The annual pension expense for what type of pension plan(s) is recorded by a journal

entry that includes a debit to pension expense and a credit to a noncurrent liability?

a. A defined benefit plan only.

b. A defined contribution plan only.

c. Both a defined benefit and a defined contribution plan.

d. This is not the correct entry.

Liddy Corp. began constructing a new warehouse for its operations during the current

year. In the year Liddy incurred interest of $30,000 on a working capital loan, and

interest on a construction loan for the warehouse of $60,000. Interest computed on the

average accumulated expenditures for the warehouse construction was $50,000. What

amount of interest should Liddy expense for the year?

a. $ 30,000.

b. $ 40,000.

c. $ 90,000.

d. $140,000.

Which of the following differences between financial accounting and tax accounting

ordinarily creates a deferred tax asset?

a. Unrealized loss from recording inventory impairments.

b. Prepaid expenses.

c. Installment sales for which taxable income recognized when cash is collected.

d. None of these answer choices are correct.

The difference between single-step and multiple-step income statements is primarily an

issue of:

a. Consistency.

b. Presentation.

c. Measurement.

d. Valuation.

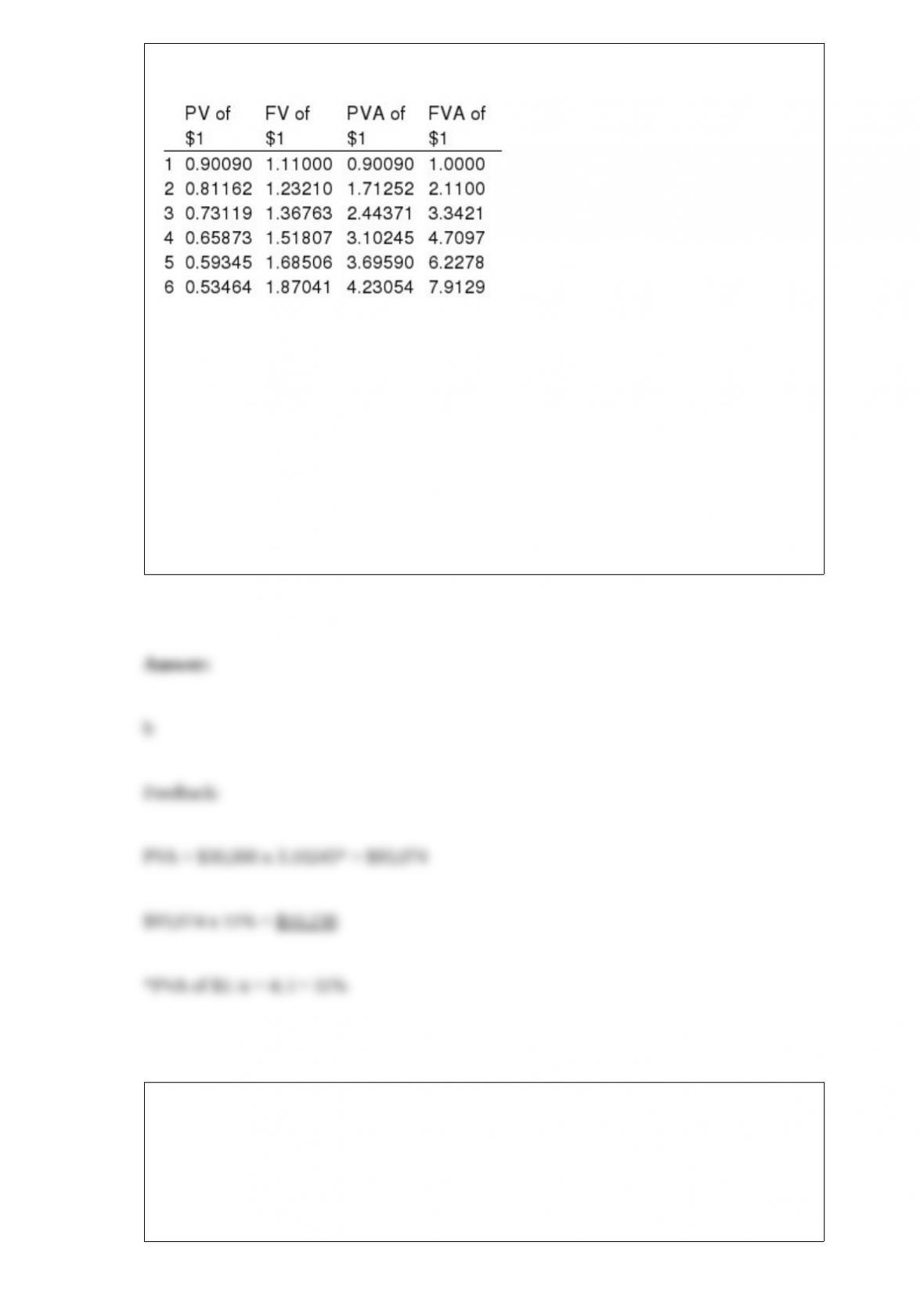

Present and future value tables of 1 at 11% are presented below.

Titanic Corporation leased executive limos under terms of $20,000 down and four equal

annual payments of $30,000 on the anniversary date of the lease. The interest rate

implicit in the lease is 11%. The first year’s interest expense would be:

a. $13,200.

b. $10,238.

c. $33,200.

d. $15,543.

In computing capitalized interest, average accumulated expenditures:

a. Is the arithmetic mean of all construction expenditures.

b. Is determined by time-weighting individual expenditures made during the asset

construction period.

c. Is multiplied by the company’s most recent financing rates.

d. All of these answer choices are correct.

If Frasquita accrued interest of $15,000 on the note in its 2016 year-end financial

statements, what would the manufacturer record in its 2016 income statement for this

transaction?

a. $15,000 of interest revenue.

b. $25,000 of interest revenue.

c. $15,000 of interest revenue and $525,000 of sales revenue.

d. $550,000 of sales revenue.

On September 1, 2016, Hiker Shoes issued a $100,000, 8-month, noninterest-bearing

note. The loan was made by Second Commercial Bank where the stated discount rate is

9%. Hiker’s effective interest rate on this loan (rounded) is:

a. 9.0%.

b. 9.5%.

c. 9.6%.

d. 9.7%.

Which of the following is correct about changes in estimated variable consideration?

a. Changes in estimated variable consideration should be recognized as an adjustment to

revenue in the period the change in estimate is made.

b. Changes in estimated variable consideration should be applied retroactively to all

periods affected.

c. Changes in estimated variable consideration should be allocated retrospectively to all

prior periods.

d. Changes in estimated variable consideration are not recognized in periods after

transaction price is first estimated.

Working capital is equal to:

a. Currentassets.

b. Currentliabilities.

c. Currentassets plus currentliabilities.

d. Current assets minus currentliabilities.

Which of the following is not an uncertainty that complicates determining how much to

set aside each year to ensure that sufficient funds are available to provide the benefits

promised under a defined benefit plan?

a. Employee turnover.

b. Number of employees who retired last year.

c. Future inflation rates.

d. Future compensation levels.

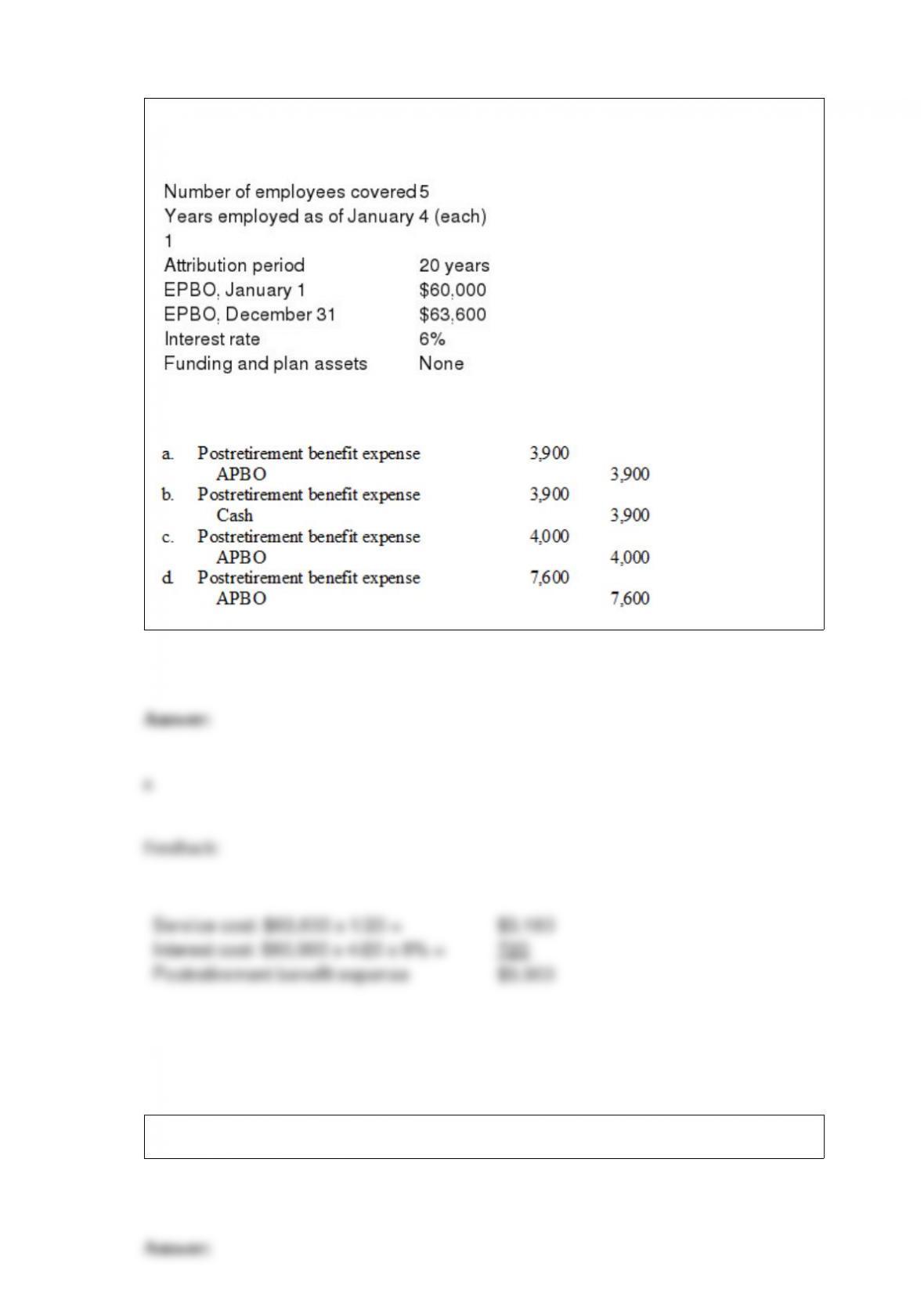

The following data are for Guava Company’s retiree health care plan for the current

calendar year.

What is the correct entry to record postretirement benefit expense for the current year?

What are the general guidelines for an investment to be considered a cash equivalent?

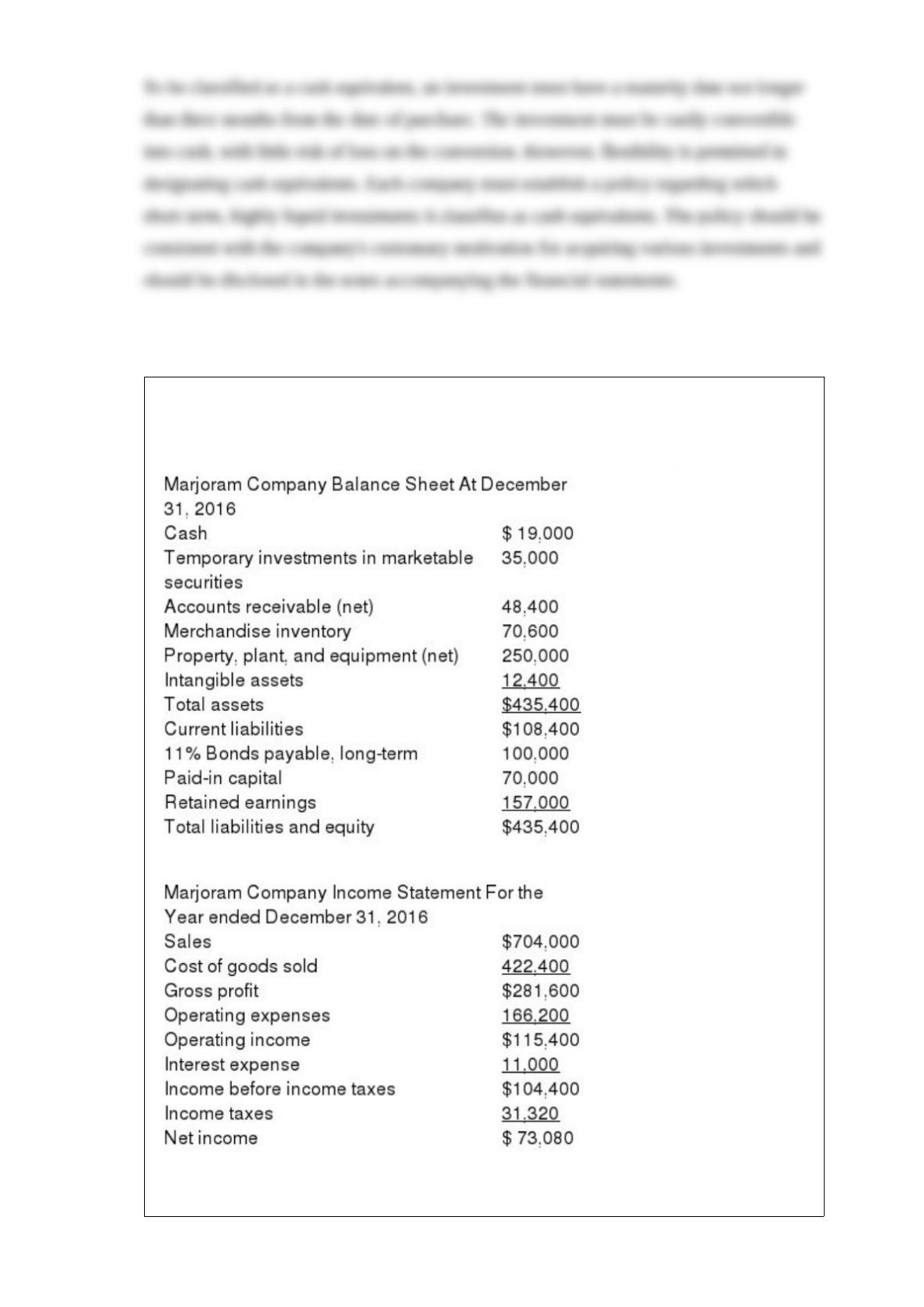

The condensed balance sheet and income statement for Marjoram Company are

presented below.

Compute the debt to equity ratio for Marjoram Company. Round your answer to two

decimal places.

Pinnacle Corporation has been using the straight-line depreciation method to depreciate

some office equipment that was acquired at the beginning of 2013. At the beginning of

2016, Pinnacle decided to change to the sum-of-the-years’-digits method. The

equipment cost $120,000 and is expected to have no salvage value. The estimated

useful life of the equipment is five years. The tax rate is 30%.

Required:

Prepare the journal entry, if any, to record the accounting change at the beginning of

2016.

Indicate the nature of each of the situations described below using the following

three-letter code.

CODE DESCRIPTION

CPR: Change in principle reported retrospectively

CPP: Change in principle reported prospectively

CES: Change in estimate

CRE: Change in reporting entity

PPA: Prior period adjustment required

____ Change from FIFO inventory costing to LIFO inventory costing.

____ Change from LIFO inventory costing to FIFO inventory costing.

____ Change in the composition of a group of firms reporting on a consolidated basis.

____ Change to the installment method of accounting for receivables.

____ Change in actuarial assumptions for a defined benefit pension plan.

____ Change from sum-of-the-years’ digits depreciation to straight-line.

____ Change from expensing extraordinary repairs erroneously recorded as an expense

to

capitalizing the expenditures.

____ Change in the percentage used to determine warranty expense.

____ Change from reporting the equity method for investments to the cost method.

____ Change in the residual value of machinery.

On April 1, 2016, Parks Co. purchased machinery at a cost of $42,000. The machinery

is expected to last 10 years and to have a residual value of $6,000. Required: Compute

depreciation for 2016 and 2017 and the book value of the machinery at December 31,

2016 and 2017, assuming double-declining balance method is used.