Which of the following is not true about accounting for investments using the equity

method under IFRS?

a. IFRS requires the equity method when the investor exercises significant influence

over the investee.

b. IFRS is more restrictive than U.S. GAAP concerning when an investor can elect the

fair value option.

c. IFRS requires that the accounting policies of an investee be adjusted to correspond to

those of the investor when applying the equity method.

d. IFRS does not allow use of the equity method where two or more investors have joint

control.

When the total expenses over the life of an operating lease are compared to the total

expenses over the life of a capital lease, one will find that:

a. The expenses of a capital lease are greater than the expenses of the operating lease.

b. The expenses of the capital lease and operating lease are equal.

c. The expenses of an operating lease are greater than the expenses of a capital lease.

d. No meaningful comparison can be made.

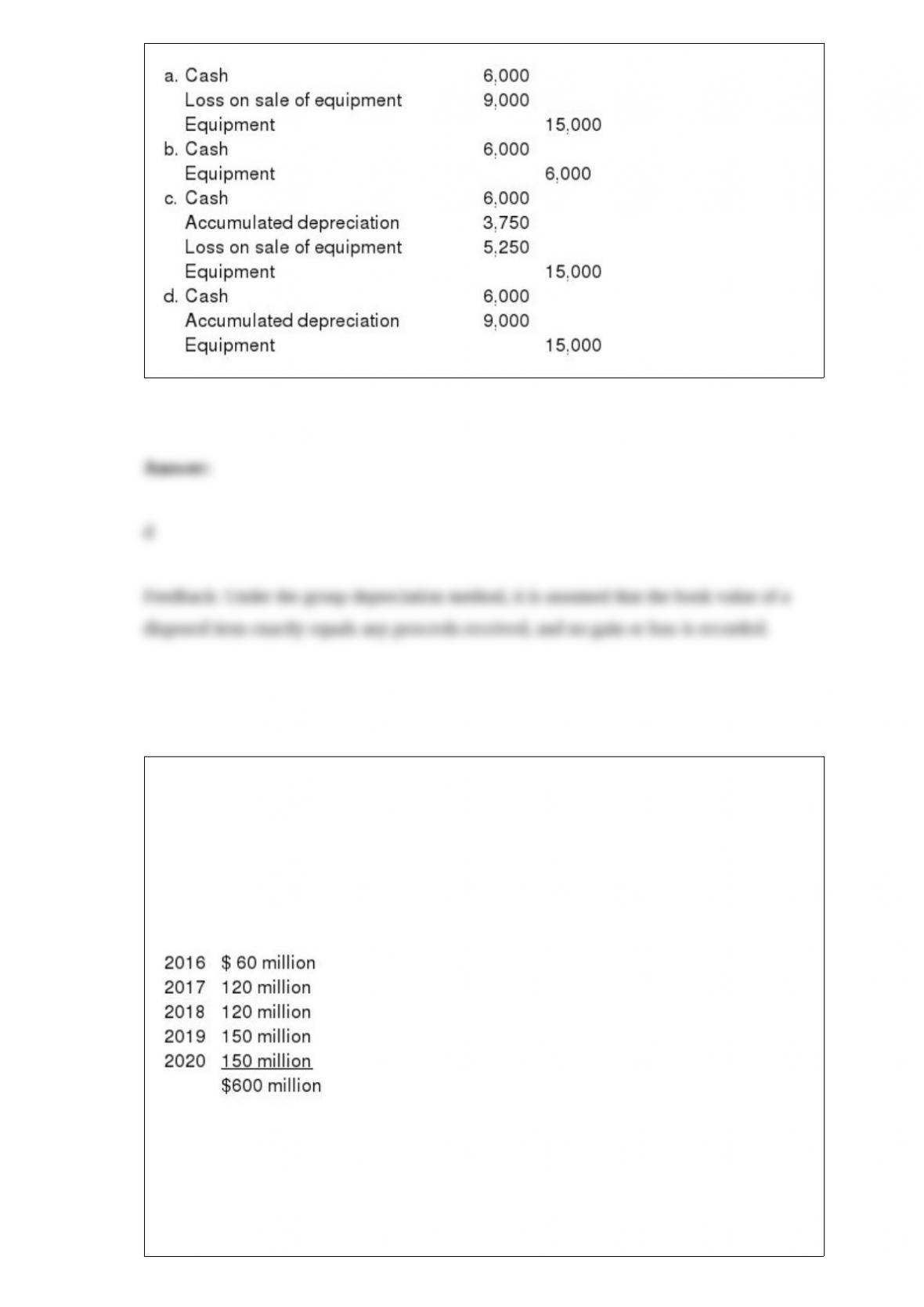

An asset acquired January 1, 2016, for $15,000 with an estimated 10-year life and no

residual value is being depreciated in an equipment group asset account that has an

average service life of eight years. The asset is sold on December 31, 2017, for $6,000.

The entry to record the sale would be:

Isaac Inc. began operations in January 2016. For certain of its property sales, Isaac

recognizes income in the period of sale for financial reporting purposes. However, for

income tax purposes, Isaac recognizes income when it collects cash from the buyer’s

installment payments.

In 2016, Isaac had $600 million in sales of this type. Scheduled collections for these

sales are as follows:

Assume that Isaac has a 30% income tax rate and that there were no other differences in

income for financial statement and tax purposes.

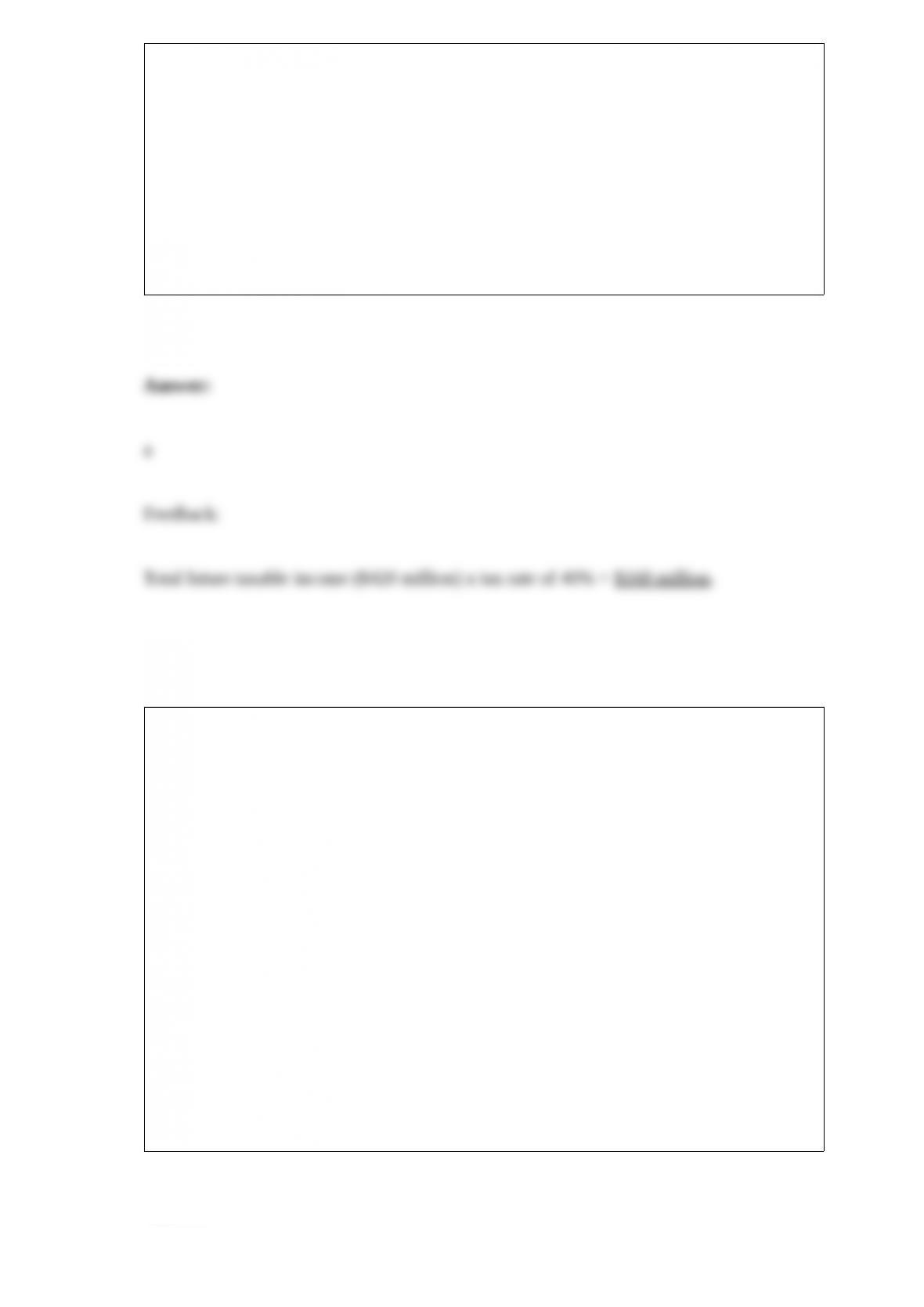

Suppose that, in 2017, legislation revised the income tax rates so that Isaac would be

taxed in 2018 and beyond at 40%, rather than 30%. Assume that there were no other

differences in income for financial statement and tax purposes. Ignoring operating

expenses and additional sales in 2017, what deferred tax liability would Isaac report in

its year-end 2017 balance sheet?

a. $168 million

b. $144 million

c. $126 million

d. $240 million.

Consider the following three scenarios:

I. ABC Lawncare performed lawn maintenance services for Drake Inc. on June 1st, and

received payment of $500 for those services.

II. On June 1st, Melly Corp received payment for 100 pounds of raw material to be

delivered to Drake Inc. in 6 months

III. Lodo, LLC collected cash on June 1st for services rendered on May 1st. Given these

scenarios, revenue can not be recognized on June 1st for

a. I, II

b. I only

c. II, III only

d. III only

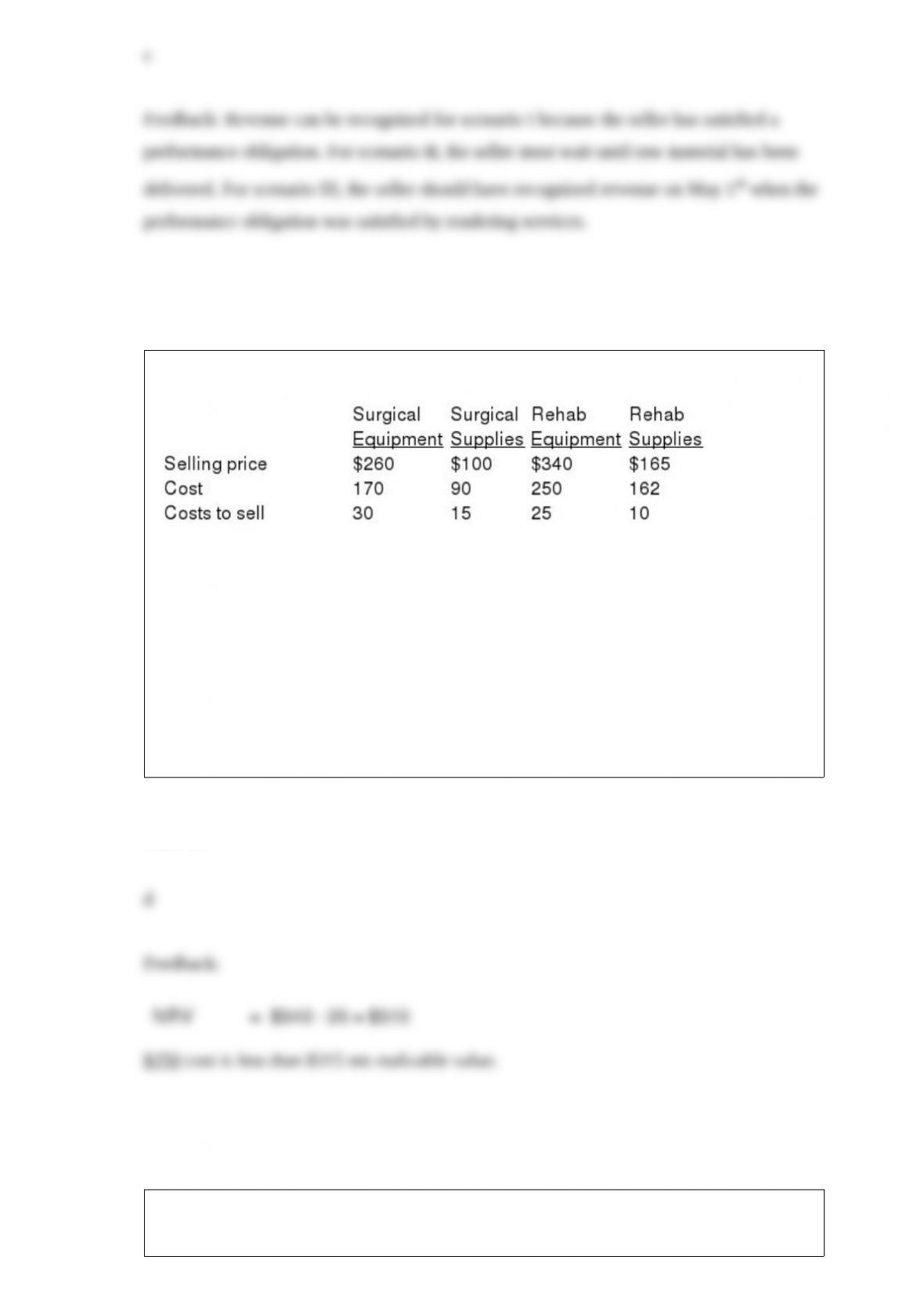

Data related to the inventories of Costco Medical Supply are presented below:

In applying the lower of cost and net realizable value rule, the inventory of rehab

equipment would be valued at:

a. $315.

b. $340.

c. $225.

d. $250.

When bonds are sold at a premium, if the annual straight-line amortization amount is

compared to the annual effective interest amortization amount over the life of the bond

issue, the annual amount of the straight-line amortization of premium is:

a. Higher than the effective interest amount in the early years and less than the effective

interest amount in the later years.

b. Less than the effective interest amount in the early years and more than the effective

interest amount in the later years.

c. Higher than the effective interest amount every year.

d. Less than the effective interest amount every year.

At January 1, 2016, BB Industries, Inc., owed Second Bank $24 million, under a 10%

note due December 31, 2017. Interest was paid last on December 31, 2014. BB was

experiencing severe financial difficulties and asked Second Bank to modify the terms of

the debt agreement. After negotiation Second Bank agreed to:

– Forgive the interest accrued for the year just ended,

– Reduce the remaining two years’ interest payments to $2 million each and delay the

first payment until December 31, 2017, and

– Reduce the principal amount to $22 million. Required:

Prepare the journal entries by BB Industries, Inc. necessitated by the restructuring of the

debt at (A) January 1, 2016, (B) December 31, 2017, and (C) December 31, 2018.

Which of the following is not a financing ratio?

a. Times interest earned ratio.

b. Debt to equity ratio.

c. Current ratio.

d. Return on shareholders’ equity.

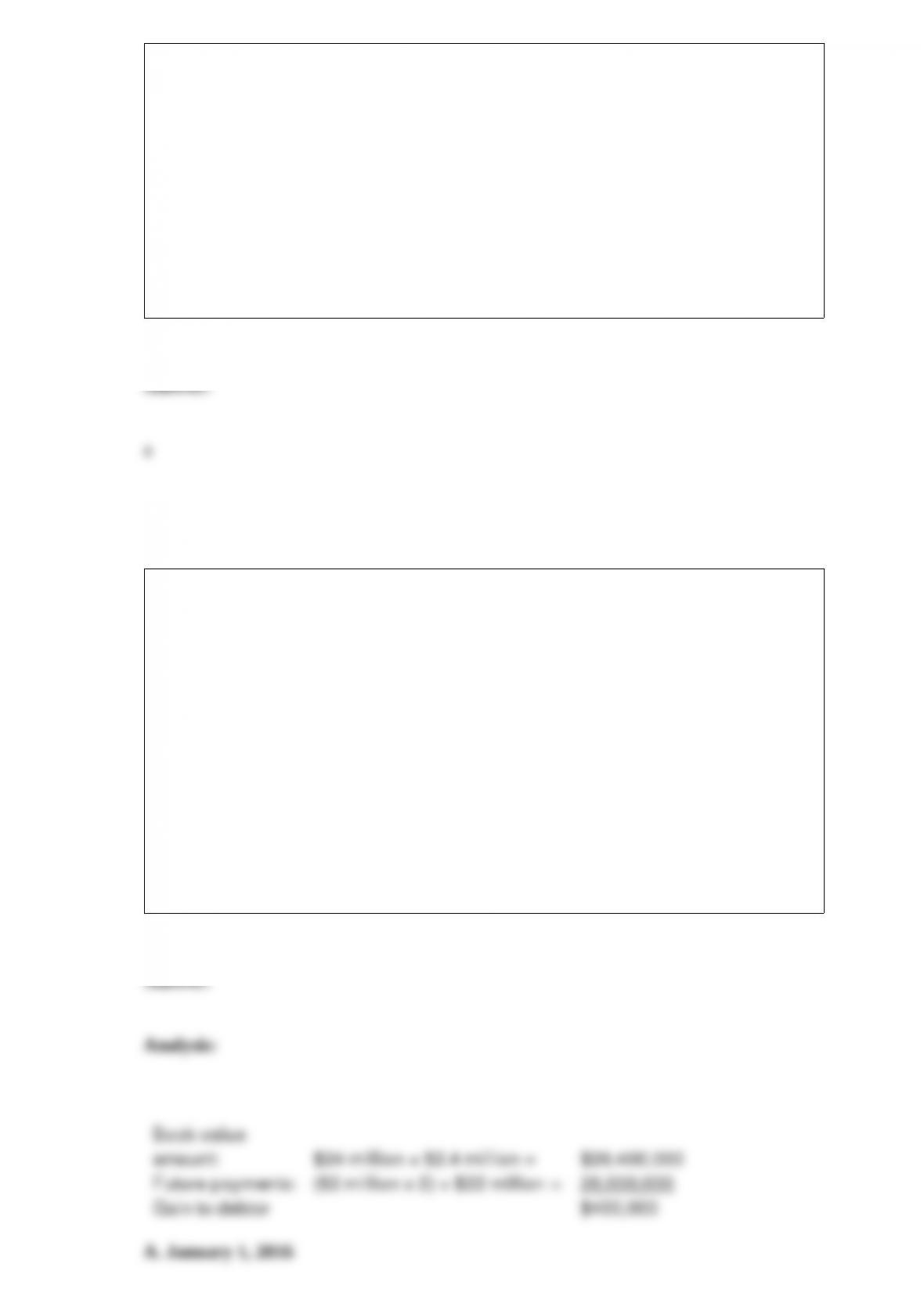

Data below for the year ended December 31, 2016, relates to Houdini Inc. Houdini

started business January 1, 2016, and uses the LIFO retail method to estimate ending

inventory.

Current period cost-to-retail percentage is:

a. 70.0%.

b. 68.7%.

c. 63.6%.

d. 63.5%.

On January 1, 2016, Hoosier Company purchased $930,000 of 10% bonds at face value.

The bond market value was $980,000 on December 31, 2016.

Required:

Prepare the appropriate journal entry on December 31, 2016, to properly value the

bonds assuming the bonds are classified as:

1> Trading securities.

2> Securities available for sale.

3> Held-to-maturity securities.

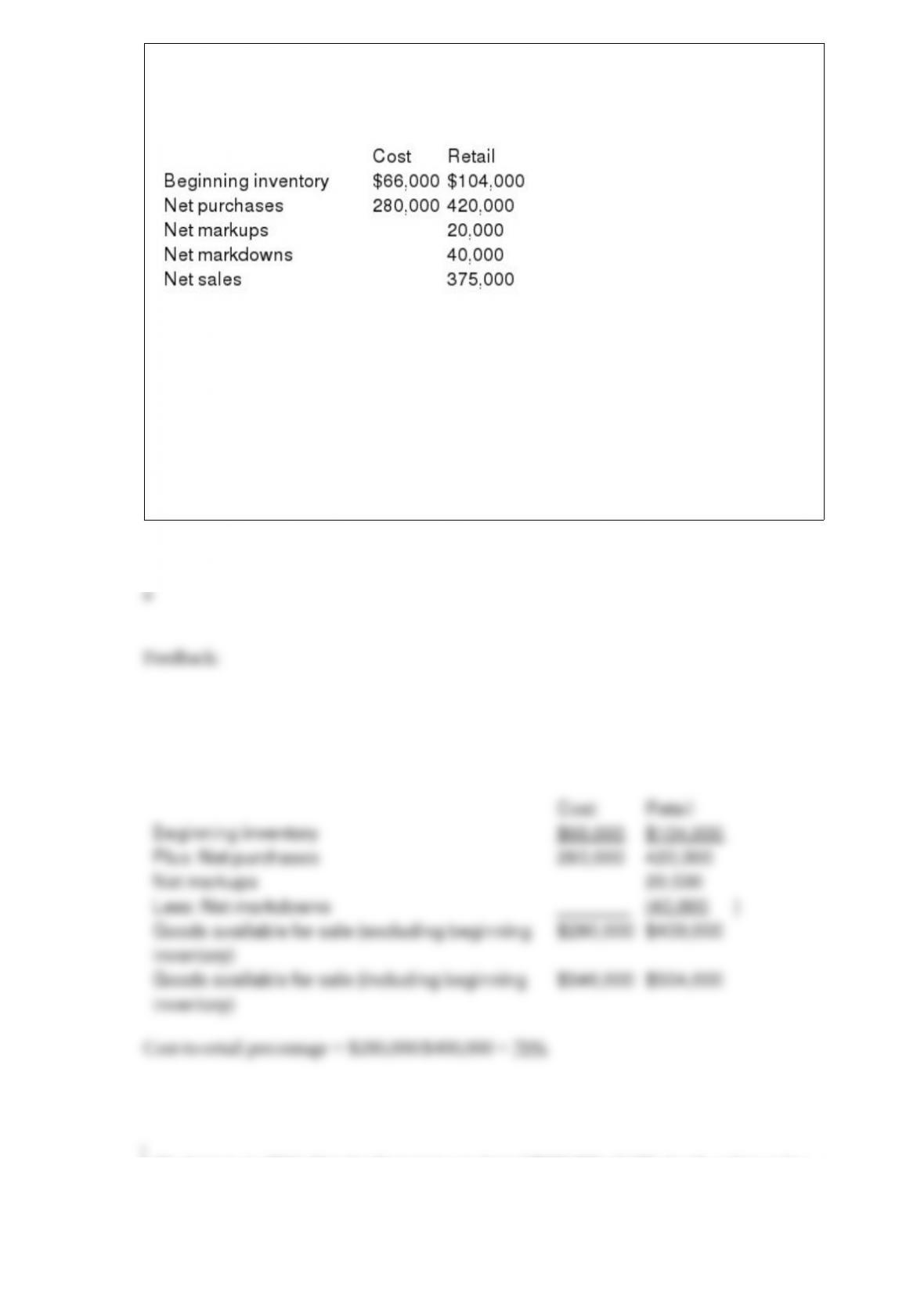

Jackson Company engaged in the following investment transactions during the current

year.

Required:

Prepare the appropriate journal entries to record the transactions for the year including

year-end adjustments. Show calculations.

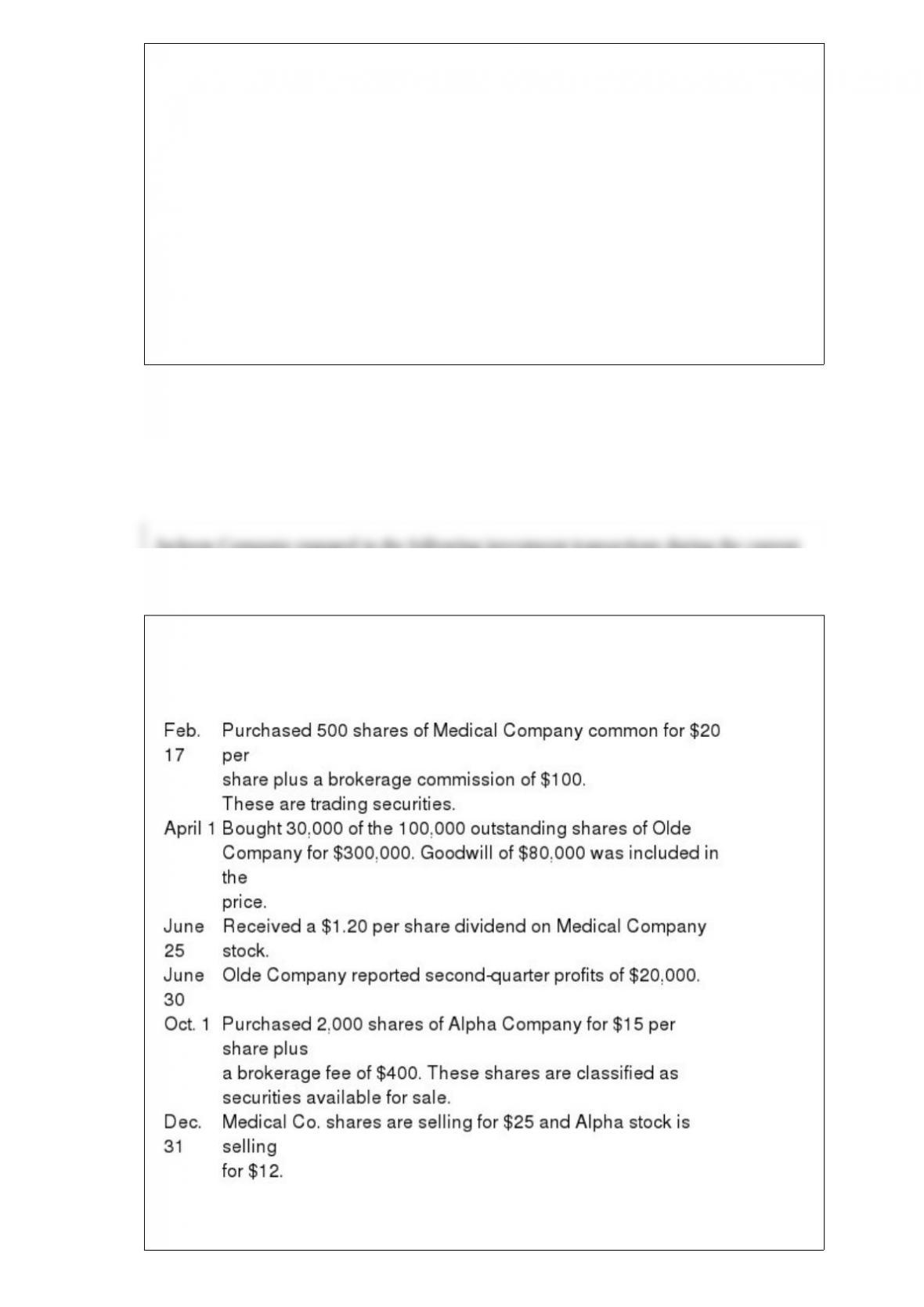

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Prepaid rent

Green Co. constructed a machine at a total cost of $70 million. Construction was

completed at the end of 2012 and the machine was placed in service at the beginning of

2013. The machine was being depreciated over a 10-year life using the

sum-of-the-years’-digits method. The residual value is expected to be $4 million. At the

beginning of 2016, Green decided to change to the straight-line method.

Required:

1) Ignoring income taxes, what journal entry(s) should Green record relating to the

machine for 2016?

2) Suppose Green has been using the straight-line method and switches to the

sum-of-the-years’-digits method. Ignoring income taxes, what journal entry(s) should

Green record relating to the machine for 2016?

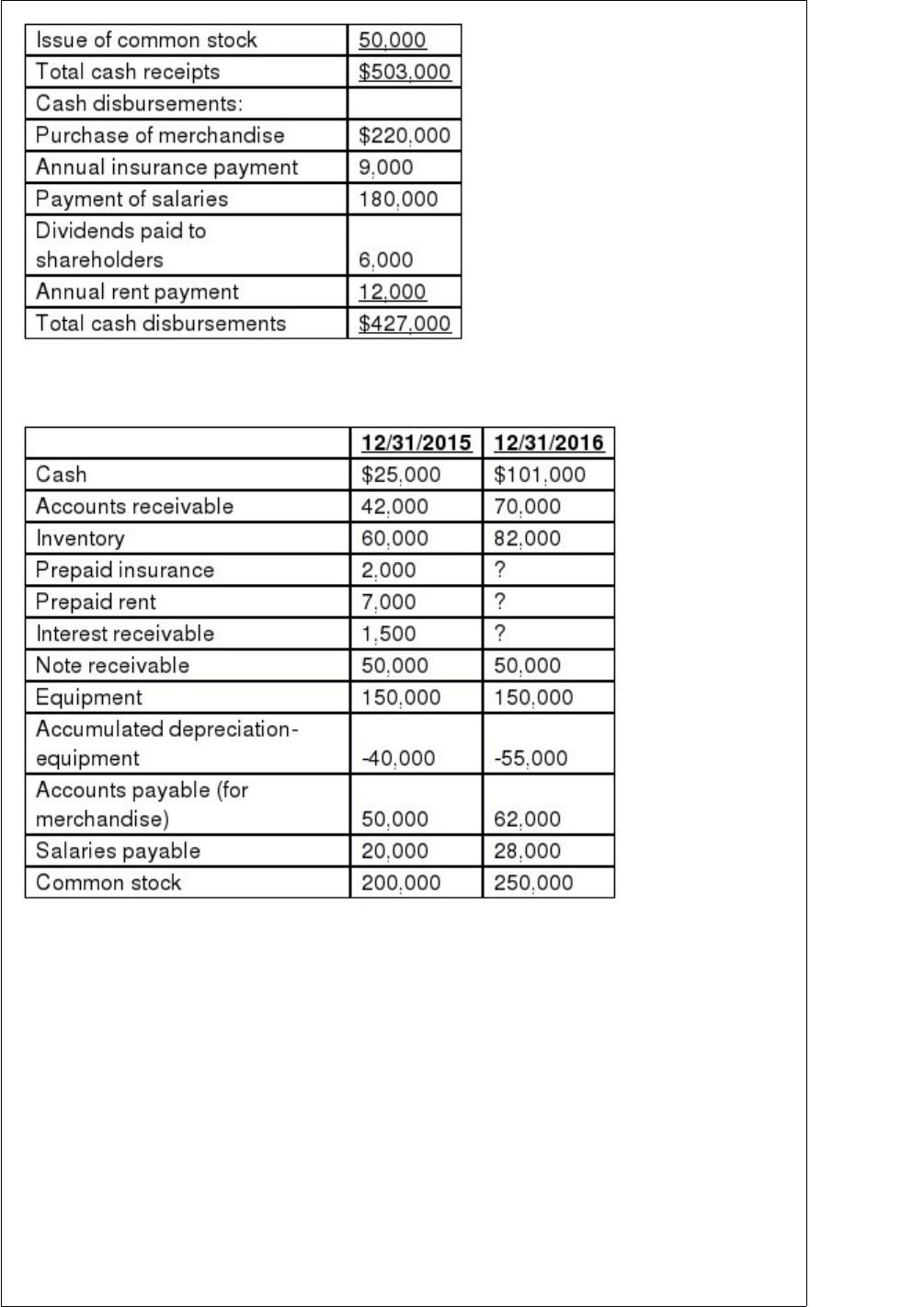

Raintree Corporation maintains its records on a cash basis. At the end of each year the

company’s accountant obtains the necessary information to prepare accrual basis

financial statements. The following cash flows occurred during the year ended

December 31, 2016:

Selected balance sheet information:

Additional information:

1> On June 30, 2015, Raintree lent a customer $50,000. Interest at 6% is payable

annually on each June 30. Principal is due in 2019.

2> The annual insurance payment is made in advance on March 31.

3> Annual rent on the company’s facilities is paid in advance on September 30.

Required:

1> Prepare an accrual basis income statement for 2016 (ignore income taxes).

2> Determine the following balance sheet amounts on December 31, 2016:

•

Interest receivable

•

•

Prepaid insurance

•

•

Prepaid rent

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term.

On November 1, 2016, Ziegler Products issued a $200,000, 9-month,

noninterest-bearing note to the bank. Interest was discounted at a 12% discount rate.

Required:

1> Prepare the appropriate journal entry by Ziegler to record the issuance of the note.

2> Determine the effective interest rate.

3> Suppose the note had been structured as a 12% note with interest and principal

payable at maturity. Prepare the appropriate journal entry to record the issuance of the

note by Ziegler.

4> Prepare the appropriate journal entry on December 31, 2016, to accrue interest

expense on the note described in number 3 for the 2016 financial statements.

Indicate (by number) the way each of the items listed below should be reported in a

balance sheet at December 31, 2016. Match each phrase with the number of the term for

the accounting treatment.

Branch Industries changes from declining balance depreciation to straight-line

depreciation for existing assets. Describe in detail the way Branch would account for

the change and include reasons for the accounting.

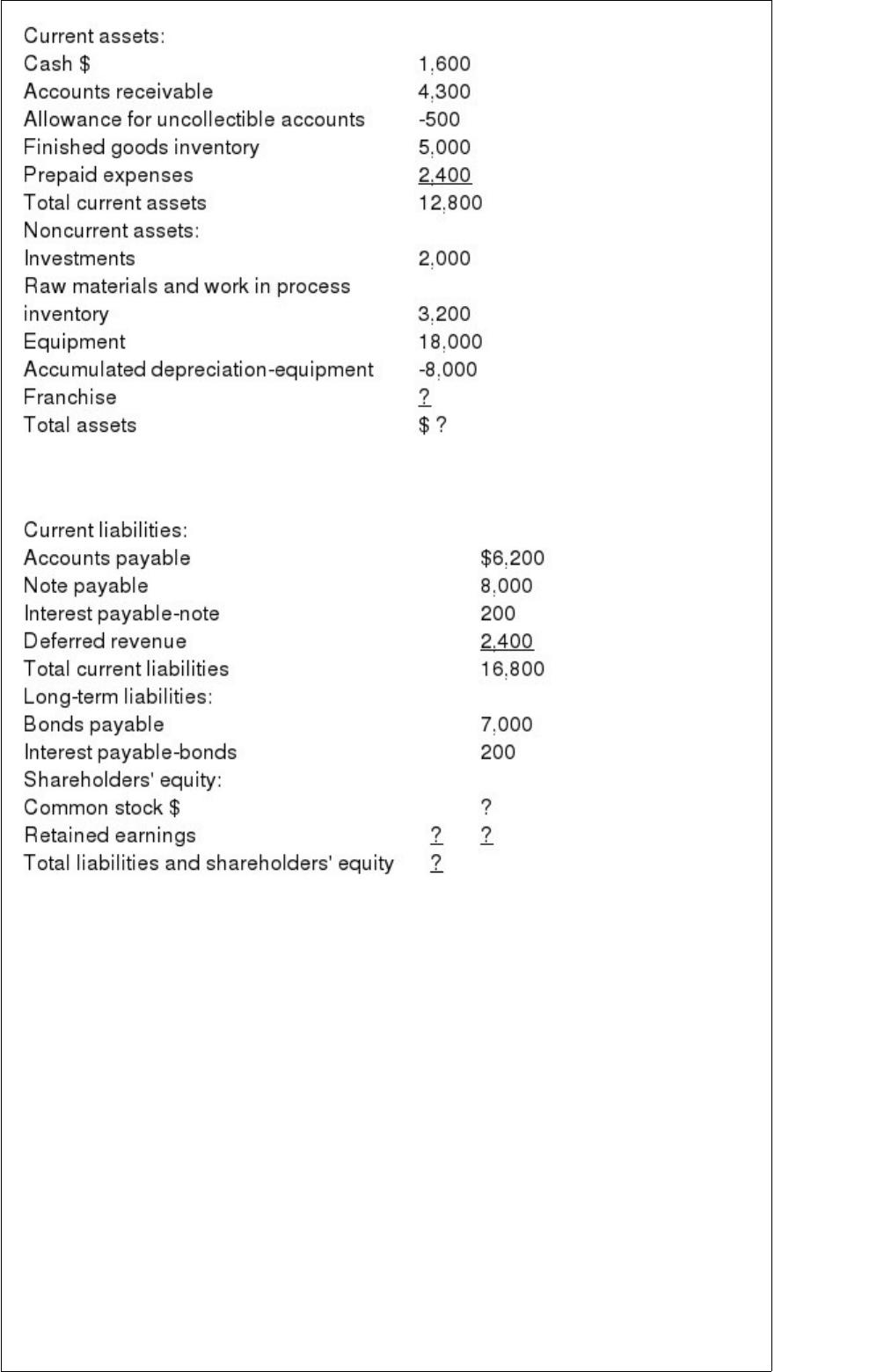

As controller for Henderson, you are attempting to reconstruct and revise the following

balance sheet prepared by a staff accountant. Henderson Manufacturing Company

Balance Sheet

At December 31, 2016

($ in 000s) Assets

Liabilities and Shareholders’ Equity

Additional information ($ in 000s):

1> Certain records that included the account balances for the franchise and

shareholders’ equity items were lost. However, a complete, preliminary balance sheet

prepared before the records were lost showed a debt to equity ratio of 1.5. That is, total

liabilities are 150% of total shareholders’ equity. Retained earnings at the beginning of

the year was $4,300. Net income for 2016 was $2,500, and $800 in cash dividends were

declared and paid to shareholders.

2> The investments represent treasury bills purchased in December 2016 that mature in

January 2017. These are considered cash equivalents.

3> Interest on both the note and the bonds is payable annually.

4> The note payable is due in annual installments of $800 each.

5> Deferred revenue will be earned equally over the next 18 months.

6> The common stock represents 500,000 shares of no par stock authorized, 300,000

shares issued and outstanding. Required:

Prepare a complete, corrected, classified balance sheet.