Discounting a future amount of a cash receipt will determine the present value of that

receipt.

Having a liability that is fixed in terms of a foreign currency results in a loss for the

debtor if the exchange rate falls between the transaction date and the payment date.

The most common method to allocate joint costs is in proportion to the relative sales

value of the products.

Common fixed costs jointly benefit several parts of the business and would not change

significantly even if one of the parts of the business were discontinued.

Preferred stockholders generally do not have the same voting rights as do common

stockholders in a corporation.

A statement of stockholders’ equity is not a required financial statement and need not be

prepared along with a statement of retained earnings.

While the price-earnings ratio is computed using historical earnings, it reflects

investors’ expectations of future earnings.

The acquiring of a subsidiary company by a publicly traded company would be an

example of a capital expenditure.

Product costs are charged directly to expense accounts.

Short-term investments in marketable securities may not be reported in the balance

sheet at values higher than original cost.

In capital budgeting, the investment proposal with the shortest payback period always

has the highest rate of return.

Most disclosures appear within the body of the financial statements; however, a few

disclosures may also appear in the notes that accompany the financial statements.

The payment of cash dividends to common stockholders is classified as a financing

activity on the statement of cash flows whereas payment of a cash dividend to preferred

stockholders is classified as an investing activity.

To increase return on sales, a manager could decrease cost of goods sold while

increasing revenues.

Financial assets may be current or long-term assets.

A major purpose of using an Allowance for Doubtful Accounts is to recognize

uncollectible accounts expense in the same accounting period as the related sales which

caused the expense.

A budget provides a comprehensive plan enabling multiple departments to work

together in a coordinated manner.

A cost that is directly traceable to a particular center must be a variable cost.

The LIFO conformity requirement permits a company to use LIFO for tax purposes

only if the company also uses LIFO for internal reporting purposes.

A partnership has a limited life and each partner has unlimited personal liability.

Every transaction which affects an income statement account also affects a balance

sheet account.

The residual value of an asset should be subtracted from the cost of the asset when

determining the average amount invested.

If the maker of a note defaults, an entry is made which debits Accounts Receivable and

credits Notes Receivable.

Charges for depositing NSF checks are an example of a transaction that has been

recorded by the depositor but may not have been recorded by the bank.

A trial balance that balances provides proof that all transactions were correctly

journalized and posted to the ledger.

A dollar that is stronger than the British pound would make travel to the United States

more attractive to British citizens.

The statement of financial position and the income statement are one and the same.

An accounting practice can become a “generally accepted accounting principle” through

widespread use, even if the practice is not mentioned in the official pronouncements of

the accounting standard-setting organizations.

Stockholders of a corporation are personally liable for the debts of the corporation if all

shares of stock are owned by the officers of the corporation.

An annuity due assumes the cash flow will occur at the beginning of the period.

Stock splits:

A. Allow management to conserve cash.

B. Give stockholders more shares.

C. Cause no change in total assets, liabilities, or stockholders’ equity.

D. Allow management to conserve cash, give stockholders more shares, and cause no

change in total assets, liabilities, or stockholders’ equity.

On November 1, 2014, Salem Corporation sold land priced at $900,000 in exchange for

a 6%, six-month note receivable.

Refer to the information above. Salem’s balance sheet at December 31, 2014 includes

which of the following as a result of the sale of land on November 1?

A. Notes Receivable of $900,000 and Interest Receivable of $9,000.

B. Notes Receivable of $927,000 and Interest Receivable of $9,000.

C. Notes Receivable of $900,000 and Interest Receivable of $27,000.

D. Notes Receivable of $900,000 only.

A cost that has already been incurred and cannot be changed is called a(n):

A. Opportunity cost.

B. Out-of-pocket cost.

C. Joint cost.

D. Sunk cost.

At the beginning of the year, Robert Company’s Allowance for Doubtful Accounts had a

$3,200 credit balance. During January, a provision of 2% of sales was made for

uncollectible accounts expense. During January, sales totaled $350,000, and $2,900 of

accounts receivable were written off as worthless. No recoveries of accounts previously

written off were made during the month. Robert’s financial statements for January

show:

A. Allowance for Doubtful Accounts with a credit balance of $10,200.

B. Allowance for Doubtful Accounts with a credit balance of $7,300.

C. Uncollectible Accounts Expense of $9,900.

D. Uncollectible Accounts Expense of $4,100.

To compute a future amount from a present value, we need to know:

A. The future value and length of time.

B. The interest rate and length of time.

C. The future annuity amount.

D. The present annuity amount.

The time value of money is based on the idea that:

A. The value of money in the future equals the interest received in the present.

B. The value of money in the future will be greater than an amount available today.

C. The value of money at present over some length of time will be reduced by inflation.

D. The future value of money will become the current value as time passes.

Grand Gimmicks Company produces a single product with a current selling price of

$170. Variable costs are $130 per unit, and fixed costs per month average $6,240.

Management is considering increasing the selling price to $190 per unit. Assume that

the variable cost per unit of the product and monthly fixed expenses will not change as

a result of the proposed increase in selling price.

Refer to the information above. At the current selling price of $170 per unit, closest to

what dollar volume of sales per month is required for Grand Gimmicks to break-even?

(Round your intermediate percentage to one decimal place.)

A. $6,178.

B. $8,299.

C. $26,553.

D. $20,800.

Net income in a partnership may not be distributed to the partners:

A. As a salary allowance.

B. As interest on beginning capital.

C. In a fixed ratio.

D. In the form of dividends.

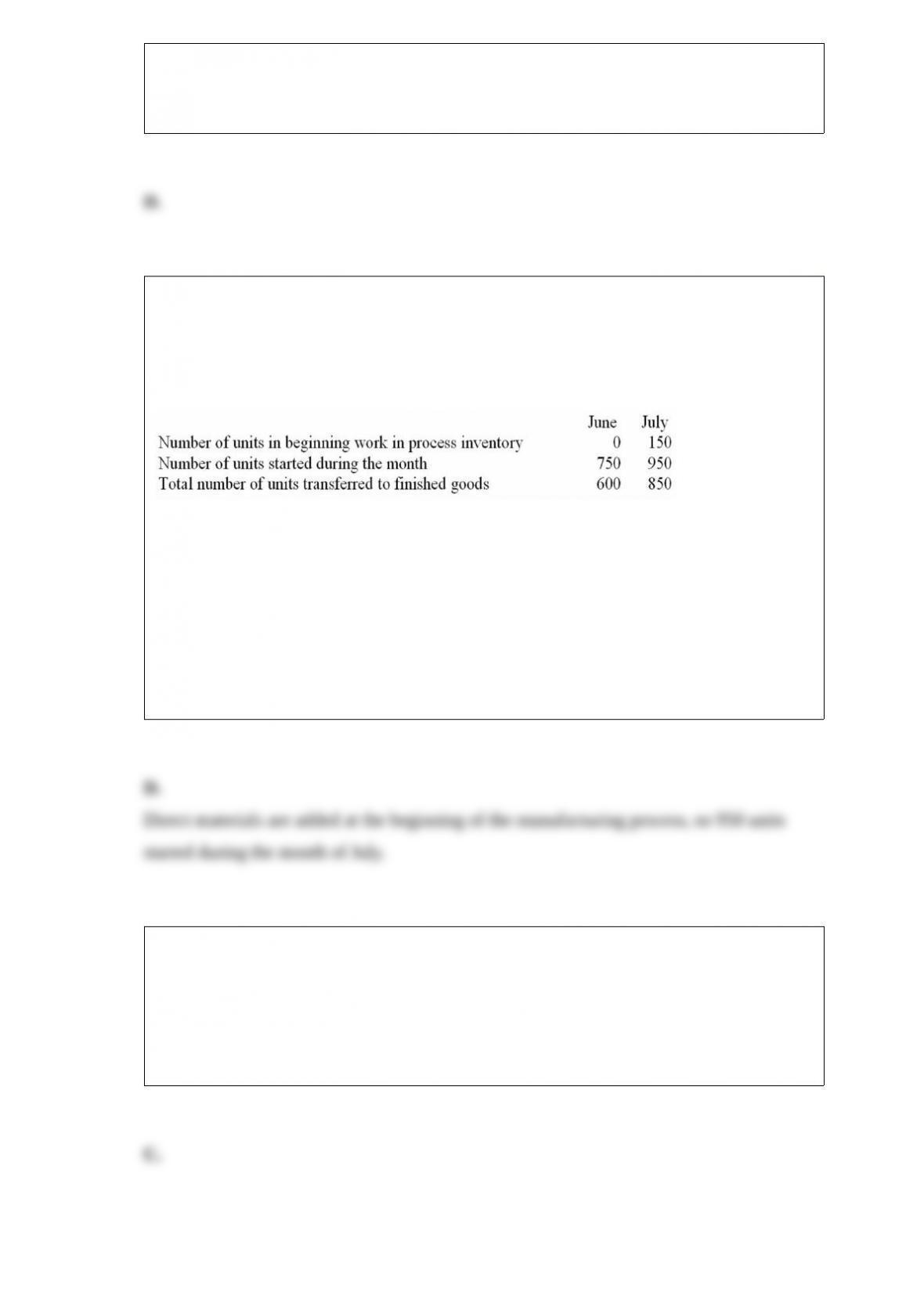

Aves Treats, Inc. produces bird seeds. All direct materials used in the production

process are added at the beginning of the manufacturing process. Labor and overhead

are added evenly thereafter, as each unit is mixed and packaged. Aves Treats uses

process costing and had the following unit production information available for the

months of June and July:

The units remaining in work in process at the end of June were 30% complete. During

the month of July, all of the beginning work in process units was completed and the

units remaining in work in process at the end of the month were 60% complete.

Refer to the information above. For the month of July, the number of equivalent units of

direct materials produced was:

A. 700.

B. 800.

C. 900.

D. 950.

Ben Dryden, president of Jet Glass, Inc, noticed a $8,000 debit to Accounts Payable in

the company’s general ledger. This debit could correspond to:

A. A $8,000 sale to a customer.

B. A purchase of equipment costing $8,000 on credit.

C. A payment of $8,000 to a supplier to settle a balance due.

D. The failure to pay this month’s $8,000 utility bill on time.

The book value of equipment:

A. Increases with the passage of time.

B. Decreases with the passage of time.

C. Remains the same with the passage of time.

D. May increase or decrease depending upon the economy.

Grand Gimmicks Company produces a single product with a current selling price of

$170. Variable costs are $130 per unit, and fixed costs per month average $6,240.

Management is considering increasing the selling price to $190 per unit. Assume that

the variable cost per unit of the product and monthly fixed expenses will not change as

a result of the proposed increase in selling price.

Refer to the information above. At the current selling price of $170 per unit, the

contribution margin ratio is closest to:

A. 23.5%.

B. 76%.

C. 34%.

D. 21%.

Adjusting entries are needed:

A. Whenever revenue is not received in cash.

B. Whenever expenses are not paid in cash.

C. Only to correct errors in the initial recording of business transactions.

D. Whenever transactions affect the revenue or expenses of more than one accounting

period.

Capital expenditures are recorded as:

A. An expense.

B. An asset.

C. A liability.

D. Income.

The measures used by an organization to provide reasonable assurance that the

organization produces reliable financial reports, complies with applicable laws and

regulations, and conducts its operations in an efficient and effective manner are

collectively referred to as:

A. Generally accepted accounting principles.

B. Financial accounting standards.

C. Securities and exchange regulations.

D. The internal control structure.

Sultan Company produces a single product. The selling price is $50 per unit, and

variable costs amount to $20 per unit. Sultan’s fixed costs per month total $80,000.

Refer to the information above. What will be Sultan’s monthly operating income if

3,700 units are sold each month?

A. $15,000.

B. $31,000.

C. $75,000.

D. $105,000.

The ratio which measures total liabilities as a percentage of total assets is called:

A. Current ratio.

B. Working capital.

C. Debt ratio.

D. Quick ratio.

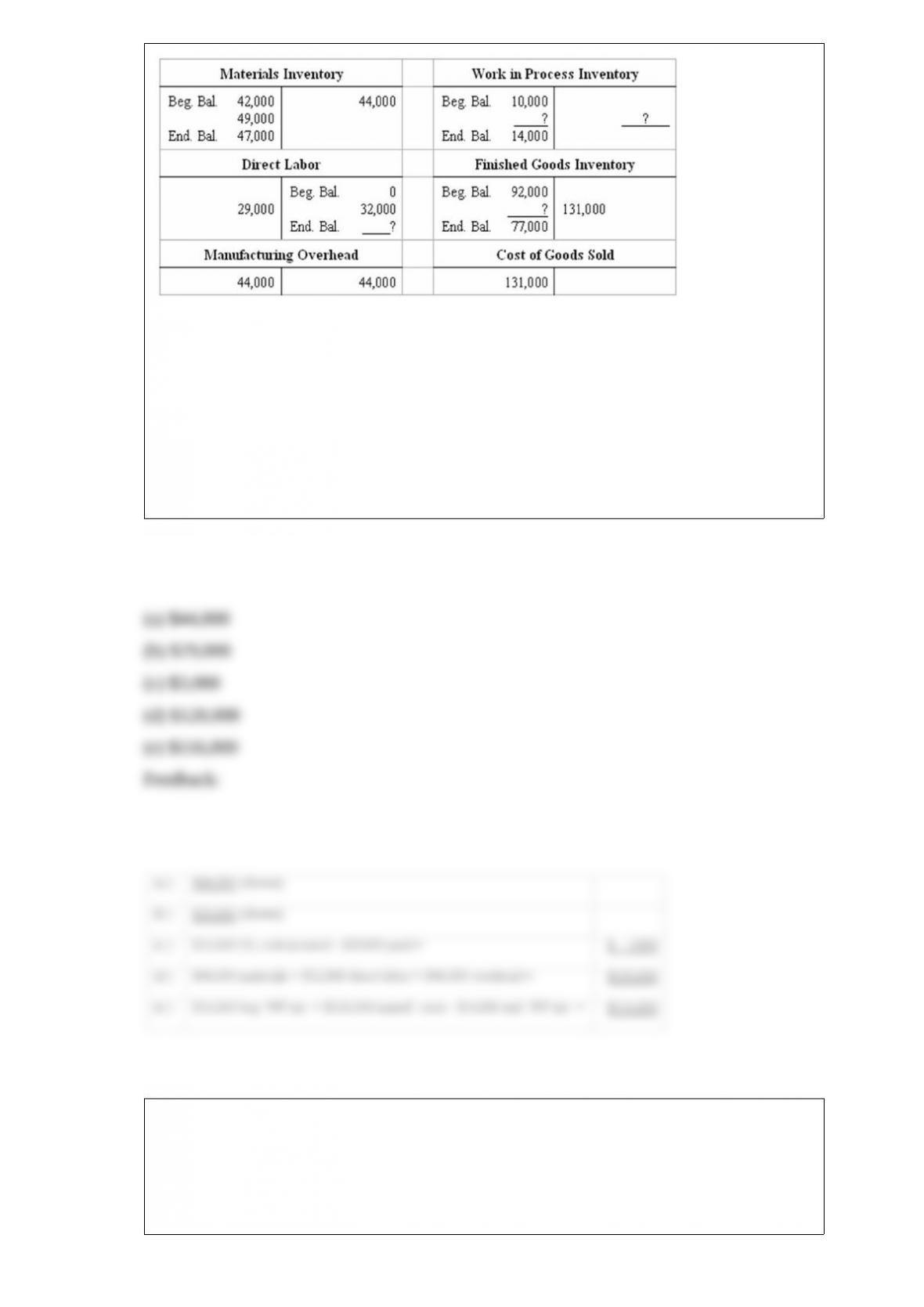

Flow of manufacturing costs

The “flow” of manufacturing costs through the ledger of Wolpe Mfg. Co. during the

month of October is summarized in the following T accounts. Certain amounts have

been omitted and are represented by question marks.

From the data supplied above, determine each of the following amounts. Some of the

required amounts already appear in the T accounts; others require a short computation.

(a) The amount of direct materials used during the month: $___________

(b) The amount paid to direct labor workers during the month: $___________

(c) The amount of accrued wages payable to direct labor workers at October 31:

$___________

(d) Total manufacturing costs charged (debited) to the Work in Process Inventory

account during the month: $___________

(e) The cost of finished goods manufactured during the month: $___________

Which of the following is not an advantage of using a standard cost system?

A. It eliminates the need for analysis of variances.

B. It facilitates establishing an effective system of responsibility accounting.

C. It requires an analysis of all aspects of operations.

D. It helps management control costs.

For financial reporting purposes, the gain or loss on the sale of a plant asset is

determined by comparing the asset’s:

A. Cost with its book value.

B. Sales price with its book value.

C. Tax basis with its book value.

D. Sales price with its tax basis.

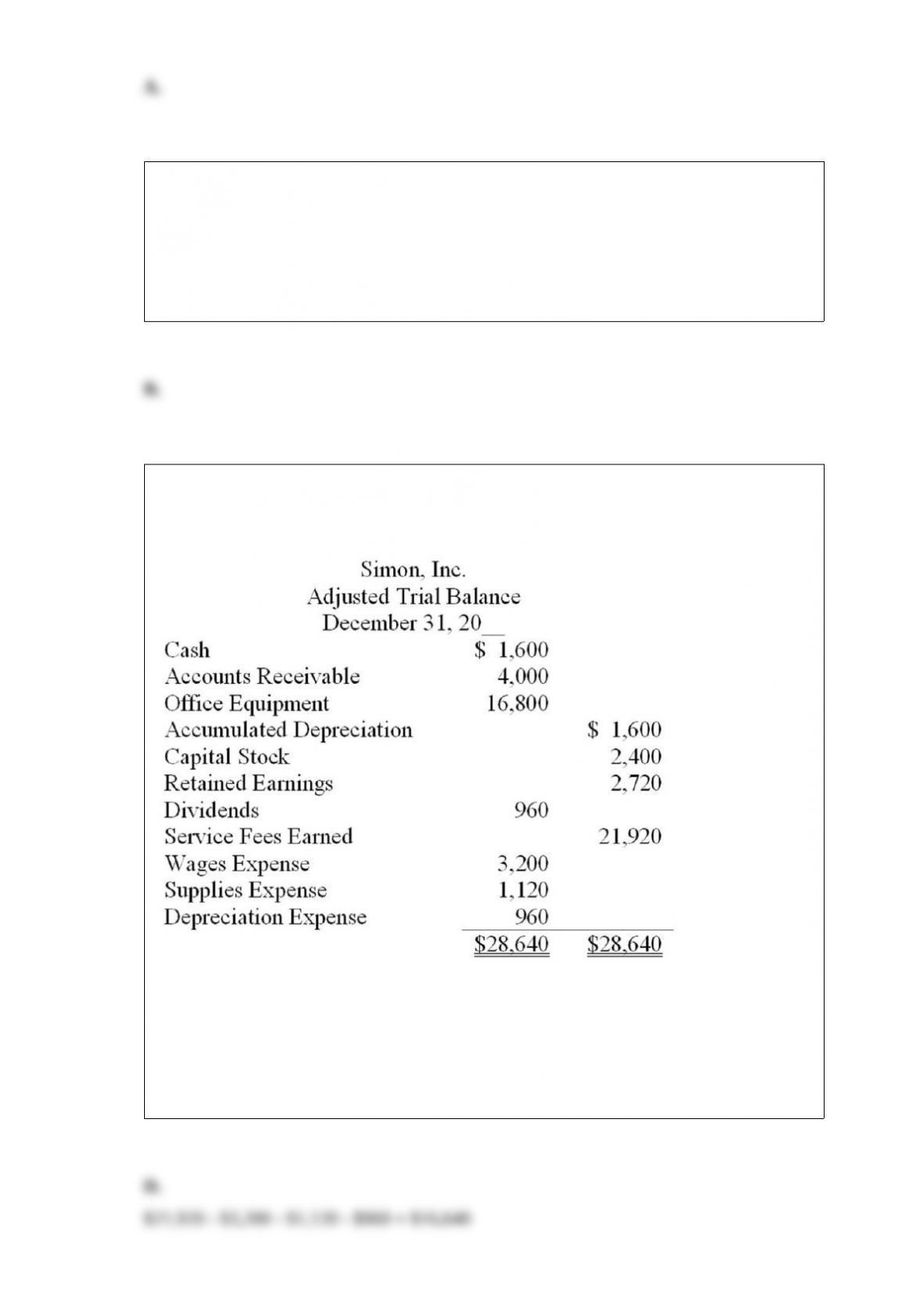

Shown below is the adjusted Trial Balance for Simon Inc., on December 31, after the

first year of operations, after adjusting entries:

Refer to the information above. Income Summary will have what balance before it is

closed?

A. $28,640.

B. $15,600.

C. $21,920.

D. $16,640.

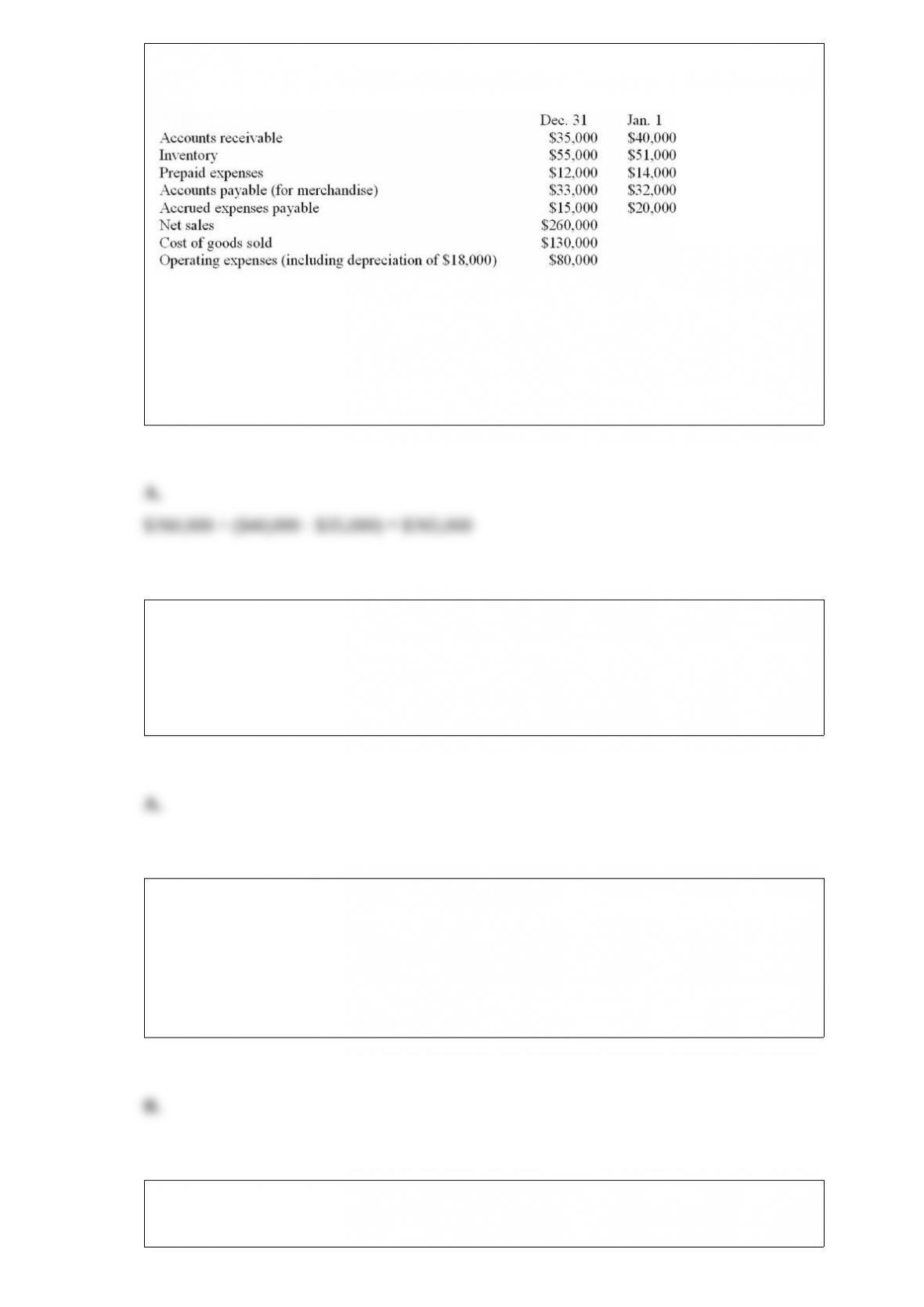

The financial statements of Seldin, Inc., provide the following information for the

current year:

Refer to the information above. Compute the amount of cash received from customers

during the current year.

A. $265,000.

B. $255,000.

C. $260,000.

D. $40,000.

Which of the following is a characteristic of financial accounting information?

A. Its preparation requires judgment.

B. It is more about the future than it is about the past.

C. None of it is based on estimates, assumptions, and judgments.

D. Notes and explanations from management are not included.

In an activity-based costing system, manufacturing overhead costs are divided into

separate:

A. Cost drivers.

B. Activity cost pools.

C. Activity bases.

D. Indirect cost centers.

Refer to the information above. The expected rate of return on average investment of

the machine is:

A. 10%.

B. 17%.

C. 18.6%.

D. 48%.

A rising gross profit rate most strongly suggests:

A. An increase in physical sales volume.

B. Strong consumer demand for the company’s products.

C. Intense competition.

D. Increased short-term solvency.

Shrek Cyclery sells a bicycle to W. O’Connor, a customer who uses Empress Charge (a

national credit card, but not issued by a bank). In recording this sale, Shrek Cyclery

should record:

A. An account receivable from W. O’Connor.

B. A cash receipt.

C. An account receivable from Empress Charge.

D. A small increase in the allowance for doubtful accounts.

If a business ceases operations and liquidates, which of the following will be paid last?

A. Owners.

B. General creditors.

C. Employees.

D. Creditors who have collateral for their loans.

Cranston Instrumentation sold a depreciable asset for cash of $150,000. The original

cost of the asset was $600,000. Cranston recognized a gain of $22,500 on the sale.

What was the amount of accumulated depreciation on the asset at the time of its sale?

A. $472,500.

B. $127,500.

C. $577,500.

D. $495,000.

Interest that has accrued during the accounting period on a note payable requires an

adjusting entry consisting of:

A. A debit to Interest Expense and a credit to Cash.

B. A debit to Notes Payable and a credit to Interest Payable.

C. A debit to an asset and a credit to a liability.

D. A debit to Interest Expense and a credit to Interest Payable.

A call provision on a bond:

A. Permits the corporation to redeem the bonds at a specified price.

B. Allows the corporation to revise the stated interest rate.

C. Allows the corporation to revise the maturity date.

D. Always creates the lowest price at which the bond will sell for.

The purchase of treasury stock for cash will have which effect upon the following

items?

A. Option A

B. Option B

C. Option C

D. Option D

An adjusting entry involving recognition of accrued revenue is necessary at the end of

March in which of the following situations?

A. Midwood Consultants received payment in February for consulting services

rendered in March.

B. Midwood Consultants began working for a client on March 15; bills will be sent

monthly beginning April 15.

C. Midwood Consultants made payment in January for office rent for the first three

months of the year.

D. On March 31, a major customer paid his bill for a consulting job completed in

February.

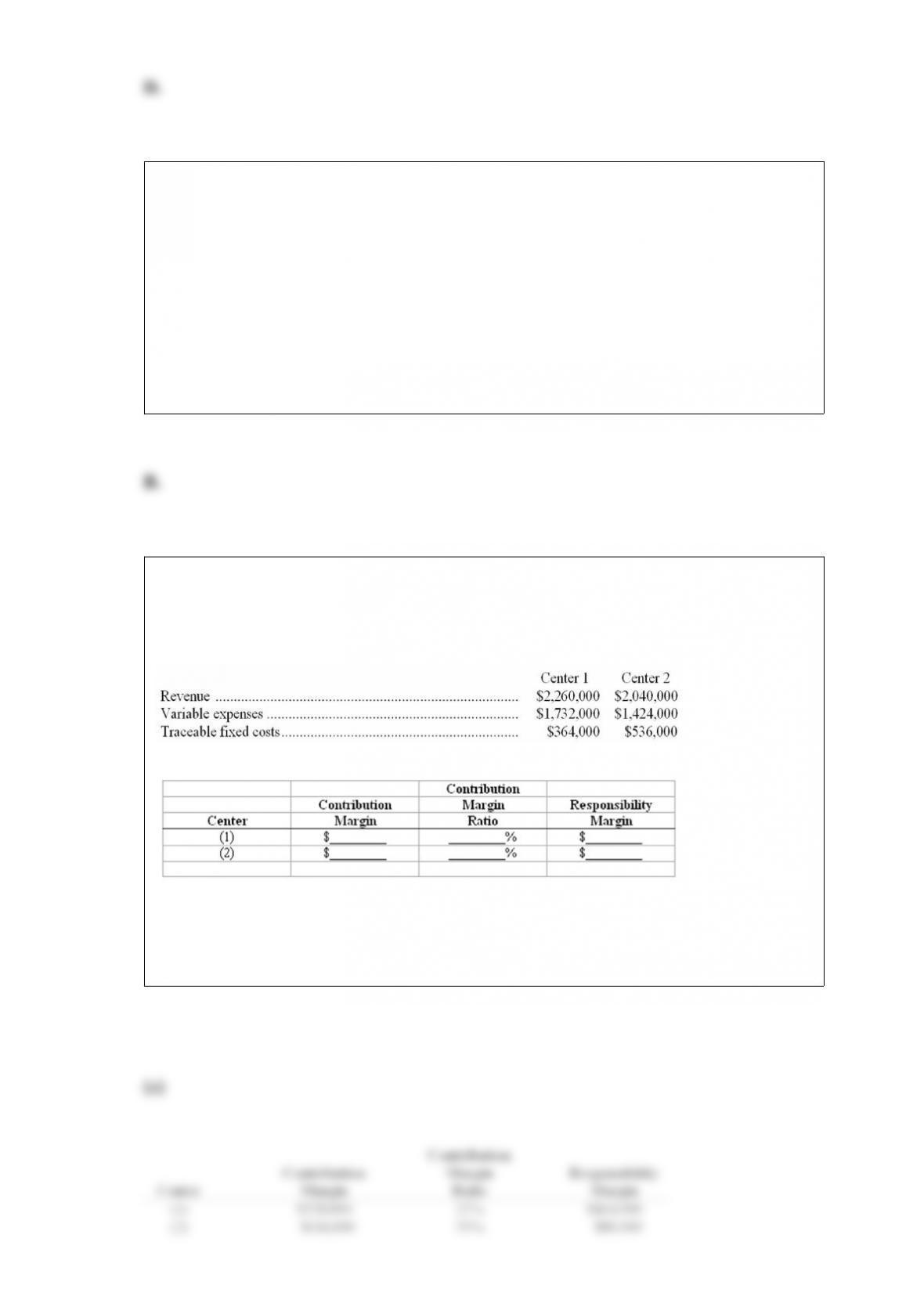

Evaluation of responsibility centers

Shown below are the current-year data for two investment centers of Chelsea Trading,

Inc. The total assets utilized by each of these investment centers during the year amount

to $1,500,000:

(a) Compute the following measures for each investment center:

(b) Assume that a $3,000 monthly expenditure for advertising could increase the

monthly sales of either investment center by $20,000. Which center should the

company advertise to receive the maximum benefit from its advertising expenditure?

Center _________. Explain your reasoning: