, representing accumulated depreciation and amounts owed to

suppliers of overhead items.

C. Either a debit or a credit balance, depending upon whether the overhead application

rate used throughout the year was higher or lower than 100%.

D. A zero balance, since all overhead costs incurred during the period should have been

assigned to the production of the period.

At the end of the first year of operations, Meacham’s balance sheet showed the

following account balances: Accounts Receivable, $13,400; Inventory, $9,400; and

Accounts Payable, $14,650. The company’s income statement reports net income of

$37,400, including depreciation expense of $10,400. Using only the given information,

compute Meacham’s net cash flow from operating activities using the indirect method.

A. $65,250.

B. $39,650.

C. $24,350.

D. $26,650.

Sand, Inc. has outstanding $5,000,000, 10%, 20-year bonds. The bonds are callable at

104 on any interest date. The bonds were issued at par and mature in 10 years. Recently,

interest rates have declined to 5% and the market price of the bonds has increased to

107. If the company exercises the call provision, the company will record

A. A credit to cash of $5,350,000.

B. A loss of $200,000 on its income statement in the year the bonds are called.

C. A loss of $20,000 in the year the bonds are called and a $20,000 loss for the next 9

years.

D. A gain of $150,000 in the year the bonds are called.

Shares that have been sold and are in the hands of stockholders are called:

A. Outstanding.

B. Issued.

C. Treasury.

D. Underwritten.

The ending inventory of a merchandising company corresponds most closely to which

of the following amounts of a manufacturer?

A. Ending inventory of finished goods.

B. Cost of finished goods manufactured.

C. Ending inventory of work in process.

D. Total manufacturing costs incurred during the period.

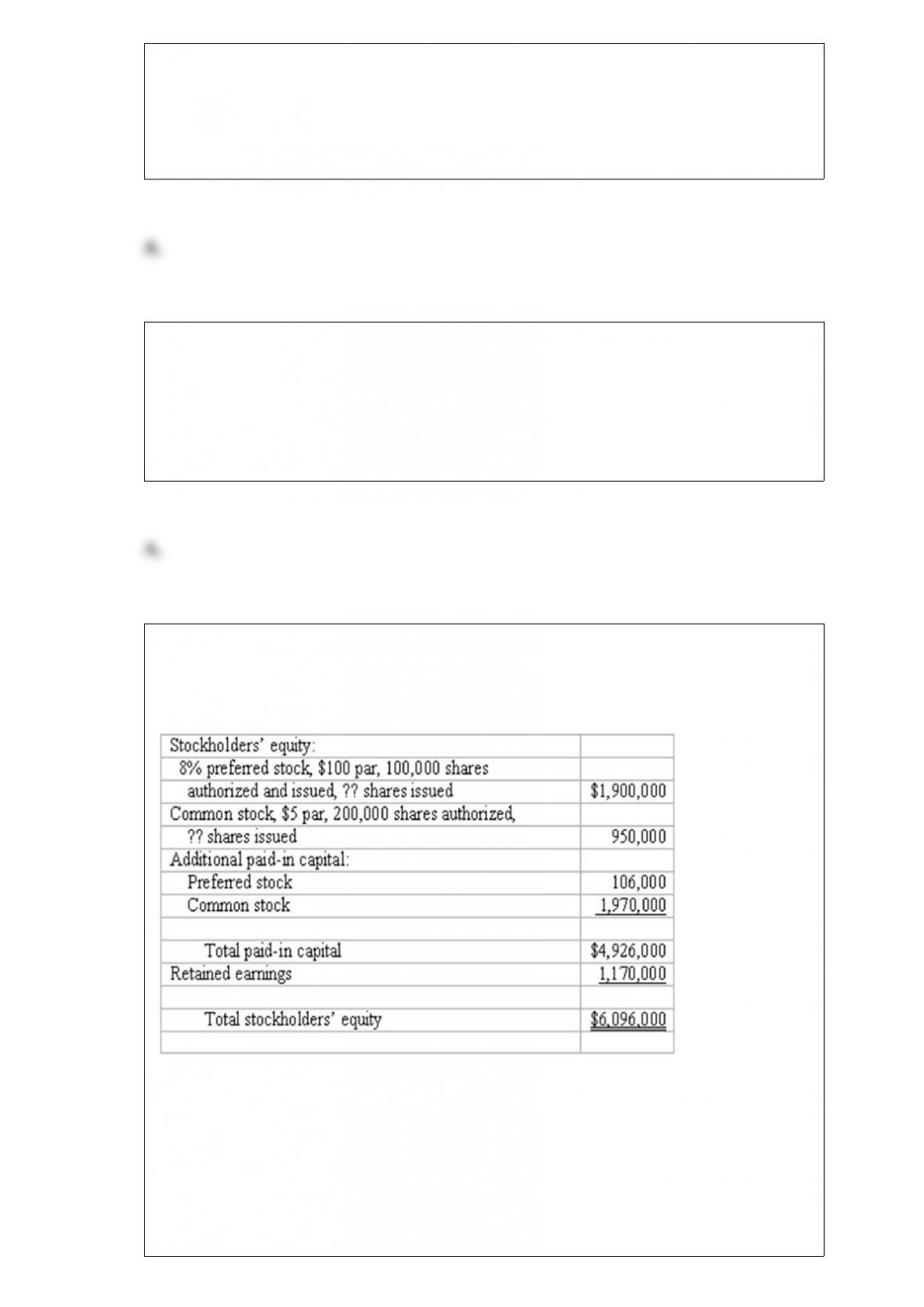

Interpreting stockholders’ equity section

The stockholders’ equity section of the balance sheet of Powell Corporation (with

certain details omitted) appears below:

Answer the following questions based on the stockholders’ equity section given above:

(a) What is the total amount of legal capital?

(b) What is the total amount of dividends paid annually to the preferred stockholders?

(c) What is the average issue price of a share of common stock?

(d) The balance in retained earnings at the beginning of the current year was

$1,351,500, and there were no dividends in arrears. Net income for the current year was

$700,000. What is the amount of the dividends declared on each share of common stock

during the current year?

Compound interest:

A. Is interest only on the principal amount for several years.

B. Is interest on the principal and previously earned interest.

C. Is interest only on previous interest excluding the principal.

D. Is equal to simple interest received for several years.

Sultan Company produces a single product. The selling price is $50 per unit, and

variable costs amount to $20 per unit. Sultan’s fixed costs per month total $80,000.

Refer to the information above. What will be the monthly margin of safety (in dollars)

if 3,000 units are sold each month? (Rounded)

A. $16,667.

B. $100,000.

C. $43,333.

D. $150,000.

The normal balance of the Accumulated Depreciation account is:

A. A debit balance.

B. A credit balance.

C. Either a debit balance or a credit balance.

D. There is no normal balance for this account.

An accelerated depreciation method:

A. Results in reporting higher earnings every year.

B. Depreciates an asset over a shorter life than does the straight-line method.

C. Recognizes more depreciation expense in the early years of an asset’s useful life and

less in the later years.

D. Is required for assets that become technologically obsolete before they physically

wear out.

Gamma Company adjusts its accounts at the end of each month. The following

information has been assembled in order to prepare the required adjusting entries at

December 31:

(1) A one-year bank loan of $720,000 at an annual interest rate of 6% had been obtained

on December 1.

(2) The company’s pays all employees up-to-date each Friday. Since December 31 fell

on Tuesday, there was a liability to employees at December 31 for two day’s pay.

Employees earn a total of $12,800 per week.

(3) On December 1, rent on the office building had been paid for three months. The

monthly rent is $7,000.

(4) Depreciation of office equipment is based on an estimated useful life of five years.

The balance in the Office Equipment account is $12,360; no change has occurred in the

account during the year.

(5) All fees totaling $19,800 were earned during the month for clients who had paid in

advance.

Refer to the information above. How much is owed the employees for their wages?

A. $0

B. $2,560

C. $5,120

D. $12,800

A journal entry to record revenue could include each of the following, except:

A. A credit to a revenue account.

B. A credit to the Capital Stock account.

C. A debit to Cash.

D. A debit to Accounts Receivable.

Sultan Company produces a single product. The selling price is $50 per unit, and

variable costs amount to $20 per unit. Sultan’s fixed costs per month total $80,000.

Refer to the information above. What is the contribution margin ratio of Sultan’s

product?

A. 25%.

B. 75%.

C. 60%.

D. 40%.

On January 1, 2015, Juniper Corporation issued 60,000 shares of its total 200,000

authorized shares of $4 par value common stock for $8 per share. On December 31,

2015, Juniper Corporation’s common stock is trading at $12 per share.

Refer to the information above. Assuming Juniper Corporation did not issue any more

common stock in 2015, how does the increase in value of its outstanding stock affect

Juniper?

A. Juniper should recognize additional net income for 2015 of $4 per share, or

$240,000.

B. Paid-in capital at December 31, 2015, is $720,000 (i.e., 60,000 shares times $12 per

share).

C. This increase in market value of outstanding stock is not recorded in the financial

statements of Juniper Corporation.

D. Each shareholder must pay an additional $4 per share to Jupiter.

Which of the following is not a user of internal accounting information?

A. Store manager

B. Chief executive officer

C. Creditor

D. Chief financial officer

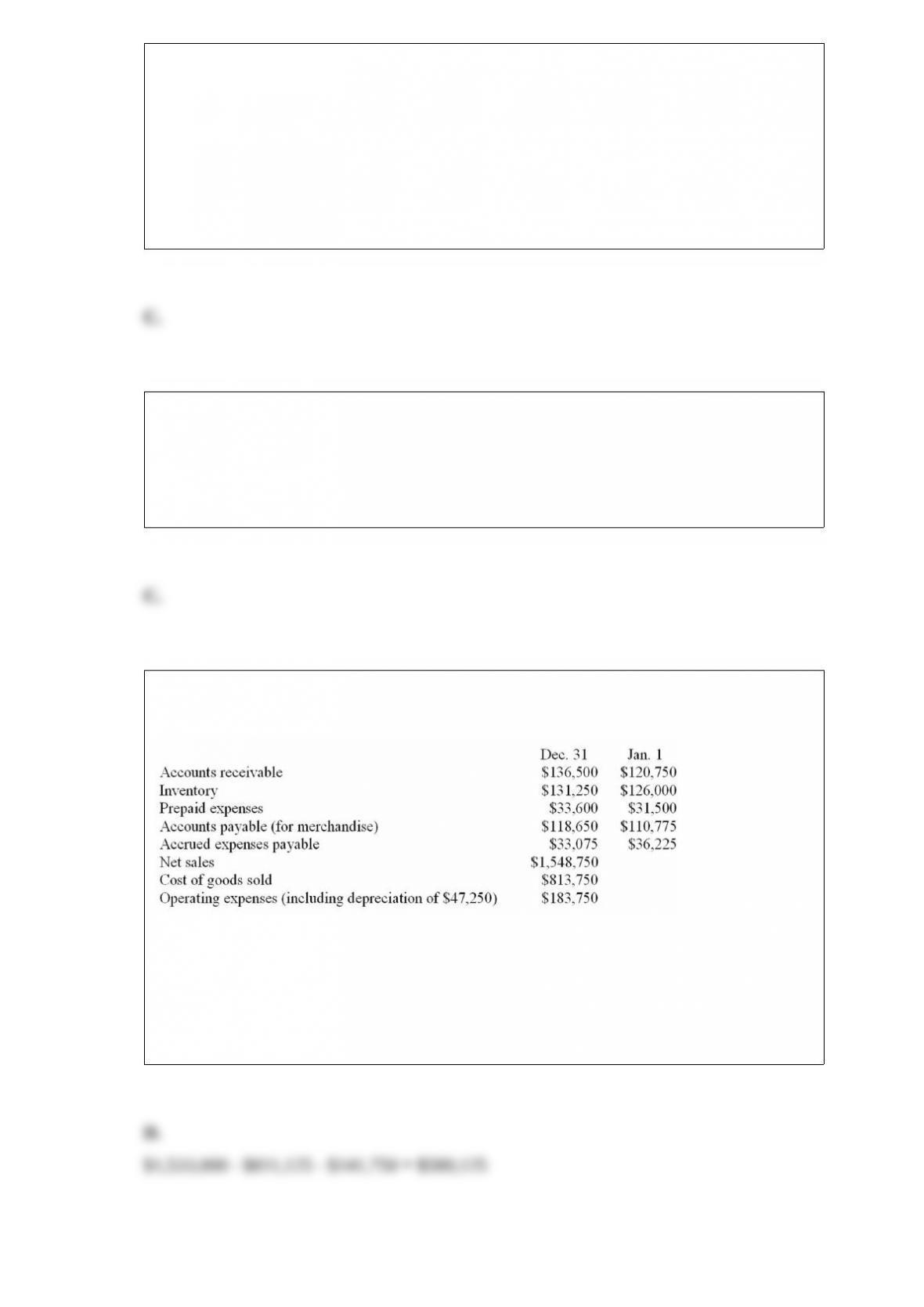

The financial statements of York, Inc., provide the following information for the current

year:

Refer to the information above. Net cash flow from operating activities for the current

year is:

A. $595,875.

B. $596,400.

C. $556,500.

D. $580,125.