1) the chart of accounts is a special ledger used in accounting systems.

2) when preparing financial statements, the accountant assumes that the business will

stay in business for the foreseeable future.

3) the monetary unit assumption states that transactions that can be measured in terms

of money should be recorded in the accounting records.

4) research and development costs that result in a successful product that is patentable

are charged to the patent account.

5) metropolitan symphony sells 200 season tickets for $40,000 that includes a

five-concert season. the amount of unearned ticket revenue after the third concert is

$24,000.

6) a loss on disposal of a plant asset as a result of a sale or a retirement is calculated in

the same way as a gain on disposal.

7) an effective system of internal control centralizes functions in a single capable

individual.

8) a company whose current liabilities exceed its current assets may have a liquidity

problem.

9) rains company purchased equipment on january 1 at a list price of $50,000, with

credit terms 2/10, n/30. payment was made within the discount period. rains paid

$2,500 sales tax on the equipment, and paid installation charges of $880. prior to

installation, rains paid $2,000 to pour a concrete slab on which to place the equipment.

what is the total cost of the new equipment?

a.$52,380

b.$54,380

c.$55,380

d.$50,500

10) net income results when

a.assets > liabilities

b.revenues = expenses

c.revenues > expenses

d.revenues < expenses

11) the term applied to the periodic expiration of a plant assets cost is

a.amortization

b.depletion

c.depreciation

d.cost expiration

12) match the items below by entering the appropriate code letter in the space provided.

1>a written promise to pay a specified amount on demand or at a definite time.

2>sales that involve the customer, the retailer, and the credit card issuer.

3>a measure of the liquidity of receivables.

4>notes and accounts receivable that result from sales transactions.

5>a note which is not paid in full at maturity.

6>analysis of customer account balances by length of time they have been unpaid.

7>emphasizes expected cash realizable value of accounts receivable.

8>bad debt losses are not estimated and no allowance account is used.

9>the net amount expected to be received in cash.

13) the sales returns and allowances account does not provide information to

management about

a.possible inferior merchandise

b.the percentage of credit sales versus cash sales

c.inefficiencies in filling orders

d.errors in filling customers

14) which of the following is not an example of a source document that provides

evidence of a transaction?

a.a cancelled check

b.a sales slip

c.a trial balance

d.a cash register tape

15) the matching rule relates to credit losses by stating that bad debt expense should be

recorded

a.in the same period as allowed for tax purposes

b.in the period of the sale

c.for an exact amount

d.in the period of the loss

16) the best way to study the relationship of the components within a financial

statement is to prepare

a.common size statements

b.a trend analysis

c.profitability analysis

d.ratio analysis

17) expensing the purchase of a waste paper basket with an estimated useful life of 10

years is an application of

a.materiality

b.consistency

c.going concern

d.economic entity

18) the expense recognition principle states that expenses should be matched with

revenues. another way of stating the principle is to say that:

a.assets should be matched with liabilities

b.efforts should be matched with accomplishments

c.dividends should be matched with stockholder investments

d.cash payments should be matched with cash receipts

19) which situation below might indicate a company has a low quality of earnings?

a.revenue is recognized when earned

b.repair costs are capitalized and then depreciated

c.the financial statements are prepared in accordance with generally accepted

accounting principles

d.the same accounting principles are used each year

20) if accounting information has relevance, it is useful in making predictions about

a.future irs audits

b.new accounting principles

c.foreign currency exchange rates

d.the future events of a company

21) an expense account is closed with a credit to the expense account and a debit to the

income summary account.

22) young company lends dobson industries $30,000 on august 1, 2012, accepting a

9-month, 12% interest note. if young accrued interest at its december 31, 2012

year-end, what entry must it make to record the collection of the note and interest at its

maturity date?

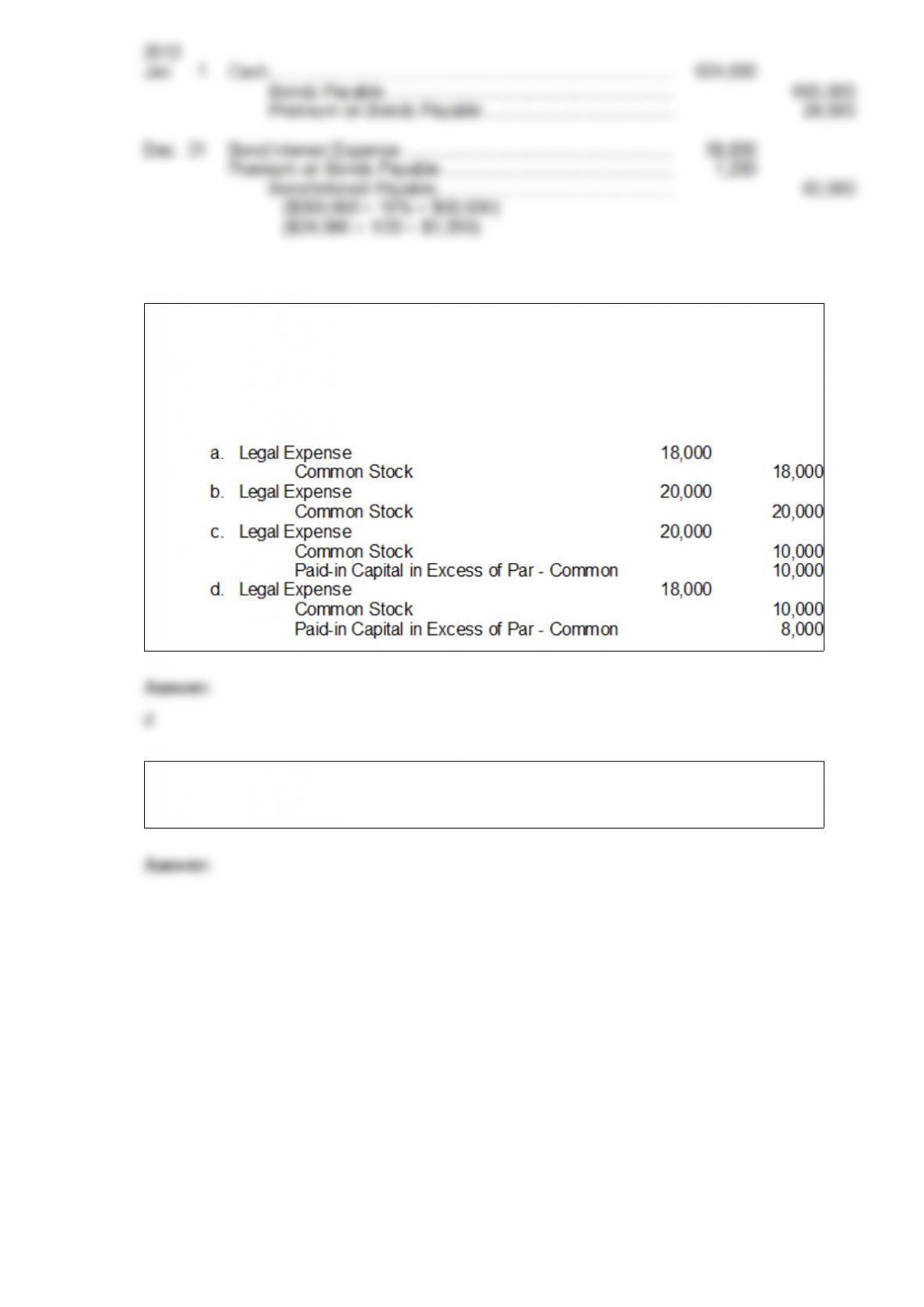

23) on january 1, 2011, powell corporation issued $800,000, 5%, 5-year bonds dated

january 1, 2011, at 95. the bonds pay annual interest on january the company uses the

straight-line method of amortization and has a calendar year end.

instructions

prepare all the journal entries that powell corporation would make related to this bond

issue through january 1, 2012. be sure to indicate the date on which the entries would

be made.

24) s. lawyer performed legal services for e. corp. due to a cash shortage, an agreement

was reached whereby e. corp. would pay s. lawyer a legal fee of approximately $20,000

by issuing 10,000 shares of its common stock (par $1). the stock trades on a daily basis

and the market price of the stock on the day the debt was settled is $1.80 per share.

given this information, the best journal entry for e. corp. to record for this transaction is

25) using the following information, prepare a bank reconciliation for hintz company

for july 31, 2012

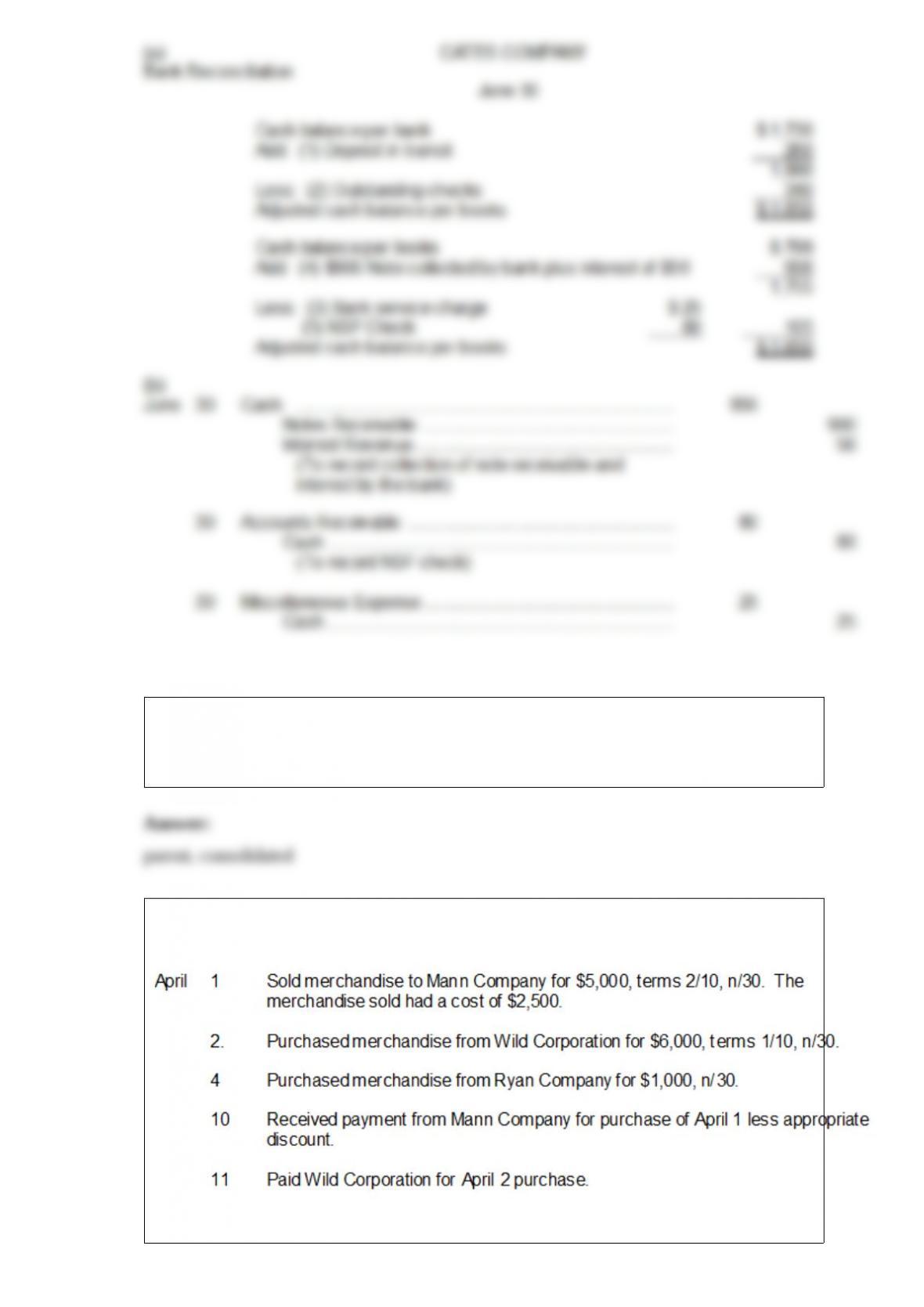

26) the bank statement for cates company indicates a balance of $1,730 on june 30. the

cash balance per books had a balance of $799 on this date. the following information

pertains to the bank transactions for the company.

instructions

27) a company that owns more than 50% of the common stock of another company is

known as the ______________ company and _____________ financial statements are

usually prepared.

28) presented here are selected transactions for the leiss company during april. leiss

uses the perpetual inventory system.

instructions

journalize the april transactions for leiss company.

29) fredrickson inc. obtained significant influence over unruh corporation by buying

40% of unruh 30,000 outstanding shares common stock at a total cost of $11 per share

on january 1, 2012. on june 15 unruh declared and paid a cash dividend of $35,000. on

december 31 unruh reported a net income of $120,000 for the year.

instructions

prepare all the necessary journal entries for 2012 for fredrickson inc.

30) payments or receipts of equal dollar amounts are referred to as

__________________.