A favorable variance would be credited to a cost variance account.

The statement of cash flows provides a link between two balance sheets by showing

how net income (or loss) has changed owners’ equity from one balance sheet date to the

next.

During periods of inflation, the FIFO cost flow assumption will yield a higher cost of

goods sold than LIFO.

A statement of cash flows depicts the way profits have changed during a designated

period.

An increase in a liability is recorded by a credit; an increase in owners’ equity by a

debit.

The quality of earnings tends to be higher for a company that uses accounting principles

and methods that lead to a conservative measurement of earnings.

An oil reserve is depreciated because of physical deterioration or obsolescence.

An overhead application rate is computed by dividing the actual overhead costs by the

expected amount of units in the activity base.

Cumulative preferred stock means the stock is entitled to its regular dividend plus an

additional share of the total amount of declared dividends.

If the account Cash Over and Short has a debit balance, it is reported in the balance

sheet as a current asset.

Treasury stock is stock that is issued and outstanding but not authorized.

Payments of pensions and other benefits to retired workers are recognized as expense in

the period payment is made.

The Dividends account is closed directly to retained earnings at year-end.

In a just-in-time manufacturing system, reliable vendor relationships are essential only

if the prices they charge are the lowest possible prices.

A perpetual inventory system requires the capability of recording the cost of the goods

sold for individual sales transaction.

Federal unemployment taxes apply to a set dollar amount of employee wages and tend

to decline dramatically as the year progresses.

The FASB permits a company to use the direct method or the indirect method for the

statement of cash flows.

Prior period adjustments appear in the statement of retained earnings and in the income

statement for the current year.

The ability of a sole proprietorship to pay its debts may be determined by the financial

strength of the owner.

In a periodic inventory system, the cost of goods sold is determined by the following

end-of-period computation: Beginning Inventory + Purchases – Ending inventory =

Cost of Goods Sold.

A physical inventory is usually taken during a period of high activity.

A performance report can be easily adjusted to show budgeted revenues and costs at

different levels of activity.

Under international accounting standards, companies may revalue their plant and

equipment rather than using historical cost throughout the assets’ lives.

The present value of a future cash flow is the amount you would pay today for the right

to receive that future amount.

When an income statement does not show gross profit or operating income it is called a

consolidated statement.

The behavioral approach to budgeting has as its goal the complete elimination of

inefficiency.

A coal mine is regarded as an underground inventory of coal and is recorded as a

current asset, Underground Coal Inventory, in the balance sheet.

The purchase or sale of marketable securities is reported in the statement of cash flows

as a financing activity.

The maker of a note is the party to whom payment is to be made.

Deducting the cost of goods sold from net income gives us operating income.

A loss contingency is recorded in the accounting records when it is probable that a loss

has been incurred and the amount of the loss is known.

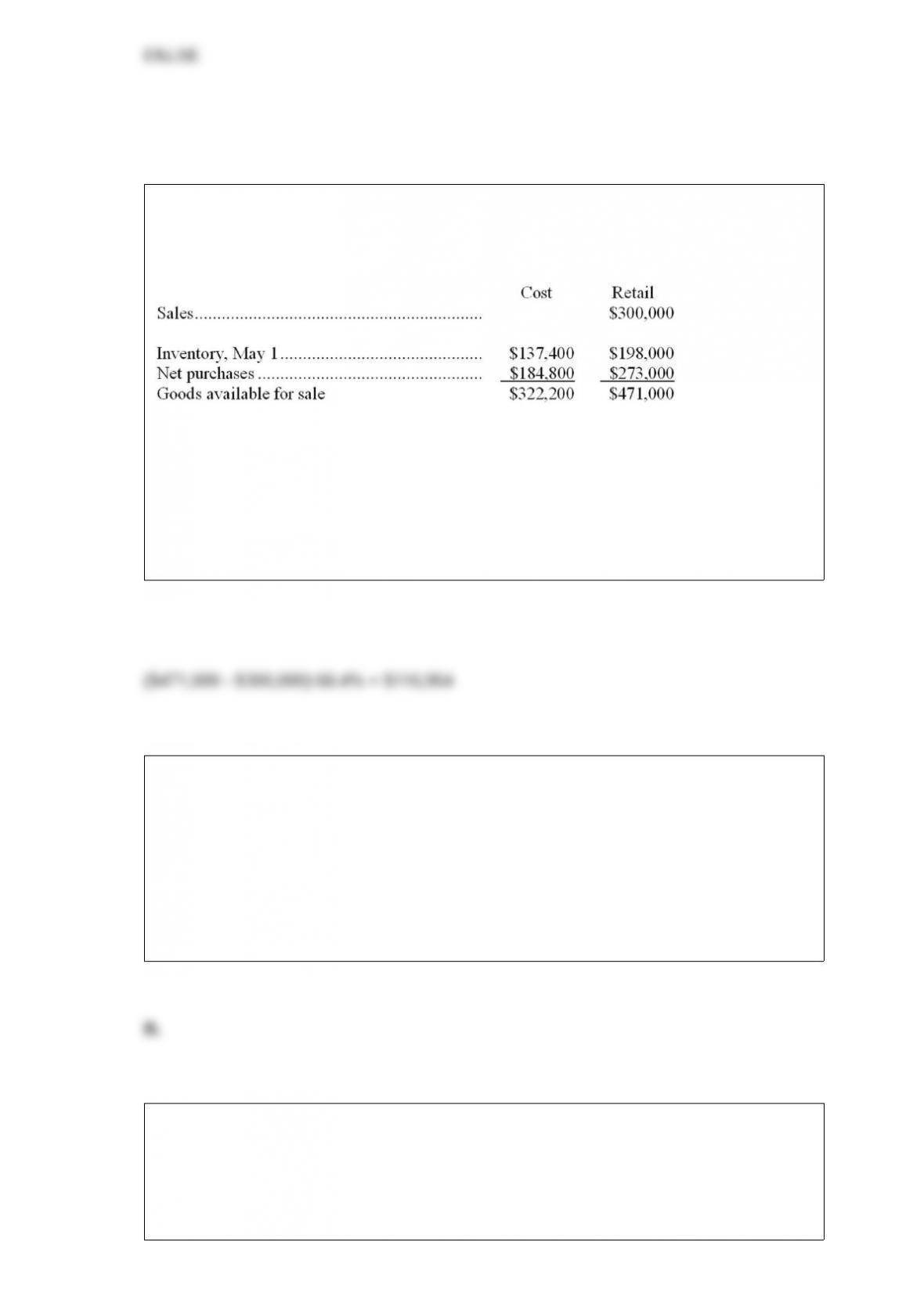

Midwest Office Products uses the retail method to estimate ending inventory in its

monthly financial statements. The following information is available for the month

ended May 31:

Refer to the information above. Estimate the cost of the May 31 inventory using the

retail method.

A. $116,964.

B. $137,400.

C. $150,425.

D. $204,000.

In February of each year, the Carlton Hotel holds a very popular wine tasting event.

Tickets must be ordered and paid for in advance, and are typically sold out by

November of the preceding year. The realization principle indicates that the revenue

from these ticket sales should be recognized in the period in which the:

A. Order is placed.

B. Wine tasting event is held.

C. Payments are received.

D. Expenses associated with the wine tasting are paid in full.

Total stockholders’ equity of Tucker Company is $4,000,000. The fair market value of

Tucker’s net identifiable assets (assets less liabilities) is $5,000,000. Empire

Corporation makes an offer to purchase Tucker’s entire business for $5,800,000. In this

situation:

A. Tucker Company should report goodwill of $800,000 in its balance sheet.

B. Tucker Company should report goodwill of $1,800,000 in its balance sheet.

C. Empire Corporation is willing to pay $1,800,000 for goodwill generated by Tucker,

and Empire will report this goodwill in its balance sheet if the purchase is finalized.

D. Empire Corporation is willing to pay $800,000 for goodwill generated by Tucker,

and Empire will report this goodwill in its balance sheet if the purchase is finalized.

The purchasing agent of Superb Service Co. wants to know the dollar amount of

inventory purchased on account during the year from a particular supplier. This

information can be found most easily in Superb Service’s:

A. Inventory subsidiary ledger.

B. Accounts payable controlling account.

C. Inventory controlling account.

D. Accounts payable subsidiary ledger.

Rent expense in Burr Company’s income statement is $480,000. If Prepaid Rent was

$120,000 on January 1 and is $95,000 on December 31, the cash paid for rent during

the year is:

A. $480,000.

B. $455,000.

C. $360,000.

D. $575,000.

The amount of net income (or loss) will appear on the debit side of the Income

Statement columns in a worksheet if:

A. Revenue exceeds total expenses for the period.

B. The trial balance is out of balance.

C. Dividends are more than the income or loss for the period.

D. There is a net loss for the period.

Castle TV, Inc. purchased 1,000 monitors on January 5 at a per-unit cost of $185, and

another 1,000 units on January 31 at a per-unit cost of $230. In the period from

February 1 through year-end, the company sold 1,800 units of this product. At year-end,

200 units remained in inventory.

Refer to the information above. Assume that Castle TV, Inc. uses the FIFO flow

assumption. The cost of the 200 units in inventory at year-end is:

A. $41,500.

B. $46,000.

C. $37,000.

D. $83,000.

In comparison with a financial statement prepared in conformity with generally

accepted accounting principles, a managerial accounting report is less likely to:

A. Focus upon the entire organization as the accounting entity.

B. Focus upon future accounting periods.

C. Make use of estimated amounts.

D. Be tailored to the specific needs of an individual decision maker.

Which of the following amounts appears in both the Income Statement debit column

and the Balance Sheet credit column of a worksheet?

A. Net income.

B. Net loss.

C. Dividends.

D. Retained earnings.

Which of the following accounts should not be closed?

A. Expenses and revenues.

B. Dividends.

C. Income summary.

D. Accumulated depreciation.

On April 1, 2015, Jetter Corporation reacquired 2,000 shares of its own $10 par stock

for $120,000 cash. On October 15, 2015, 600 of the treasury shares were reissued at a

price of $65 per share.On April 16, 2015, Rodriguez Corporation reacquired 12,000

shares of its own $10 par stock for $660,000 cash. On November 4, 2016, 1,000 of the

treasury shares were reissued at a price of $65 per share. The journal entry to record the

reissuance of the 1,000 shares of stock on November 4 includes a:

A. Credit to Common Stock of $10,000.

B. Credit to Additional Paid-In Capital: Treasury Stock Transactions of $10,000.

C. Credit to Gain on Treasury Stock Transactions of $10,000.

D. Credit to Treasury Stock Reissued of $65,000.

An example of a non-cash investing or financing activity that is disclosed in a

supplementary schedule accompanying the statement of cash flows is:

A. Recording depreciation expense for the current year.

B. Declaring, but not paying, dividends on common stock.

C. Selling land in exchange for a note receivable.

D. Transferring cash from a checking account into a money market fund.

Accounting terminology

Listed below are nine technical accounting terms introduced in this chapter:

Gross profit

Gross profit rate

General ledger

Cost of goods sold

Physical inventory

Subsidiary ledger

Perpetual inventory system

Periodic inventory system

Inventory shrinkage

Each of the following statements may (or may not) describe one of these technical

terms. In the space provided below each statement, indicate the accounting term

described, or answer “None” if the statement does not correctly describe any of the

terms.

______ a. An approach to accounting for inventories and the cost of goods sold used

primarily in small businesses with manual accounting systems.

______ b. A reason why perpetual inventory records may not be entirely accurate.

______ c. The difference between the revenue earned by selling merchandise and the

cost of goods sold.

______ d. Gross profit divided by average total stockholders’ equity.

______ e. An accounting procedure used in both perpetual and periodic inventory

systems. In a perpetual system, this procedure brings to light the amount of inventory

shrinkage. In a periodic system, it is the basis for computing the cost of goods sold.

______ f. An accounting record showing the individual items comprising the balance of

a general ledger account.

______ g. The accounting record in which transactions initially are recorded.

On October 12, 2014, Neptune Corporation invested $700,000 in short-term

available-for-sale marketable securities. The market value of this investment was

$730,000 at December 31, 2014, but had slipped to $725,000 by December 31, 2015.

Refer to the information above. Assuming Neptune does not sell this investment, the

financial statements prepared at December 31, 2015 will report:

A. Investments in Marketable Securities of $700,000, reduced by a $30,000 Unrealized

Holding Gain on Investments, in the asset section of the balance sheet.

B. The asset Investments in Marketable Securities of $700,000 in the balance sheet, and

a $25,000 Unrealized Holding Loss on Investments in the income statement.

C. The asset Investments in Marketable Securities of $725,000, and a $5,000

Unrealized Holding Loss deducted from total stockholders’ equity.

D. Investment in Marketable Securities of $725,000 in the asset section of the balance

sheet, with a $25,000 Unrealized Holding Gain on Investments included in the

stockholders’ equity section.

A measure of a company’s liquidity is:

A. Assets divided by liabilities.

B. The current ratio.

C. The dollar amount of liabilities that bear interest.

D. The dollar amount of assets used as collateral for a loan.

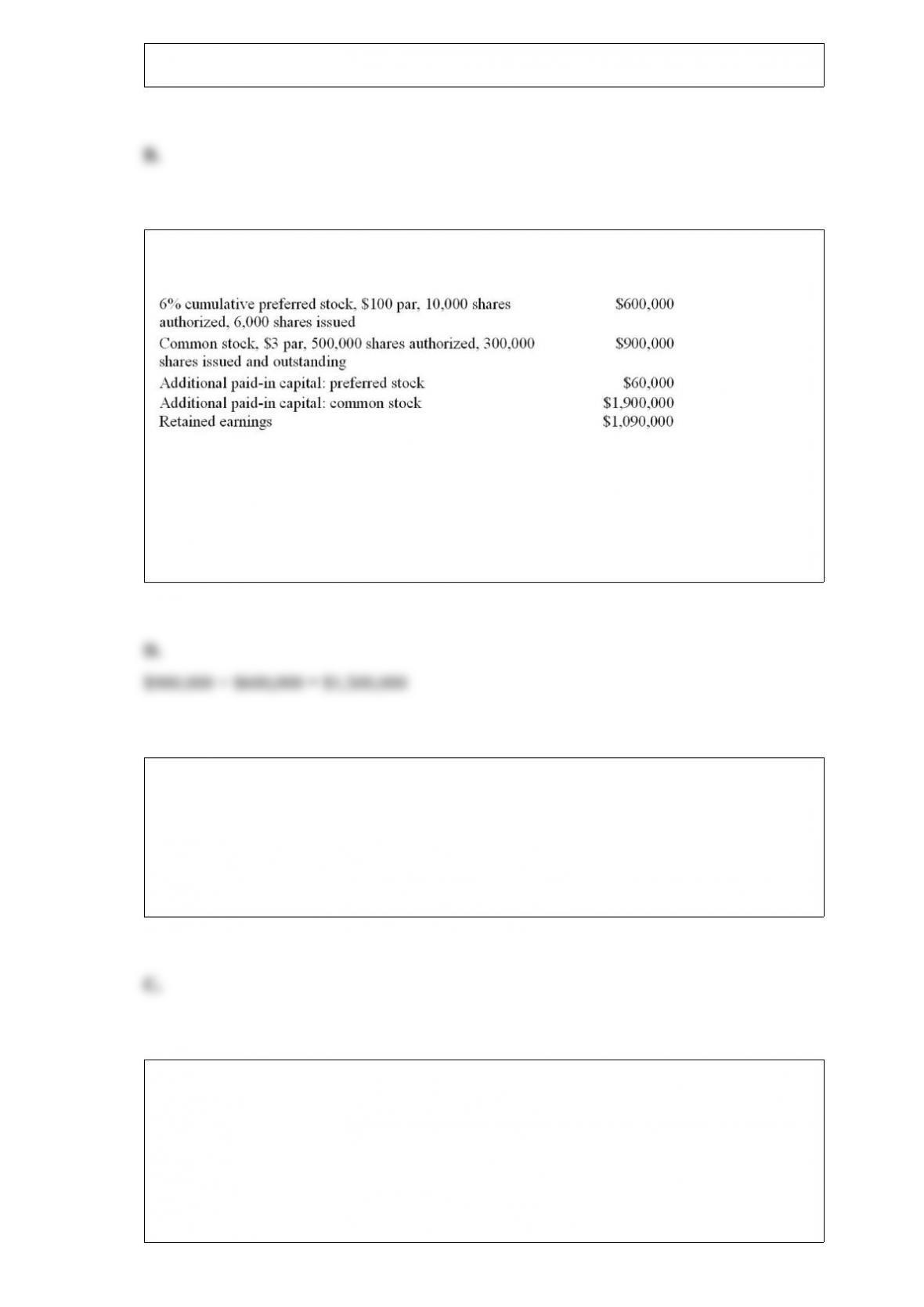

Shown below is information relating to the stockholders’ equity of Grant Corporation at

December 31, 2015:

Dividends have been declared and paid for 2015.

Refer to the information above. Grant’s total legal capital at December 31, 2015, is:

A. $3,160,000.

B. $3,000,000.

C. $2,590,000.

D. $1,500,000.

In a cash budget, the budgeted level of cash receipts depends on all of the following

except:

A. The sales forecast.

B. The credit terms offered to customers.

C. The credit terms offered by suppliers.

D. Experience in collecting receivables.

Suffolk Associates sold office furniture for cash of $42,000. The accumulated

depreciation at the date of sale amounted to $38,000, and a gain of $18,000 was

recognized on the sale. The original cost of the asset must have been:

A. $56,000.

B. $62,000.

C. $84,000.

D. $59,000.

The Foreign Corrupt Practices Act (FCPA) affects all of the following except:

A. United States companies.

B. Foreign companies operating in the United States.

C. Foreign companies operating solely in their home country.

D. Affiliates and agents of a United States company or a foreign company operating in

the United States.

On November 1, 2014, Salem Corporation sold land priced at $900,000 in exchange for

a 6%, six-month note receivable.

Refer to the information above. Assuming the maker of the note defaults on May 1,

2015, Salem will record on this date:

A. An accounts receivable of $900,000 from the maker of the note.

B. An accounts receivable in the amount of $900,000, as well as interest expense of

$27,000.

C. An accounts receivable in the amount of $927,000, as well as interest revenue of

$18,000.

D. An accounts receivable in the amount of $900,000, as well as interest revenue of

$18,000.

The FASB classifies interest received on investments and interest paid on debt

financing as part of operating cash flows, while the IASB:

A. Allows interest received to be classified as either operating or investing and interest

paid as either operating or financing.

B. Allows interest received to be classified as either operating or financing and interest

paid as either operating or investing.

C. Allows interest received to be classified only as investing and interest paid only as

financing.

D. Allows interest received to be classified only as financing and interest paid only as

investing.

Manufacturing overhead is not:

A. A product cost.

B. An indirect cost.

C. A manufacturing cost.

D. A period cost.

Refer to the information above. What is the quick ratio?

A. 1.5 to 1.

B. .7 to 1.

C. .45 to 1.

D. .8 to 1.

In order for investors and creditors to decide whether to invest in a company or loan a

company funds they may:

A. Only analyze financial statements.

B. Only focus on corporate governance.

C. Both analyze financial statements and focus on corporate governance.

D. Neither analyze financial statements nor focus on corporate governance.

The measurement that best reflects investors’ expectations about future earnings is:

A. Earnings per share.

B. Return on assets.

C. The price-earnings ratio.

D. Return on equity.

During periods of rising prices, and being primarily concerned with tax implications,

most of the companies would select:

A. LIFO.

B. FIFO.

C. Specific identification.

D. The inventory valuation does not affect taxation.

In the notes to financial statements, adequate disclosure would typically not include:

A. The accounting methods in use.

B. Lawsuits pending against the business.

C. Customers that account for 10 percent or more of the company’s revenues.

D. The optimism of the CFO regarding future profits.

When an installment note is structured as a “fully amortizing” loan with equal monthly

payments (such as a traditional mortgage):

A. The portion of each payment allocated to interest expense is the same each month.

B. The sum of the monthly payments is equal to the amount of the installment note

(mortgage).

C. The difference between the sum of all monthly payments and the principal amount of

the note constitutes interest.

D. The portion of each payment allocated to repayment of principal decreases each

month as the mortgage is paid off.

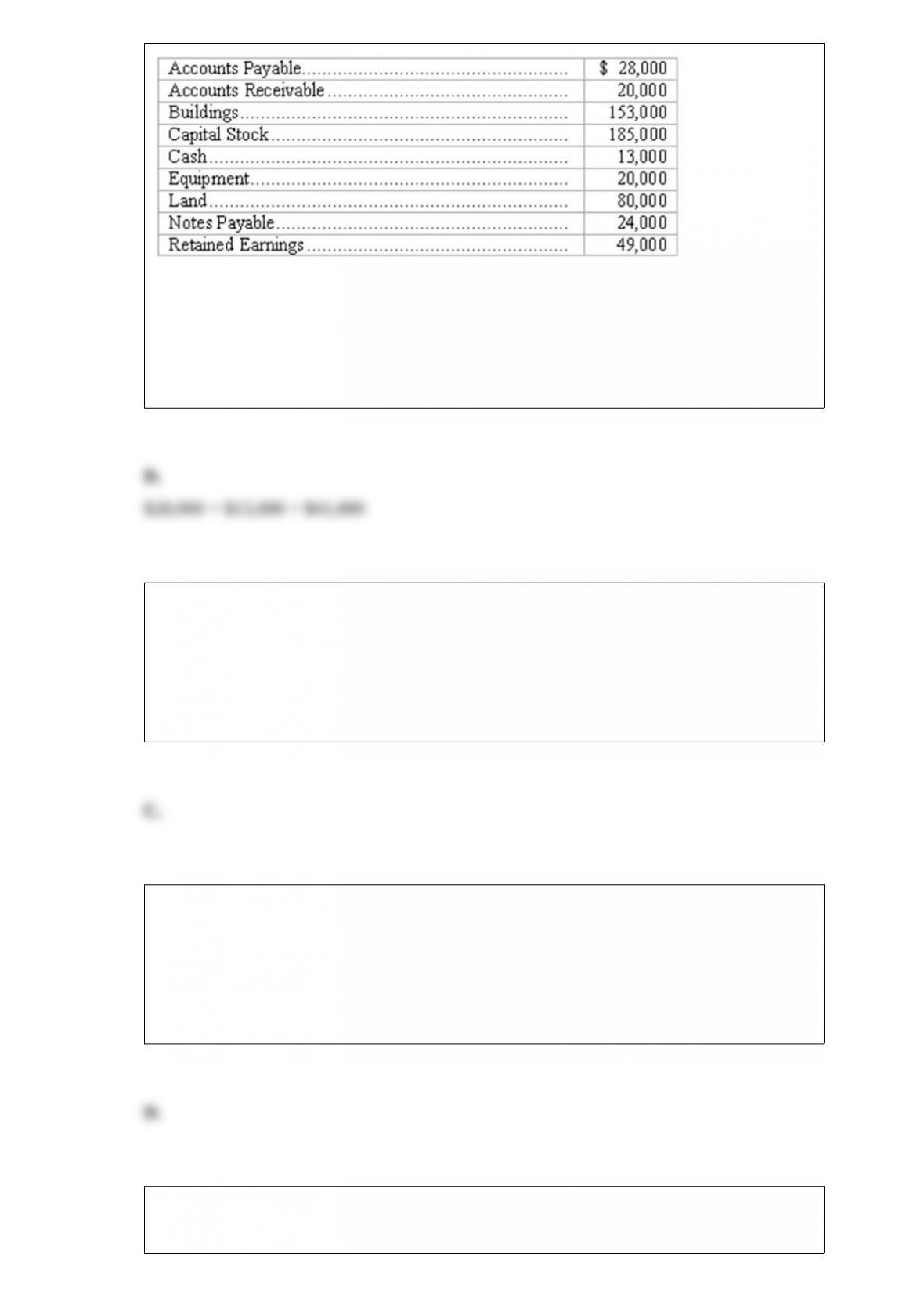

Ceramic Products, Inc. reports these account balances at January 1, 2015 (shown in

alphabetical order):

On January 5, Ceramic Products collected $12,000 of its accounts receivable and paid

$11,000 on its note payable. On January 6, 2015, total liabilities are:

A. $0.

B. $30,000.

C. $56,000.

D. $41,000.

The minimum rate of return used by an investor to bring future cash flows to their

present value is called:

A. The investment rate.

B. The prime rate.

C. The discount rate.

D. The present rate.

A promissory note:

A. Is a conditional promise in writing to pay on demand or at a future date a definite

sum of money.

B. Is recorded by the maker by crediting Note Receivable.

C. Is signed by the person promising to pay the note, called the payee.

D. Will be recorded on both the books of the payee and the maker.

Which of the following events is not a transaction that would be recorded in a

company’s accounting records?

A. The purchase of equipment for cash.

B. The purchase of equipment on account.

C. The investment of additional cash in the business by the owner.

D. The death of a key executive.

A company issues $50 million of bonds at par on January 1, 2015. The bonds pay 10%

interest semi-annually on 12/31 and 6/30 and mature in 20 years. The journal entry

when the bonds are sold is:

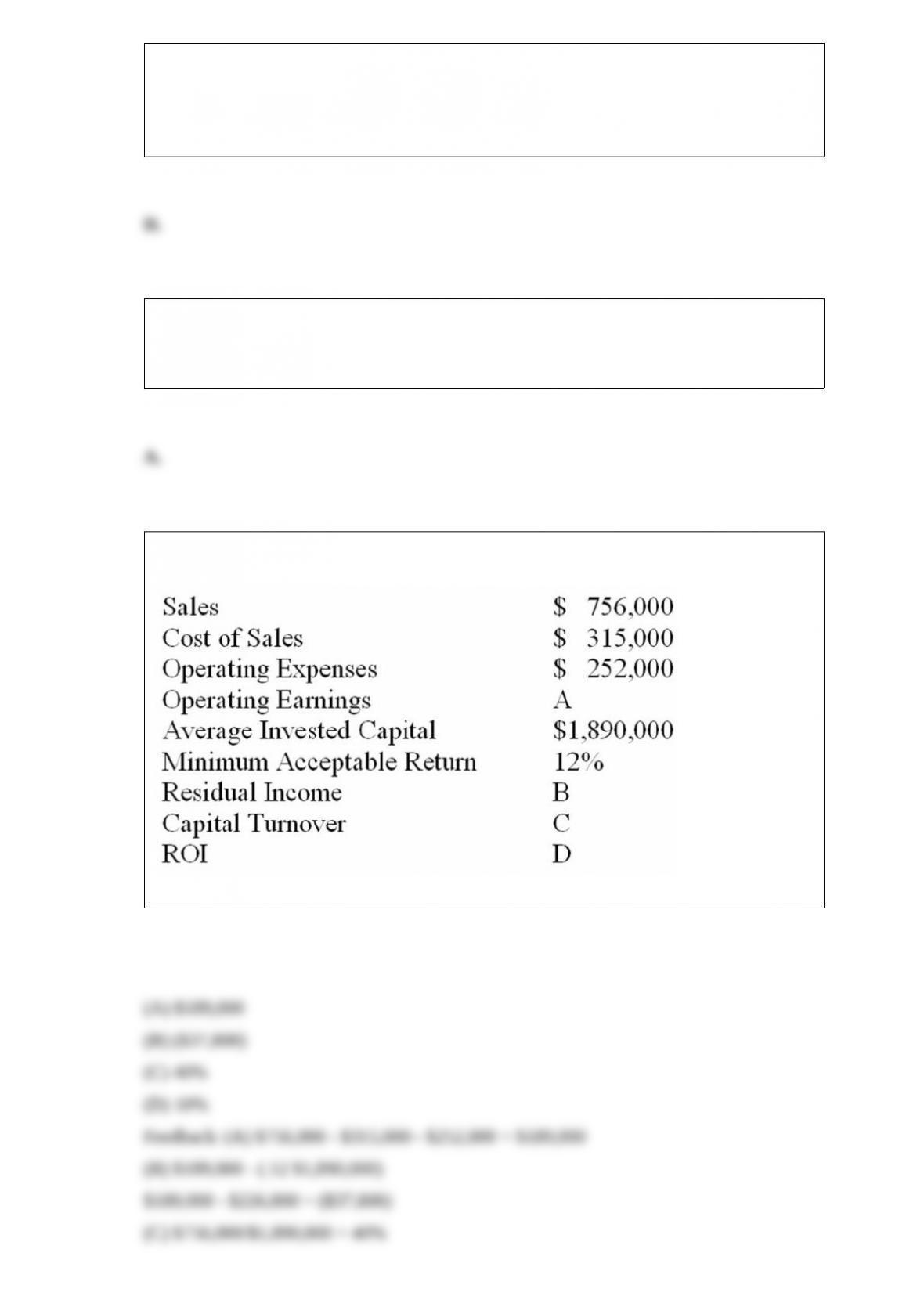

The following information is available for the Hancock Company.

Compute the answers for items A-D.

Capital budget audit

Briefly discuss the reasons that a company’s management would conduct a regular

capital budget audit.

Objectives of financial reporting

List and briefly describe the objectives of financial reporting beginning with the most

general and ending with the most specific.

Identify and explain the components of management compensation and the tradeoffs

that compensation designers make.

Computation of goodwill

The income of Greystone, Inc., during the last several years has averaged $765,000

annually. The company is now being offered for sale as a going concern. The value of

Greystone’s net identifiable assets (total assets minus all liabilities) at the present time is

$4,675,000.

One of several corporations interested in buying Greystone, offers to pay an amount

equal to the value of the net identifiable assets and to assume all liabilities. In addition,

this prospective buyer is willing to pay for goodwill an amount equal to net earnings in

excess of 10% on net assets, expected to continue four years.

You are to use the above information as a basis for computing the price that the

investing corporation will offer for Greystone, Inc. $________________.

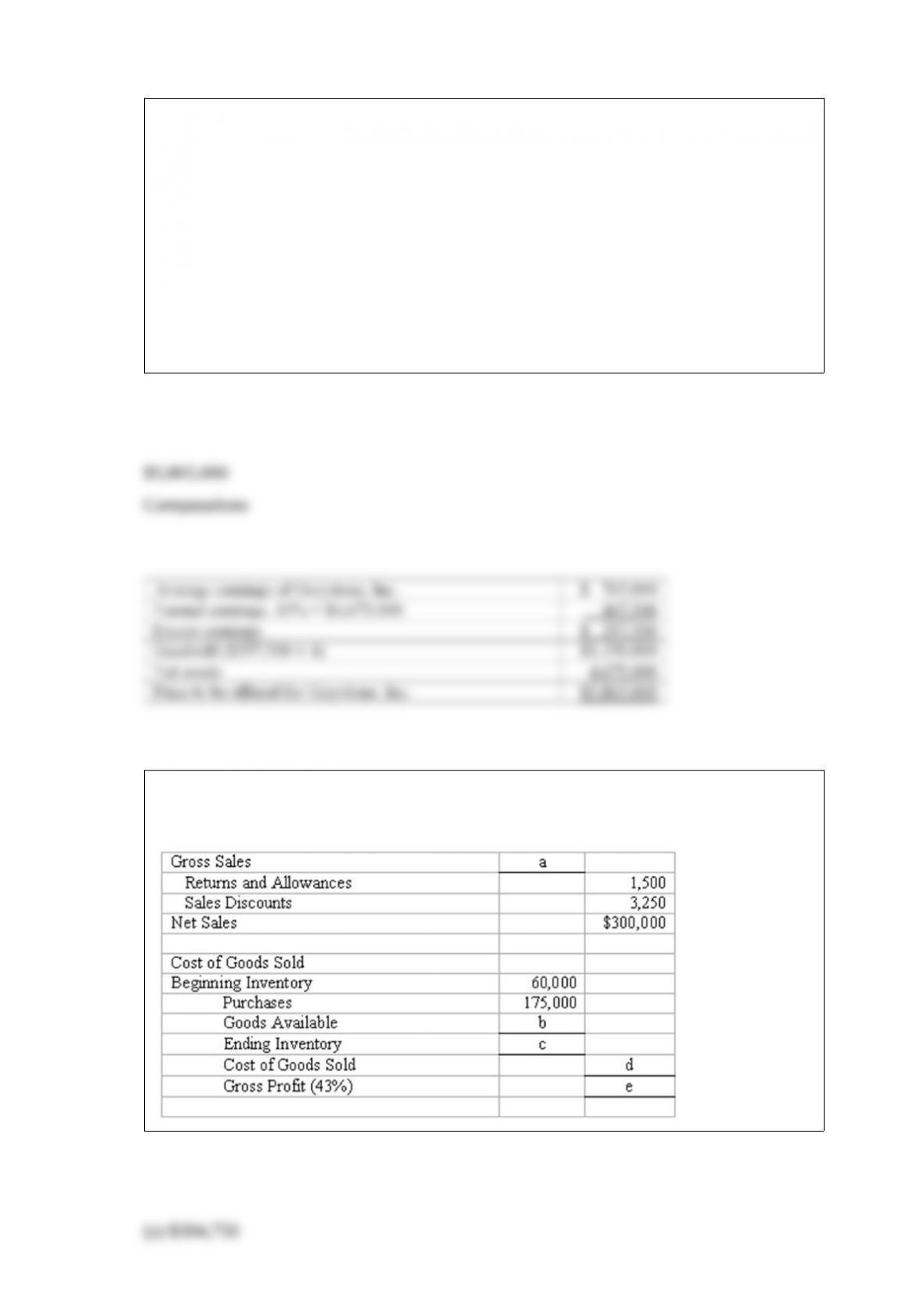

The Multi-Tech Company uses the gross profit method to estimate inventories. Fill in

the missing amounts.

Financial statements

Briefly describe the balance sheet, the income statement, and the statement of cash

flows.

Fully amortizing installment notes

When Sue Meadow purchased a home, she signed a $150,000, 12%, fully amortizing

mortgage note, payable at $1,543 per month. After making the first monthly payment,

Meadow received a notice from the bank stating that $1,500 of the payment had applied

to interest, and only $43 reduced the principal amount of the loan. Meadow does not

understand how this loan is fully amortizing over a period of 30 years. She computes

that at $43 per month, it will take approximately 3,488 months (or 290 years) to repay

this loan. Evaluate Meadow’s analysis.