Goods on consignment are goods shipped by the owner to another company that holds

the goods and sells them on behalf of the owner.

A company does not need to record the receipt of a bill for utilities used during this year

if the company will not pay the bill until next year.

Revenue is reported on the income statement only if cash was received at the point of

sale.

Unearned Revenue is reported on the balance sheet as a liability.

Consignment inventory is reported on the balance sheet of the company holding the

inventory.

The normal balance of an account is on the same side that increases the account.

Tax accounting and financial accounting use the same depreciation calculations and

there are no differences in the results between the two accounting systems.

The trial balance is a financial statement that reports the assets, liabilities, and equity of

a business at a point in time.

Revenues:

A) decrease assets.

B) increase stockholders’ equity.

C) increase liabilities.

D) decrease expenses.

Cash

Beg. Bal. 123,900

(a) 14,700 6,000 (c)

(b) 38,300 5,800 (d)

7,400 (e)

12,000 (f)

11,200 (g)

Use the information above to answer the following question. In the T-account above:

A) (a) and (b) are credits.

B) (c) through (g) are debits.

C) if the sum of (a) and (b) is less than the sum of (c) through (g), the Cash account

balance will increase.

D) (a) and (b) are increases.

A building has a 10-year useful life and a residual value equal to 10% of the building’s

original cost. If the double-declining balance method is used, what depreciation rate

would be used?

A) 9%

B) 10%

C) 18%

D) 20%

If net income is rising, but net sales revenue and the gross profit percentage remain the

same, then:

A) operating expenses are falling.

B) operating expenses are rising.

C) cost of goods sold is falling.

D) cost of goods sold is rising.

Most companies pay salaries and wages to employees through EFTs, which are known

by

employees as:

A) direct deposits.

B) vouchers.

C) remittance advices.

D) checks.

Which of the following statements about the debit/credit framework is correct?

A) Asset and liability accounts have a normal debit balance.

B) To debit an account means to increase it.

C) Common Stock has a normal credit balance.

D) To credit an account means to decrease it.

All of the following are requirements of the Sarbanes-Oxley Act (SOX) except:

A) tip lines that allow employees to secretly submit concerns about questionable

accounting or auditing practices

B) fines of up to $5 million plus repayment of any fraud proceeds

C) evaluation and reporting on the effectiveness of internal control over financial

reporting for large public companies by external auditors

D) evaluation and reporting on the effectiveness of internal control over financial

reporting for all public companies by management with disclosure that management is

not responsible for the internal control system

Which of the following statements regarding inventory counts is not correct?

A) Companies need to perform a physical count of their inventory at least yearly

regardless of which inventory system is being used.

B) A perpetual inventory system does not require a physical count during the

accounting period to determine cost of goods sold.

C) In a perpetual inventory system, the inventory count is compared to the inventory

account balance to reveal shrinkage.

D) If a company uses a perpetual inventory system and the inventory count at the end of

the accounting period is greater than the balance in the inventory ledger account, there

must have been shrinkage.

A company has bonds outstanding with a face value of $100,000. The unamortized

premium on these bonds is $2,700. If the company retired these bonds at a call price of

99, the journal entry to record this retirement includes a debit to:

A) Bonds Payable for $100,000, a debit to Premium on Bonds Payable for $2,700, a

credit to Cash for $99,000, and a credit to Gain on Bond Retirement for $3,700.

B) Bonds Payable for $100,000, a debit to Loss on Bond Retirement for $1,700, a credit

to Cash for $99,000, and a credit to Premium on Bonds Payable for $2,700.

C) Bonds Payable for $100,000, credit to Cash for $99,000, and a credit to Gain on

Bond Retirement for $1,000.

D) Bonds Payable for $100,000, a debit to Loss on Bond Retirement for $1,673, and a

credit to Cash for $101,673.

Which of the following is a financing activity?

A) The business receives land and gives a check for $1,000.

B) The business receives $1,000 cash and in exchange gives a promissory note.

C) The business promises to hire an employee on the 15th of the month.

D) The business orders supplies and promises to pay for them at the end of the month.

During its first year of operations, Widgets Incorporated reported Sales Revenue of

$386,000 but collected only $303,000 from customers. At the end of the year, Accounts

Receivable equal:

A) $689,000.

B) $386,000.

C) $303,000.

D) $83,000.

Momentum Products Inc. just recorded an adjusting journal entry for the current year’s

estimate of bad debts. Assuming all else is equal, this adjusting journal entry will cause:

A) the accounts receivable turnover ratio to increase.

B) net income to increase.

C) total assets to remain unchanged.

D) net accounts receivable to increase.

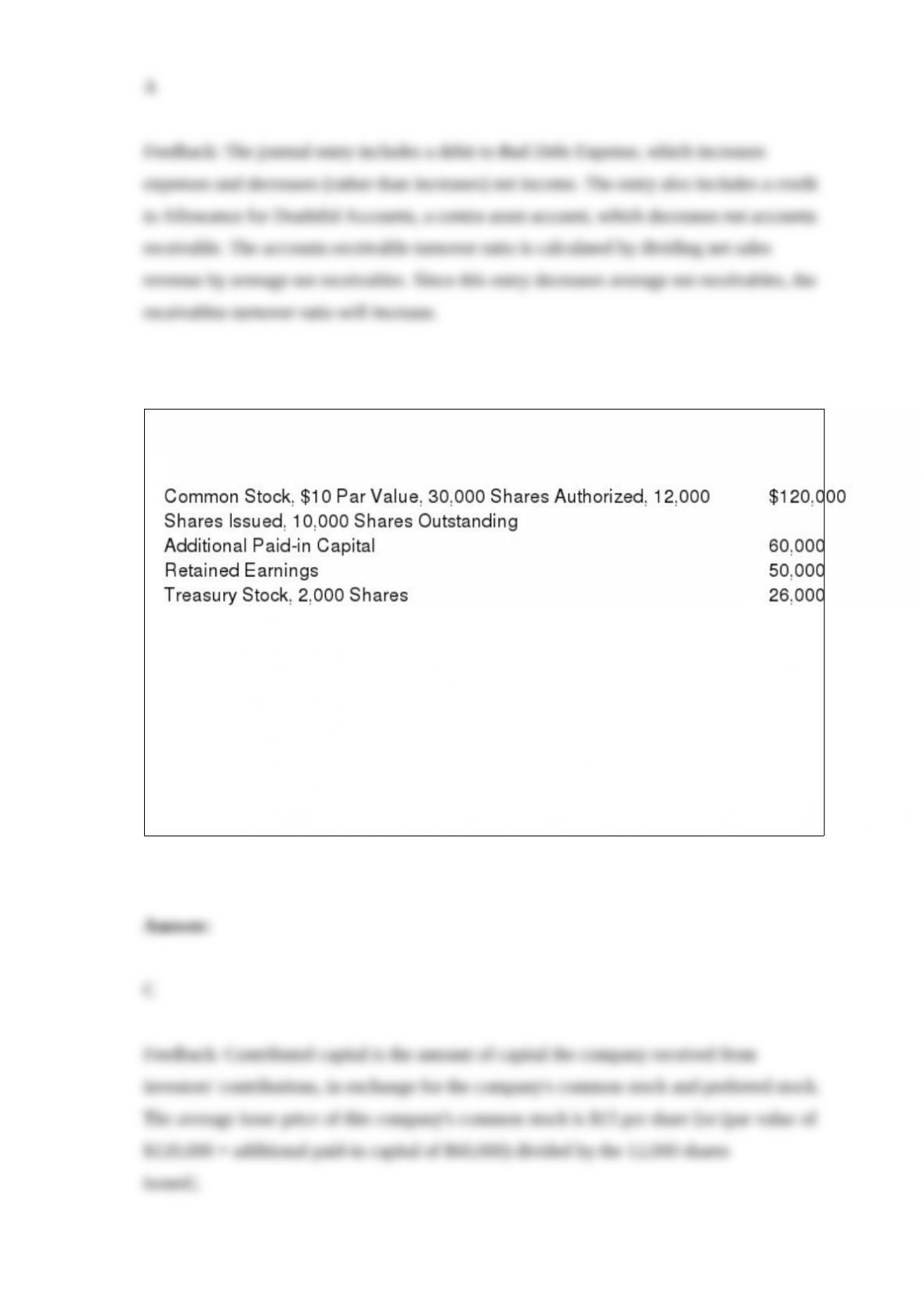

The following data are taken from the stockholders’ equity section of the balance sheet

of a company:

What was the average issue price per share of the common stock?

A) $13.00

B) $10.00

C) $15.00

D) $18.00

When the amount of a contingent liability cannot be reasonably estimated but its

likelihood is probable, the company should:

A) include a description in the notes to the financial statements.

B) record the amount of the liability times the probability of its occurrence.

C) record the amount of the liability as a long-term liability on the balance sheet.

D) exclude the information about the contingent liability from its financial statements

and footnotes.

When a petty cash fund is in use:A) expenses paid with petty cash are recorded when

the fund is replenished.B) Petty Cash is debited when funds are replenished.C) Petty

Cash is credited when funds are replenished.D) expenses are not recorded.

On January 1, a company lends a corporate customer $80,000 at 6% interest. The

amount of interest revenue that should be recorded for the quarter ending March 31

equals:

A) $4,800

B) $1,200

C) $400

D) $1,600

Under the cost principle, a company capitalizes:

A) all ordinary repair expenditures incurred in the use of an asset.

B) any interest incurred in borrowing money to help pay for asset acquisitions.

C) all reasonable and necessary costs of acquiring an asset and preparing it for use.

D) the total market value of individual assets acquired in a €basket purchase.’

Samberg Inc. had the following transactions.

Oct. 1 – Sold $10,000 of merchandise on account, 1/10, n/30 to McCormick Industries.

Nov. 1 – Received a $10,000, 90-day, 10% note from McCormick Industries to settle its

$10,000 unpaid balance.

Dec. 31 – Accrued interest on the note. (Round to the nearest whole dollar amount.)

Jan. 31 – Received the interest on the note’s maturity date.

Jan. 31 – Received the principal on the note’s maturity date. (Round to the nearest whole

dollar amount.)

Required:

Prepare the required journal entries.

On September 1, a company established a petty cash fund of $100. On September 10,

the petty cash fund was replenished when there was $16 remaining and there were petty

cash receipts for supplies, $27, and postage, $54. On September 15, the petty cash fund

was increased to $125.

Required:

Prepare the journal entries, if any, required on September 1, September 10, and

September 15.

A journal entry to record the purchase of supplies for $400 cash was properly prepared.

The debit in the entry was properly posted to the related account. However, the credit in

the entry was mistakenly recorded as a credit to the Supplies account.

Required:

Determine the impact of this error on the accounting equation.

On April 1, a company established a petty cash fund of $1,000.

Required:

Prepare the journal entry, if any, required on April 1

Company X has net sales revenue of $1,250,000, cost of goods sold of $760,000, and

all other expenses of $290,000. The beginning balance of stockholders’ equity is

$400,000 and the beginning balance of fixed assets is $361,000. The ending balance of

stockholders’ equity is $600,000 and the ending balance of fixed assets is $389,000.

Required:

Compute the return on equity (ROE) ratio.

Maple Industries Inc. deposits all cash receipts on the day when they are received and it

makes all cash payments by check. At the close of business on December 31, its Cash

account shows a debit balance of $18,303. The company ‘s bank statement as of June 30

shows an ending cash balance of $15,921. The following information was also

available.

Outstanding checks as of December 31 total $2,261.

Included with the bank statement was a debit memo in the amount of $35 for service

charges.

Check No. 2519, listed with the canceled checks, was correctly drawn for $805 in

payment of a utility bill on December 16. The company mistakenly recorded it with a

debit to Utilities Expense and a credit to Cash in the amount of $850.

The December 31 cash receipts of $3,425 were placed in the bank ‘s night depository

after banking hours and were not recorded on the December 31 bank statement.

The bank deducted $1,228 for an NSF check from a customer deposited on December

10.

Required:

Prepare the bank reconciliation as of December 31.

Choose the appropriate letter match each financial performance ratios with the

appropriate category.

Ratio

1> ___ Debt-to-assets ratio

2> ___ Receivables turnover ratio

3> ___ Fixed asset turnover ratio

4> ___ Current ratio

5> ___ Return on equity

6> ___ Price earnings ratio

7> ___ Times interest earned ratio

8> ___ Quick ratio

9> ___ Inventory turnover ratio

10> ___ Earnings per share

Category

P – Profitability

L – Liquidity

S – Solvency

For each of the independent cases below, identify and describe the principle of internal

control that is violated and recommend what should be done to remedy the violation.

Tesoro Corp. uses a perpetual inventory system. The following activities occurred

during May:

May 2 – Tesoro purchased $45,000 worth of inventory, on credit terms 3/10 n/30.

May 2 – Because the terms of the purchase were FOB shipping point, Tesoro pays

$1,200 to the trucker.

May 5 – Tesoro returned $5,000 worth of that inventory to the supplier.

May 10 – Tesoro paid for the inventory, taking advantage of all available discounts.

Required:

Prepare the journal entries to record these transactions on the books of Tesoro Corp.