1) Under IFRS the preferred term for accounts payable is provisions.

2) The general journal is used to record all transactions that do not fit one of the special

journals.

3) The operating cycle is the time span during which cash is used to acquire goods and

services and the goods and services are sold to customers.

4) The cost of removing an old building from acquired land would be a part of the land

account.

5) The components of the payroll system are a payroll register, payroll cheques, and an

earnings record for each employee.

6) Payroll deductions withheld from employees become a liability of the employer.

7) Accounting system flexibility creates additional cost to the organization.

8) Accrued interest on a note payable should be credited to interest payable.

9) Corporations and individuals both pay income tax.

10) The income statement must be prepared before the statement of owner’s equity

since net income or net loss is added to or subtracted from the beginning balance in the

owner’s capital account.

11) Capital on the adjusted trial balance represents capital at the end of the accounting

period.

12) Which of the following is an important internal control over payroll?

A) Separating the duties of the disbursement of paychecks from the recording of payroll

transactions in the ledger

B) Separating the duties of safeguarding property from record-keeping of property

C) Separating the duties of approving invoices from signing disbursement checks

D) Separating the duties of cash disbursement from bank reconciliations

13) Stan’s Shoe Repairs recorded $2,000 of unearned service revenue being earned and

the collection of $4,000 cash for service revenue previously accrued. The impact of

these two entries on total service revenue is:

A) a decrease of $2,000

B) an increase of $4,000

C) an increase of $6,000

D) an increase of $2,000

14) Net income is entered onto which column(s) of a worksheet?

A) adjusted trial balance debit column

B) income statement debit and balance sheet credit

C) income statement debit and balance sheet debit

D) adjusted trial balance credit and income statement credit

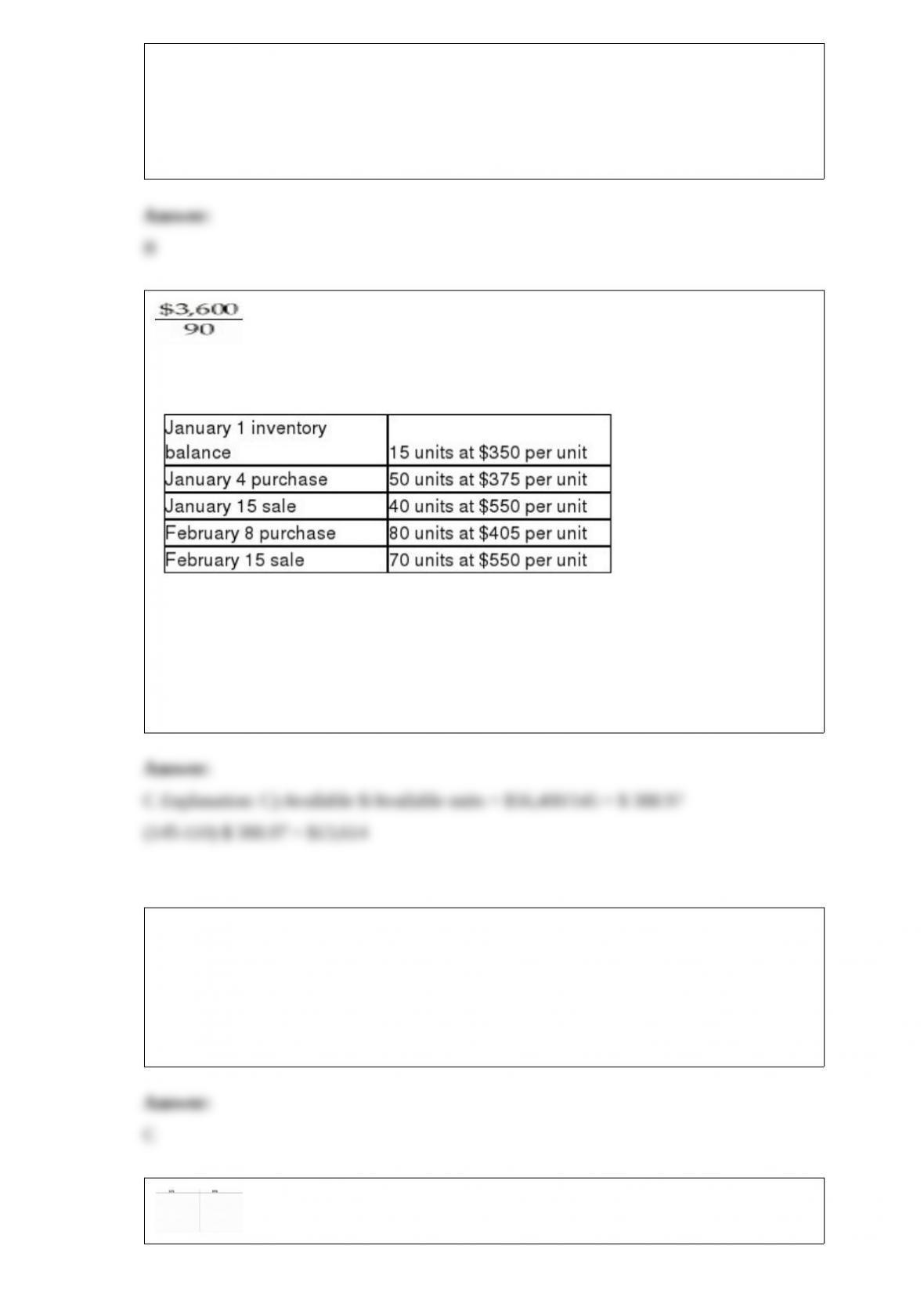

15) Table 6-6 Sam’s Wholesale Bikes

Refer to Table 6-6. What is the value of the February ending inventory assuming that

Sam’s uses the periodic weighted-average inventory method?

A) $12,845

B) $17,408

C) $13,614

D) $10,603

16) A liability that arises from an expense that the business has incurred but has not yet

paid is called a(n):

A) deferred asset

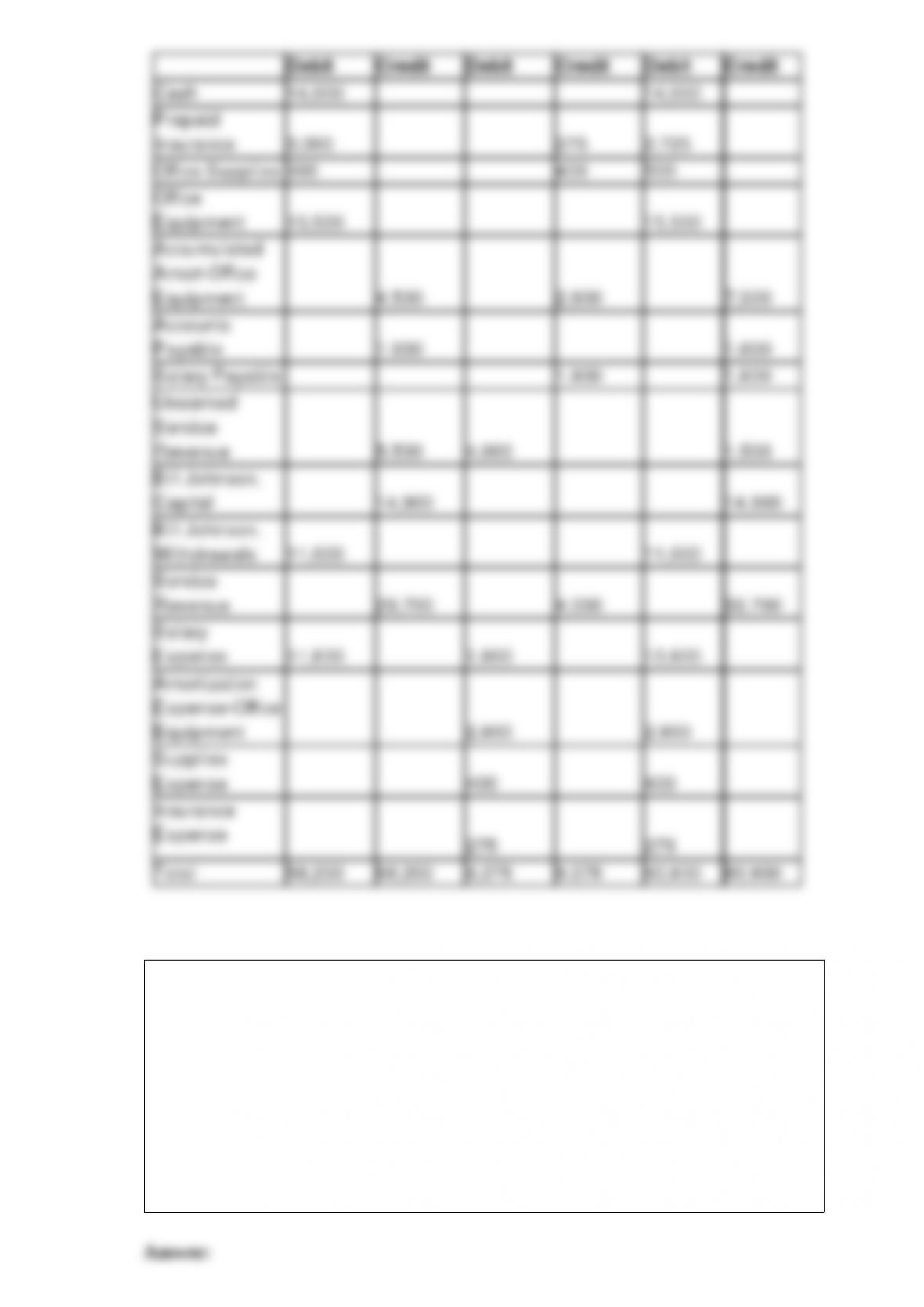

B) accrued asset

C) accrued expense

D) deferred expense

17) Table 9-11 Mark’s Sales

At the beginning of 2014, Mark’s sales had the following ledger balances:

During the year there were $450,000 of credit sales, $460,000 of collections, and

$3,700 of write-offs.

Refer to Table 9-11. At the end of the year, Mark’s adjusted for uncollectible account

expense using the percent-of-sales method, and applied a rate, based on past history, of

1.2%. At the end of the year, what was the balance in the allowance account?

A) $2,300

B) $1,700

C) $6,400

D) $2,700

18) The accountant at Wilton and Jones gathered the following selected accounting

information:

20142013

Cash$ 40,000$ 35,000

Short-term investments30,00017,000

Accounts receivable (net)35,00025,000

Inventory65,00065,000

Prepaid expenses7,0009,000

Accounts payable60,00054,000

Salary payable14,00015,000

Income taxes payable11,00013,000

Bonds payable (due 2019)80,00080,000

Net credit sales270,000235,000

Cost of goods sold165,000141,000

a) Compute the acid-test ratio for 2014 and 2013 .

b) Compute the days’ sales in receivables for 2013 and 2014 . The accounts receivable

(net) at December 31, 2012, were $39,000.

c) Are the ratios improving or deteriorating?

19) Carolina Supply accepted an eight-month, $16,000 note receivable, with 8%

interest, from Reading Corporation on August 1, 2013 . Carolina Supply’s year end is

December 31 . The amount of interest to be accrued on December 31, 2013 is:

A) $533

B) $1,280

C) $853

D) $320

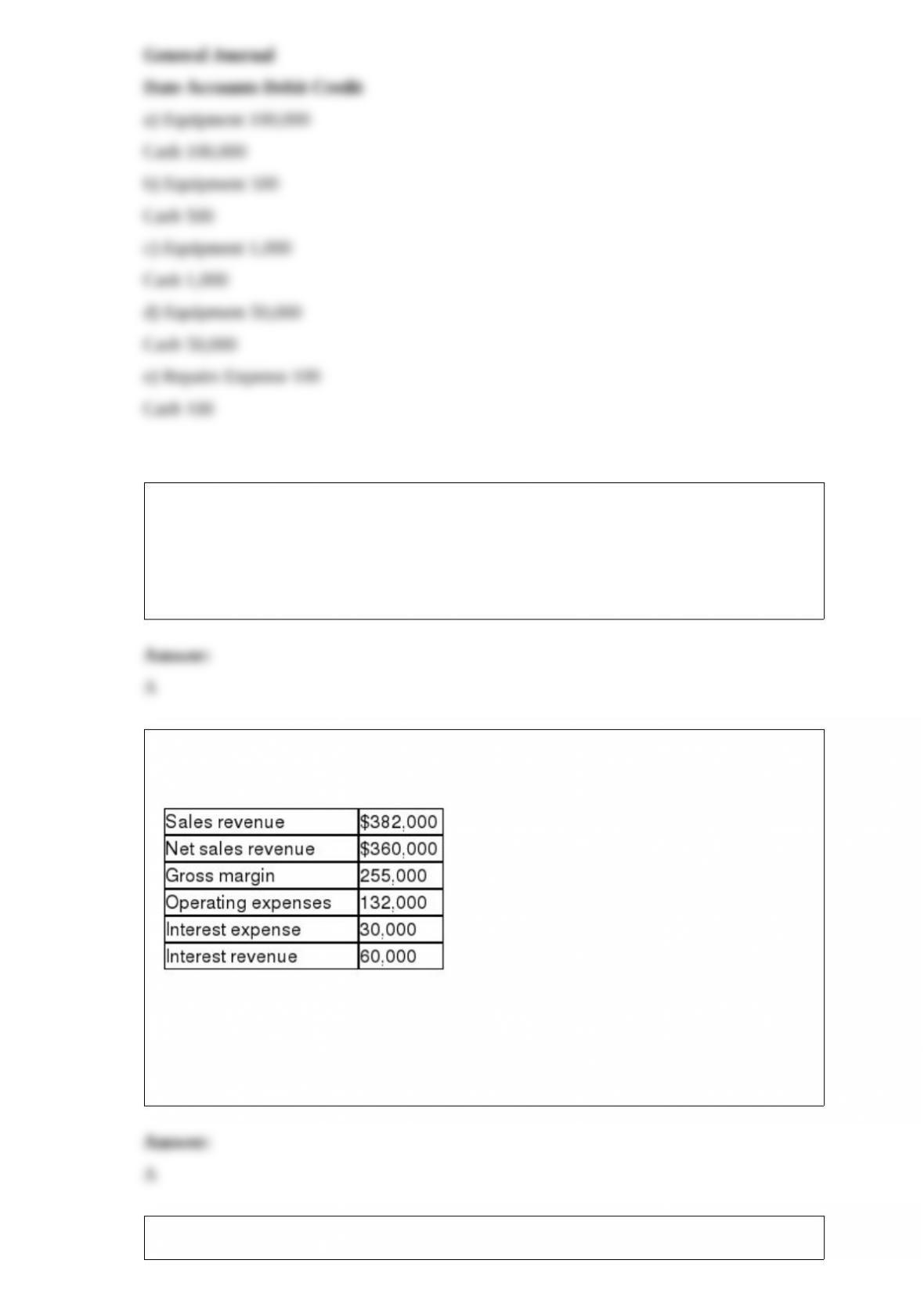

20) Record journal entries for the following transactions involving property, plant and

equipment for Blankenship Company Ltd.:

a) Purchased equipment costing $100,000.

b) Paid freight to have equipment delivered, $500.

c) Paid $1,000 to have equipment installed.

d) Paid $50,000 to have a similar piece of equipment overhauled.

e) Paid $100 for periodic maintenance to the new equipment.

21) All of the following describe a liability except:

A) investments by owners

B) economic obligations to creditors

C) debts to creditors

D) outsider claims

22) Table 5-2

Referring to Table 5-2, what is the operating income or operating loss?

A) operating income of $123,000

B) operating loss of $177,000

C) operating loss of $27,000

D) operating income of $27,000

23) Alpha Company had $45,000 in beginning inventory and $80,000 in ending

inventory. Cost of goods sold for the period was $25,000. The inventory turnover is:

A) 0.56

B) 0.3125

C) 0.4

D) 4.0

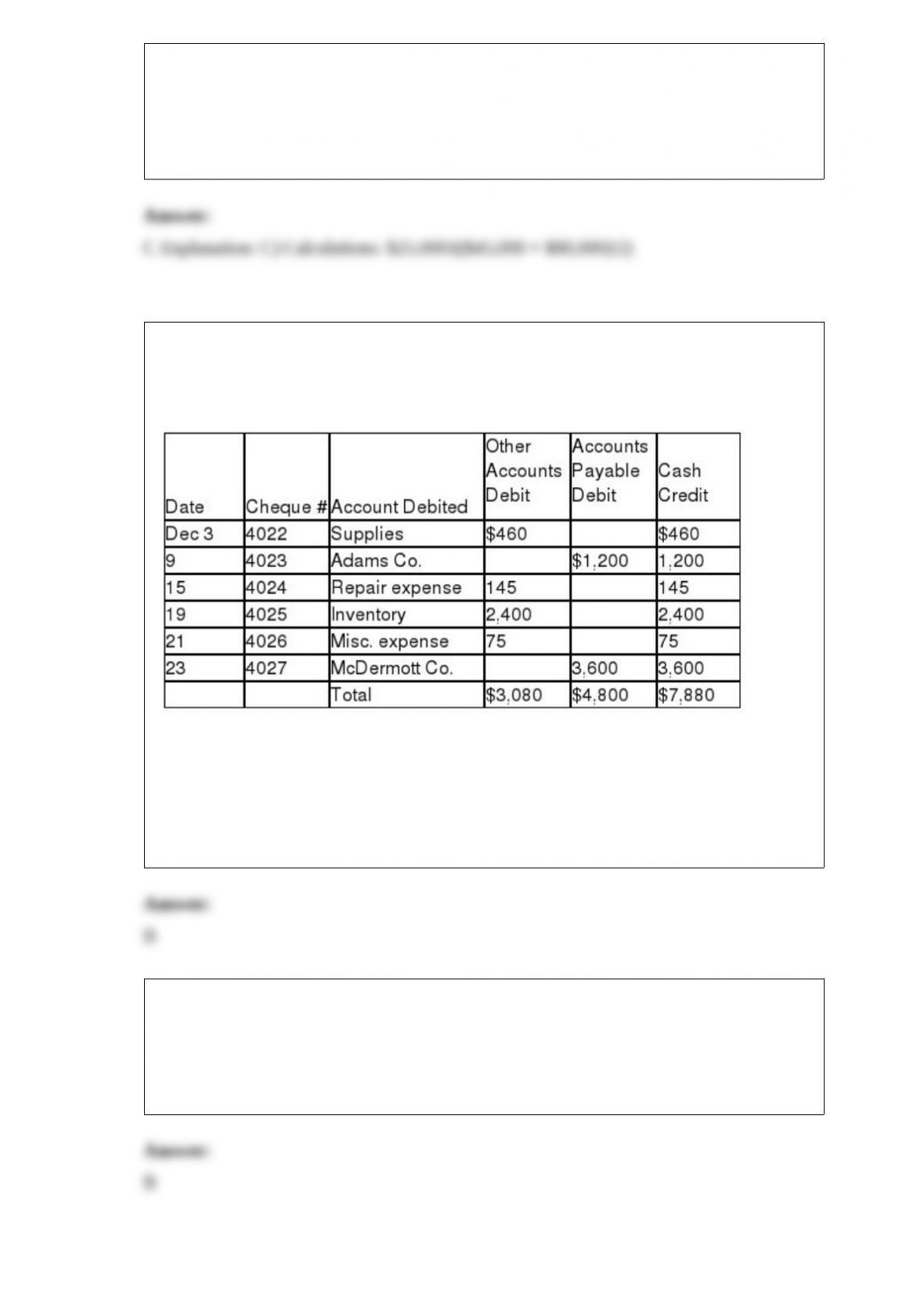

24) Laoshan Company uses a cash payments journal for all its payments by cheque. At

the end of December, the journal shows the following information:

When this journal is posted, what entry will be made to the accounts payable control

account?

A) Credit $4,800

B) Debit $4,800

C) Credit $7,880

D) Debit $7,880

25) Internal control does not:

A) help safeguard the assets a business uses in its operations

B) guarantee a company will not go bankrupt

C) prevent and detect error and fraud

D) promote operational efficiency

26) After all of the account balances have been extended to the income statement

columns of the worksheet, the totals of the debit and credit columns are $172,300 and

$176,900, respectively. It can be concluded the company has a:

A) net loss of $14,600

B) net income of $4,600

C) net income of $176,900

D) net loss of $176,900

27) Which of the following items are both reconciling items on the book side of the

reconciliation?

A) Outstanding cheques and correction of book error

B) Deposit in transit and NSF cheque

C) Bank service charge and outstanding cheques

D) Bank service charge and correction of book error

28) One of the differences between IFRS and ASPE is that:

A) ASPE is used mostly in Europe

B) IFRS uses accrual accounting; ASPE uses cash-basis accounting

C) IFRS uses cash-basis accounting; ASPE uses accrual accounting

D) to record amortization, IFRS uses the word depreciation; ASPE allows both

depreciation and amortization to be used

29) If the bank mistakenly recorded a $71 deposit as $17, the error would be shown on

the bank reconciliation as a:

A) $71 addition to the bank balance

B) $54 addition to the bank balance

C) $71 deduction from the bank balance

D) $54 deduction from the bank balance

30) The acid-test ratio would include in the numerator:

A) cash, short-term investments, and prepaid expenses

B) inventory, cash, and short-term investments

C) cash, short-term investments, and net current receivables

D) cash, inventory, and prepaid expenses

31) Bathworks Company wants to estimate its ending inventory based on the following

data: beginning inventory of $70,000, net sales revenue of $195,000, purchases of

$140,000, and a normal gross margin percent of 40%. Ending inventory is equal to:

A) $78,000

B) $117,000

C) $93,000

D) $132,000

32) State whether the following accounts are assets, liabilities or owner’s equity.

a)________Equipment

b)________Capital

c)________Supplies

d)________Accounts payable

e)________Accounts receivable

f)________Wages payable

g)________Cash

33) Intangible assets are classified on the balance sheet as:

A) long-term assets

B) property, plant and equipment

C) current assets

D) a component of owner’s equity

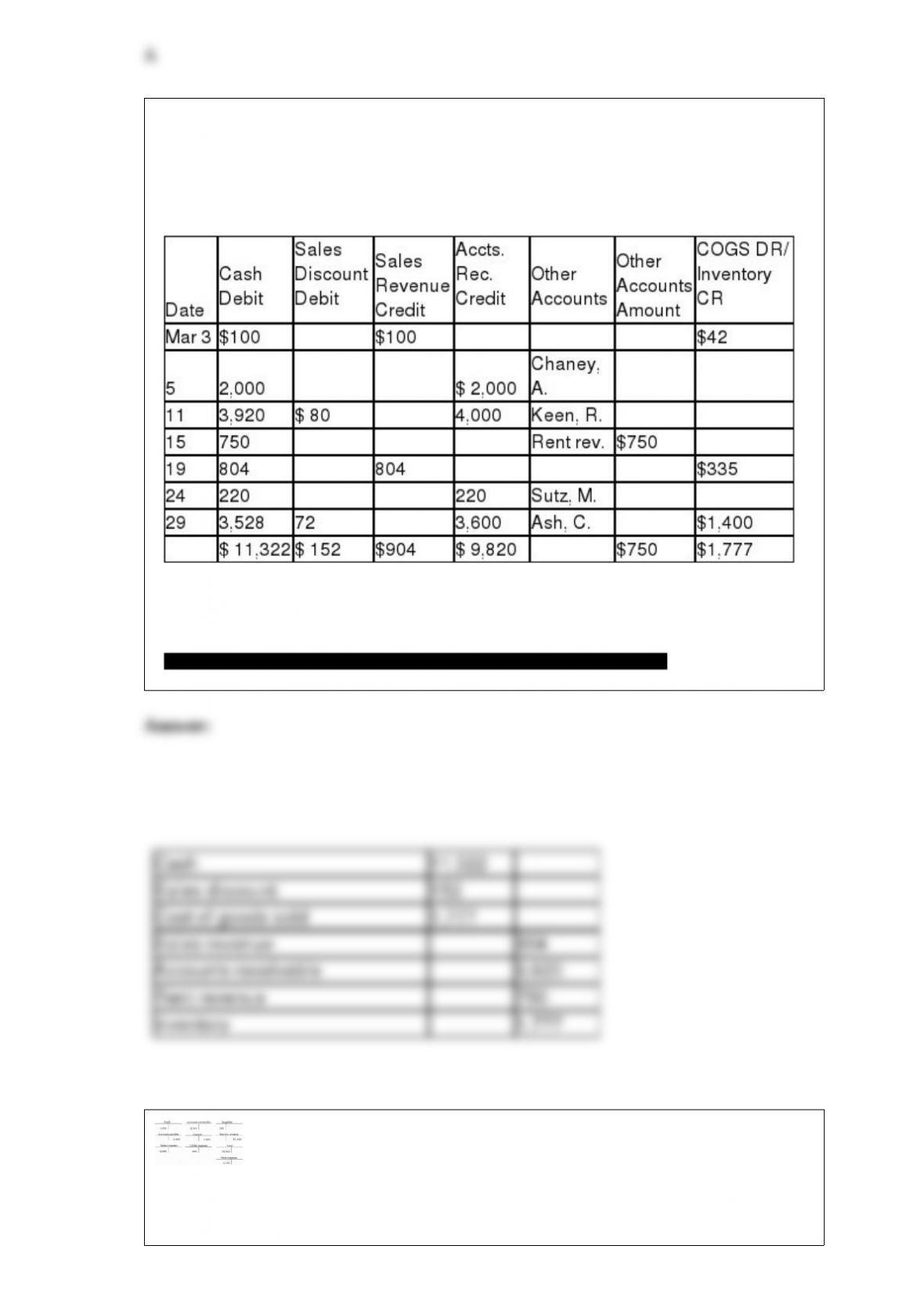

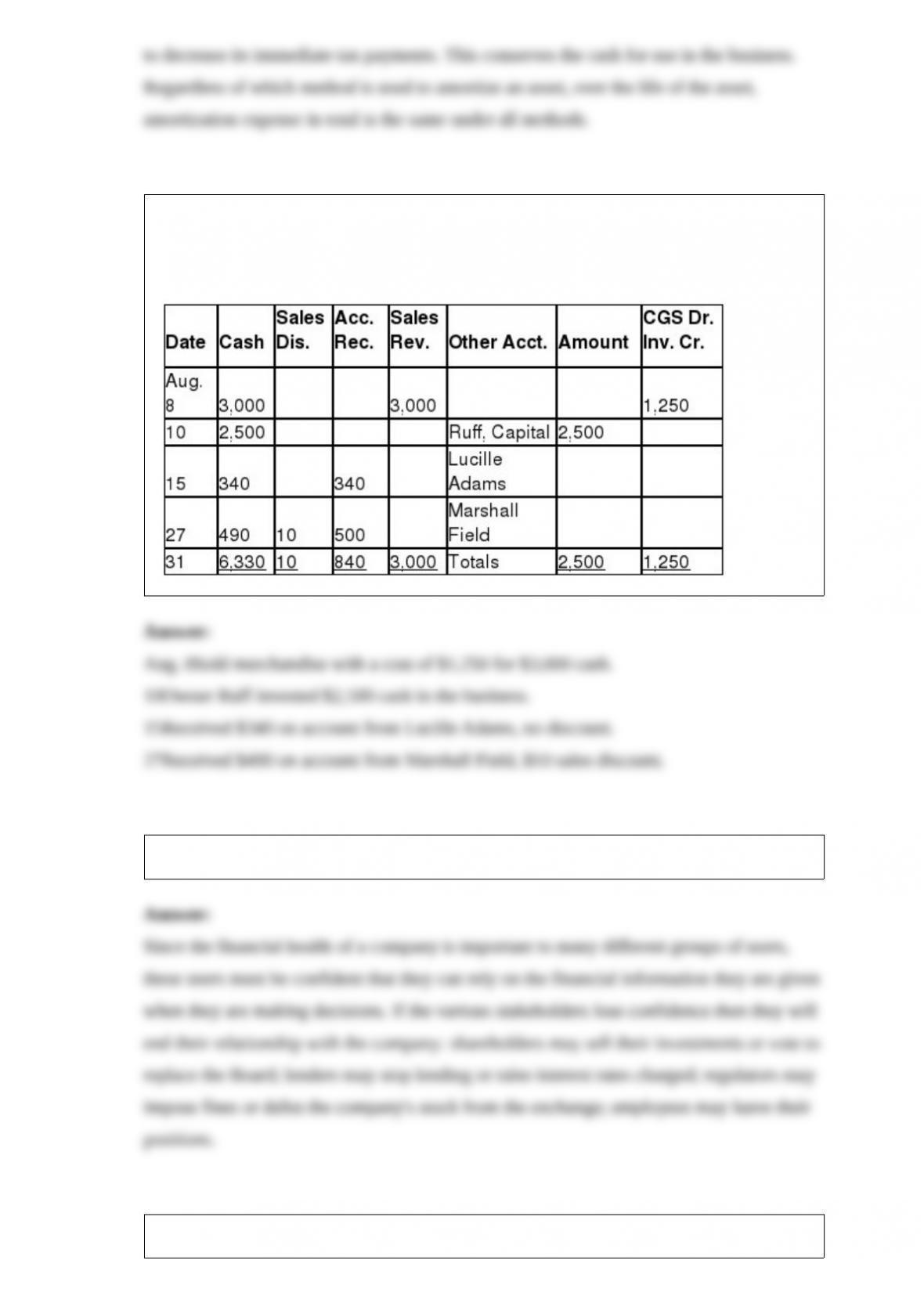

34) Martin Manufacturing Company uses a cash receipt journal. At the end of March,

the cash receipts journal was completed as follows:

Cash Receipts Journal

Provide a summary general journal entry, including all accounts that were affected

during the month.

35) Table 3-3

The unadjusted trial balance of Holitzner Roof Repairs appears below as at December

31, 2014 .

DebitCredit

Cash$5,300

Accounts receivable7,600

Roofing supplies1,100

Equipment6,000

Accumulated amortization$1,200

Salaries payable1,100

Interest payable

Unearned service revenue300

Note payable10,000

Carmen Holitzner, capital6,400

Carmen Holitzner, withdrawals600

Service revenue3,000

Salaries expense500

Amortization expense

Rent expense2,100

Roofing supplies expense

Interest expense__________

$22,600$22,600

Refer to Table 3-3. Given the following information, prepare the necessary adjusting

entries at year end, December 31, 2014 .

a) A physical count reveals only $520 of roofing supplies are on hand at December 31,

2014 .

b) The equipment is amortized at a rate of $120 per month.

c) Unearned service revenue amounted to $200 at December 31, 2014 .

d) Accrued salary expense at December 31, 2014, amounts to $150.

e) Interest accrued on the note payable at December 31, 2014, amounts to $50.

36) Amounts are posted individually from the purchases journal to the:

A) cash account in the general ledger

B) inventory account in the general ledger

C) accounts payable account in the general ledger

D) accounts payable subsidiary ledger

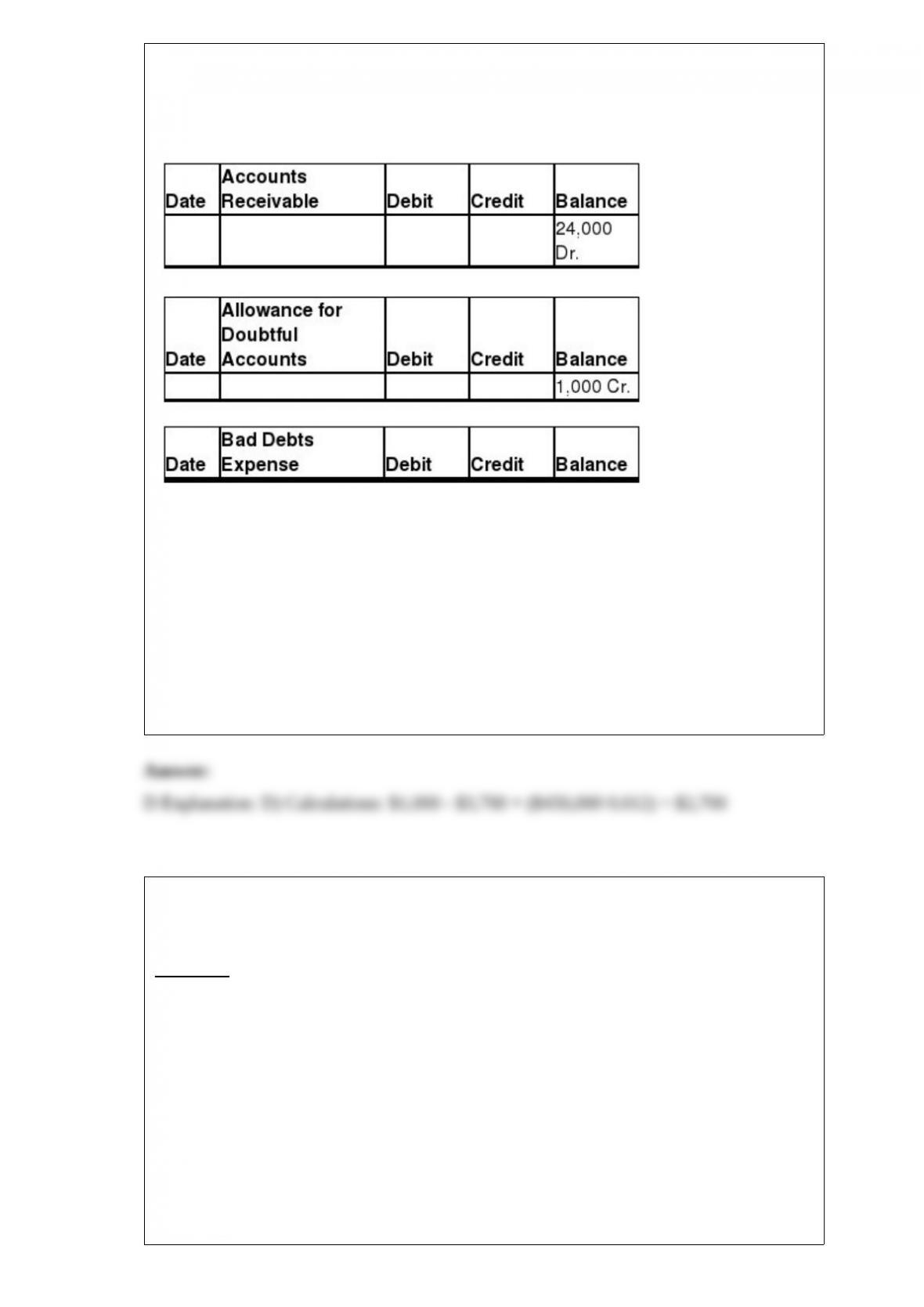

37) Santagos Industries gathered the following information from its accounting records

for the year ended December 31, 2013, prior to adjustment:

Net credit sales for the year$730,000

Accounts receivable balance, Dec. 31, 2013142,000

Allowance for doubtful

accounts balance, Dec. 31, 20131,850Dr.

Santagos uses the allowance method of accounting for uncollectible accounts and

estimates bad-debt expense at 1.5% of net credit sales.

Required:

a) Prepare the adjusting entry to record bad-debt expense on December 31, 2013 .

b) Determine the balance in allowance for doubtful accounts after the adjusting entry is

prepared.

c) Show how the receivables would be reported on the December 31, 2013, balance

sheet for Santagos Industries.

38) Table 11-17

Grant Caballero works for a media company. He earns $3,000 a week for a 40-hour

week and time and a half for anything over 40 hours per week. During the first week of

the year, Grant worked 45 hours. The income tax withholdings are 25% of gross

earnings. Canada Pension Plan deductions are 4.95% of gross earnings and

Employment Insurance deductions are 1.83% of gross earnings. The worker’s

compensation premium is 1.6% of gross earnings. Both Grant and the company

contribute 5% of gross earnings into a group RRSP. In addition Grant has $25 deducted

from his weekly pay to contribute to his favorite charity, Accounting Students’ Tutor

Fund.

Refer to Table 11-17. What is the amount of the employee’s share of the Canada

Pension Plan payable amount if the exemption is used in the calculation?

39) Most companies use straight-line amortization for their books but an accelerated

method for the tax return. Explain why companies use these two different methods that

result in the need for two sets of records.

40) Given the following unidentified journal, write an explanation for each transaction.

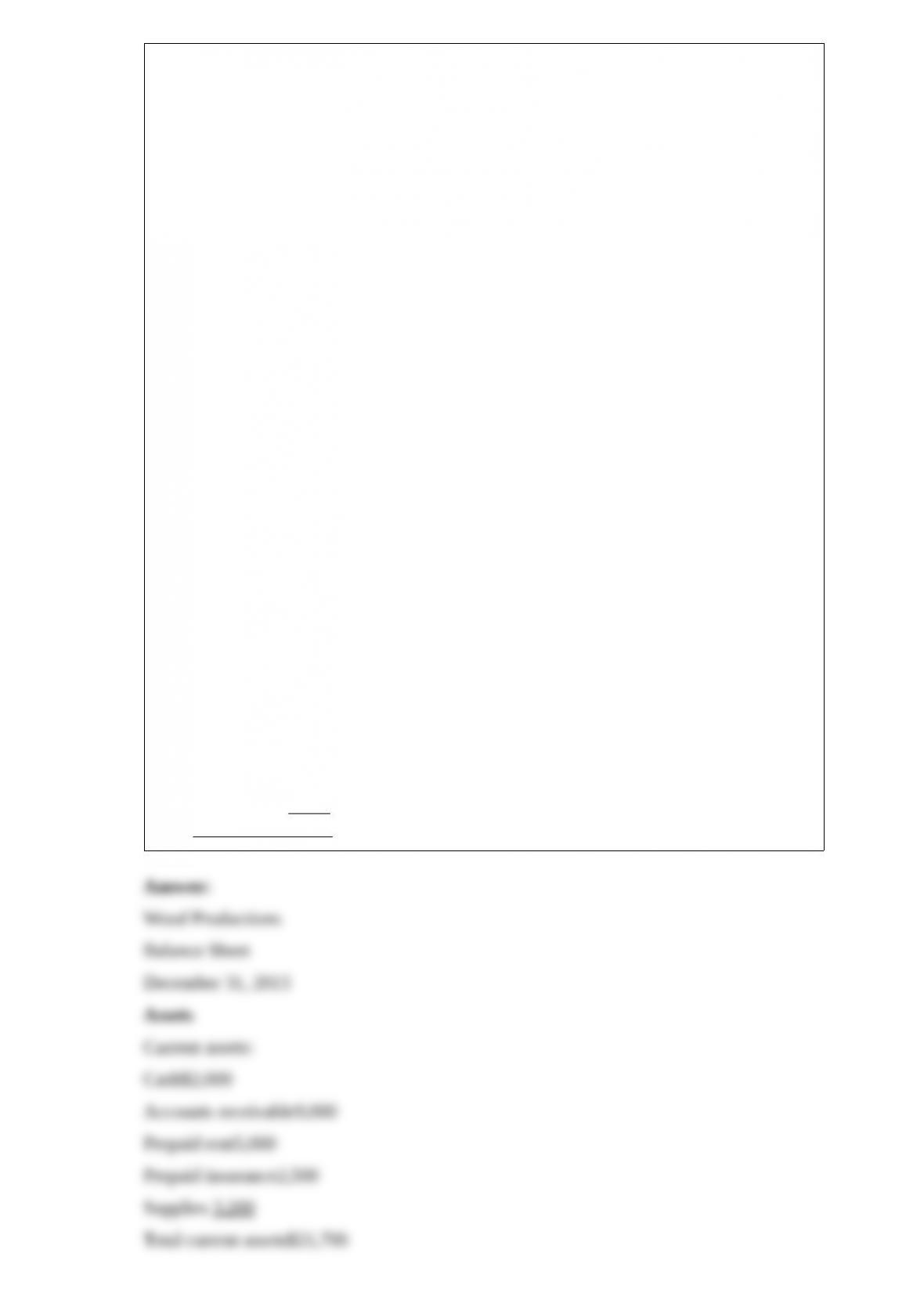

|Debits|Credits|

41) Why is it in the interest of a corporation for management to behave ethically?

42) Prepare a classified balance sheet in report form based on the adjusted trial balance

for the Wood Productions on December 31, 2013 .

Wood Productions

Adjusted Trial Balance

December 31, 2013

DebitCredit

Cash$2,000

Accounts receivable9,000

Prepaid rent5,000

Prepaid insurance2,500

Supplies3,200

Land30,000

Building50,000

Accumulated amort.-building$10,000

Equipment35,000

Accumulated amort.-equipment7,000

Accounts payable8,000

Salary payable3,000

Interest payable1,000

Mortgage payable

(due 12/31/2018)40,000

Jennifer Wood, Capital84,900

Jennifer Wood, Withdrawals10,000

Service revenue80,000

Salary expense28,000

Insurance expense5,000

Rent expense12,000

Utilities expense15,000

Advertising expense9,000

Amortization expense-building10,000

Amortization expense-equipment7,000

Supplies expense 1,200________

Total$233,900$233,900

43) Samson Distributing purchased a patent at a cost of $45,000 on June 30, 2013 . It is

estimated the the patent has a remaining useful life of 4 years in spite of the fact that the

patent will expire in 6 years from the date of purchase. Samson has a December year

end.

Record the amortization for 2013 for the patent.

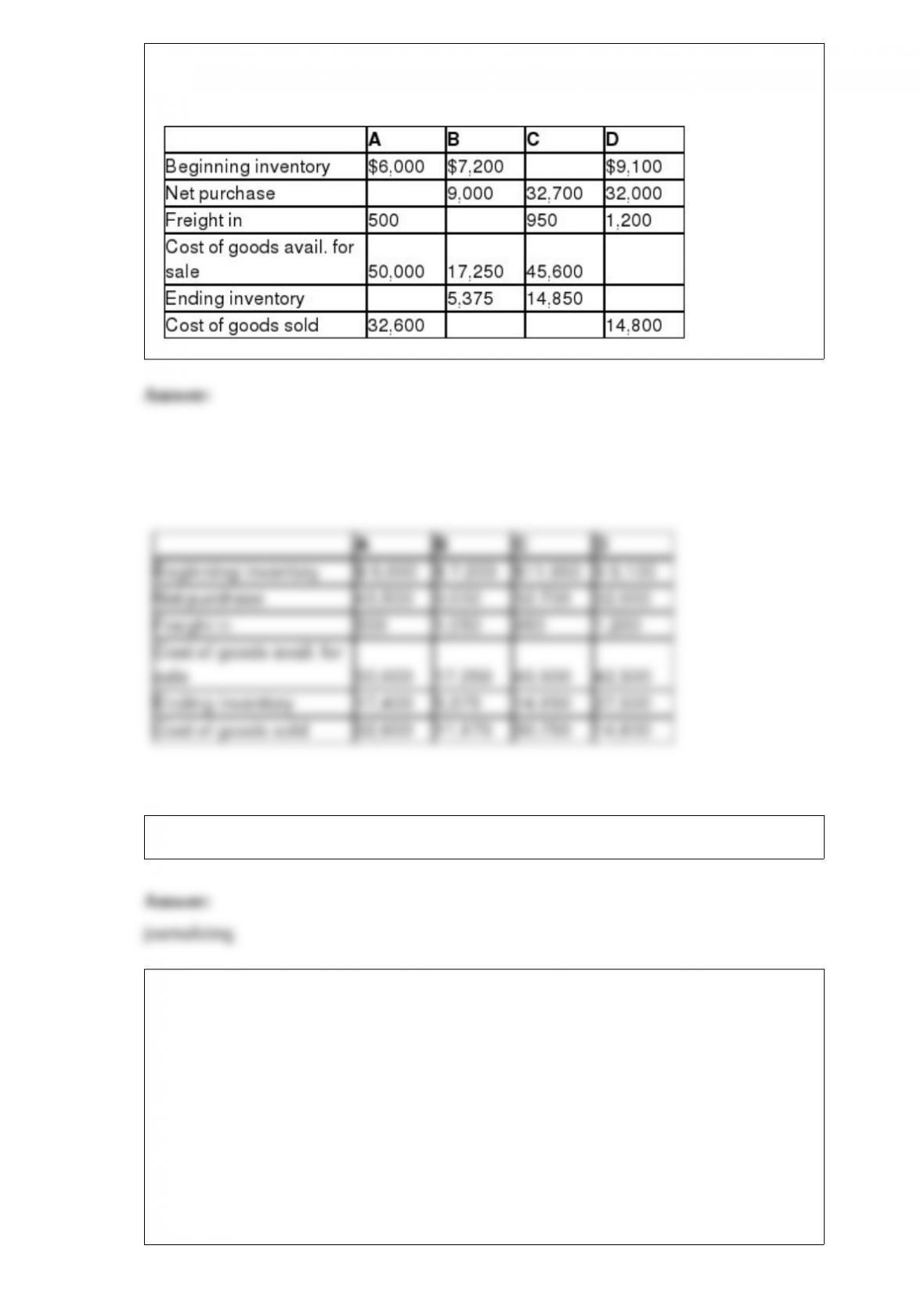

44) Fill in the missing amounts for each case in the table presented below:

45) The process of entering transactions into the journal

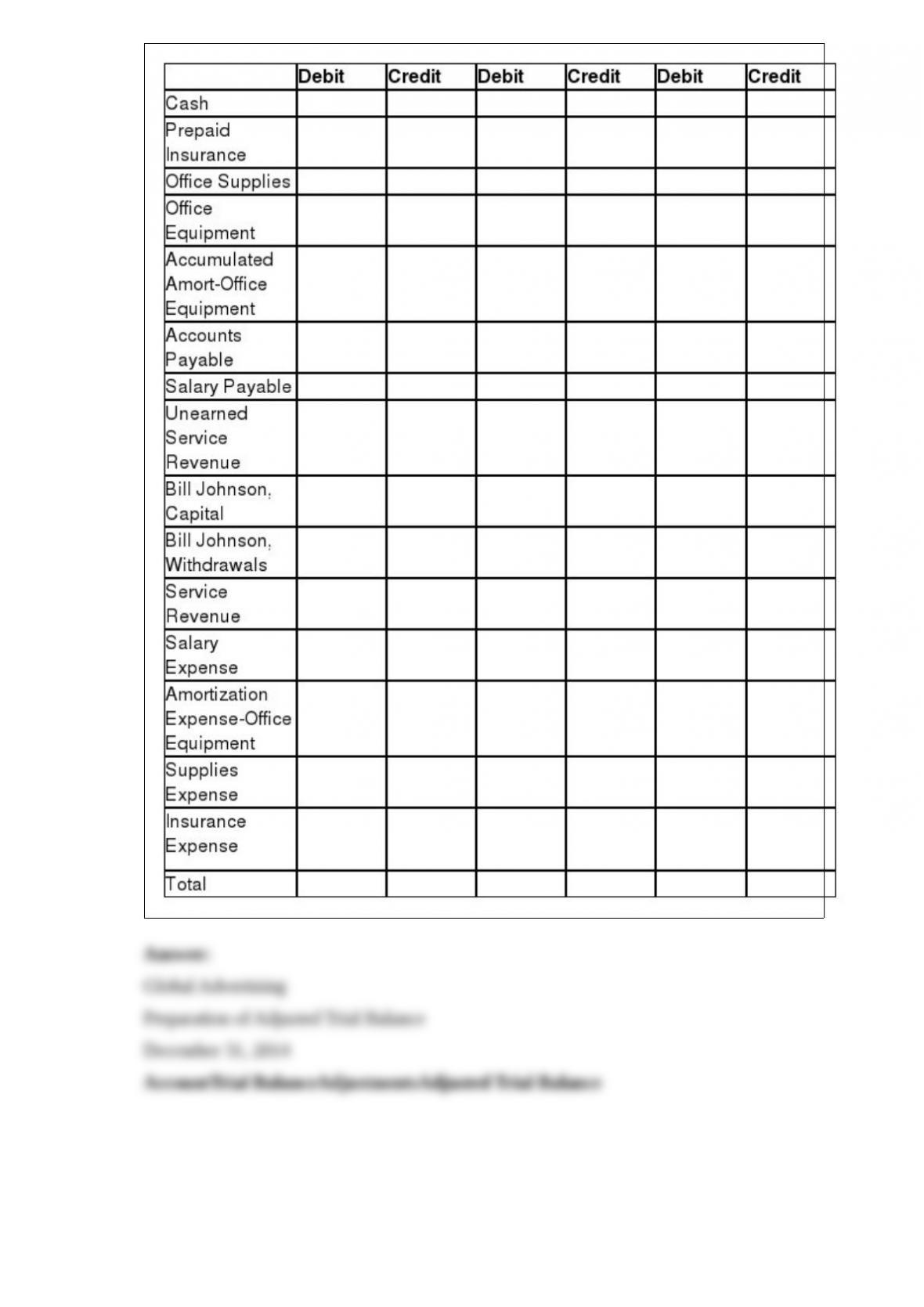

46) The following unadjusted account balances and adjustment data are for Global

Advertising as of December 31, 2014:

Cash$14,000

Prepaid insurance3,000

Office supplies900

Office equipment15,500

Accumulated amort.-office equipment4,500

Accounts payable1,600

Salary payable0

Unearned service revenue5,500

Bill Johnson, Capital14,900

Bill Johnson, Withdrawals11,000

Service revenue29,700

Salary expense11,800

Amort. expense-office equipment0

Supplies expense0

Insurance expense0

Adjustment data:

Office supplies on hand December 31, 2014, $500

Prepaid insurance expired during 2014, $275

Unearned service revenue, December 31, 2014, $1,500

Amortization on equipment for 2014, $2,800

Accrued salaries, $1,800

Fill in the trial balance, adjustments, and adjusted trial balance columns in the following

table.

Global Advertising

Preparation of Adjusted Trial Balance

December 31, 2014

AccountTrial BalanceAdjustmentsAdjusted Trial Balance

47) Based on the following adjusted account balances, prepare a statement of owner’s

equity for the MacMahan Services for the year ended December 31, 2014 .

Service revenue 8,300

Advertising expense1,100

Salary expense6,800

Mandy MacMahan, Capital, Jan. 1, 20145,150

Insurance expense900

Supplies expense1,350

Mandy MacMahan, Withdrawals3,200