Trading securities are most commonly found on the books of:

a. Oil companies.

b. Manufacturing companies.

c. Banks.

d. Foreign subsidiaries.

The International Accounting Standards Board:

a. Was the predecessor to the IASC.

b. Can overrule the FASB when their policies disagree.

c. Promotes the use of high-quality, understandable global accounting standards.

d. Has its headquarters in Geneva.

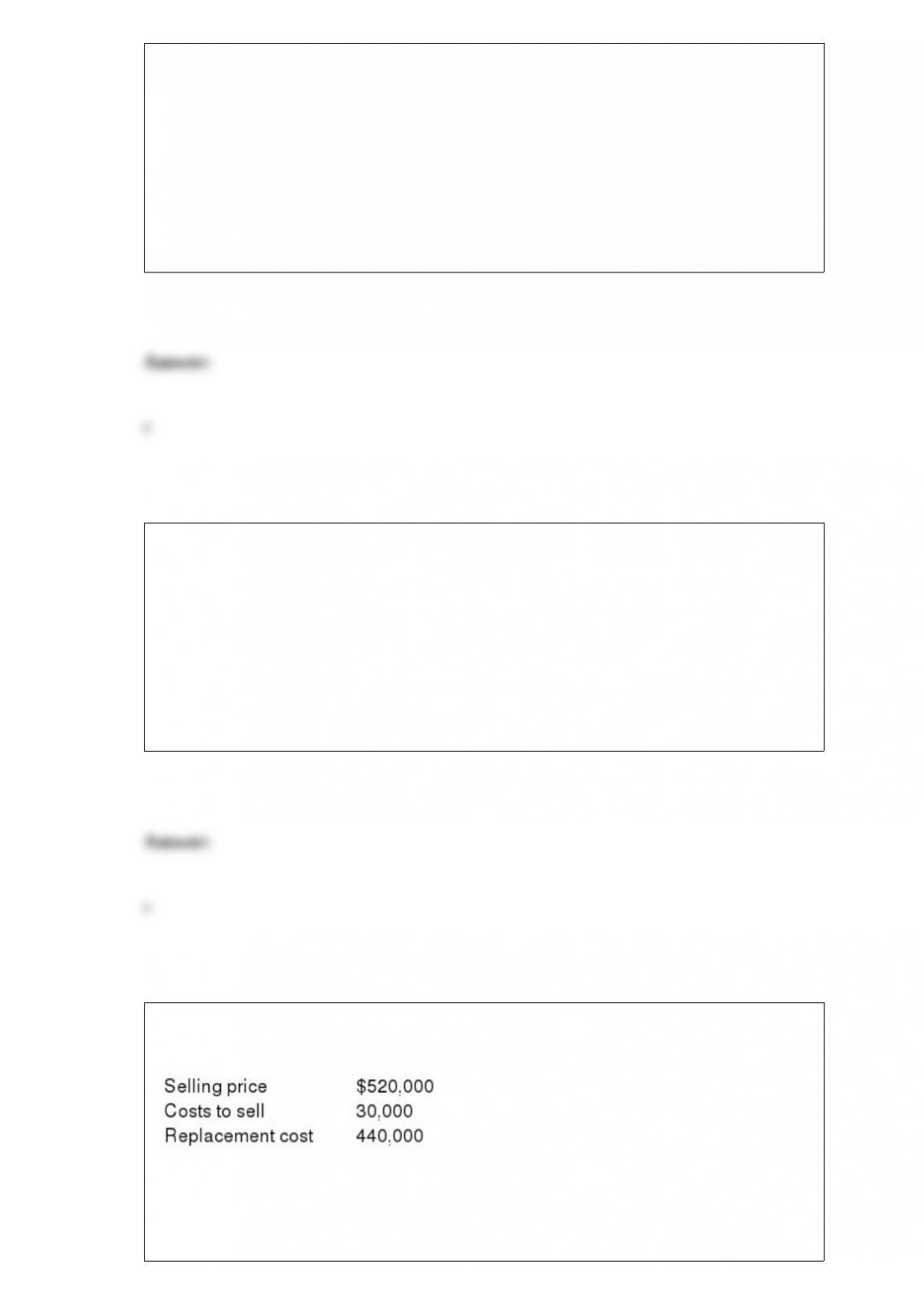

Sullivan Corporation has determined its year-end inventory on a FIFO basis to be

$500,000. Information pertaining to that inventory is as follows:

What should be the reported value of Sullivan’s inventory?

a. $500,000.

b. $440,000.

c. $470,000.

d. $490,000.

Goofy Inc. bought 15,000 shares of Crazy Co.’s stock for $150,000 on May 5, 2015,

and classified the stock as available for sale. The market value of the stock declined to

$118,000 by December 31, 2015. Goofy reclassified this investment as trading

securities in December of 2016 when the market value had risen to $125,000. What

effect on 2016 income should be reported by Goofy for the Crazy Co. shares?

a. $0.

b. $25,000 net loss.

c. $7,000 net gain.

d. $32,000 net loss.

Indiana Co. began a construction project in 2016 with a contract price of $150 million

to be received when the project is completed in 2018. During 2016, Indiana incurred

$36 million of costs and estimates an additional $84 million of costs to complete the

project. Indiana recognizes revenue over time and for this project recognizes revenue

over time according to the percentage of the project that has been completed. Indiana:

a. Recognized no gross profit or loss on the project in 2016.

b. Recognized $6 million loss on the project in 2016.

c. Recognized $9 million gross profit on the project in 2016.

d. Recognized $36 million loss on the project in 2016.

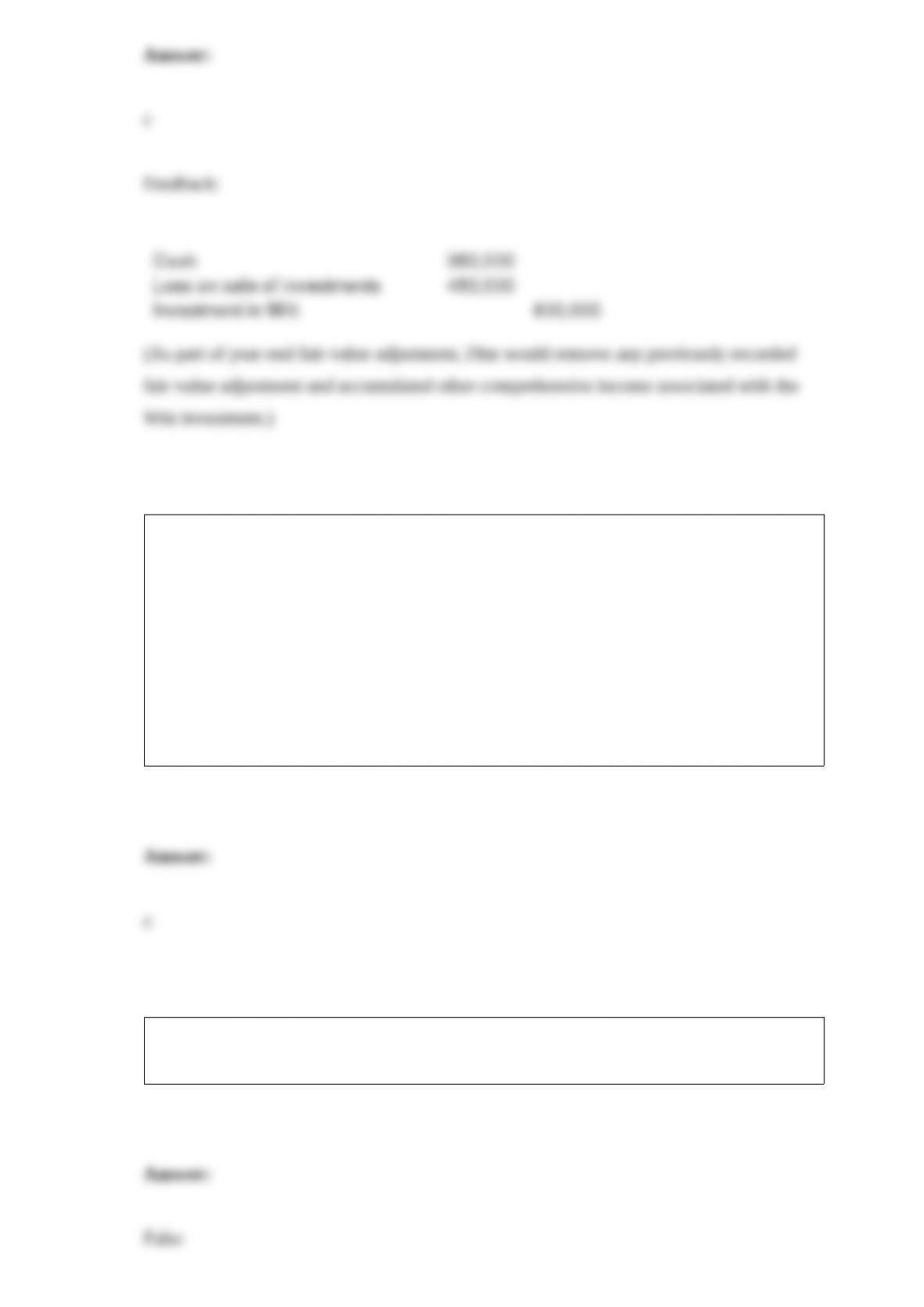

Dim Corporation purchased 1,000 shares of Witt Corporation stock in 2013 for $800

per share and classified the investment as securities available for sale. Witt’s market

value was $400 per share on December 31, 2014, and $300 on December 31, 2015.

During 2016, Dim sold all of its Witt stock at $350 per share. In its 2016 income

statement, Dim would report:

a. A realized gain of $50,000.

b. A recognition of unrealized losses of $400,000.

c. A loss on the sale of investments of $450,000.

d. A trading gain of $50,000 and an unrealized loss of $500,000.

Galaxy sells used videogames for cash and provides a one-week return right. Returns

are material and reasonably predictable. Galaxy should:

a. Not record sales until the right to return has expired.

b. Record a contra-receivable in the year of the sale.

c. Recognize a refund liability associated with estimated returns.

d. Credit sales in the period of the return.

State and Federal Unemployment Taxes (SUTA and FUTA) must be withheld from

employees’ wages.

Goosen Company bought a copyright for $90,000 on January 1, 2013, at which time the

copyright had an estimated useful life of 15 years. On January 5, 2016, the company

determined that the copyright would expire at the end of 2021. How much should

Goosen record retrospectively as the effect of change?

a. $ 0.

b. $12,000.

c. $ 8,000.

d. $14,400.

When treasury shares are sold at a price above cost:

a. A gain account is credited.

b. A loss is reported.

c. A revenue account is credited.

d. Paid-in capital is increased.

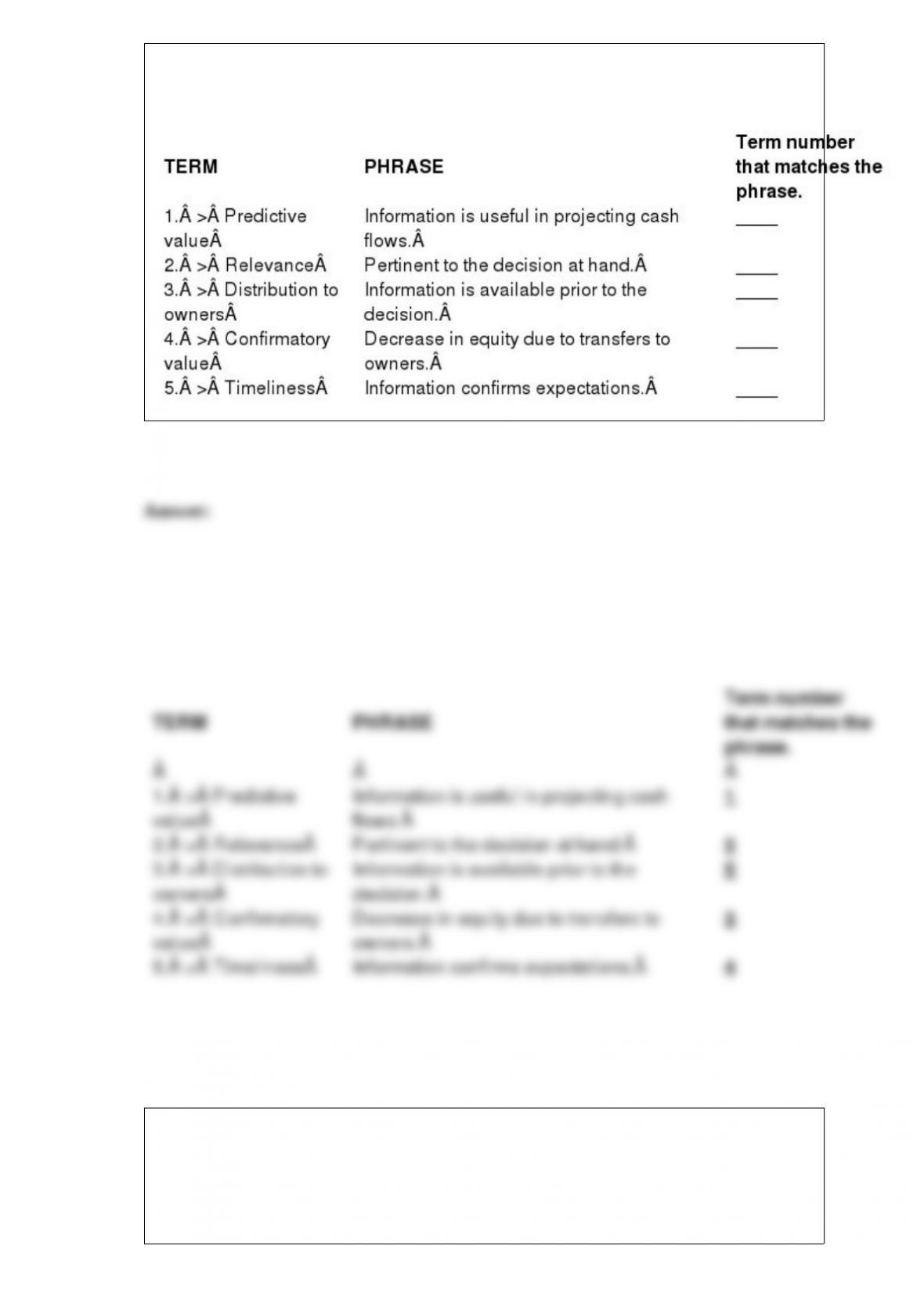

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct number code for the term.

Rice Inc. had 420 million shares of common stock and 1 million shares of 6%, $200

par, cumulative preferred stock outstanding at the end of 2015 and 2016. No dividends

were declared or paid on either class of stock in either year. Net income for 2016 was

$398.4 million. The company’s tax rate is 30%.

Required:

Compute basic earnings per share for the year ended December 31, 2016.

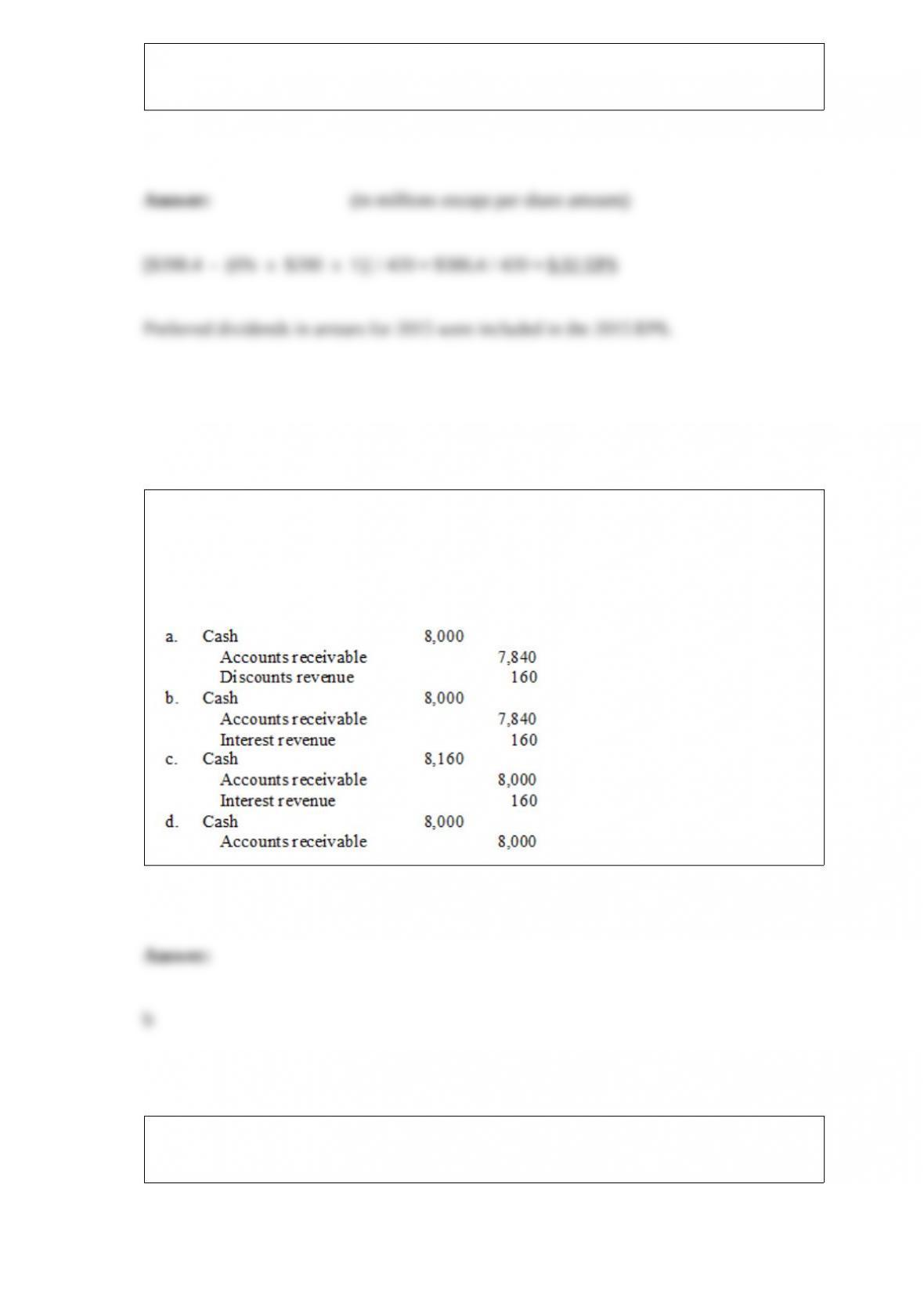

On November 10 of the current year, Cherokee Industries sold materials to a customer

for $8,000 with credit terms 2/10, n/30. Cherokee uses the net method of accounting for

cash discounts. What entry would Cherokee make on December 10, assuming the

correct payment was received on that date?

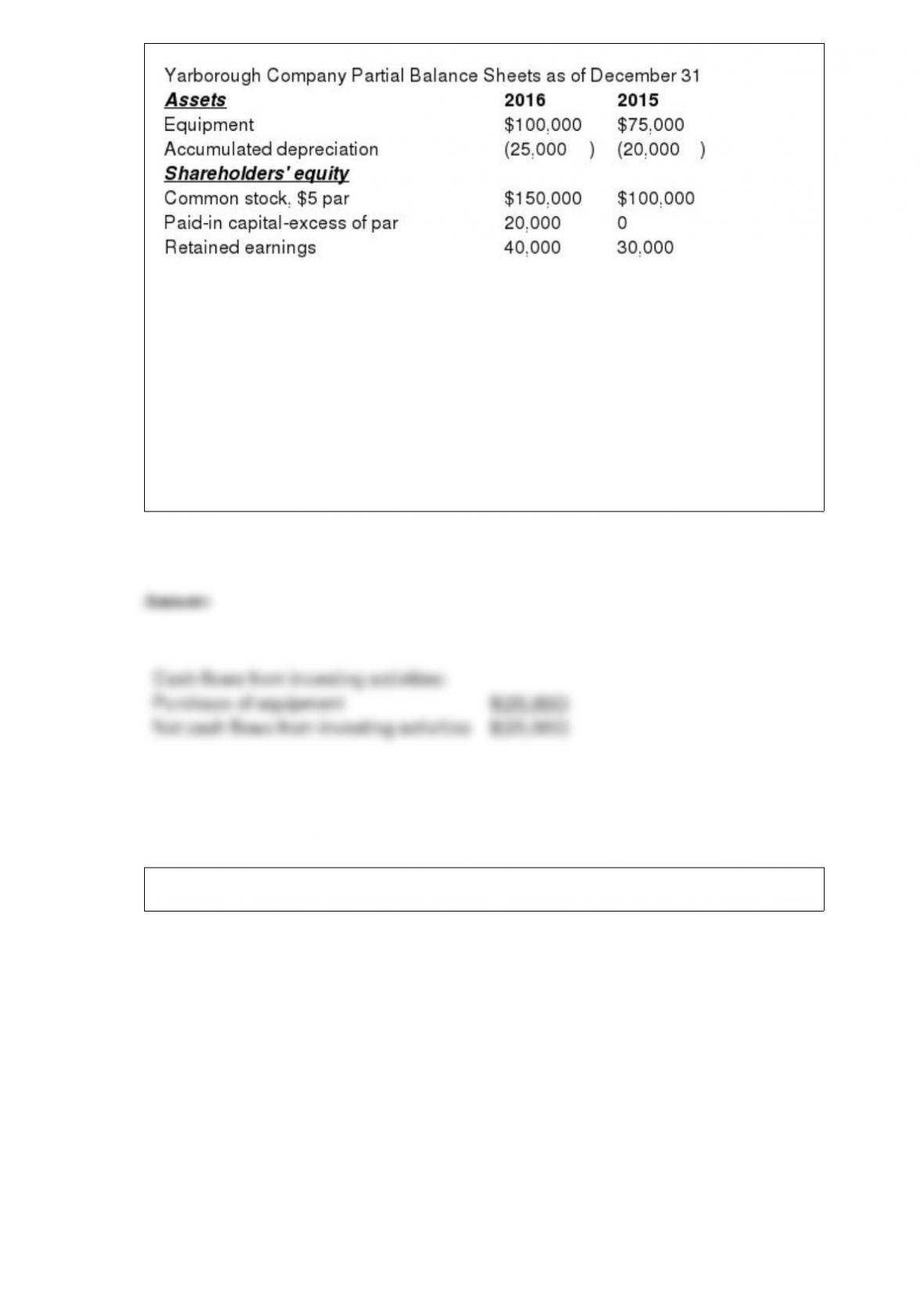

Partial balance sheets for Yarborough Company and additional information are found

below.

Additional information for 2016:

July 1: Issued 10,000 shares of common stock for cash.

July 1: Purchased new equipment for cash.

Dec. 31 Paid cash dividends of $30,000.

Required:

Prepare the investing activities section of the statement of cash flows for 2016.

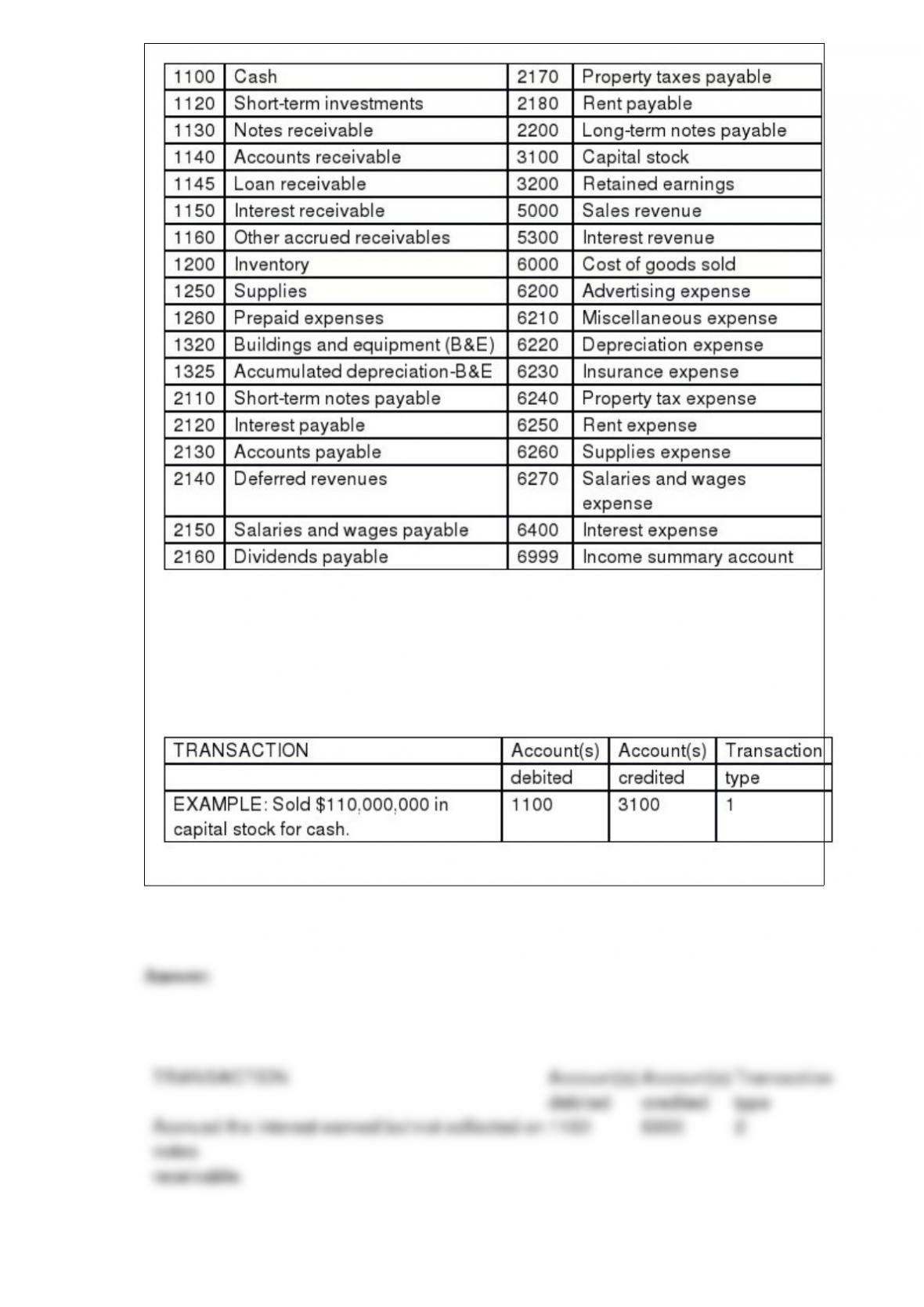

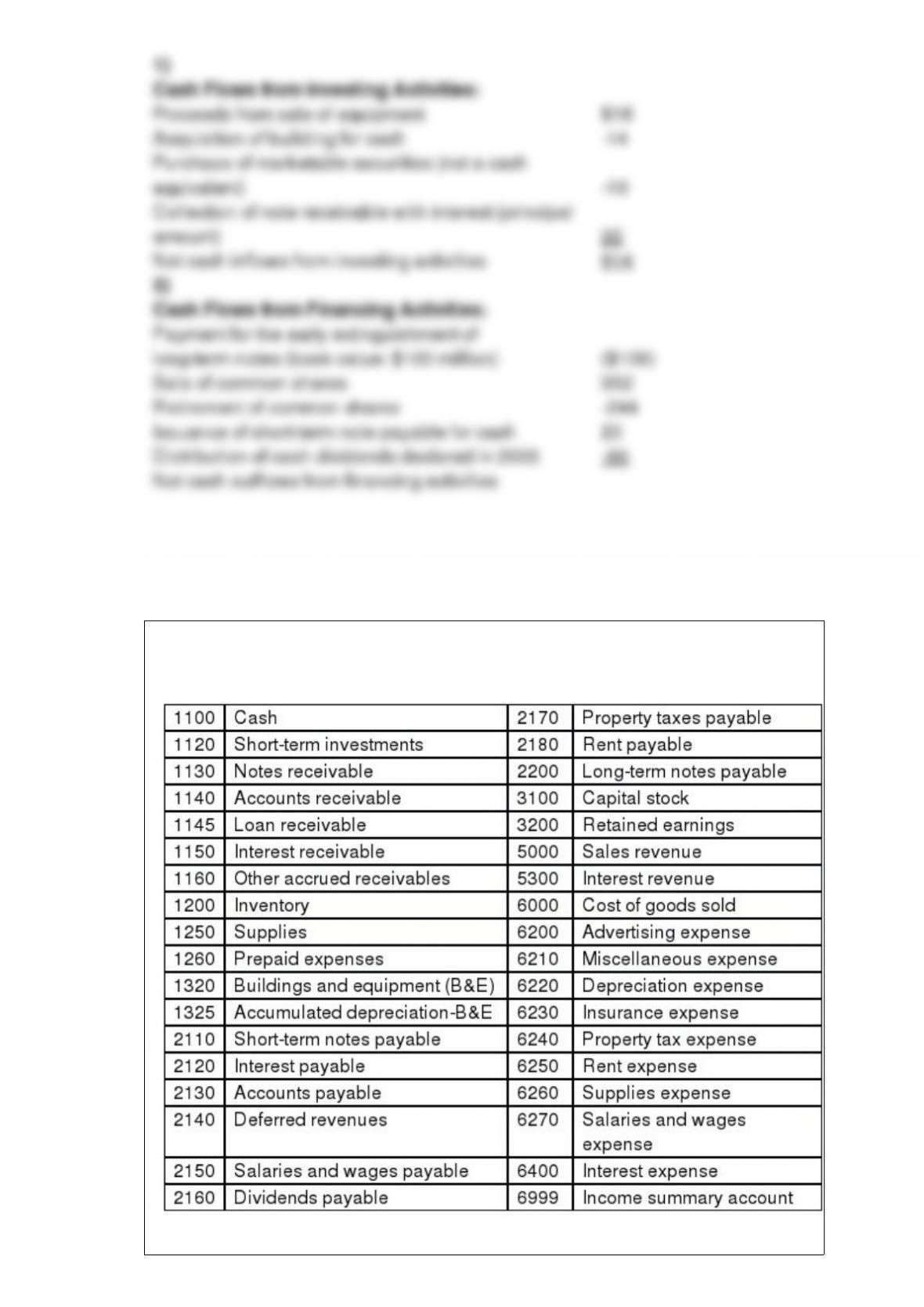

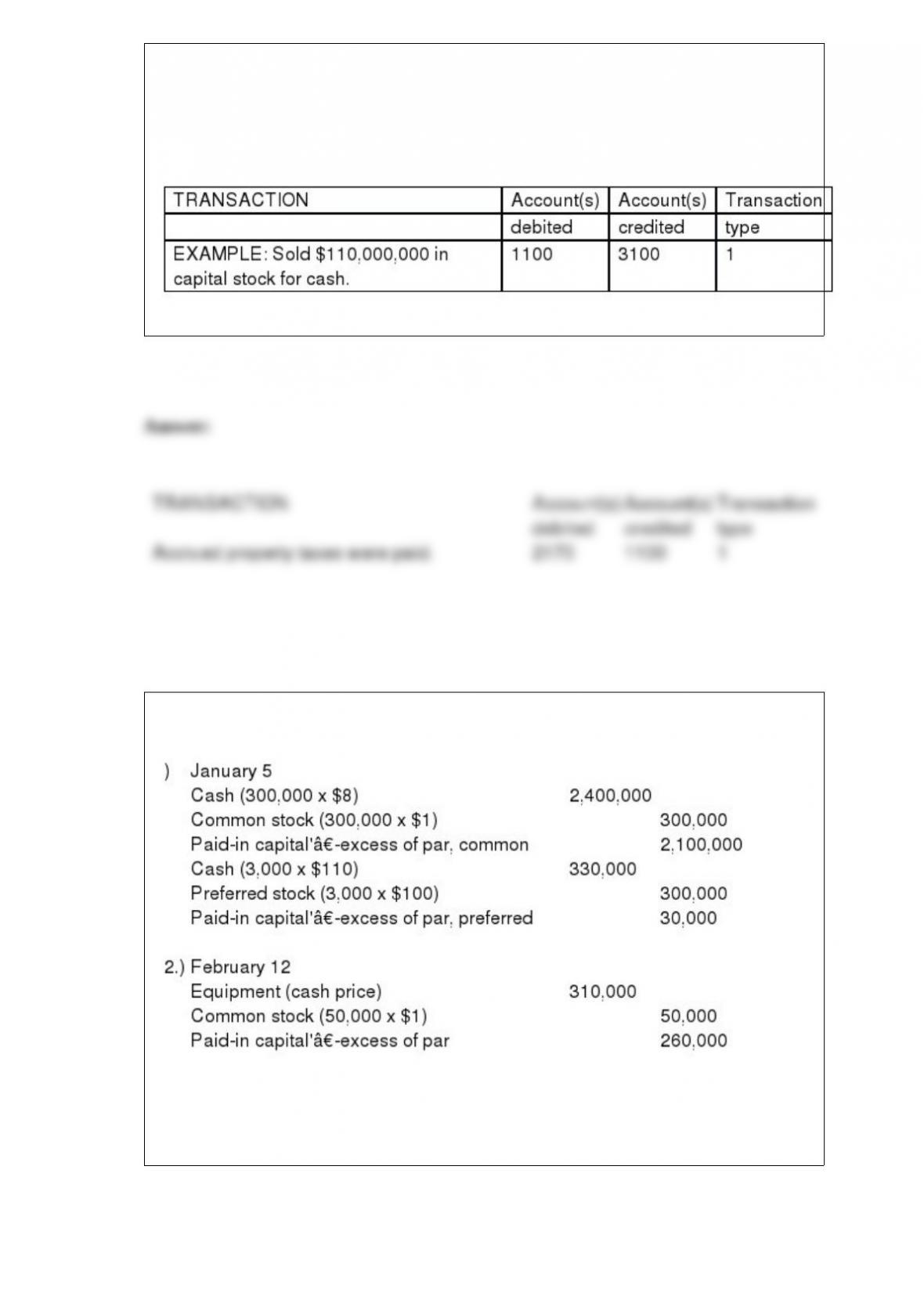

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Accrued the interest earned but not collected on notes receivable.

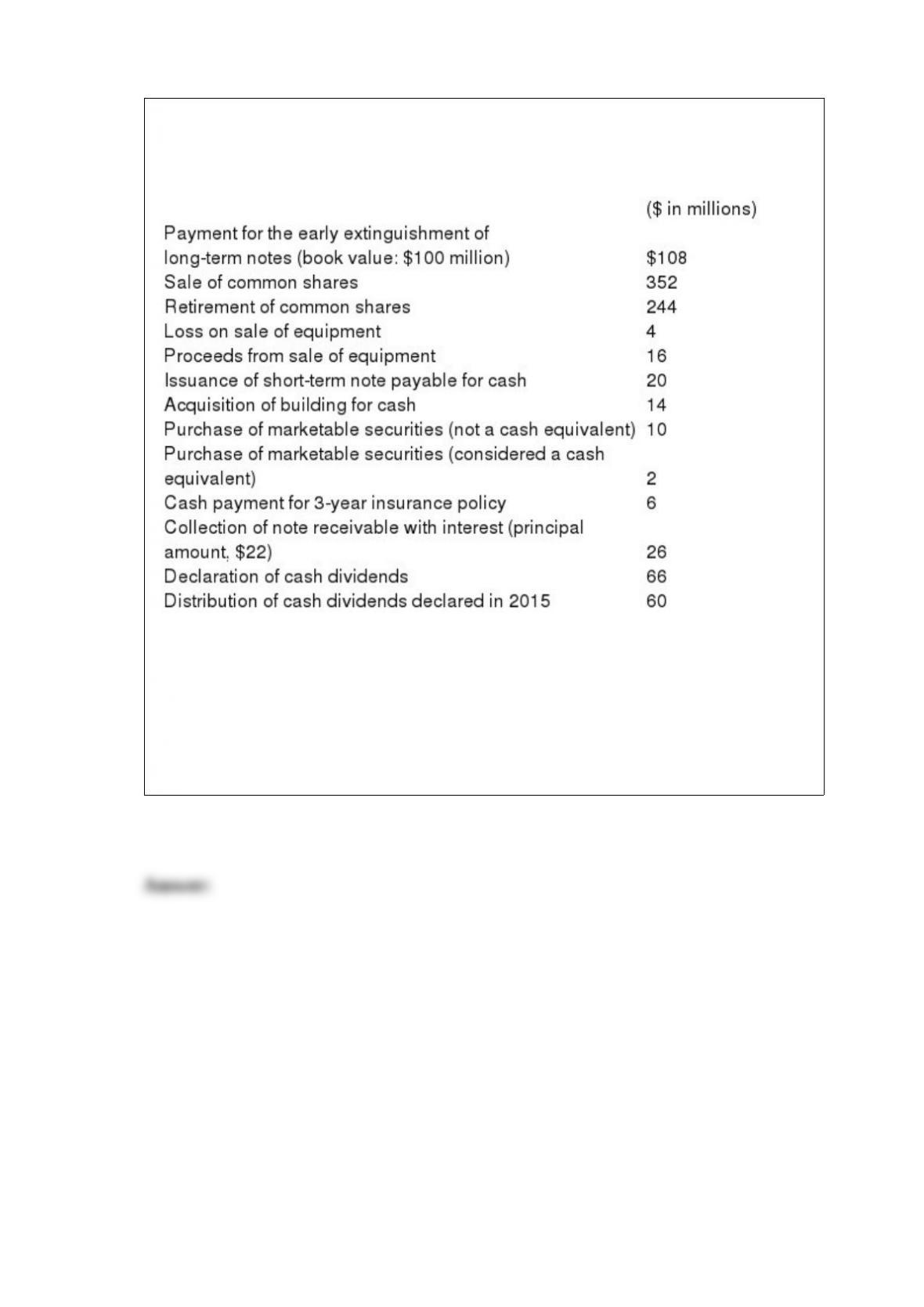

In preparation for developing its statement of cash flows for the year ended December

31, 2016, Millennium Solutions, Inc., collected the following information:

Required:

1) In Millennium’s statement of cash flows, what were net cash inflows (or outflows)

from investing activities for 2016?

2) In Millennium’s statement of cash flows, what were net cash inflows (or outflows)

from financing activities for 2016?

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Accrued property taxes were paid.

Topic Area:

Topic Area:

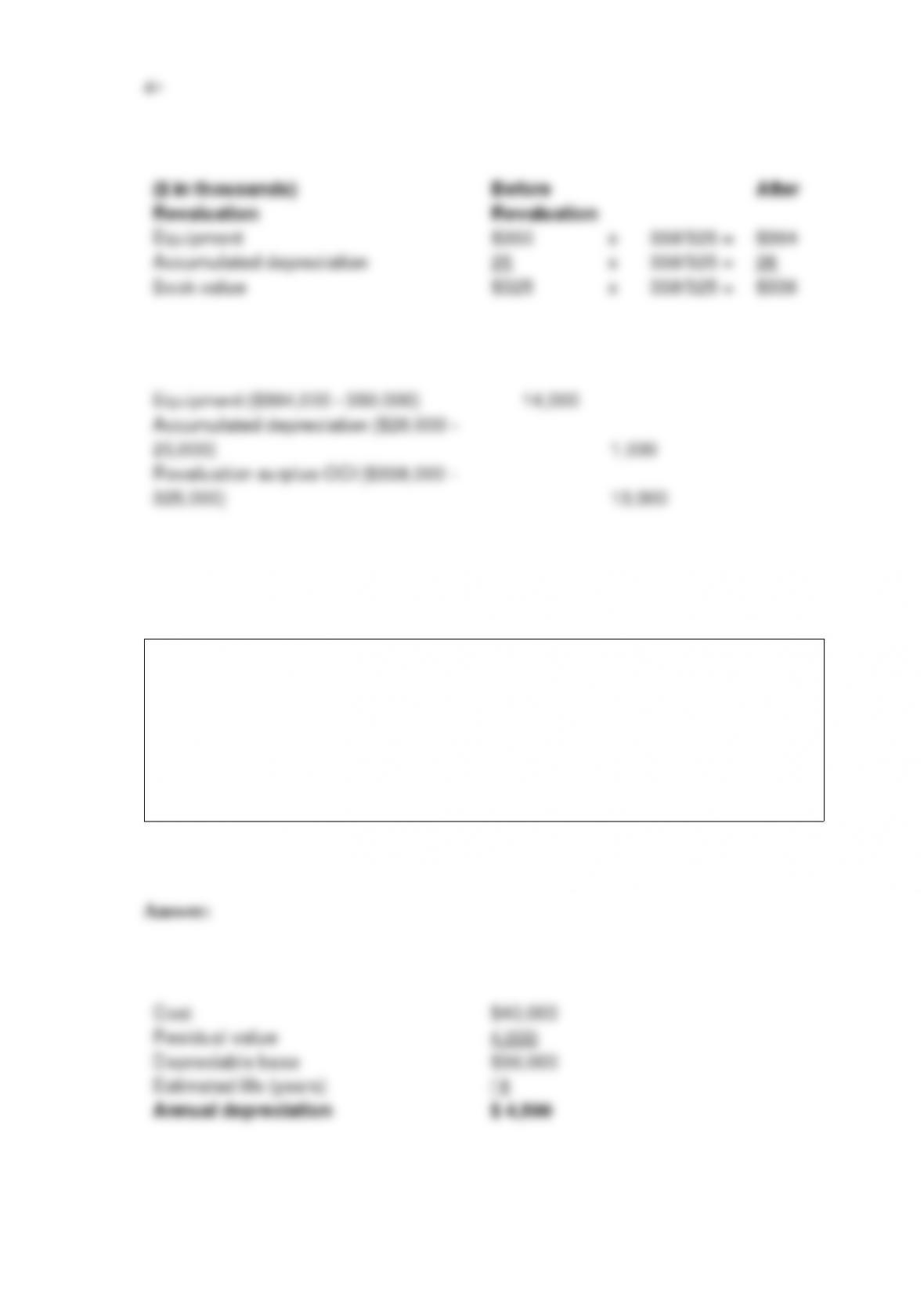

Synthetic Fuels Corporation prepares its financial statements according to IFRS. On

June 30, 2016, the company purchased equipment for $350,000. The equipment is

expected to have a seven-year useful life with no residual value. Synthetic uses the

straight-line depreciation method for all depreciable assets. On December 31, 2016, the

end of the company’s fiscal year, Synthetic chooses to revalue the machinery to its fair

value of $299,000.

Required:

1> Calculate depreciation for 2016.

2> Prepare the journal entry at the end of 2016 to record the revaluation of the

equipment.

3> Calculate depreciation for 2017.

4> Repeat requirement 2 assuming that the fair value of the equipment at the end of

2016 is $338,000.

On January 1, 2016, Morrow Inc. purchased a spooler at a cost of $40,000. The

equipment is expected to last eight years and have a residual value of $4,000. During its

eight-year life, the equipment is expected to produce 250,000 units of product. In 2016

and 2017, 42,000 and 76,000 units respectively were produced. Required:

Compute depreciation for 2016 and 2017 and the book value of the spooler at

December 31, 2016 and 2017, assuming the straight-line method is used.