Paul Company had 100,000 shares of common stock outstanding on January 1, 2016.

On September 30, 2016, Paul sold 48,000 shares of common stock for cash. Paul also

had 10,000 shares of convertible preferred stock outstanding throughout 2016. The

preferred stock is $100 par, 6%, and is convertible into 3 shares of common for each

share of preferred. Paul also had 500, 8%, convertible bonds outstanding throughout

2016. Each $1,000 bond is convertible into 30 shares of common stock. The bonds sold

originally at face value. Reported net income for 2016 was $300,000 with a 40% tax

rate. Common shareholders received $2 per share dividends after preferred dividends

were paid in 2016.

Required:

Compute basic and diluted earnings per share (rounded to 2 decimal places) for 2016.

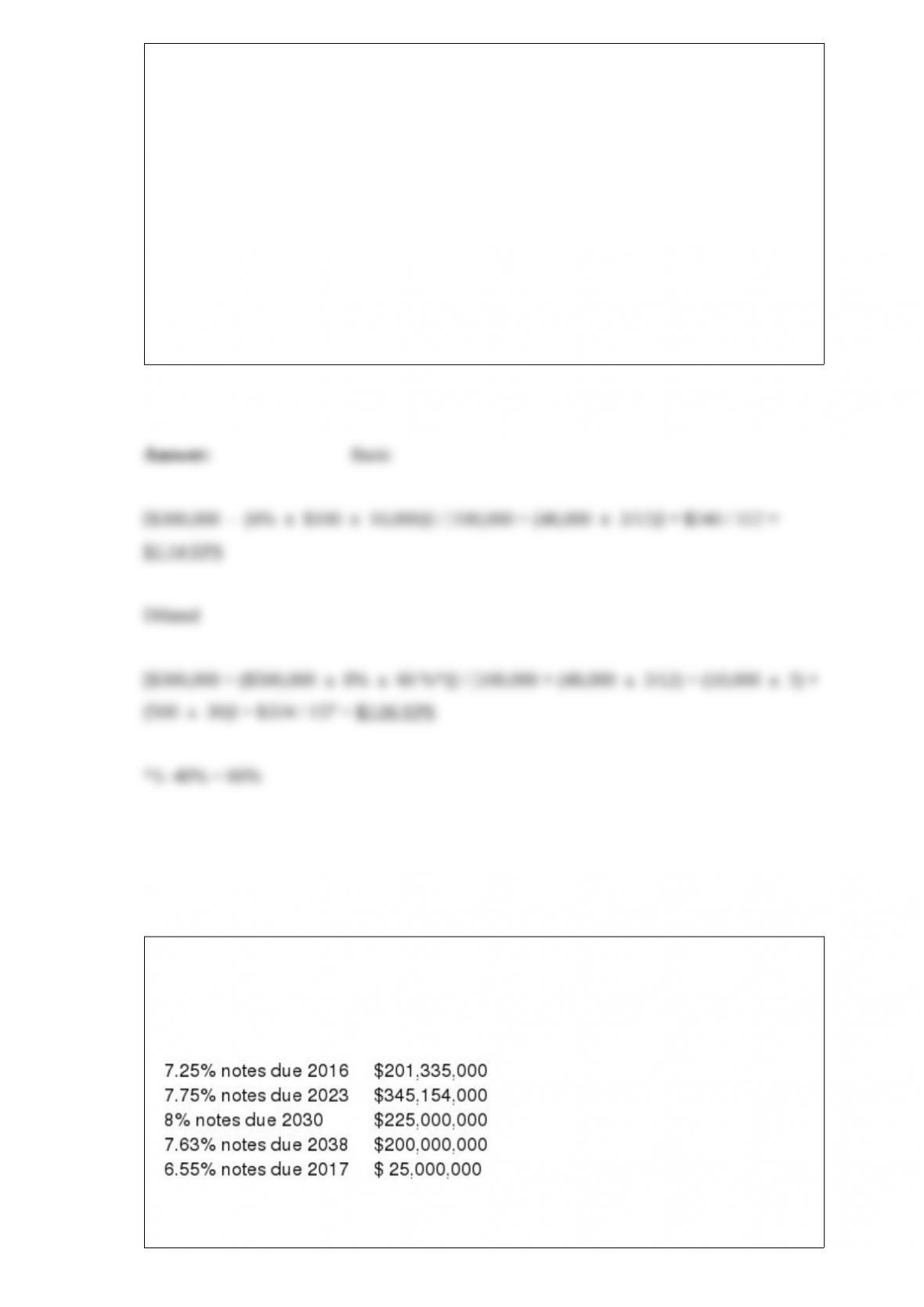

The note about debt included in the financial statements of Healdsburg Company for

the year ended December 31, 2015 disclosed the following: Debt. The following table

summarizes the long-term debt of the Company at December 31, 2015. All of the notes

were issued at their face (maturity) value.

Required: Assuming that the notes pay interest annually and mature on December 31

of the respective years, compute the following: Suppose that Healdsburg renegotiates

the 8% notes on December 31, 2021, when the going interest rate is 8%. Healdsburg

agrees to make 12 equal annual installments, commencing on December 31, 2022,

rather than pay the annual interest payments and the $225 million in a lump sum at

maturity. What would the annual payments be?

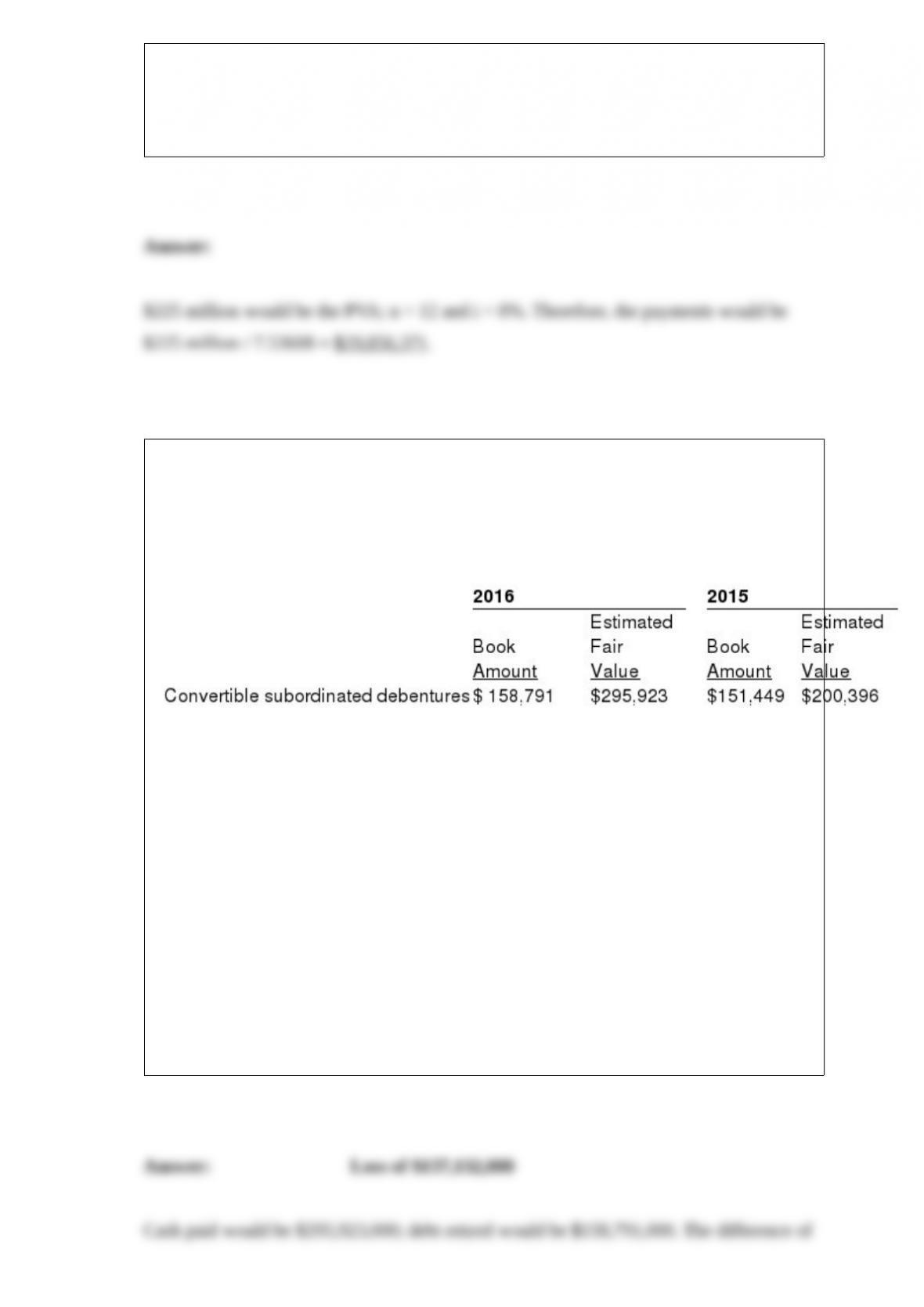

In its 2016 annual report to shareholders, Health Foods, Inc., disclosed the following

information about some of its indebtedness: The fair value of convertible subordinated

debentures is estimated using quoted market prices. Book amounts and estimated fair

values of our financial instruments other than those for which book amounts

approximate fair values as noted above are as follows (in thousands)

In addition, the company disclosed the following: We have outstanding zero coupon

convertible subordinated debentures which had a book amount of approximately $158.8

million and $151.4 million at September 26, 2016, and September 28, 2015,

respectively. The debentures have an effective yield to maturity of 5 percent and a

principal amount at maturity on March 2, 2030, of approximately $308.8 million. The

debentures are convertible at the option of the holder, at any time on or prior to

maturity, unless previously redeemed or otherwise purchased. The debentures have a

conversion rate of 10.64 shares per $1,000 principal amount at maturity, representing

3,285,632 shares. The debentures may be redeemed at the option of the holder on

March 2, 2020, or March 2, 2025, at the issue price plus accrued original discount

totaling approximately $188 million and $241 million, respectively.

Required: Determine the gain or loss that Health Foods would have reported in its

2016 income statement if it had redeemed (and retired) the debentures at fair value at

the end of the fiscal year.

Chapter 15 Leases

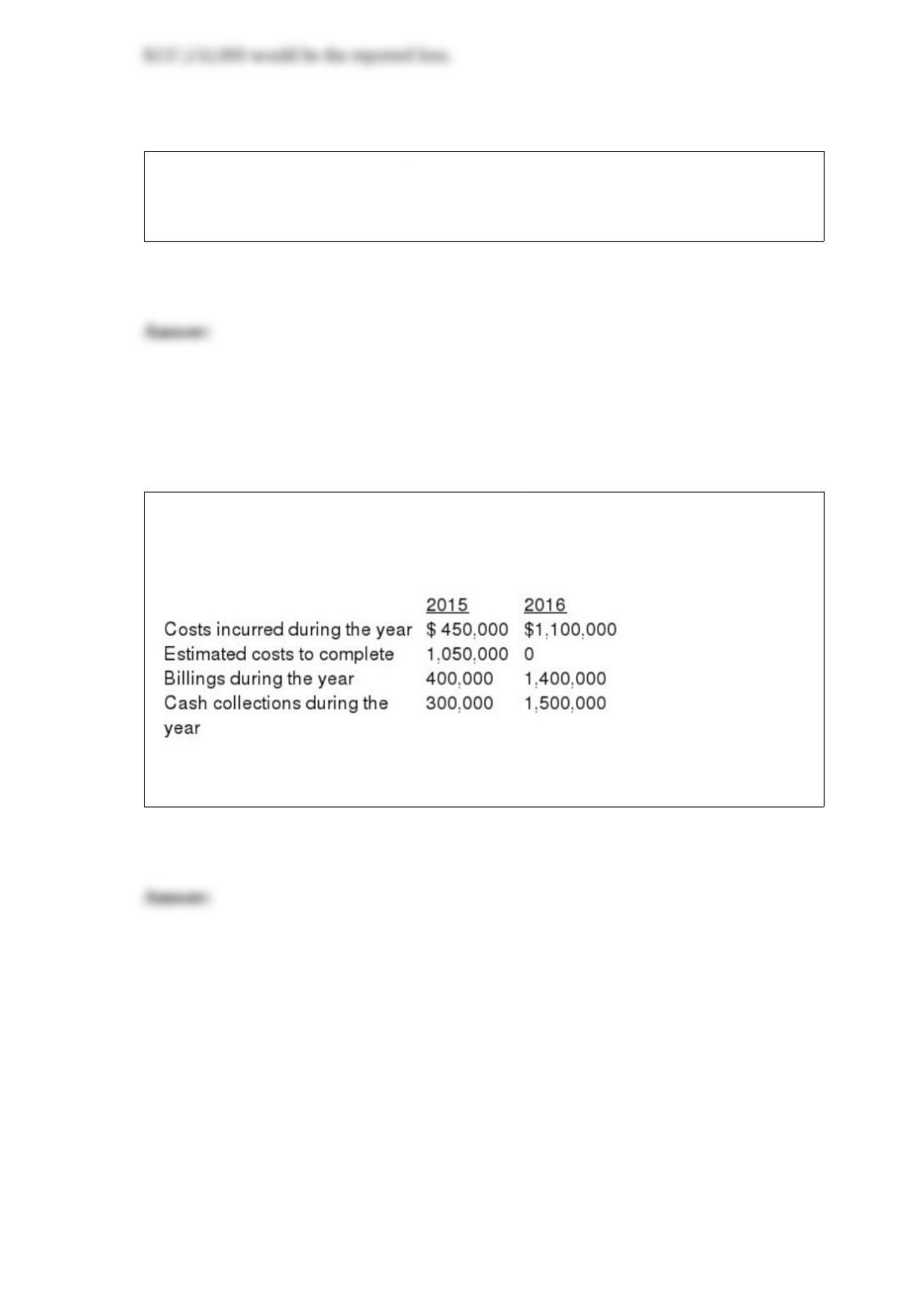

Beavis Construction Company was the low bidder on a construction project to build an

earthen dam for $1,800,000. The project was begun in 2015 and completed in 2016.

Cost and other data are presented below:

Assume that Beavis recognizes revenue upon completion of the project. Required:

Prepare all journal entries to record costs, billings, collections, and profit recognition.