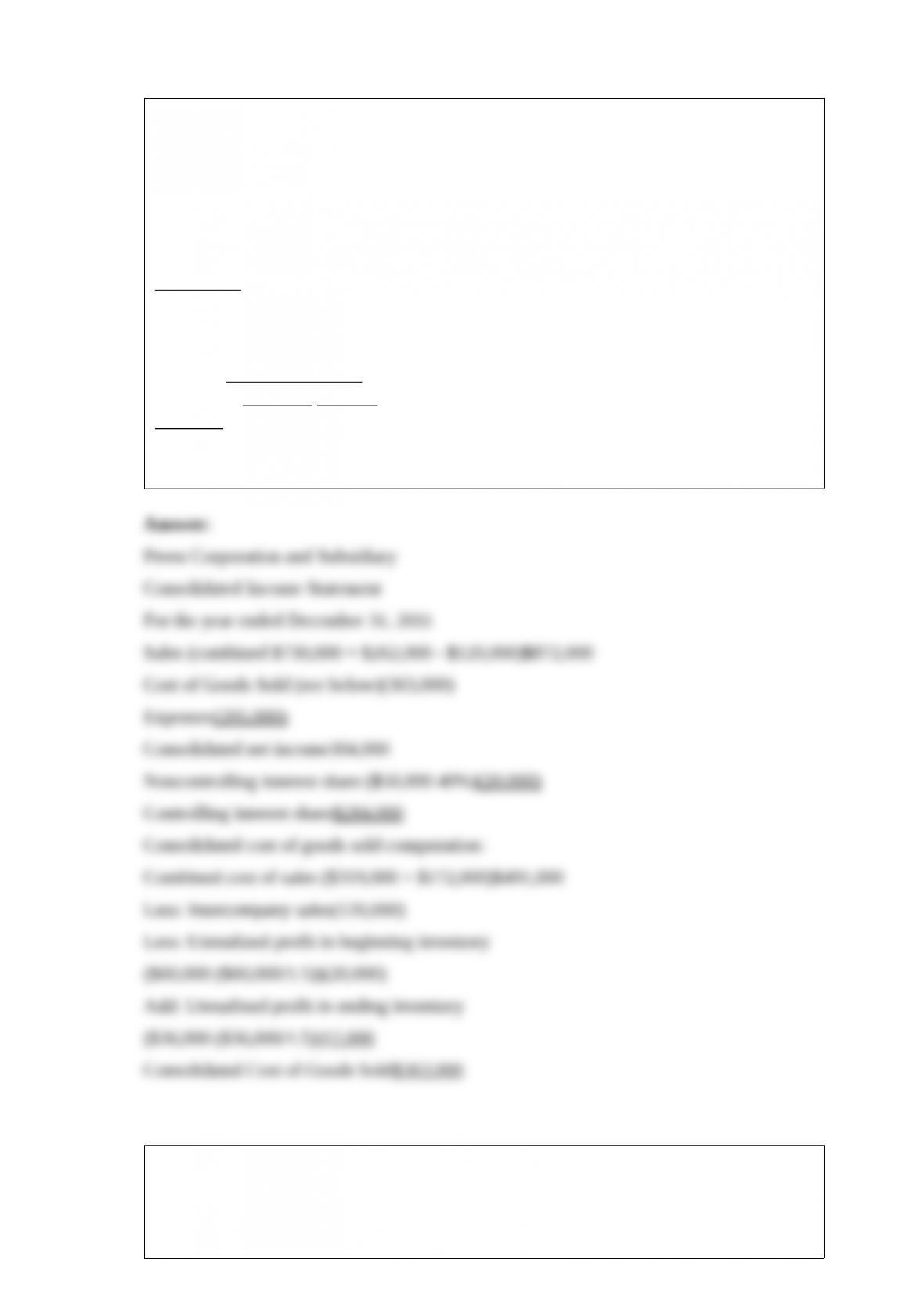

1) Preen Corporation acquired a 60% interest in Shino Corporation at a cost equal to

60% of the book value of Shino’s net assets in 2010 . At the time of acquisition, the

book value and fair value of Shino’s assets and liabilities were equal. During 2011,

Preen sold $120,000 of merchandise to Shino. All intercompany sales are made at 150%

of Preen’s cost. Shino’s beginning and ending inventories resulting from intercompany

sales for 2011 were $60,000 and $36,000, respectively. Income statement information

for both companies for 2011 is as follows:

PreenShino

Sales Revenue$730,000 $262,000

Investment income from Shino38,000

Cost of Goods Sold(319,000)(172,000)

Expenses(165,000)(40,000)

Net Income$284,000 $50,000

Required:

Prepare a consolidated income statement for Preen Corporation and Subsidiary for 2011

.

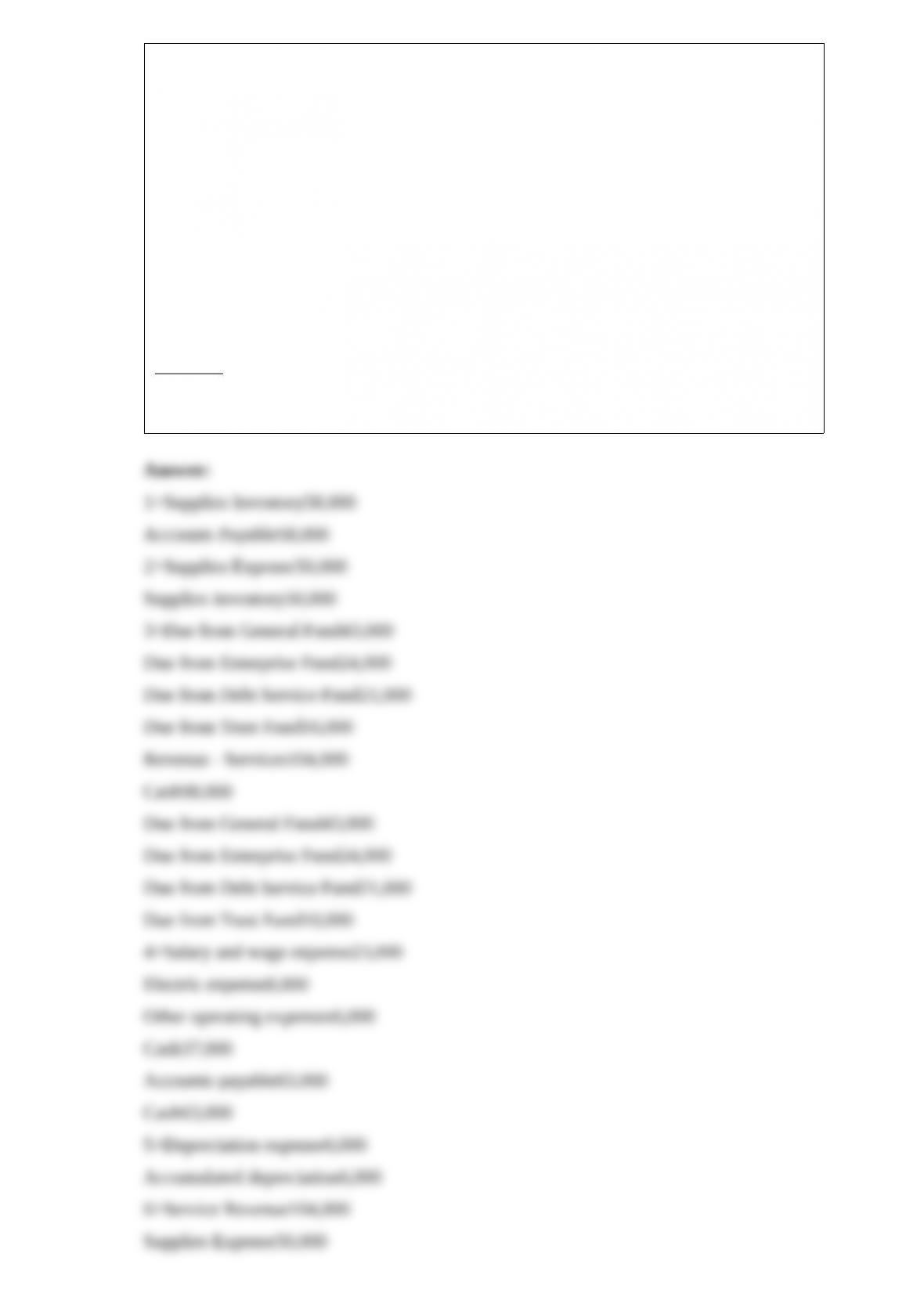

2) Static City started a department to provide copy, printing and mailing services for all

departments and agencies of the city.

During the fiscal year from July 1, 2010 through June 30, 2011, the copy services

department had the following transactions:

1>Paper and toner inventory was purchased for $58,000, on account.

2>The paper and toner inventory physical count showed only $8,000 on hand at June

30, 2011 .

3>The department billed other departments for services rendered to them amounting to:

General Fund, $43,000; Enterprise Fund, $24,000; Debt Service Fund, $21,000; and

Trust Fund, $16,000. All receivables were collected with the exception of $6,000 from

the Trust Fund which is expected to be collected in July, 2011 .

4>The department incurred and paid the following expenses: salaries and wages,

$23,000; Electric, $8,000; Other operating expenses, $6,000. Also, $63,000 of the

Accounts Payable were paid during the year.

5>Depreciation Expense on Equipment amounted to $6,000 for the year ending June

30, 2011 .

6>The department prepared the closing entry on June 30, 2011 .

Required:

For the fiscal year ended June 30, 2011, prepare the journal entries to record the

transactions for the Internal Service Fund.

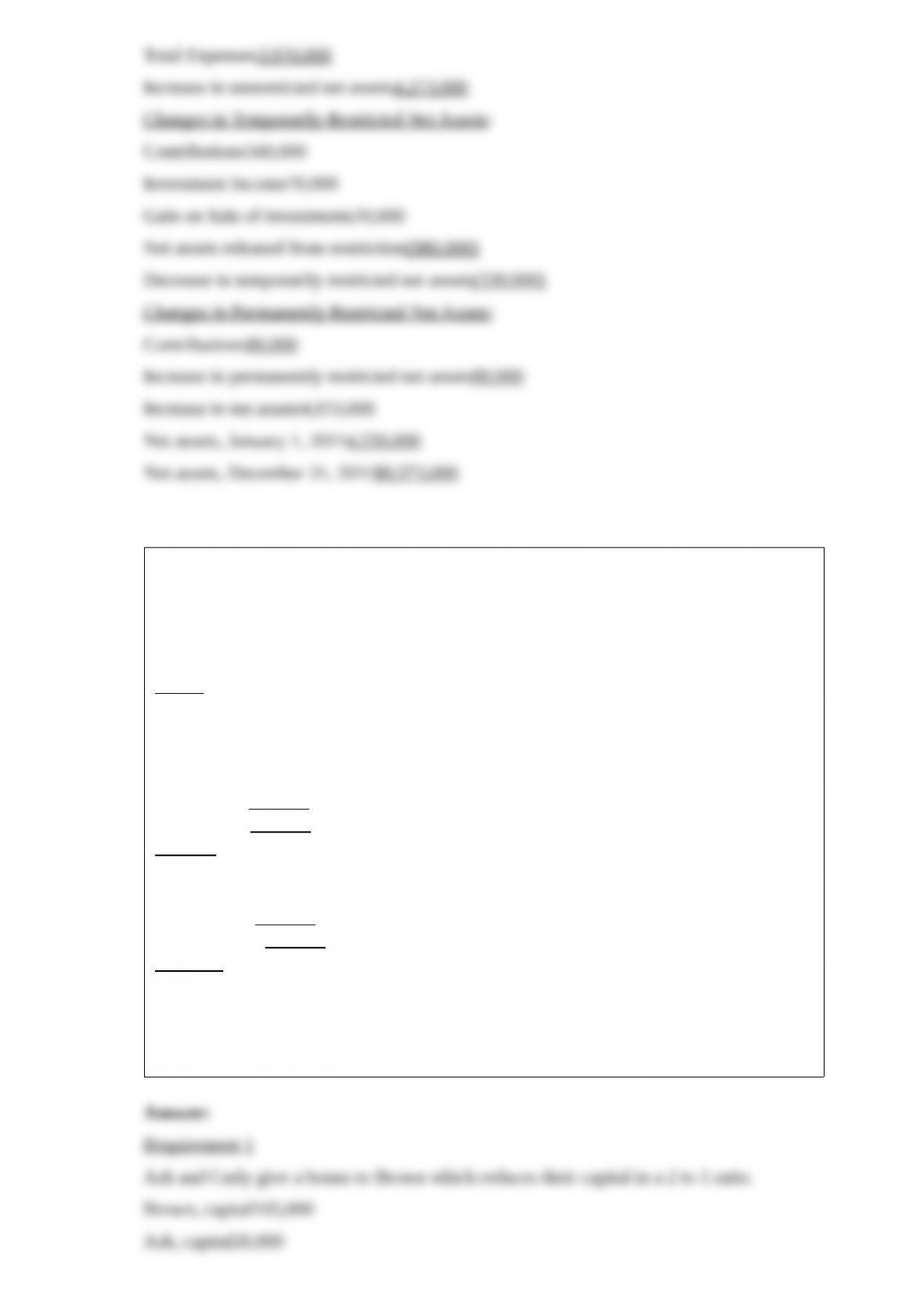

3) The following information was taken from the accounts and records of the

Community Chest Foundation, a private, not-for-profit VHWO organization. All

balances are as of December 31, 2011, unless otherwise noted.

Unrestricted Support – Contributions$6,500,000

Unrestricted Support – Membership Dues700,000

Unrestricted Revenues – Investment Income63,000

Temporarily restricted gain on sale of investments20,000

Expenses – Program Services2,950,000

Expenses – Supporting Services670,000

Expenses – Supporting Services350,000

Temporarily Restricted Support – Contributions560,000

Temporarily Restricted Revenues – Investment Income70,000

Permanently Restricted Support – Contributions80,000

Unrestricted Net Assets, January 1, 2011500,000

Temporarily Restricted Net Assets, January 1, 20114,000,000

Permanently Restricted Net Assets, January 1, 201150,000

The unrestricted support from contributions was received in cash during the year. The

expenses included $980,000 paid from temporarily-restricted cash donations.

Required:

Prepare Community Chest’s Statement of Activities for the year ended December 31,

2011 .

4) A summary balance sheet for the Ash, Brown, and Curly partnership on December

31, 2011 is shown below. Partners Ash, Brown, and Curly allocate profit and loss in

their respective ratios of 2:1:1. The partnership agreed to pay partner Brown $135,000

for his partnership interest upon his retirement from the partnership on January 1,

2012 . The partnership financials on January 1, 2012 are:

Assets

Cash$ 75,000

Marketable securities60,000

Inventory85,000

Land90,000

Building-net110,000

Total assets$420,000

Equities

Ash, capital$210,000

Brown, capital105,000

Curly, capital105,000

Total equities$420,000

Required:

Prepare the journal entry to reflect Brown’s retirement from the partnership:

1>Assuming a bonus to Brown.

2>Assuming a revaluation of total partnership capital based on excess payment.

3>Assuming goodwill equal to the excess payment is recorded.

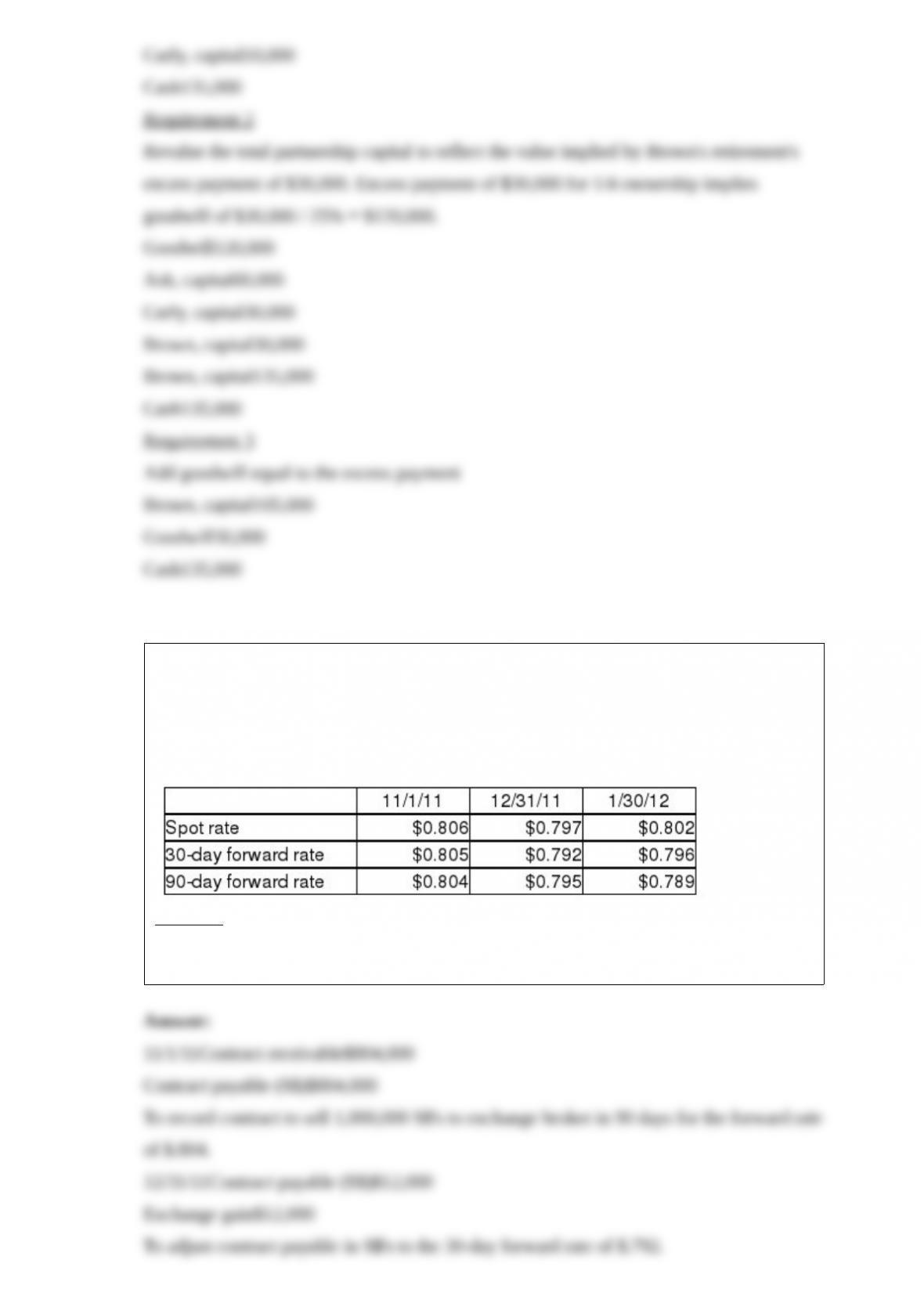

5) Slickton Corporation, a U.S. holding company, enters into a forward contract on

November 1, 2011 to speculate in Singapore dollars (S$). The forward contract requires

Slickton to sell 1,000,000 Singapore dollars to the exchange broker on January 30, 2012

. Net settlement is not permitted. Relevant exchange rates for the Singapore dollar are

listed below:

Required:

Prepare the journal entries required by Slickton on November 1, 2011, December 31,

2011 (year end), and January 30, 2012 .

6) Flagship Company has the following information collected in order to prepare a cash

flow statement and uses the indirect method for Cash Flow from Operations. The

annual report year end is December 31, 2011 .

Noncontrolling Interest Dividends Paid$17,000

Undistributed Income of Equity Investees7,000

Depreciation Expense80,000

Controlling Interest Share of Consolidated Net Income325,000

Increase in Accounts Payable26,000

Amortization of Patent10,000

Decrease in Accounts Receivable57,000

Increase in Inventories72,000

Gain on sale of equipment45,000

Noncontrolling Interest Share27,000

Required:

Prepare the Cash Flow for Operations part of the cash flow statement for Flagship for

the year ended December 31, 2011 .

7) Savy Corporation’s stockholders’ equity on December 31, 2010 was as follows:

8% cumulative preferred stock, $100 par value,

callable at $109, with two years of dividends

in arrears$100,000

Common stock, $25 par value700,000

Additional paid-in capital250,000

Retained earnings400,000

Total stockholders’ equity$1,450,000

On January 1, 2011, Paul Corporation purchased a 70% interest in Savy’s common

stock for $2,100,000. On this date the book values of Savy’s assets and liabilities are

equal to their fair values.

Required:

1> Determine the book value of the common stockholders’ equity for Savy Corporation

on January 1, 2011 .

2> What is the amount of goodwill reported on the consolidated balance sheet for Paul

Corporation and Subsidiary at January 2, 2011?

3> On January 2, 2011, Paul purchased 70% of Savy’s preferred stock for $50,000.

Prepare the journal entry(ies) for Paul for this purchase on January 2, 2011 .

4> Prepare the elimination entry on the consolidating work papers for the Investment in

Savy, Preferred Stock and Savy’s Preferred Stock on January 2, 2011 .

8) DeFunk Corporation is being liquidated under Chapter 7 of the Bankruptcy Act. The

trustee has determined that the unsecured claims will receive $.18 on the dollar. Magma

Corporation holds a $200,000 mortgage receivable from DeFunk that is secured by the

land and buildings with a book value of $180,000 and a fair value of $190,000. Magma

also holds an $80,000 unsecured note receivable from Defunk. Mortgage interest owed,

which is secured with the mortgage note, is $4,000. Note interest owed, which is

unsecured, is $2,000.

Required:

How much of the amounts owed will Magma recover?

9) On December 31, 2010, Peris Company acquired Shanta Company’s outstanding

stock by paying $400,000 cash and issuing 10,000 shares of its own $30 par value

common stock, when the market price was $32 per share. Peris paid legal and

accounting fees amounting to $35,000 in addition to stock issuance costs of $8,000.

Shanta is dissolved on the date of the acquisition. Balance sheet information for Peris

and Shanta immediately preceding the acquisition is shown below, including fair values

for Shanta’s assets and liabilities.

PerisShantaShanta

Book ValueBook ValueFair Value

Cash490,000$140,000$140,000

Accounts Receivable560,000280,000280,000

Inventory520,000200,000260,000

Land460,000150,000140,000

Plant Assets Net980,000325,000355,000

Construction Permits380,000170,000190,000

Accounts Payable(460,000)(140,000)(140,000)

Other accrued expenses(160,000)(45,000)(45,000)

Notes Payable(800,000)(460,000)(460,000)

Common Stock ($30 par)(960,000)

Common Stock ($20 par)(200,000)

Additional P.I.C(192,000)(80,000)

Retained Earnings(818,000)(340,000)

Required: Determine the consolidated balances which Peris would present on their

consolidated balance sheet for the following accounts.

Cash

Inventory

Construction Permits

Goodwill

Notes Payable

Common Stock

Additional Paid in Capital

Retained Earnings