1) On December 31, 2010, Parminter Corporation owns an 80% interest in the common

stock of Sanchez Corporation and an 80% interest in Sanchez’s preferred stock. On

December 31, 2010, Sanchez’s stockholders’ equity was as follows:

10% preferred stock, cumulative, $10 par value $50,000

Common stock350,000

Retained earnings100,000

Total stockholders’ equity$500,000

On December 31, 2010, preferred dividends are not in arrears. Sanchez had 2011 net

income of $30,000 and only preferred dividends are declared and paid in 2011 . There

are no book value/fair value differentials associated with Parminter’s investments.

What should be the noncontrolling interest share, preferred in the consolidated financial

statements of Parminter for the year ending December 31, 2011?

A) $1,000

B) $2,000

C) $4,000

D) $5,000

2) Pasfield Corporation acquired a 90% interest in Santini Corporation for $90,000 cash

on January 1, 2011 . The following information is available for Santini at that time.

Book ValueFair ValueDifference

Current assets$40,000$50,000$10,000

Plant assets60,00075,00015,000

Liabilities(50,000)(50,000)0

Net assets$50,000$75,000

Under the entity theory, a consolidated balance sheet prepared immediately after the

business combination will show noncontrolling interest of

A) $5,000

B) $7,500

C) $9,000

D) $10,000

3) Bower Corporation purchased a 70% interest in Stage Corporation on June 1, 2010 at

a purchase price of $350,000. On June 1, 2010, the book values of Stage’s assets and

liabilities were equal to fair values. On June 1, 2010, Stage’s stockholders’ equity

consisted of $290,000 of Common Stock and $210,000 of Retained Earnings. All

cost-book differentials were attributed to goodwill.

During 2010, Stage earned $120,000 of net income, earned uniformly throughout the

year and paid $6,000 of dividends on March 1 and another $6,000 on September 1 .

Noncontrolling interest share for 2010 is

A) $21,000

B) $32,400

C) $36,000

D) $50,000

4) What statements are required for Government-wide financial statements?

A) Statement of Cash Flows and Balance Sheet

B) Statement of Cash Flows and Statement of Net Assets

C) Statement of Net Assets and Statement of Activities

D) Operating Statement and Balance Sheet

5) Everything else held constant, if the federal government were to guarantee today that

it will pay creditors if a corporation goes bankrupt in the future, the interest rate on

corporate bonds will ________ and the interest rate on Treasury securities will

________

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

6) Sandpiper Corporation paid $120,000 for annual property taxes on January 15, 2011,

and $20,000 for building repair costs on March 10, 2011 . Total repair expenses for the

year were estimated to be $200,000, and are normally accrued during the year until

incurred. What total amount of expense for these items was reported in Sandpiper’s first

quarter 2011 interim income statement?

A) $ 50,000

B) $ 80,000

C) $100,000

D) $140,000

7) Bart Company purchased a 30% interest in Simpson Corporation on January 1, 2008,

and Bart accounted for its investment in Simpson under the equity method for the next

3 years. On January 1, 2011, Bart sold one-half of its interest in Simpson after which it

could no longer exercise significant influence over Simpson. Bart should

A) continue to account for its remaining investment in Simpson under the equity

method for the sake of consistency

B) adjust the investment in Simpson account to one-half of its original amount and

account for the remaining 15% interest using the equity method

C) account for the remaining investment under the cost method, using the investment in

Simpson account balance immediately after the sale as the new cost basis

D) adjust the investment account to one-half of its original amount (one-half of the

purchase price in 2008), and account for the remaining 15% investment under the cost

method

8) The four cash flow categories required in an Enterprise Fund’s Statement of Cash

Flows are listed below and assigned a letter code.

A)Cash flows from operating activities

B)Cash flows from noncapital financing activities

C)Cash flows from capital and related financing activities

D)Cash flows from investing activities

Required:

Use the correct letter code to indicate where each of the following ten items associated

with an Enterprise Fund should be reported in the Statement of Cash Flows.

1>An enterprise fund’s fixed asset was sold for cash.

2>Cash paid to suppliers for goods.

3>Paid principal, $100,000, and interest, $5,000, on a mortgage.

4>Cash proceeds from sale of investments, $65,000.

5>Cash paid for new equipment, $18,000.

6>Cash received from the general fund; restricted to cover part of the cost of plant

expansion, $900,000.

7>Cash received from another fund as a 6-month loan for the sole purpose of financing

purchase of equipment, $47,000.

8>Cash proceeds from issuing bonds for an enterprise fund’s construction project.

9>Cash paid to employees for salaries.

10>Cash received from interest earned on investments.

9) Using the revenue types shown below, match each of the revenue sources to a

revenue type. Each revenue type may be used more than once.

A.Derived Tax Revenues

B.Imposed Nonexchange Revenues

C.Government-Mandated Nonexchange Transactions

D.Voluntary Nonexchange Transactions

_____1> Corporate income tax

_____2> Sales taxes

_____3> Liquor taxes

_____4> Fines and penalties paid to a government entity

_____5> Cigarette taxes

_____6> Personal income tax

_____7> Donation made to a government entity

_____8> Motor fuel tax

_____9> Property tax

10) The accounting equation for a governmental fund is

A) Assets = Liabilities + Equity

B) Current assets + Noncurrent assets – Current liabilities – Noncurrent liabilities = Net

assets

C) Current assets – Current liabilities = Fund Balance

D) Assets = Liabilities + Fund Balance

11) On January 1, 2011, Jeff Company acquired a 90% interest in Margaret Company

for $198,000 cash. On January 1, 2011, Margaret Company had the following assets

and liabilities:

Book ValueFair Value

Cash$5,000$5,000

Accounts Receivable30,00035,000

Inventory40,00050,000

Plant Assets60,00080,000

Total Assets$135,000$170,000

Liabilities$25,000$25,000

Capital Stock100,000

Retained Earnings10,000

Total Liabilities &

Stockholders’ Equity$135,000

Push-down accounting is used for the acquisition.

Required:

1> Assume both companies use the entity theory.

a. Record the journal entry on Margaret’s separate books on January 1, 2011 .

b. Record the journal entry on Jeff’s separate books on January 1, 2011 .

2> Assume both companies use the parent company theory.

a. Record the journal entry on Margaret’s separate books on January 1, 2011 .

b. Record the journal entry on Jeff’s separate books on January 1, 2011 .

12) The Justin, Kyle, and Lulu partnership was dissolved by the partners on May 1,

2011 . Their balance sheet on that date is shown below:

Cash$26,000Liabilities$41,000

Other assets96,000Loan from Kyle3,000

Loan to Justin10,000Justin,capital (20%)19,000

Kyle, capital (20%)26,000

Lulu, capital (60%)43,000

Total assets$132,000Total liab./equity$132,000

In May, other assets with a book value of $46,000 were sold for $50,000 in cash.

Required:

Determine how the available cash on May 31, 2011 will be distributed.

13) Paleo Corporation holds 80% of the capital stock of Sockrite Company. On January

1, 2011, Sockrite purchased $50,000 par value, 10% bonds on the open market that had

been issued by Paleo on January 1, 2009 . Sockrite paid $58,000 for these bonds which

had originally been issued by Paleo for $53,000, with a 10-year maturity from the date

of issue. Interest is paid annually on December 31 . Straight-line amortization is used

by both companies.

Required:

1> Calculate the interest income reported by Sockrite related to these bonds in 2011 .

2> Calculate the interest expense reported by Paleo related to these bonds in 2011 .

3> Calculate the gain or loss on retirement of bonds payable to be reported on

consolidated financial statements in 2011 .

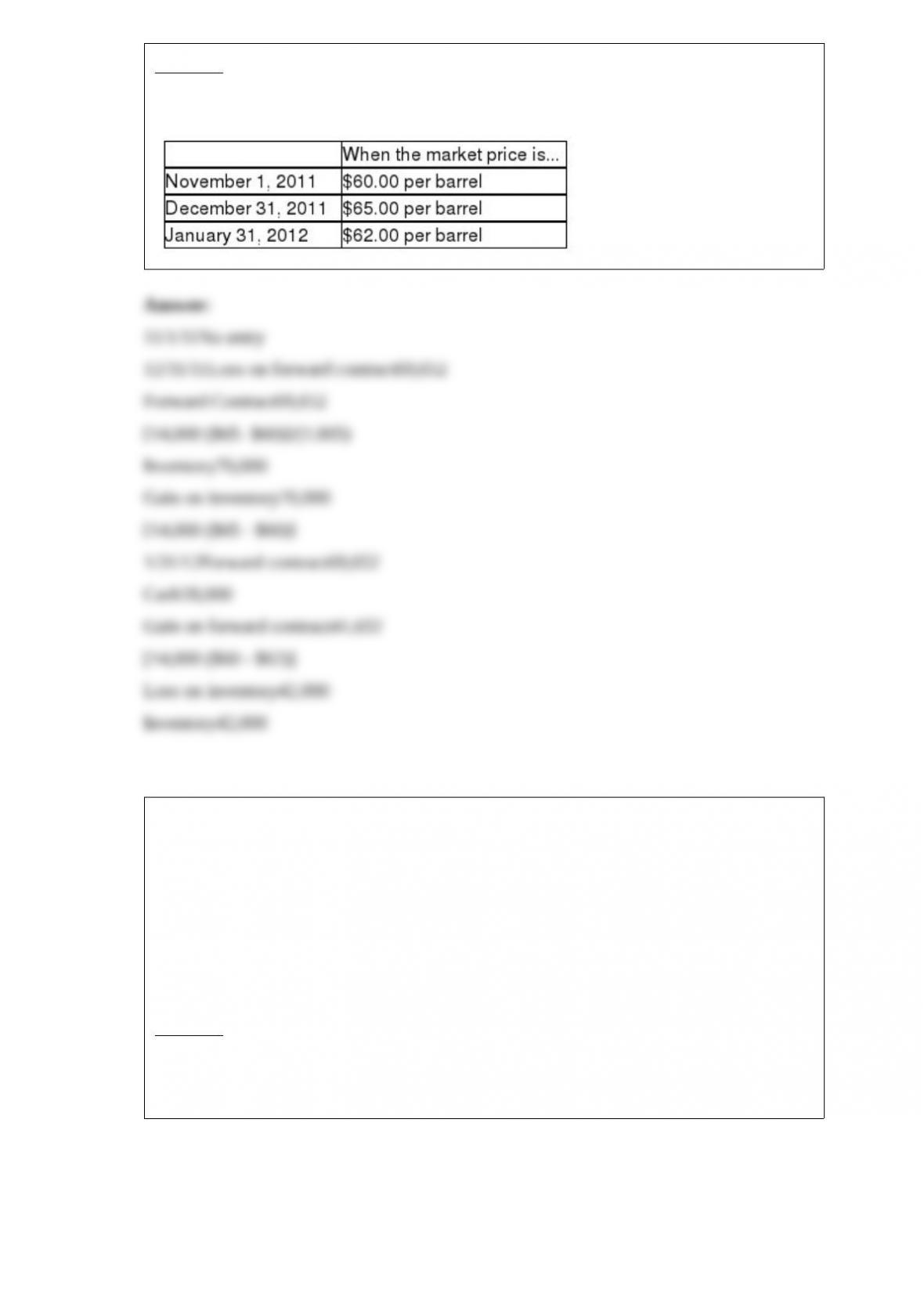

14) Ivan has 14,000 barrels of oil that were purchased a month ago at $50.00 per barrel.

On November 1, 2011 Ivan hedges the value of the inventory by entering into a forward

contract to sell 14,000 barrels of oil on January 31, 2012 for $60.00 per barrel. The

forward contract is to be settled net.

Assume this is a fair value hedge.

Required:

Assume a 6% discount rate is reasonable, and using a mixed-attribute model, prepare

the journal entries to account for this hedge at the following dates:

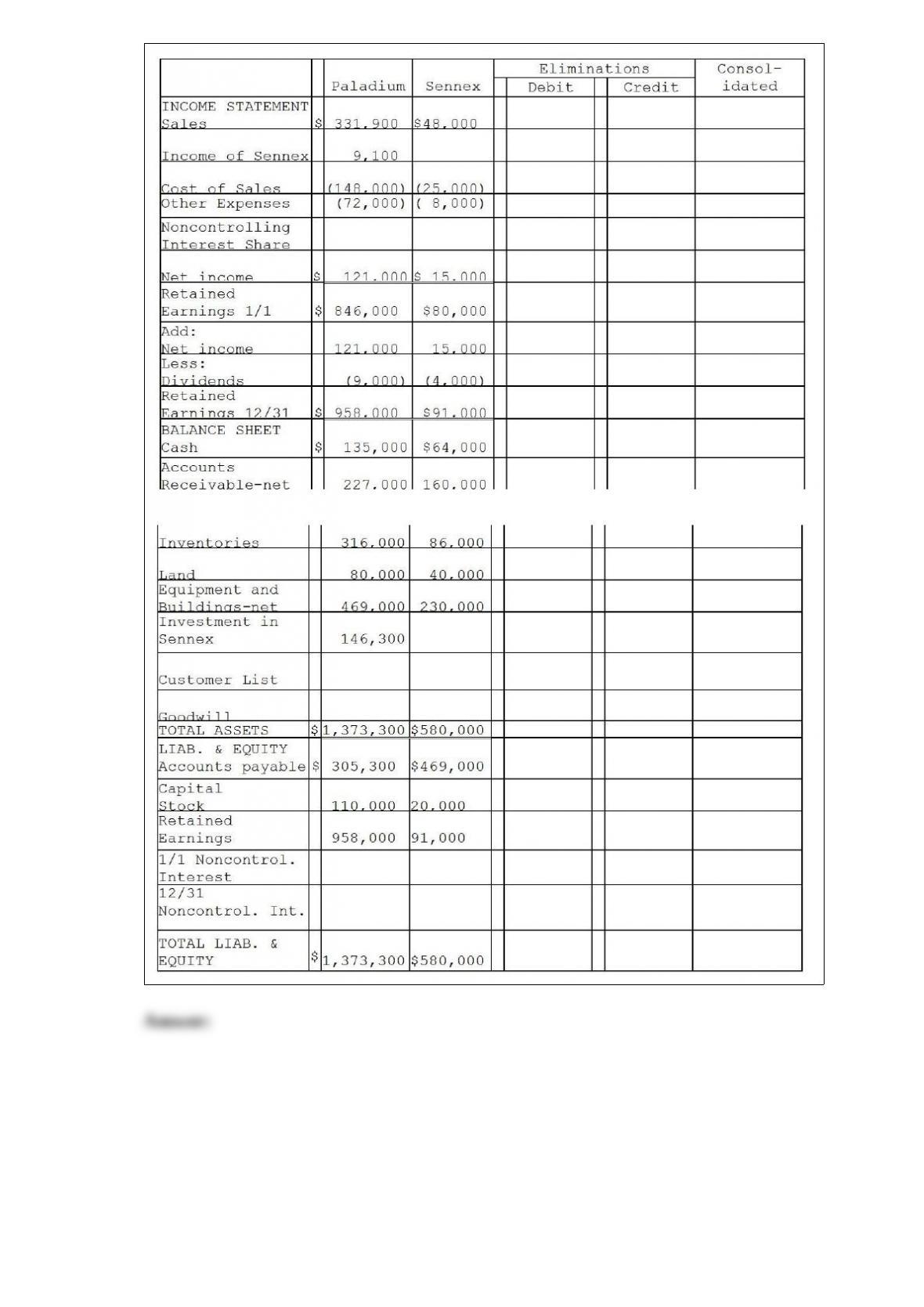

15) On December 31, 2011, Paladium International purchased 70% of the outstanding

common stock of Sennex Chemical. Paladium paid $140,000 for the shares and

determined that the fair value of all recorded Sennex assets and liabilities approximated

their book values, with the exception of a customer list that was not recorded and had a

fair value of $10,000, and an expected remaining useful life of 5 years. At the time of

purchase, Sennex had stockholders’ equity consisting of capital stock amounting to

$20,000 and retained earnings amounting to $80,000. Any remaining excess fair value

was attributed to goodwill. The separate financial statements at December 31, 2012

appear in the first two columns of the consolidation workpapers shown below.

Required:

Complete the consolidation working papers for Paladium and Sennex for the year

2012 .

Paladium

16) Plymouth Corporation (a U.S. company) began operations on September 1, 2011,

when the owner borrowed $250,000 to establish the business. Plymouth then had the

following import and export transactions with unaffiliated Chinese companies:

September 6, 2011Bought material inventory for 100,000 yuan on account. Invoice

denominated in yuan.

September 18, 2011Sold 80% of inventory acquired on 9/6/11 for 110,000 yuan on

account. Invoice denominated in yuan.

October 5, 2011Acquired and paid the 100,000 yuan owed to the Chinese supplier

October 18, 2011Collected the 110,000 yuan from the Chinese customer and

immediately converted them into U.S. dollars

The following exchange rates apply:

DateRate

September 6$0.1544 = 1 yuan

September 18$0.1607 = 1 yuan

September 30$0.1591 = 1 yuan

October 5$0.1578 = 1 yuan

October 18$0.1593 = 1 yuan

Required:

1> What were Sales in the September month-end income statement?

2> What was the COGS associated with these sales?

3> What is the Accounts Receivable balance in the balance sheet at September 30,

2011?

4> What is the Inventory balance in the balance sheet at September 30, 2011?

5> What is the Exchange gain or loss that will be reported for the month of September?

17) If the federal government where to raise the income tax rates, would this have any

impact on a state’s cost of borrowing funds? Explain

18) Pongo Company has $2,000,000 of 6% bonds outstanding on December 31, 2010

with unamortized premium of $60,000. These bonds pay interest semiannually on

January 1 and July 1 and mature on January 1, 2016 . Straight-line amortization is used.

Syring Inc., 90%-owned subsidiary of Pongo, buys $1,000,000 par value of Pongo’s

outstanding bonds in the market for $980,000 on January 2, 2011 . There is only one

issue of outstanding bonds of the affiliated companies and they have consolidated

financial statements.

For the year 2011, Pongo has income from its separate operations (excluding

investment income) of $3,000,000 and Syring reports net income of $200,000. Pongo

uses the equity method to account for the investment.

Required: Determine the following:

1>Noncontrolling interest share for 2011 .

2>Controlling share of consolidated net income for Pongo Company and subsidiary for

2011 .

19) On November 1, 2011, Portsmith Corporation, a calendar-year U.S. corporation,

invested in a purely speculative contract to purchase 1 million yen on January 30, 2012,

from the Karoke Trading Company, a Japanese brokerage firm. Portsmith agreed to

purchase 1,000,000 yen from Karoke at a fixed price of $0.0100 per yen. Karoke agreed

to transmit 1,000,000 yen to Portsmith on January 30 . Net settlement is not permitted.

The spot rates for yen are:

Nov 01, 2011 1 yen = $0.0097

Dec 31, 2011 1 yen = $0.0104

Jan 30, 2012 1 yen = $0.0106

The 30-day forward rate for yen on December 31, 2011 was $0.0104.

Required:

Prepare the General Journal entries that Portsmith would record on November 1,

December 31, and January 30 .

20) Shebing Corporation had $80,000 of $10 par value common stock outstanding on

January 1, 2010, and retained earnings of $120,000 on the same date. During 2010 and

2011, Shebing earned net incomes of $30,000 and $45,000, respectively, and paid

dividends of $8,000 and $10,000, respectively.

On January 1, 2010, Pentz Company purchased 25% of Shebing’s outstanding common

stock for $60,000. On January 1, 2011, Pentz purchased an additional 10% of Shebing’s

outstanding stock for $30,200. The payments made by Pentz in excess of the book value

of net assets acquired were attributed to equipment, with each excess value amount

depreciable over 8 years under the straight-line method.

Required:

1>What is the adjustment to Investment Income for depreciation expense relating to

Pentz’s Investment in Shebing in 2010 and 2011?

2>What will be the December 31, 2011 balance in the Investment in Shebing account

after all adjustments have been made?

21) An adjusted trial balance is provided below for the Dade County copy services

department at June 30, 2011 .

Cash$ 21,000

Due from Enterprise Fund6,000

Due from Debt Service Fund2,000

Supplies inventory5,000

Supplies used3,000

Equipment32,000

Salary expense25,000

Utility expense9,000

Depreciation expense6,000

Operating transfer to General Fund4,000

$113,000

Accumulated depreciation $ 24,000

Accounts payable2,000

Advance from General Fund (not for capital assets)10,000

Capital Contribution from General Fund1,000

Net assets (beginning)28,000

Revenue – services billed48,000

$113,000

Required:

1>Prepare a statement of revenues, expenses and changes in net assets for the copy

services department for the year ended June 30, 2011 .

2>Prepare a statement of net assets for the copy services department at June 30, 2011 .

Assume all assets are not externally or internally restricted.