Revenue is not recognized under the realization principle unless the earnings process is

complete or virtually complete and there is reasonable certainty about the expected

collection of the asset received.

Periodic interest expense is the stated interest rate times the amount of debt outstanding

during the period.

The revenue/expense approach emphasizes determining the appropriate amounts of

revenue and expense in each reporting period.

Comprehensive income is another term for net income.

Under IFRS, the term “probable” indicates a threshold of probability that is

substantially more than a 50 percent chance of occurrence.

Mandatorily redeemable preferred stock is reported as a liability.

Conceptually, the service method provides a better matching of costs and benefits in

amortizing prior service cost than does the straight-line method.

In IFRS, the conceptual framework indicates appropriate accounting when a more

specific accounting standard does not apply.

Recognition of franchise fee revenue is dependent on judgments of both substantial

performance and expected collection of fees.

Giada Foods reported $940 million in income before income taxes for 2016, its first

year of operations. Tax depreciation exceeded depreciation for financial reporting

purposes by $100 million. The company also had non-tax-deductible expenses of $80

million relating to permanent differences. The income tax rate for 2016 was 35%, but

the enacted rate for years after 2016 is 40%. The balance in the deferred tax liability in

the December 31, 2016, balance sheet is:

a. $16 million.

b. $35 million.

c. $40 million.

d. $56 million.

The interest rate that is printed on the bond certificate is referred to as any of the

following except:

a. Stated rate.

b. Contract rate.

c. Nominal rate.

d. Effective rate.

When the interest payment dates are March 1 and September 1, and notes are issued on

July 1, the amount of interest expense to be accrued at December 31 of the year of issue

would:

a. Not be required.

b. Be for six months.

c. Be for four months.

d. Be for 10 months.

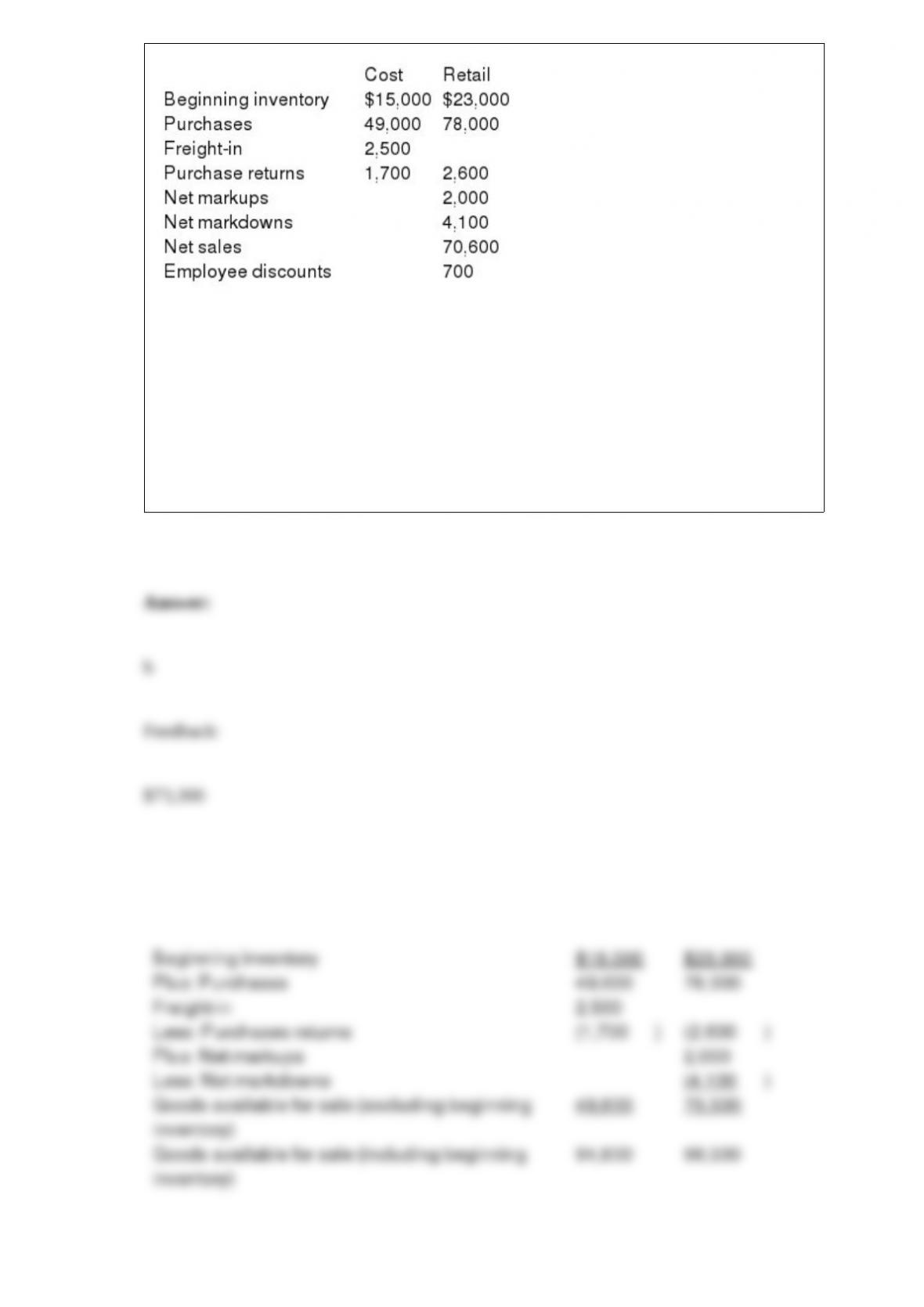

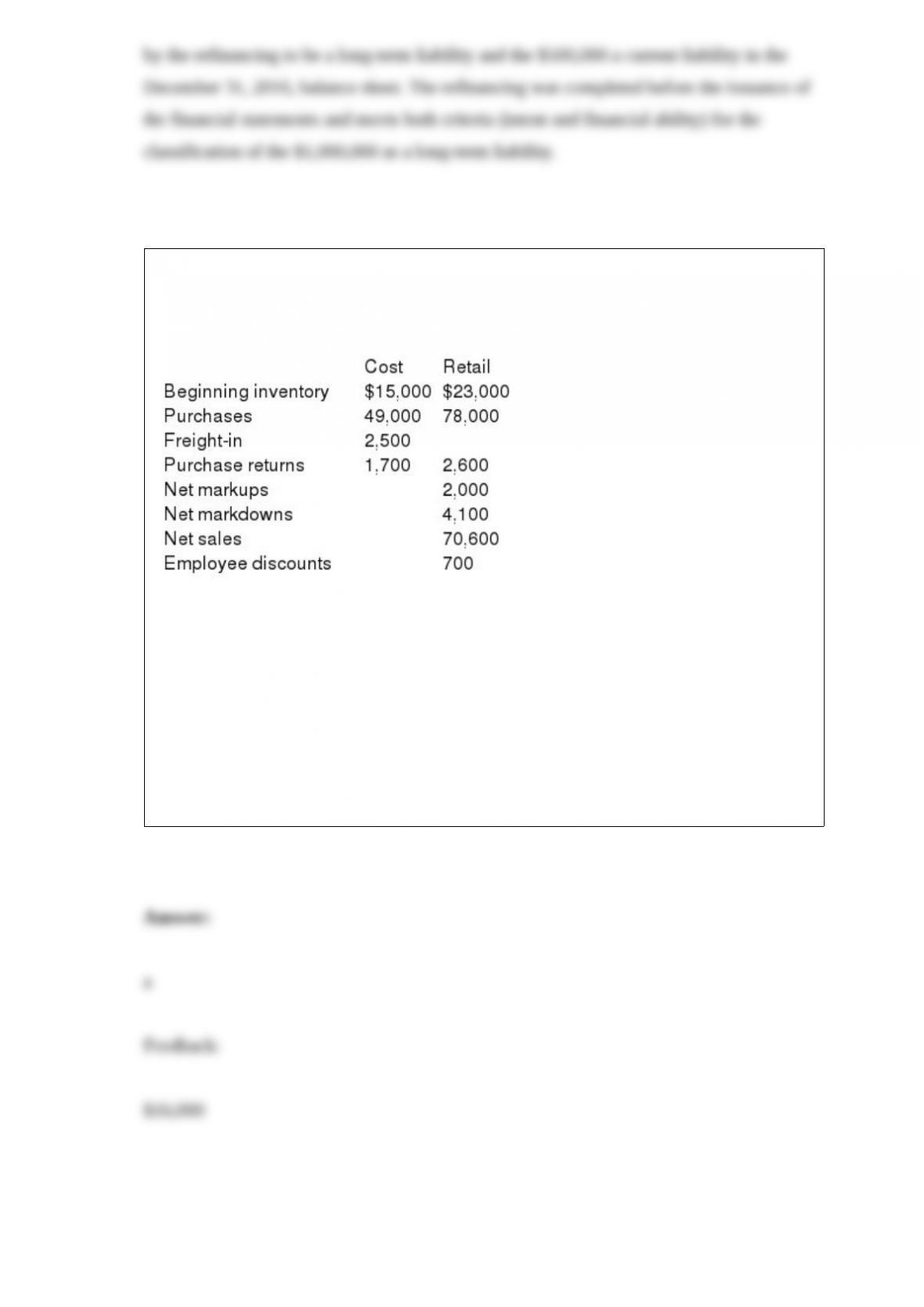

Harvey’s Junk Jewelry started business January 1, 2016, and uses the LIFO retail

method to estimate ending inventory. Listed below is data accumulated for the year

ended December 31, 2016:

The denominator for the current period’s cost-to-retail percentage is:

a. $ 96,300.

b. $ 73,300.

c. $101,000.

d. $ 81,500.

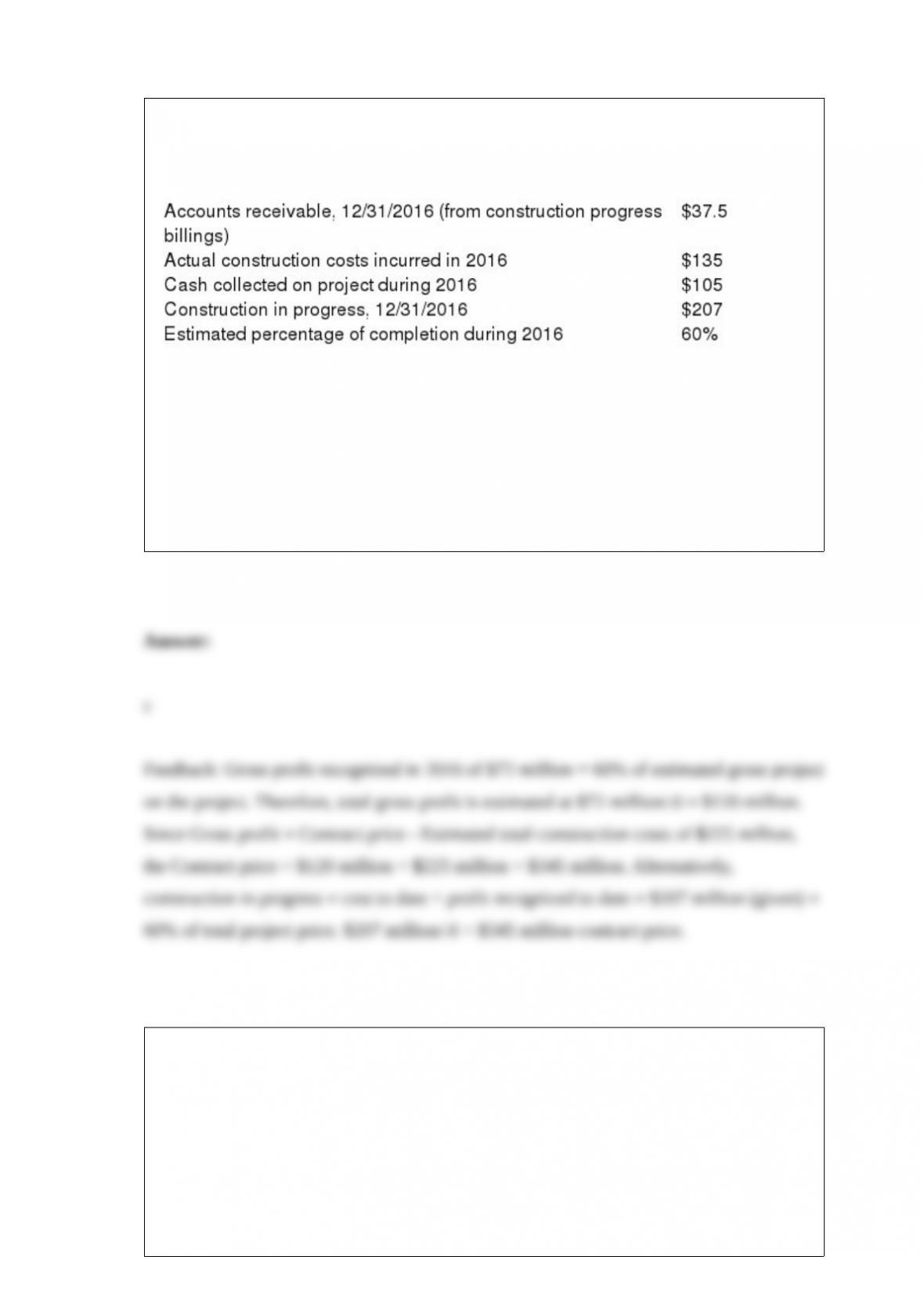

In 2016, Cupid Construction Co. (CCC) began work on a two-year fixed price contract

project. CCC recognizes revenue over time according to percentage of completion for

this contract, and provides the following information (dollars in millions):

What is the fixed contract price for CCC’s project?

a. $120 million.

b. $225 million.

c. $345 million.

d. $349.5 million.

Which of the following is an example of a variable consideration?

a. John is expected to receive $100 for his tutoring services provided that he keeps track

of his hours.

b. Melody’s Piano will get paid for the 50 pianos sold provided that the pianos are

non-defective after the customer takes control.

c. Cantankerous Computers gets paid a base amount for every repair plus an additional

hourly fee of $10.

d. Excellent Electronics has a 10% mail-in rebate program for the Model X-001 speaker

system. The company sold $10,000 worth of systems and believes there is a 50%

chance that rebates will be redeemed.

Payment of retirement benefits:

a. Increases the PBO.

b. Increases the ABO.

c. Reduces the GBO.

d. Reduces the PBO.

On January 1, 2016, G Corporation agreed to grant all its employees two weeks paid

vacation each year, with the stipulation that vacations earned each year can be taken the

following year. For the year ended December 31, 2016, G’s employees each earned an

average of $800 per week. A total of 500 vacation weeks earned in 2016 were not taken

during 2016. Wage rates for employees rose by an average of 5 percent by the time

vacations actually were taken in 2017. What is the amount of G’s 2017 wages expense

related to 2016 vacation time?

a. $ 0.

b. $ 20,000.

c. $400,000.

d. $420,000.

XYZ Company leased equipment to West Corporation under a lease agreement that

qualifies as a capital lease to West but not as a result of a bargain purchase option or a

title transfer. The present value of the asset is $600,000. The expected economic life of

the asset is 10 years. The lease term is five years. Using the straight-line method, what

would West record as annual depreciation?

a. $120,000.

b. $61,000.

c. $60,000.

d. $0.

The amount of cash paid annually for unfunded postretirement health benefit plans,

assuming they are not independently insured, usually is equal to:

a. The amount required by the actuarial formula.

b. The present value of future benefits.

c. The amount necessary to cover future benefits.

d. The amount necessary to pay the current year’s health care cost.

On December 31, 2016, L Inc. had a $1,500,000 note payable outstanding, due July 31,

2017. L borrowed the money to finance construction of a new plant. L planned to

refinance the note by issuing long-term bonds. Because L temporarily had excess cash,

it prepaid $500,000 of the note on January 23, 2017. In February 2017, L completed a

$3,000,000 bond offering. L will use the bond offering proceeds to repay the note

payable at its maturity and to pay construction costs during 2017. On March 13, 2017, L

issued its 2016 financial statements. What amount of the note payable should L include

in the current liabilities section of its December 31, 2016, balance sheet?

a. $ 0.

b. $ 500,000.

c. $1,000,000.

d. $1,500,000.

Harvey’s Junk Jewelry started business January 1, 2016, and uses the LIFO retail

method to estimate ending inventory. Listed below is data accumulated for the year

ended December 31, 2016:

To the nearest thousand, the estimated ending inventory at cost is (round cost-to-retail

ratio to whole percentage):

a. $16,000.

b. $15,000.

c. $13,000.

d. $19,000.

A loss on the sale of machinery should be reported in the statement of cash flows as:

a. An adjustment to net income under the indirect method.

b. An operating activity under the direct method.

c. An investing activity cash outflow.

d. A noncash investing activity.

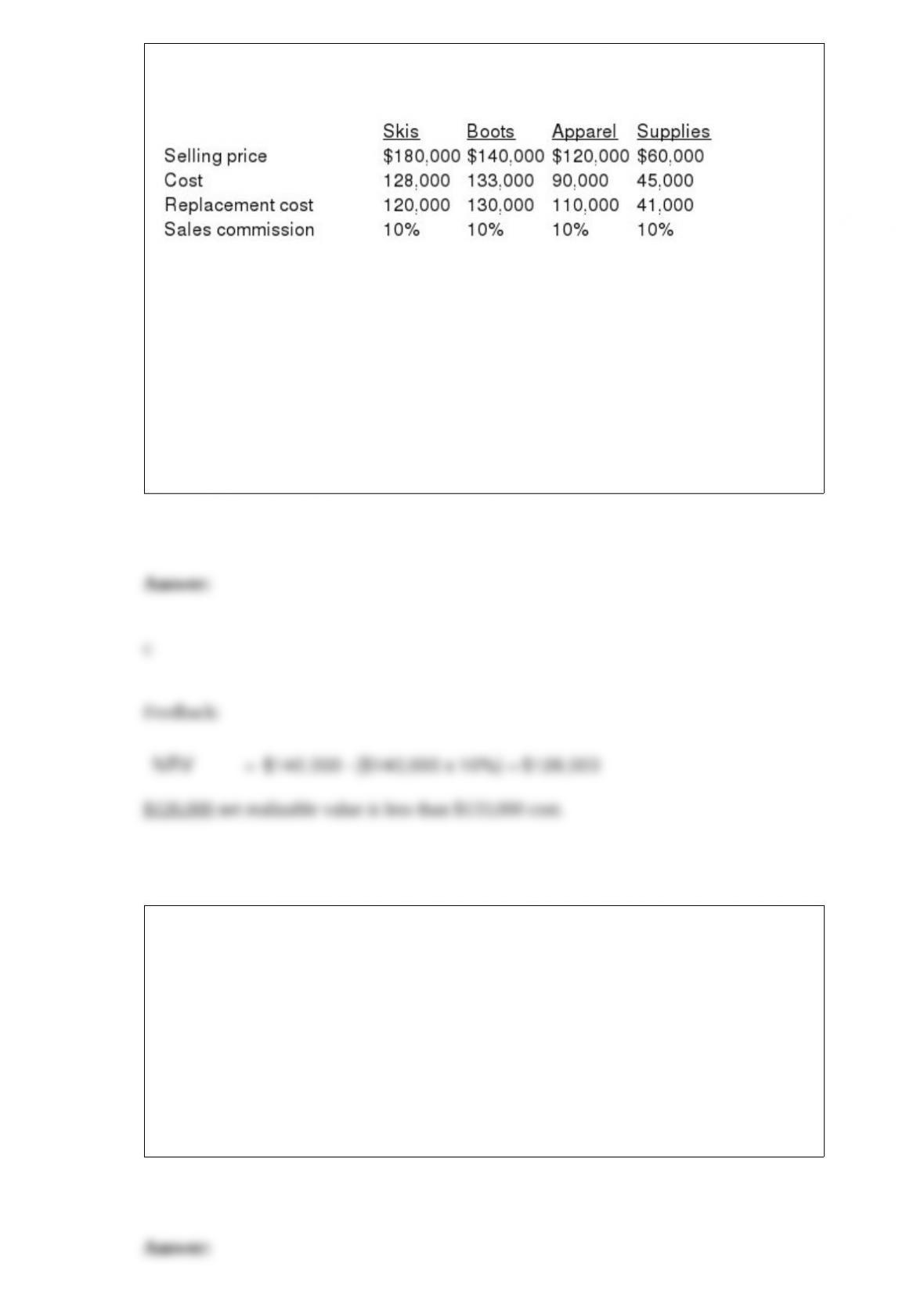

Data related to the inventories of Alpine Ski Equipment and Supplies is presented

below:

In applying the lower of cost and net realizable value rule, the inventory of boots would

be valued at:

a. $140,000.

b. $133,000.

c. $126,000.

d. $130,000.

A series of equal periodic payments in which the first payment is made one

compounding period after the date of the contract is:

a. A deferred annuity.

b. An ordinary annuity.

c. An annuity due.

d. A delayed annuity.

Annual depreciation expense on a building purchased a few years ago (using the

straight-line method) is $5,000. The cost of the building was $100,000. The current

book value of the equipment (January 1, 2016) is $85,000. At the time of purchase, the

asset was estimated to have a zero salvage value. On January 1, 2016, the company

decided to reduce the original useful life by 25% and to establish a salvage value of

$5,000. The firm also decided double-declining-balance depreciation was more

appropriate. Ignore tax effects.

Required:

(1.) Record the journal entry, if any, to report the accounting change.

(2.) Record the annual depreciation for 2016.

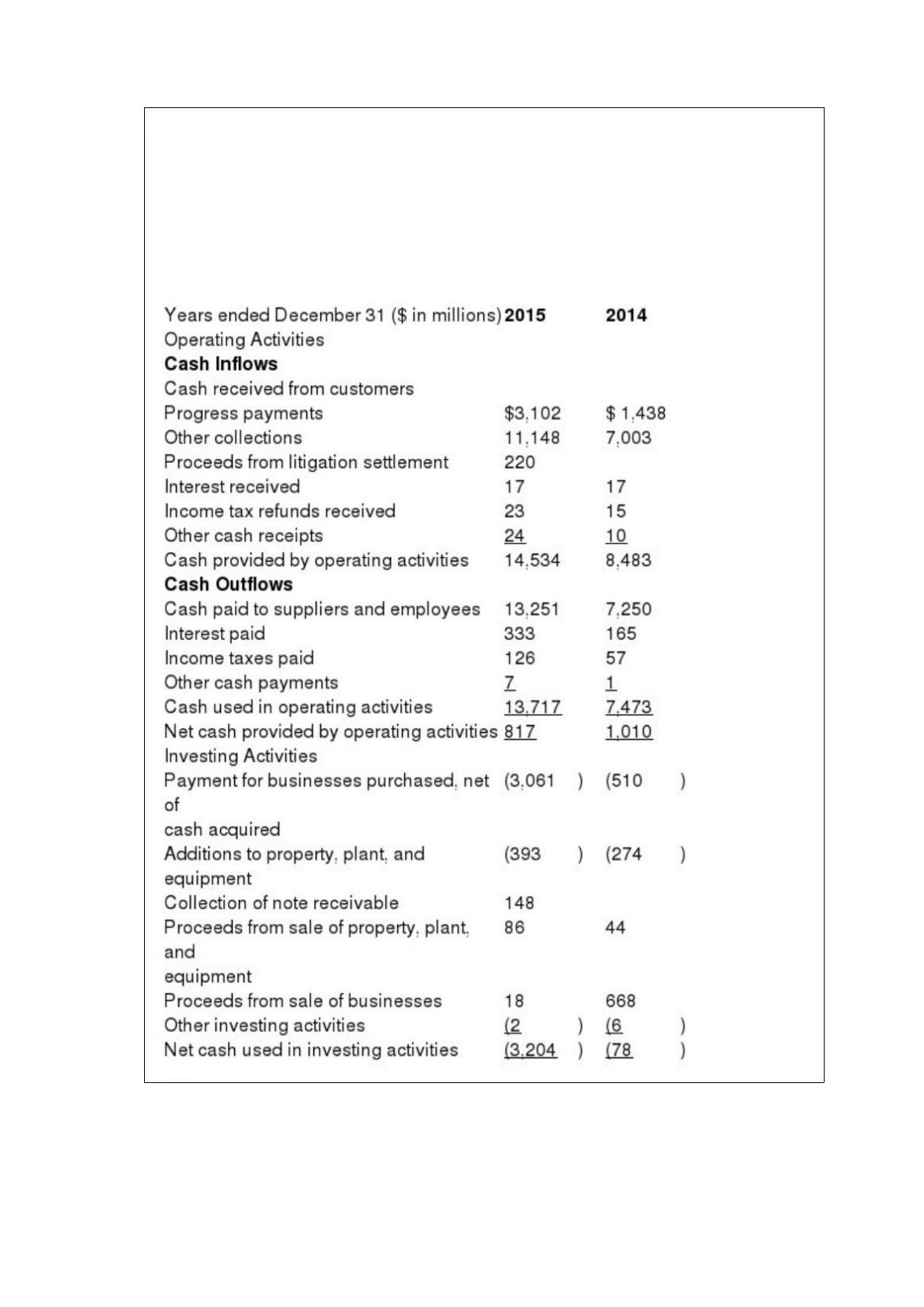

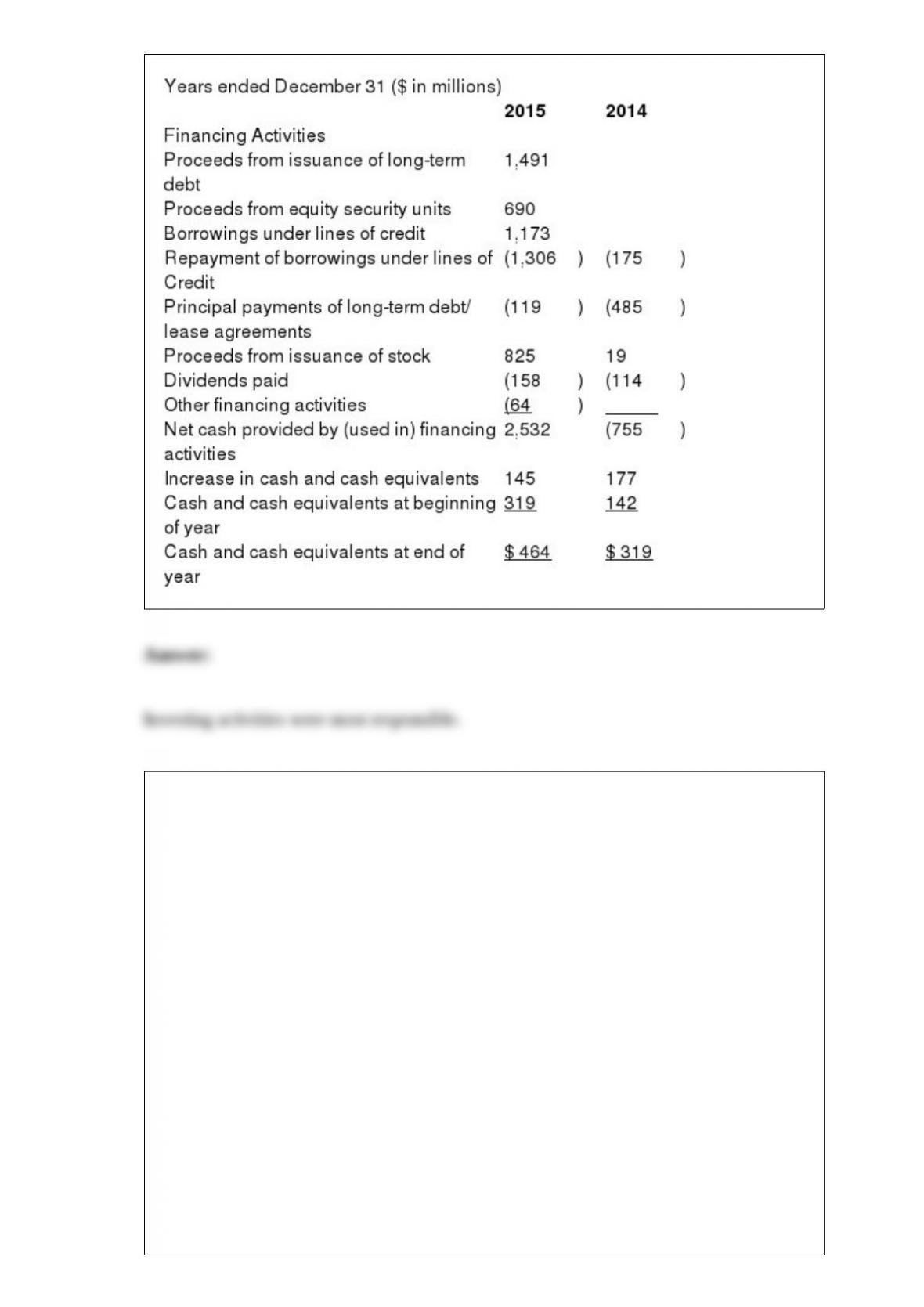

Which type of activity (operating, investing, financing) was most responsible for the

cash flow experienced by Henchman & Co. during 2015?

In its 2015 Annual Report to Shareholders, Henchman & Co. provided the following

Statement of Cash Flows:

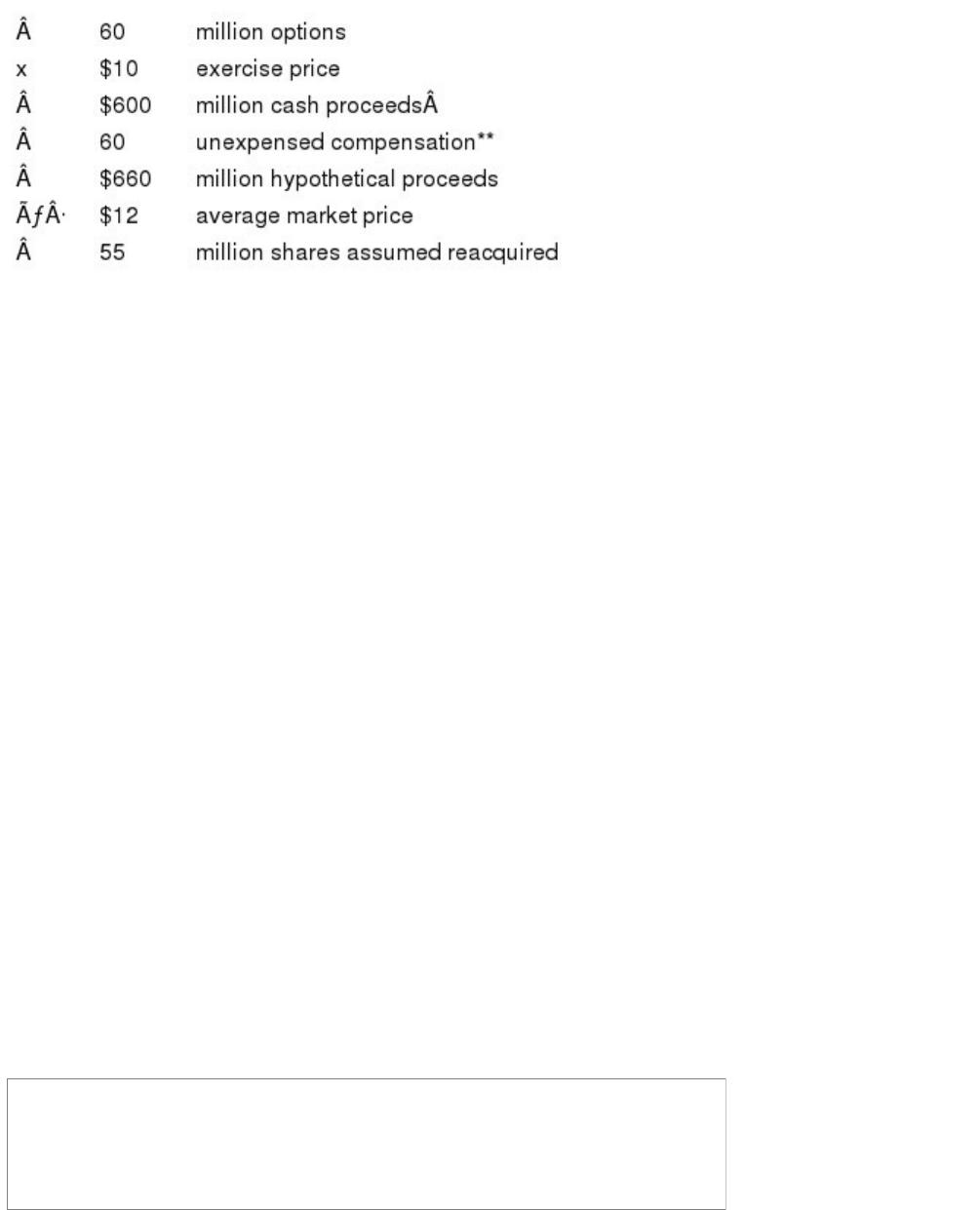

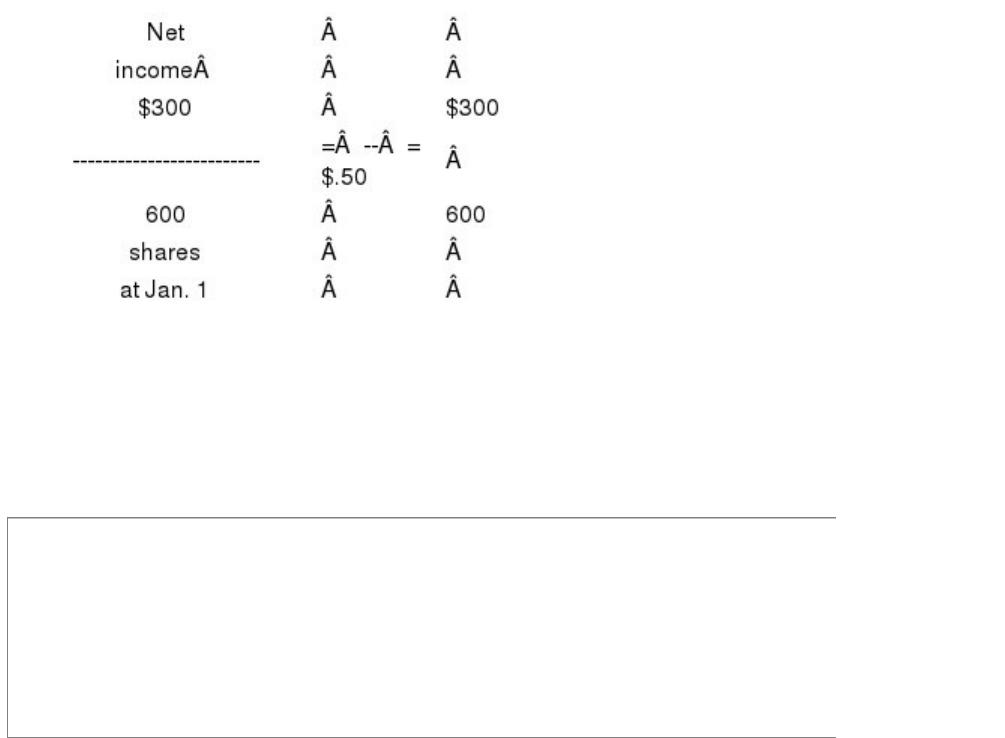

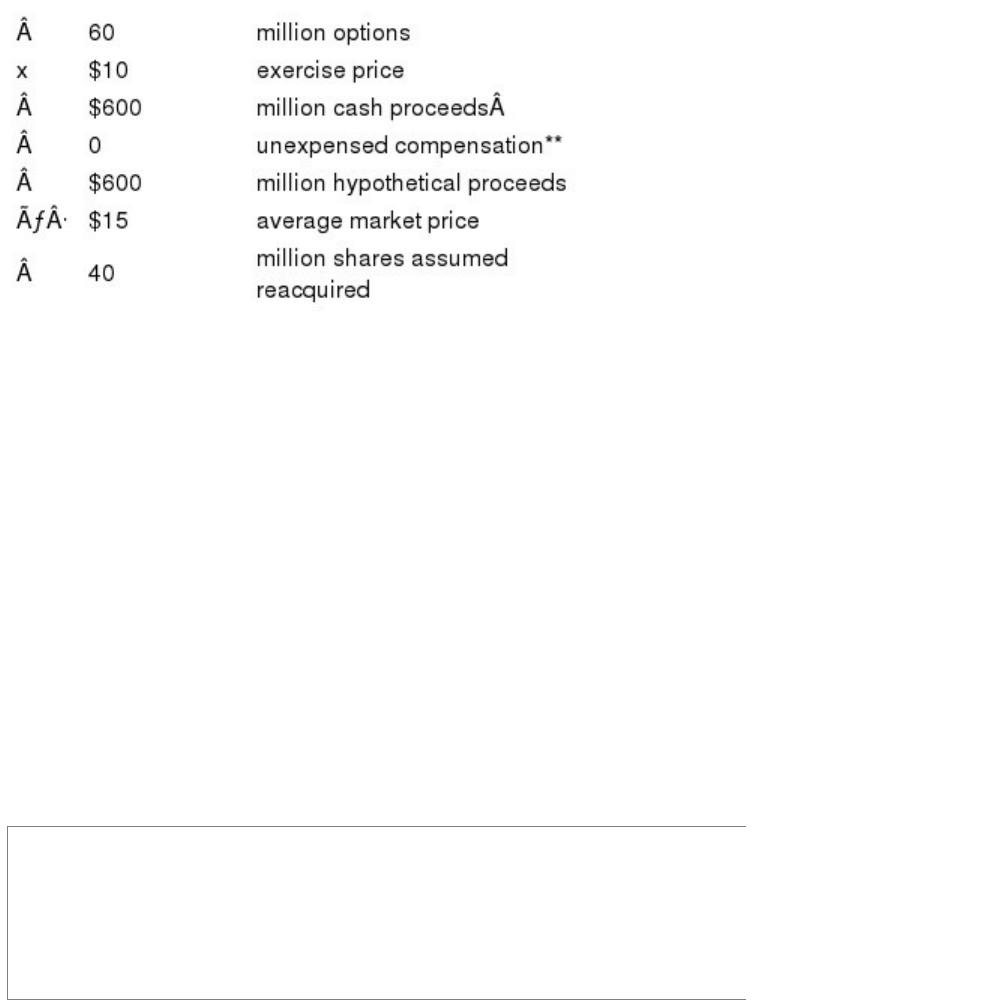

JD Co. is a calendar-year firm with 600 million common shares outstanding throughout

2016 and 2017. As part of its executive compensation plan, at January 1, 2015, the

company had issued 60 million executive stock options permitting executives to buy 60

million shares of stock for $10 per share within the next eight years, but not prior to

January 1, 2018. The fair value of the options was estimated on the grant date to be $3

per option.

In 2016, JD began granting employees stock awards rather than stock options as part of

its equity compensation plans and granted 30 million restricted common shares to

senior executives at January 1, 2016. The shares vest four years later. The fair value of

the stock was $12 per share on the grant date. The average market price of the common

shares was $12 and $15 during 2016 and 2017, respectively.

The stock options qualify for tax purposes as an incentive plan. The restricted stock

does not. The company’s net income was $240 million and $300 million in 2016 and

2017, respectively. Its income tax rate is 40%.

Required:

1) Determine basic and diluted earnings per share (rounded to 2 decimal places) for JD

in 2016.

2) Determine basic and diluted earnings per share for JD (rounded to 2 decimal places)

in 2017.

Why are “cash equivalents” included as part of cash in the statement of cash flows?

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

On January 1, 2016, Club Company purchased 10% bonds, dated January 1, 2016, with

a face amount of $20 million. The bonds mature in 2025 (10 years). For bonds of

similar risk and maturity, the market yield is 12%. Interest is paid semiannually on June

30 and December 31.

Required:

1> Determine the price of the bonds at January 1, 2016.

2> Prepare the journal entry to record the bond purchase by Club on January 1, 2016.

3> Prepare the journal entry to record interest on June 30, 2016, using the straight-line

method.

4> Prepare the journal entry to record interest on December 31, 2016, using the

straight-line method.

Heidi Baby Products issued 8% bonds with a face amount of $320 million on January 1,

2016. The bonds sold for $300 million. For bonds of similar risk and maturity the

market yield was 9%. Upon issuance, Heidi elected the option to report these bonds at

their fair value. On June 30, 2016, the fair value of the bonds was $310 million as

determined by their market value on the NASDAQ. Will Heidi report a gain or will it

report a loss when adjusting the bonds to fair value? If the change in fair value is

attributable to a change in the general (risk-free) interest rate, did the rate increase or

decrease? If the change in fair value is attributable to a change in the general (risk-free)

interest rate, is the gain or loss reported as part of net income? Explain.

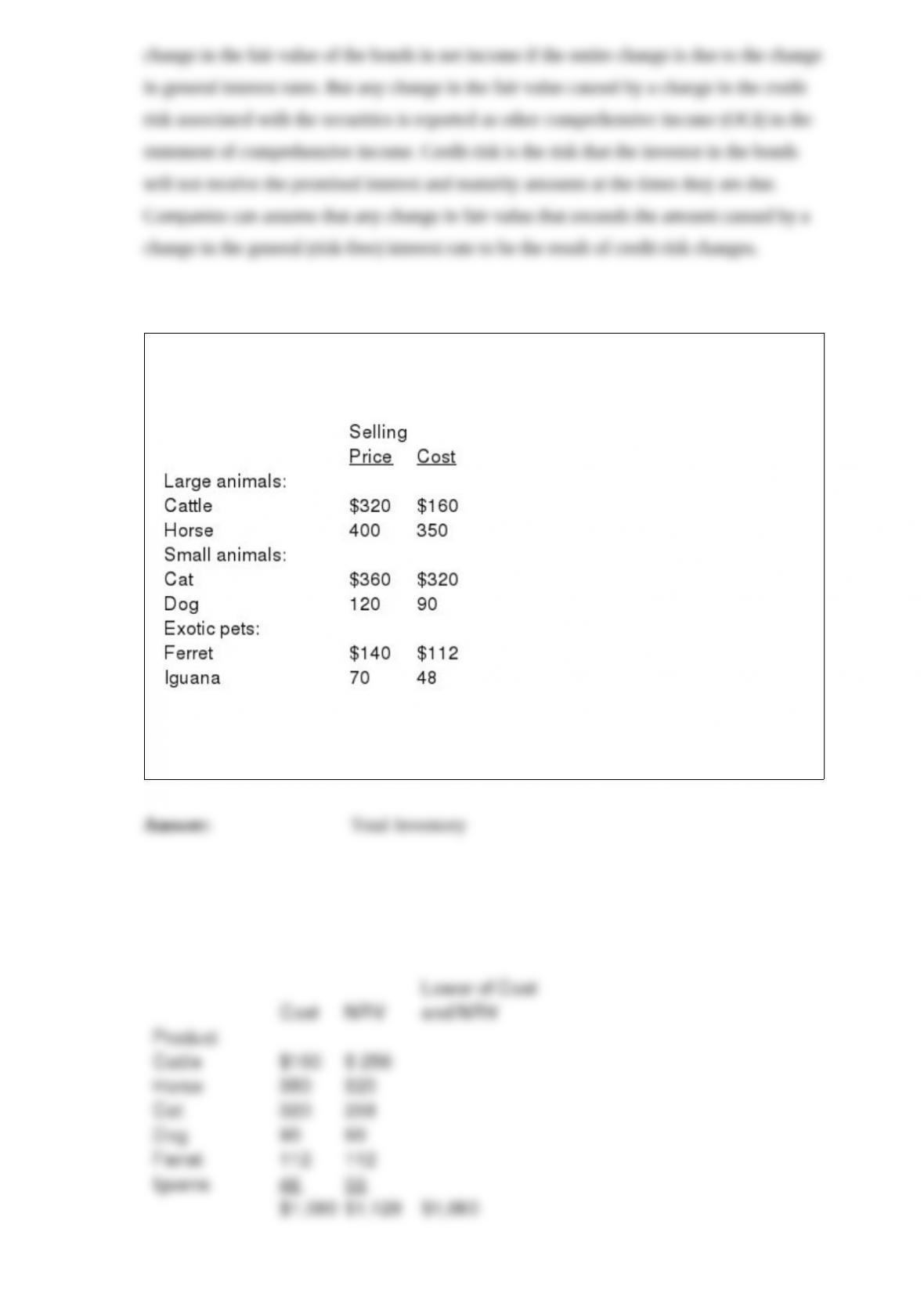

Weldon Animal Feeds has developed the following data for lower of cost and net

realizable valuation for its products (in thousands):

The costs to sell are 20% of selling price. Required: Determine the reported inventory

value assuming the lower of cost and net realizable value rule is applied to the total

inventory.

Is depreciation a source of cash? Explain.

On January 1, 2016, Rare Bird Ltd. purchased 12% bonds dated January 1, 2016, with a

face amount of $20 million. The bonds mature in 2025 (10 years). For bonds of similar

risk and maturity, the market yield is 10%. Interest is paid semiannually on June 30 and

December 31.

Required:

1> Determine the price of the bonds at January 1, 2016.

2> Prepare the journal entry to record the bond purchase by Rare Bird on January 1,

2016.

3> Prepare the journal entry to record interest on June 30, 2016, using the effective

interest method.

4> Prepare the journal entry to record interest on December 31, 2016, using the

effective interest method.