Which of the following factors most likely would cause a CPA to decide not to accept a

new audit engagement?

A. The CPA’s lack of understanding of the prospective client’s internal auditor’s

computer-assisted audit techniques.

B. Management’s disregard of its responsibility to maintain an adequate control

environment.

C. The CPA’s inability to determine whether related party transactions were

consummated on terms equivalent to arm’s-length transactions.

D. Management’s refusal to permit the CPA to perform substantive procedures before

the year-end.

A product cost is

A. an expense allocated by a systematic procedure.

B. recognized during the period in which a liability is incurred.

C. recognized in the period during which related revenue is recognized.

D. recognized in the period in which cash is spent.

During its fiscal year, a company issued, at a discount, a substantial amount of bonds.

When performing audit work in connection with the bond issue, the independent auditor

should

A. confirm the existence of the bond holders.

B. review the board of directors’ minutes for authorization.

C. trace the net cash received from the issuance to the bond payable account.

D. inspect the records maintained by the bond trustee.

Which of the following statements ordinarily is included among the written

management representations obtained by the auditor?

A. Compensating balances and other arrangements involving restrictions on cash

balances have been disclosed.

B. Management acknowledges responsibility for illegal actions committed by

employees.

C. Sufficient evidential matter has been made available to permit the issuance of an

unqualified opinion.

D. Management acknowledges that there are no material weaknesses in the account

balances.

Audit sampling is not used for which type of audit evidence?

A. Inquiry.

B. Inspection of tangible assets.

C. Reperformance.

D. Confirmation.

Which of the following is not a misstatement of the financial statements?

A. The entity uses different inventory accounting methods for internal and external

reporting.

B. A departure from GAAP.

C. The footnote for pensions is omitted.

D. A clerk incorrectly based the allowance for doubtful accounts on 31% of sales as

opposed to 13% of sales as determined by the controller.

An auditor is required to establish an understanding with a client regarding the

responsibilities for each engagement. This understanding generally includes

A. Management’s responsibility to guarantee that there are no material misstatements

due to fraud.

B. The auditor’s responsibility to plan and perform the audit to provide reasonable, but

not absolute, assurance of detecting material errors or fraud.

C. Management’s responsibility for providing the auditor with an assessment of the risk

of material misstatement due to fraud.

D. The auditor’s responsibility for the fairness of the financial statements.

Which of the following is not an audit procedure that is commonly used in performing

tests of controls?

A. Inquiring.

B. Observing.

C. Confirming.

D. Inspecting.

The auditor notices significant fluctuations in key elements of the company’s financial

statements. If management is unable to provide an acceptable explanation, the auditor

should

A. Consider the matter a scope limitation.

B. Perform additional audit procedures to investigate the matter further.

C. Intensify the examination with the expectation of detecting management fraud.

D. Withdraw from the engagement.

Which of the following statements best describes why the profession of certified public

accountants has deemed it essential to promulgate a code of conduct and to establish a

mechanism for enforcing observance of the code?

A. Ethical standards are established so that users of accounting services know what to

expect, the professionals know what behaviors are acceptable, and overseers can take

disciplinary action when appropriate.

B. A prerequisite to success is the establishment of an ethical code that stresses

primarily the professional’s responsibility to clients and colleagues.

C. A requirement of most state laws calls for the profession to establish a code of

conduct.

D. An essential means of self-protection for the profession is the establishment of

flexible ethical standards by the profession.

Which of the following is not within the class of foreseen users of an accountant’s work

product?

A. A prospective shareholder of the client.

B. A lender bank when the accountant knows only that the client will use the financial

statements to obtain a loan from an unspecified source.

C. A bank when the accountant knows the client will rely on the financial statements as

the basis for a loan from the bank.

D. An investor if the accountant knows that the client is seeking capital from a select

group of investors.

In the context of an audit of financial statements, substantive procedures are audit

procedures that

A. May be eliminated under certain conditions.

B. Are primarily designed to discover significant subsequent events.

C. May be either tests of details of transactions, tests of details of account balances, or

analytical procedures.

D. Will increase proportionately with an increase in the auditor’s reliance on internal

control.

Substantive procedures to examine the completeness assertion for accounts payable

include

A. selecting a sample of vouchers and agreeing them to authorized purchase orders.

B. selecting a sample of vouchers and tracing them to the purchases journal.

C. comparing dates on vouchers to dates in the purchases journal.

D. recomputing the mathematical accuracy of a sample of vendor invoices.

An auditor’s decision concerning whether or not to “dual date” the audit report is based

upon the auditor’s willingness to

A. extend auditing procedures.

B. accept responsibility for all events between year-end and the audit report date.

C. permit inclusion of a footnote captioned: event (unaudited) subsequent to the date of

the auditor’s report.

D. assume responsibility for events subsequent to the issuance of the auditor’s report.

An auditor performs a test to determine whether all merchandise was received for

which the entity was billed. The population for this test consists of all

A. merchandise received.

B. vendors’ invoices.

C. canceled checks.

D. receiving reports.

According to the ethical standards of the profession, which of the following acts is

generally prohibited?

A. Purchasing a product from a third party and reselling it to a client.

B. Writing a financial management newsletter promoted and sold by a publishing

company.

C. Accepting a commission for recommending a product to an audit client.

D. Accepting engagements obtained through the efforts of third parties.

An independent auditor finds that Holdaway Corporation occupies office space, at no

charge, in an office building owned by a shareholder. This finding likely indicates the

existence of

A. Management fraud.

B. Related party transactions.

C. Window dressing.

D. Weak internal control.

A substantive strategy is typically used to audit stockholders’ equity because

A. the number of transactions is small.

B. controls over stockholders’ equity transactions typically are weak.

C. a reliance strategy is most efficient.

D. a substantive strategy likely was used in prior years.

A written understanding between the auditor and the client concerning the auditor’s

responsibility for the discovery of illegal acts is usually set forth in a(n)

A. Client representation letter.

B. Letter of audit inquiry.

C. Management letter.

D. Engagement letter.

Which of the generally accepted auditing standards of reporting would not normally

apply to special reports such as cash basis statements?

A. First standard.

B. Second standard.

C. Third standard.

D. Fourth standard.

If payables turnover has increased significantly since the prior year, this is an indication

that which of the following assertions for accounts payable might be violated?

A. Existence or occurrence.

B. Completeness.

C. Rights and obligations.

D. Valuation and allocation.

Analytical procedures enable the auditor to predict the balance or quantity of an item

under audit. Information to develop this estimate can be obtained from all of the

following except:

A. Tracing transactions through the system to determine whether procedures are being

applied as prescribed.

B. Comparison of financial data with data for comparable prior periods, anticipated

results (e.g., budgets and forecasts) and similar data for the industry in which the entity

operates.

C. Study of the relationships of elements of financial data that would be expected to

conform to a predictable pattern based upon the entity’s experience.

D. Study of the relationships of financial data with relevant nonfinancial data.

In attributes sampling, a 10% change in which of the following factors normally will

have the least effect on the size of a statistical sample?

A. Population size.

B. Tolerable deviation rate.

C. Expected population deviation rate.

D. Standard deviation.

Auditors may use positive and/or negative forms of confirmation requests for accounts

receivable. Which of the following statements is true regarding the auditor’s use of

confirmations?

A. The positive confirmation form must always be used to confirm all balances

regardless of size.

B. A combination of the two confirmation types can be used, with the positive form

used for large balances and the negative form used for small balances.

C. A combination of the two confirmation types can be used, with the positive form

used for trade receivables and the negative form for other receivables.

D. The positive confirmation form should be used when controls related to receivables

are satisfactory and the negative confirmation form should be used when controls

related to receivables are unsatisfactory.

For a practitioner to examine management’s assertions about the effectiveness of

internal controls, all of the following conditions are necessary except:

A. Sufficient competent evidence can be developed to support the evaluation.

B. The practitioner must have already concluded that the financial statements are fairly

presented in accordance with the applicable accounting framework.

C. The entity’s management accepts responsibility for the effectiveness of its internal

control.

D. All of the conditions listed are necessary.

Which element(s) is/are pervasive to the application of generally accepted auditing

standards, particularly the standards of fieldwork and reporting?

A. The elements of materiality and audit risk.

B. The element of internal control.

C. The element of corroborating evidence.

D. The element of reasonable assurance.

Which of the following sample planning factors would influence the sample size for a

substantive test of details for a specific account?

A. Expected amount of misstatement but not the measure of tolerable misstatement.

B. Expected amount of misstatement and the measure of tolerable misstatement.

C. Measure of tolerable misstatement but not the expected amount of misstatement.

D. Neither the expected amount of misstatement nor the measure of tolerable

misstatement.

Ritz Corporation wished to acquire the stock of Stale, Inc. In conjunction with its plan

of acquisition, Ritz hired Fein, CPA, to audit the financial statements of Stale. Based on

the audited financial statements and Fein’s unqualified opinion, Ritz acquired Stale.

Within 6 months, it was discovered that the inventory of Stale had been overstated by

$500,000. Ritz commenced an action against Fein. Ritz believes that Fein failed to

exercise the knowledge, skill, and judgment commonly possessed by CPAs in the

locality, but is not able to prove that Fein either intentionally deceived it or showed a

reckless disregard for the truth. Ritz also is unable to prove that Fein had any

knowledge that the inventory was overstated. Which of the following two causes of

action would provide Ritz with proper bases upon which Ritz would most likely

prevail?

A. Negligence and breach of contract.

B. Negligence and gross negligence.

C. Negligence and fraud.

D. Gross negligence and breach of contract.

All of the following can assist the auditor in testing the existence assertion for

investment securities except:

A. physical examination.

B. comparing fair value to cost.

C. confirmation with the issuer.

D. confirmation with the custodian.

Which of the following is the best audit procedure for the discovery of damaged

merchandise in an entity’s ending inventory?

A. Compare the physical quantities of slow-moving items with corresponding quantities

of the prior year.

B. Observe the condition of merchandise and raw materials during the entity’s physical

inventory count.

C. Review the management’s inventory representation letter for accuracy.

D. Test overall fairness of inventory values by comparing the company’s turnover ratio

with the industry average.

In regards to the Foreign Corrupt Practices Act (FCPA), external auditors

A. are responsible for ensuring that sufficient internal controls are maintained.

B. should immediately report any discovered violation of the FCPA to the client’s

management.

C. should verify compliance with corporate codes of conduct.

D. are not subject to any penalties.

Which of the following is not an aspect of the assurances provided by a CPA WebTrust

report?

A. Product or service quality.

B. System availability.

C. Confidentiality.

D. Processing integrity.

Often in an audit, total combined tolerable misstatement is greater than overall

materiality. Why is this the case?

Auditors can usually gather sufficient, competent evidence on prepaid insurance by

performing substantive analytical procedures. Why is this?

The audit testing hierarchy is considered to be more effective and more efficient. Why?

The XYZ Company billing department has decided to assign one employee to each of

its customers. This employee will be responsible for granting credit to the entity and

then handling the billing. XYZ believes this will result in better customer service,

because the entity will only have to deal with one person and that one person will be

very familiar with the credit terms. As an auditor, would you agree with XYZ’s

decision?

For each of the following substantive procedures, first note whether it is a test of details

of transactions or a test of details of account balances. Then decide for which assertion

the test provides the best evidence.

1) Trace large cash receipts and payments to the source documents and the general

ledger.

2) Examine copies of note and bond agreements.

3) Recompute accrued interest payable.

4) Review debt activity for a few days before and after year-end to determine whether

transactions are included in the proper period.

5) Examine due dates on notes and bonds for proper classification between current and

long term debt.

Property, plant, and equipment is often a significant portion of a company’s assets.

Describe the inherent risk factors that can affect the audit of this account.

Discuss the new IAASB reporting standards for “listed” (public) entities which are

effective for financial periods ending after December 15, 2016.

Auditors can be held liable under two classes of law when sued by clients, investors,

creditors, or the government. Identify and briefly explain both classes of law.

In terms of an audit, define substantive strategy and reliance strategy. Include in your

definition how the different strategies relate to internal control. Which strategy would

best relate to a lower control risk?

Identify whether the following tests are tests of controls, substantive analytical

procedures, tests of details of transactions, or tests of details of account balances.

1) Select a sample of customer receivables and send positive confirmations to each

customer.

2) Examine monthly bank reconciliations for the internal auditors’ initials indicating

internal verification and review of the reconciliation.

3) Select a sample of entries in the sales journal and trace each to the shipping

documents.

4) Compute receivable turnover and compare with previous years.

5) For a sample of new customers, determine whether credit approval was properly

administered and documented.

6) Compare the dates on a sample of sales invoices with the dates of shipment and the

dates the transactions were recorded in the sales journal.

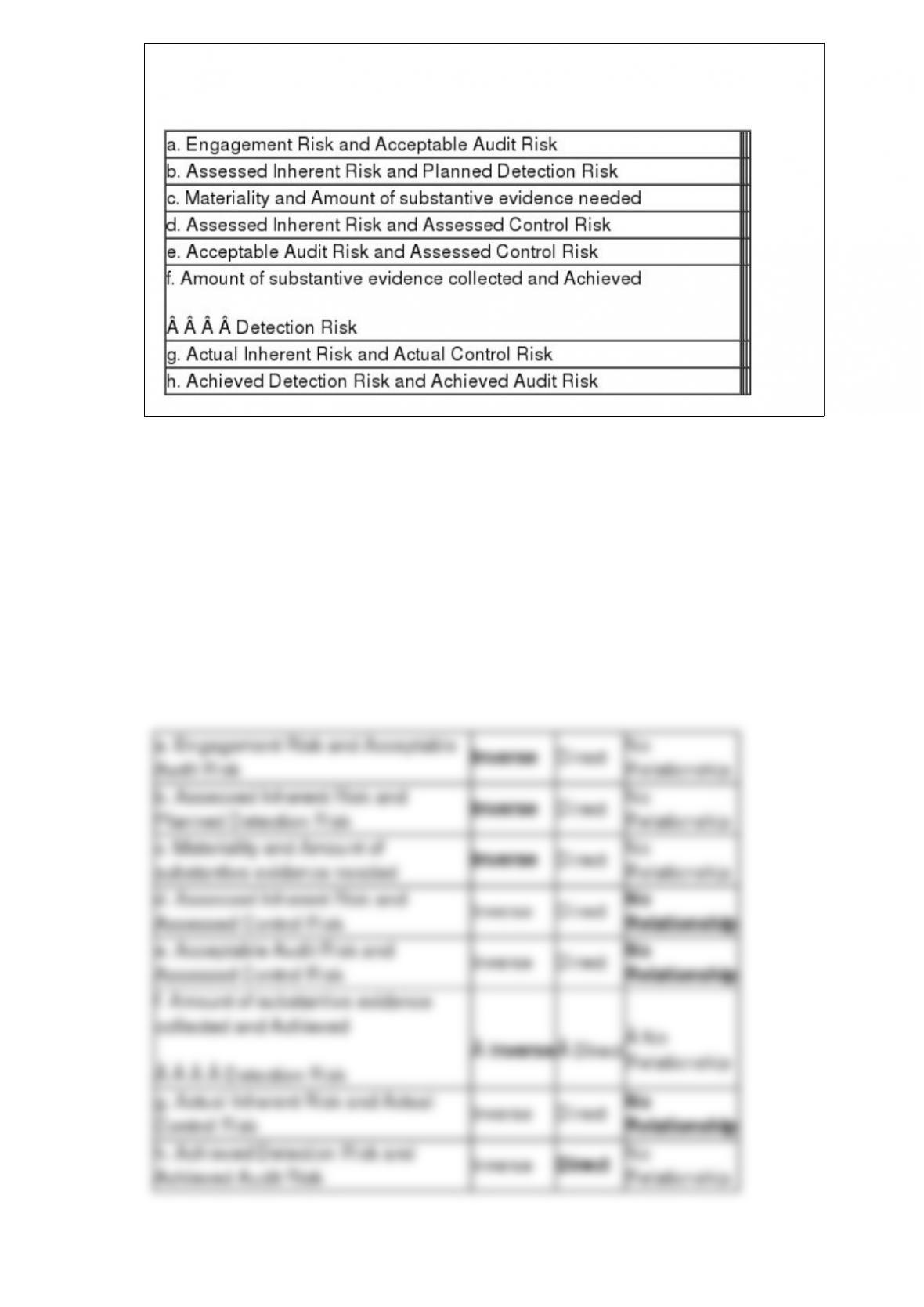

Using the audit risk model, identify the relationship between the following elements.

For each of the items below, highlight whether the two elements have an inverse

relationship, a direct relationship, or no relationship. When considering each item,

assume that the other components of the risk model remain constant.

What tests do auditors typically perform on a lead schedule for property, plant, and

equipment and what assertion are they testing?

Define corporate governance, the board of directors, and the audit committee and

explain how they relate to each other.

Changes in an entity’s accounting choices either affect “consistency” in the application

of GAAP or they do not. For each item listed below, state whether the item affects

consistency and identify the effect the change will have on the audit report.

1) Change in accounting estimate.

2) Correction of an error in principle.

3) Change in reporting entity.

4) Correction of an error that does not involve an accounting principle.

5) Change in accounting principle.

6) Change in classification and reclassification.

When auditing accounts payable using classical variables sampling, Sue finds evidence

indicating that the account may be materially misstated. What are Sue’s options?

The Hamster Stop has $93,650 in the Accrued Payroll account. Hamster’s weekly

payroll is $156,000 and the accrual represents payroll for 3 days. If controls are strong,

determine whether additional audit work should be performed on this account.

List five things an auditor should do during the observation of the physical count of

inventory.

As with most professionals, internal auditors must follow guidelines promoting ethical

conduct. The IIA Code of Ethics is important for internal auditors because the reliability

of their work depends on a reputation for a high level of personal integrity. The Code of

Ethics consists of four main principles of ethical conduct and some associated rules that

underpin the expected conduct of IIA members. List the four main principles of the

Code of Ethics and explain each.

BDK Accounting is auditing a new client, A La Carte Catering. BDK could save audit

time by using work from A La Carte’s internal audit staff. The staff consists of three

accountants with public accounting experience and certification. A La Carte requires

every member of its accounting department to spend two out of every five years on the

internal audit staff. Then, the employee is rotated back into the accounting department

for a couple of years. What factors should BDK consider when determining whether or

not it can use work of the internal audit staff? In this case, what should BDK decide?

Assume an account receivable confirmation is returned with a note to the auditor

describing a difference between your client’s records and the customer’s records.

Clearly describe below two potential non-misstatement timing differences that could

cause a discrepancy between a client’s receivable records and his/her customer’s

records. The timing differences you describe should be such that after investigation you

would determine that your client’s receivable balance is not misstated due to these

differences.