1) How does GAAP view interim accounting periods?

A) As discrete units for which net income may be separately determined

B) As integral units of the entire year for which each interim period is an essential part

of an annual period

C) As integral units of the entire year with each interim period as an independent

accounting period

D) As discrete units of the entire year using the same principles that are applied to the

annual period

2) Plenty Corporation issued six thousand, $1,000 par, 6% bonds on January 1, 2010, at

par. Interest is paid on January 1 and July 1 of each year; the bonds mature on January

1, 2015 . On January 2, 2012, Scrawn Corporation, a 75%-owned subsidiary of Plenty,

purchased 3,000 of the bonds on the open market at 102.50 . Plenty’s separate net

income for 2012 included the annual interest expense for all 3,000 bonds. Scrawn’s

separate net income for 2012 was $400,000, which included the bond interest received

on July 1 as well as the accrual of bond interest revenue earned on December 31 . Both

companies use straight-line amortization of bond discounts/premiums.

Using the original information, the amount of consolidated Interest Expense for 2012

was

A) $ 135,000

B) $ 180,000

C) $ 270,000

D) $ 360,000

3) The following are transactions for the city of Franklin.

a.Borrowed $20,000 by issuing a two-year note.

b.Purchased equipment for $6,000 cash.

c.Licenses for $700 were billed on account.

d.Accrued employee salary costs of $7,000.

e.Depreciation expense on equipment for year, $1,000.

Required:

Analyze the above transactions by using the accounting equation for a governmental

fund.

4) On January 1, 2011, Penelope Company acquired a 90% interest in Leah Company

for $180,000 cash. On January 1, 2011, Leah Company had the following assets and

liabilities:

Book ValueFair Value

Cash$10,000$10,000

Accounts Receivable30,00035,000

Inventory40,00050,000

Plant Assets60,00080,000

Total Assets$140,000$175,000

Liabilities$25,000$25,000

Capital Stock100,000

Retained Earnings15,000

Total Liabilities &

Stockholders’ Equity$140,000

Push-down accounting is used for the acquisition.

Assume the parent company theory is used. On January 2, 2011, Leah Company will

report Goodwill of ________ and Accounts Receivable of ________ on Leah’s balance

sheet.

A) $27,000; $30,000

B) $27,000; $35,000

C) $30,000; $30,000

D) $45,000; $34,500

5) If a financial instrument is classified as a cash flow hedge, then

A) its gains or losses are reported in the income statement if a fiscal year-end occurs

before the settlement date

B) it is classified as a held-to-maturity asset

C) it does not require a notional amount

D) its gains or losses are reported in the balance sheet if a fiscal year-end occurs before

the settlement date

6) Will Wealth made three charitable donations in 2011 . Each was for $500,000,

however they were made to three different organizations as follows:

1>Will donated to a local voluntary health and welfare organization (VHWO), and

indicated that the funds could be used as the VHO wanted.

2>Will donated to a local private, not-for-profit university, designating the funds to be

used for scholarships and student aid.

3>Will donated to the local not-for-profit, nongovernmental hospital, designating the

funds to be used for purchase of diagnostic equipment.

Required:

For each of the above three situations:

A.Prepare the journal entry that each organization would prepare at the time of the

contribution.

B.Prepare the journal entry that each organization would prepare at the time of the

subsequent spending of the funds. Assume that the spending is in accordance with any

restrictions that Will placed on the donation.

7) No constructive gain or loss arises from the purchase of an affiliate’s bonds if the

A) affiliate is a 100%-owned subsidiary

B) bonds are purchased at book value

C) bonds are purchased with arm’s-length bargaining from outside entities

D) gain or loss cannot be reasonably estimated

8) Which one of the following operating segment disclosures is not required by GAAP?

A) Total Assets

B) Equity

C) Intersegment sales

D) Extraordinary items

9) Voluntary health and welfare organizations classify fund-raising costs as

A) costs of services sold

B) program services

C) auxiliary expenses

D) supporting services

10) Consider a sale of stock by a subsidiary to parties outside the consolidated entity.

This transaction requires an adjustment of the parent’s investment and additional paid-in

capital accounts except when

A) the shares are sold below book value per share

B) the shares are sold above book value per share

C) the shares are sold at book value per share

D) All of the above are correct

11) Pond Corporation uses the fair value method of accounting for its investment in

Swan Company. Which one of the following events would affect the Investment in

Swan Co. account?

A) Investee losses

B) Investee dividend payments

C) An increase in the investee’s share price from last period

D) All of the above would affect the Investment in Swan Co. account

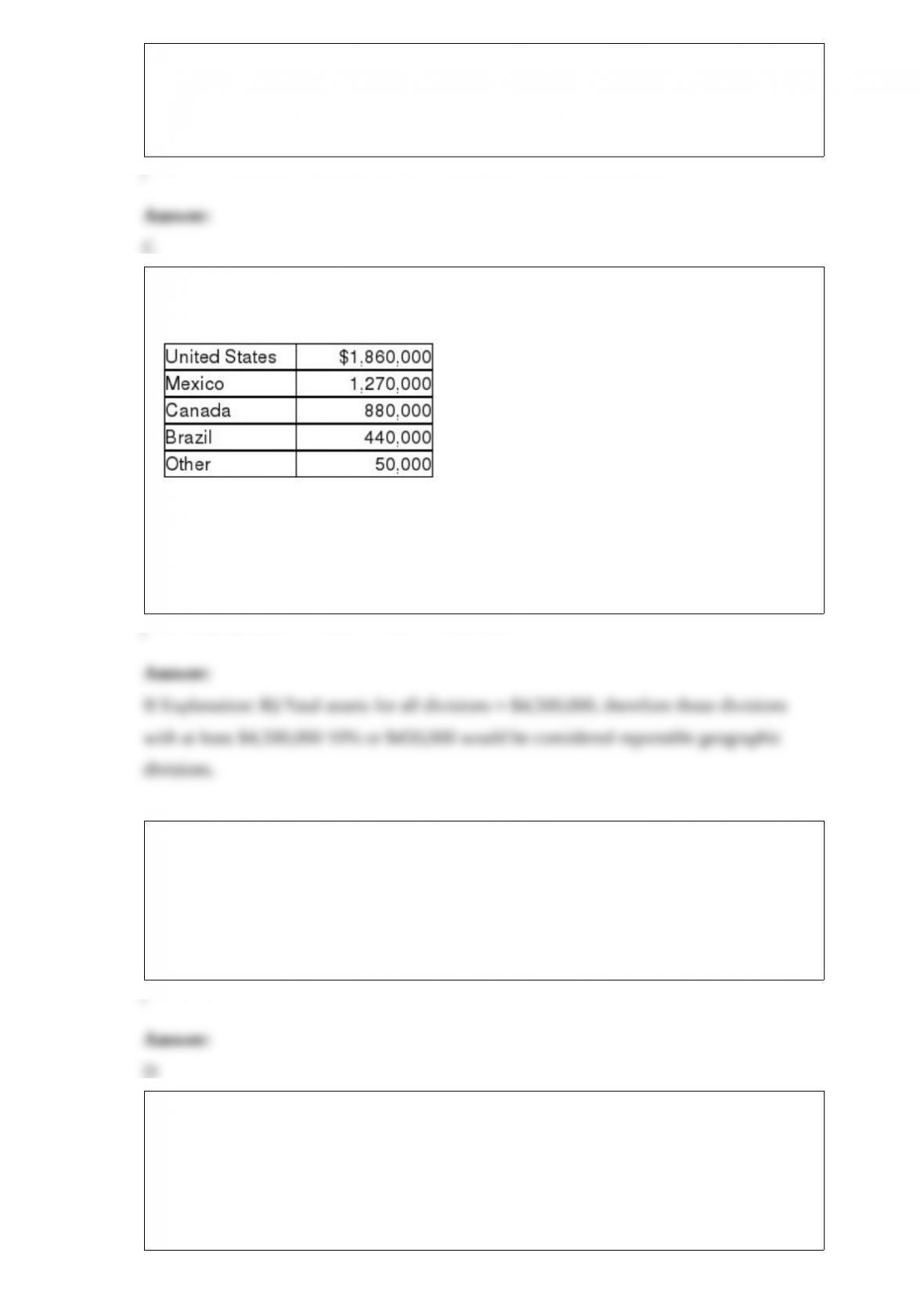

12) The following table is provided in the disclosures for interim reporting by Bigg

Company, regarding the location of their assets.

Based on the table, which of the following statements is true?

A) Only the U.S. and Mexico divisions would be reportable geographic divisions

B) The U.S., Mexico and Canada divisions would be reportable geographic divisions

C) All geographic divisions would be reportable, except for “other”

D) All geographic divisions would be reportable

13) On the Statement of Net Assets, in place of stockholders’ equity, proprietary funds

report

A) Retained Earnings only

B) Restricted Cash only

C) Unrestricted Cash only

D) Net Assets

14) Bigga Corporation purchased the net assets of Petit, Inc. on January 2, 2011 for

$380,000 cash and also paid $15,000 in direct acquisition costs. Petit, Inc. was

dissolved on the date of the acquisition. Petit’s balance sheet on January 2, 2011 was as

follows:

Accounts receivable-net$90,000Current liabilities$75,000

Inventory 220,000 Long term debt 80,000

Land30,000Common stock ($1 par)10,000

Building-net20,000Addtl. paid-in capital215,000

Equipment-net 40,000Retained earnings 20,000

Total assets$400,000Total liab. & equity$400,000

Fair values agree with book values except for inventory, land, and equipment, which

have fair values of $260,000, $35,000 and $35,000, respectively. Petit has patent rights

with a fair value of $20,000.

Required:

Prepare Bigga’s general journal entry for the cash purchase of Petit’s net assets.

15) Separate income statements of Pingair Corporation and its 90%-owned subsidiary,

Staunch Inc., for 2011 were as follows:

Pingair Staunch

Sales Revenue$2,200,000 $1,000,000

Cost of sales(1,400,000)(600,000)

Other expenses(400,000)(200,000)

Gain on equipment80,000

Income from Staunch128,000

Net income$608,000 $200,000

Additional information:

1>Pingair acquired its 90% interest in Staunch Inc. when the book values were equal to

the fair values.

2>The gain on equipment relates to equipment with a book value of $120,000 and a

4-year remaining useful life that Pingair sold to Staunch for $200,000 on January 2,

2011 . The straight-line depreciation method is used. The equipment has no salvage

value.

3>Pingair sold inventory to Staunch in 2010 and 2011 as shown in the table below. (The

2010 ending inventory is sold in 2011)

20102011

Intercompany sales$300,000200,000

Original cost from third-party180,000120,000

Percentage unsold at year-end4050

4>Staunch did not declare or pay dividends in 2010 and 2011 .

Required:

1> Prepare adjusting/eliminating entries for the consolidation worksheet at December

31, 2011 .

2> Prepare a consolidated income statement for Pingair Corporation and Subsidiary for

the year ended December 31, 2011 .

16) Popcorn Corporation owns 90% of the outstanding voting common stock of Salty

Corporation. On January 1, 2005, Salty issued $1,000,000 face amount of 12%, $1,000

bonds payable at 119.20 . The bonds pay interest on January 1 and July 1 of each year

and mature on January 1, 2013 . On July 2, 2010, Popcorn purchased all of the

outstanding bonds at a price of 107.50. Both companies use straight-line amortization.

Required:

1>Prepare the journal entries for July 1, 2010 through December 31, 2010 for Popcorn

Corporation.

2>Prepare the journal entries for July 1, 2010 through December 31, 2010 for Salty

Corporation.

3>Prepare the elimination entries necessary on the consolidating working papers for the

year ended December 31, 2010 .

17) Jefferson Company entered into a forward contract with Washington Company on

October 1, 2011, under which Jefferson agreed to buy (and Washington agreed to sell)

10,000 tons of coal at $80.00 per ton in 90 days. On October 1, 2011, the price of coal

is $82.00 per ton. On December 29, 2011, the price of coal is $85.00 per ton. The

contract allows for net settlement.

Required:

Determine the net settlement on the forward contract.

18) Ending Company is in bankruptcy and is being liquidated under the provisions of

Chapter 7 of the bankruptcy code. The trustee has converted all assets into $80,000 cash

(which includes the amounts shown below for assets sold) and has prepared the

following list of approved claims:

Property taxes payable$10,000

Accounts payable, unsecured30,000

Mortgage payable, secured by property that was sold for $50,00030,000

Note payable to bank, secured by all accounts receivable of which $20,000

was able to be collected and the balance was written off30,000

Required:

How much will the bank receive on the note payable?

19) Paine Corporation owns 90% of Achan Corporation, Achan Corporation owns 85%

of Badge Corporation, and Badge Corporation owns 5% of Achan Corporation. The

separate net incomes (excluding investment income) of Paine, Achan, and Badge are

$400,000, $160,000, and $220,000, respectively. Assume the investments were acquired

at a cost equal to the book value of each investment, which also equals the fair value.

Required:

1> Calculate revised net incomes for Paine, Achan, and Badge by using the

conventional method.

2> Determine the controlling interest share of consolidated net income and the

noncontrolling interest shares.

20) Hilfmir Corporation filed for Chapter 11 bankruptcy on January 1, 2011 . A

summary of their financial status is shown below on June 30, 2011, at the date of the

approved reorganization, along with the fair value of their assets.

Per BooksFair Value

Cash$134,000$134,000

A/R – net20,00020,000

Inventory32,00040,000

Plant Assets – net114,000106,000

Patent80,0000

$380,000

A/P$60,000

Wages Payable20,000

Prepetition liab.250,000

Common Stock140,000

Deficit(90,000)

$380,000

Under the reorganization plan, the reorganization value has been set at $320,000.

Prepetition liabilities include $30,000 of trade Accounts Payable and a $220,000 Note

Payable to Bigg Bank. The reorganization plan calls for the Prepetition accounts

payable to be paid at 80% at a later date, and the Note Payable for $220,000 to be

replaced by a Note Payable for $76,000 and the issuance of common stock of the new

entity for $100,000. The former stockholders will receive $40,000 in common stock of

the new entity, Hilfmir, in exchange for their shares.

Required:

Show the calculations to determine if Hilfmir is eligible for fresh-start accounting, and

prepare a fresh-start balance sheet for the new entity, Hilfmir, as of July 1, 2011

21) Johnsen Corporation paid $225,000 for a 70% interest in Jonas Corporation on

January 1, 2011 . On that date, Jonas’s balance sheet accounts, at book value and fair

value, were as follows:

Book ValueFair Value

Assets

Cash$25,000$25,000

Accounts receivable-net45,00055,000

Inventories40,00060,000

Plant, property and equipment-net140,000125,000

Total assets$250,000$265,000

Equities

Accounts payable$40,000$40,000

Common stock120,000

Retained earnings90,000

Total liab. & equity$250,000

Required:

1> Prepare the journal entry necessary on January 1, 2011 on Jonas Corporation’s

books. Both companies use push-down accounting and the entity theory.

2> Prepare the balance sheet for Jonas Corporation immediately after the acquisition on

January 1, 2011 .

22) The following information was collected together for the Lawson Company relating

to the preparation of their annual financial statements for 2011 . For each item, indicate

“yes” or “no” as to whether the item must be disclosed in the annual report.

_____ 1> Names of major customers for all reportable segments

_____ 2> Interest revenue and expense for all reportable segments

_____ 3> Cost of Goods Sold for all reportable segments

_____ 4> Depreciation expense and amortization expense for all reportable segments

_____ 5> Revenue from external customers for all reportable segments

_____ 6> The basis for aggregating any operating segments to arrive at reporting

segments

_____ 7> Income tax expense (or benefit) for all reportable segments

_____ 8> Total assets for all reportable segments

_____ 9> Type of product or service for all reportable segments

_____ 10> Extraordinary items for all reportable segments