A debit balance in the labor-efficiency variance account indicates that

A. standard hours exceed actual hours.

B. actual hours exceed standard hours.

C. standard rate and standard hours exceed actual rate and actual hours.

D. actual rate and actual hours exceed standard rate and standard hours.

Answer:

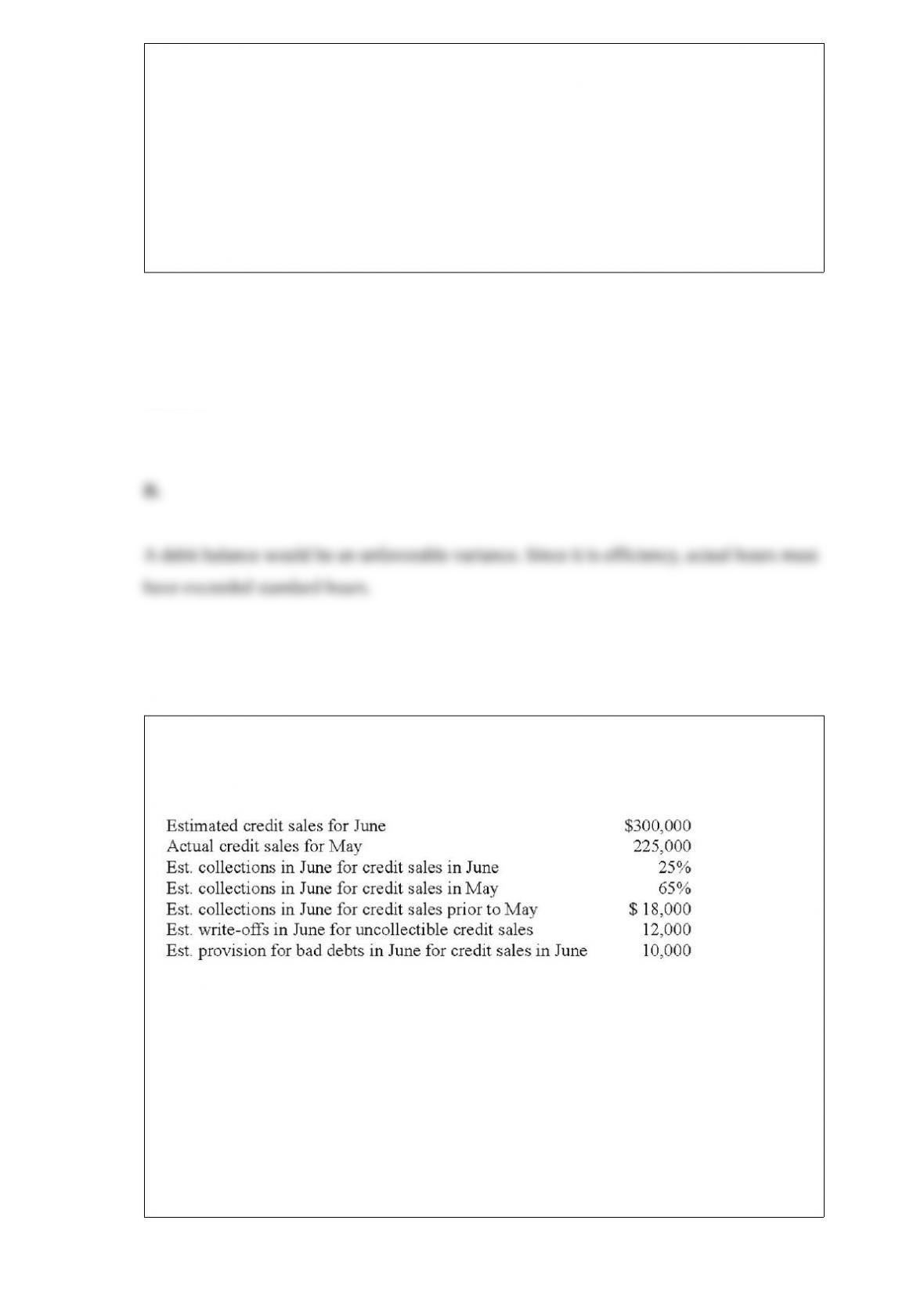

The Smart Company is preparing its cash budget for the month of June. The following

information is available concerning its accounts receivable:

What are the estimated cash receipts from accounts receivable collections in June?

A. $221,250.

B. $227,250.

C. $229,250.

D. $239,250.

Answer:

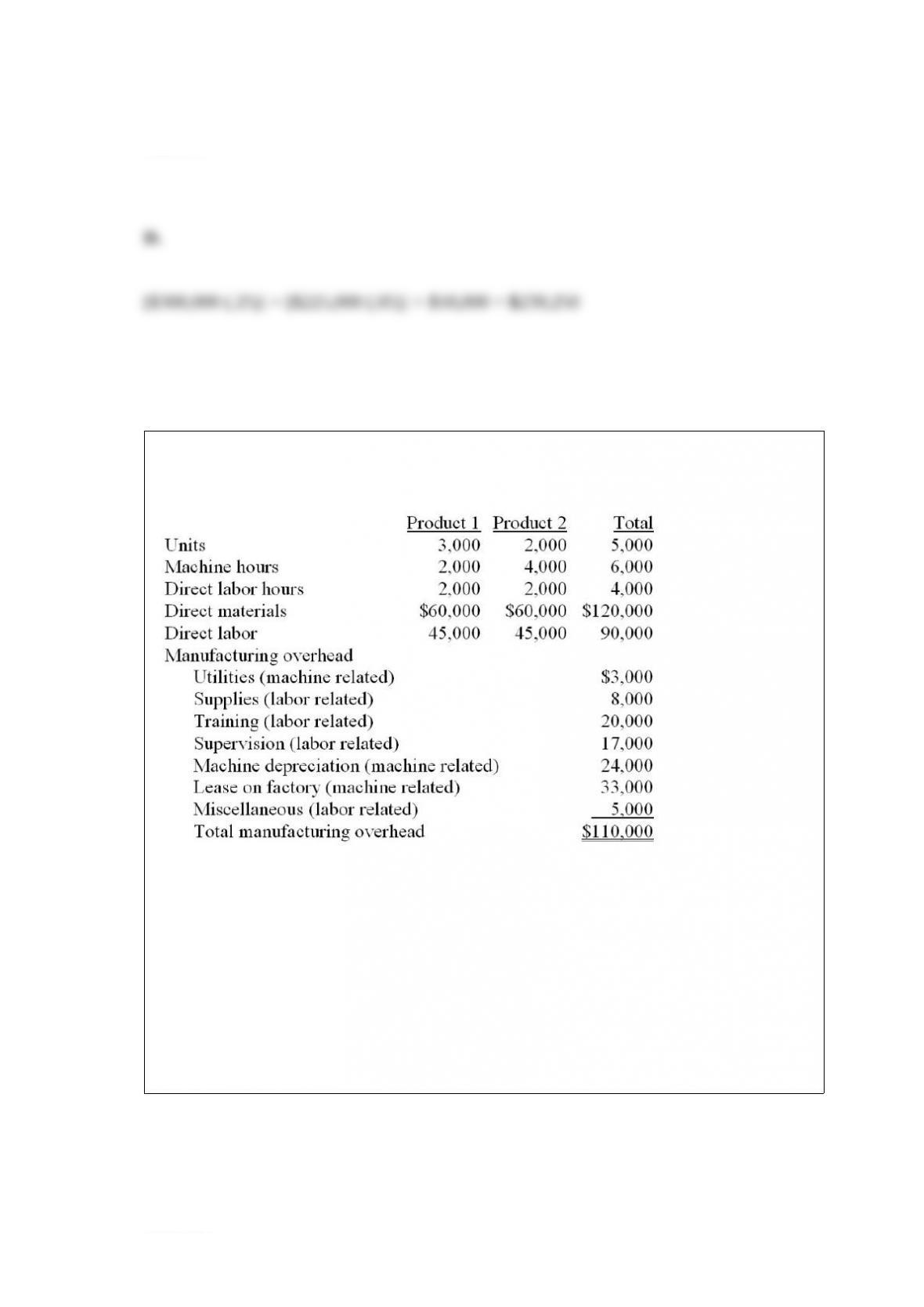

Target Products uses a two-stage allocation method to assign costs to its products. The

following information has been provided for March:

Required:

(a) Allocate the manufacturing overhead to two cost pools: machine-related and

labor-related

(b) Compute the predetermined overhead rate for the two pools, using machine hours

and direct labor hours as the bases.

(c) Compute the total costs of production for each of the two products.

Answer:

Flowers and Flowers, Inc., has two divisions. Division A has an investment base of

$750,000 and produces (and sells) 100,000 units of Eyne at a market price of $10.00

per unit. Variable costs total $3.50 per unit, and fixed charges are $4.00 per unit (based

on a capacity of 120,000 units). Division B wants to purchase 25,000 units of Eyne

from Division A. However, Division B is only willing to pay $6.75 per unit.

What is the contribution margin for Division A without the transfer to Division B?

A. $250,000

B. $650,000

C. $675,000

D. $1,000,000

Answer:

Acme Sales has two store locations. Store A has fixed costs of $125,000 per month and

a variable cost ratio of 60%. Store B has fixed costs of $200,000 per month and a

variable cost ratio of 30%. What is the break-even sales volume for Store B?

A. $666,667

B. $325,000

C. $285,714

D. Cannot determine with the information given.

Answer:

Which of the following approaches allocates overhead by multiplying a predetermined

rate xstandard activity?

A. Actual costing

B. Normal costing

C. Regression costing

D. Standard costing

Answer:

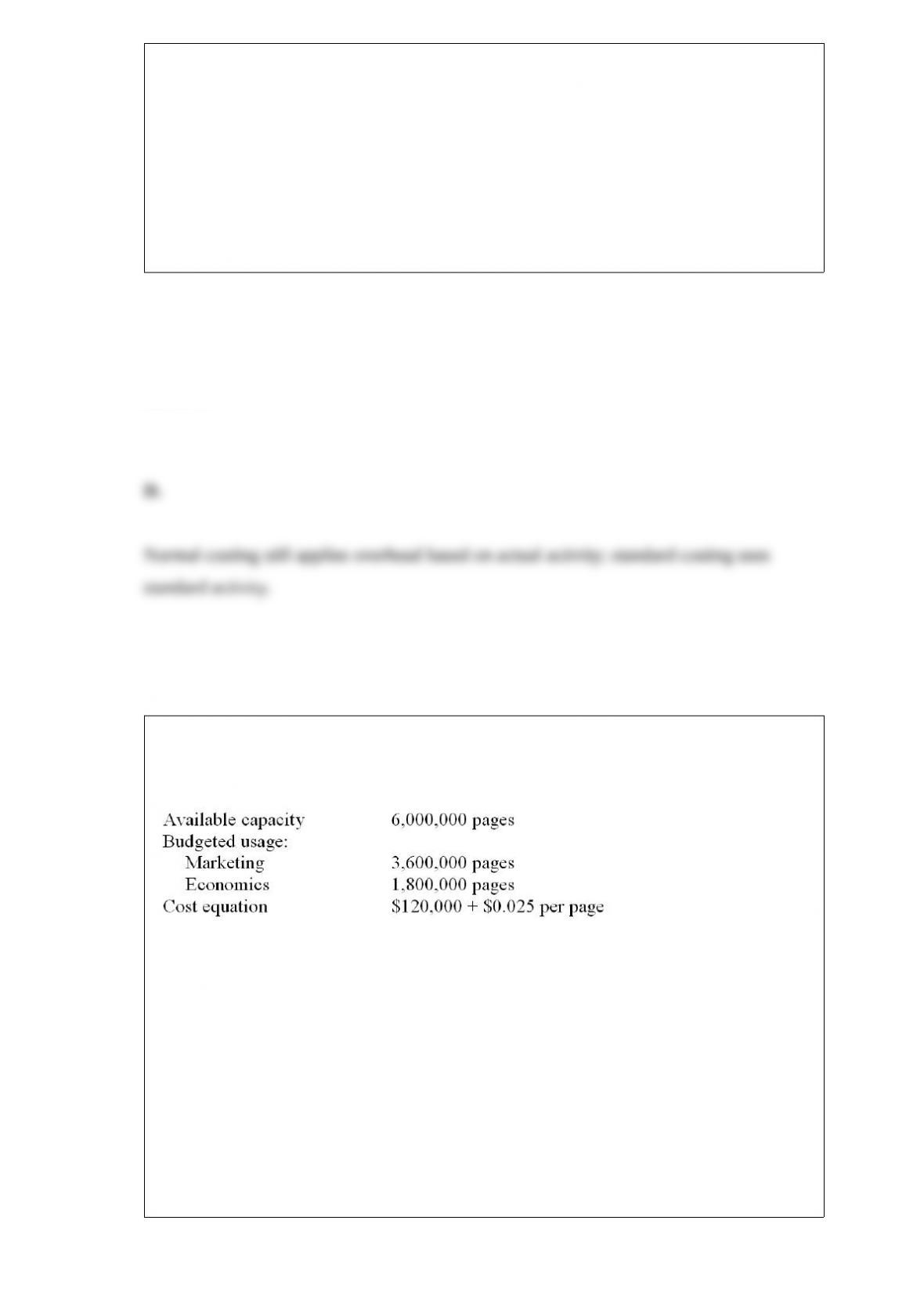

The Copy Department in the College of Business at State University provides

photocopying service for both the Marketing and Economics Department. The

following budget has been prepared for the year.

If the Copy Department uses a dual-rate for allocating its costs, how much cost will be

allocated to the Marketing Department, assuming the Marketing Department actually

made 3,000,000 copies during the year?

A. $135,000

B. $150,000

C. $155,000

D. $170,000

Answer:

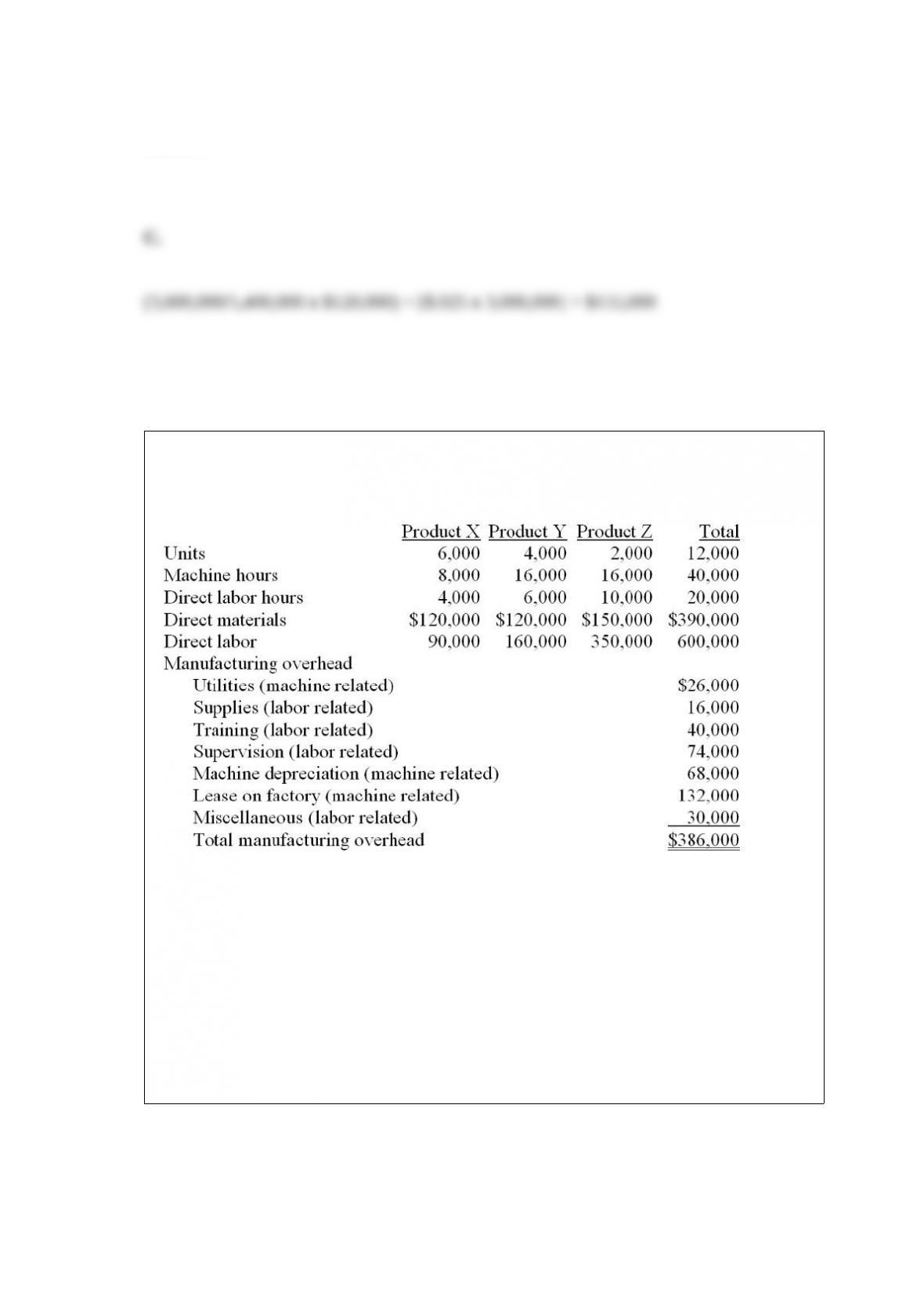

Acme Industries uses a two-stage allocation method to assign costs to its products. The

following information has been provided for the month:

Required:

(a) Allocate the manufacturing overhead to two cost pools: machine-related and

labor-related

(b) Compute the predetermined overhead rate for the two pools, using machine hours

and direct labor cost as the bases.

(c) Compute the unit cost of production for each of the three products.

Answer:

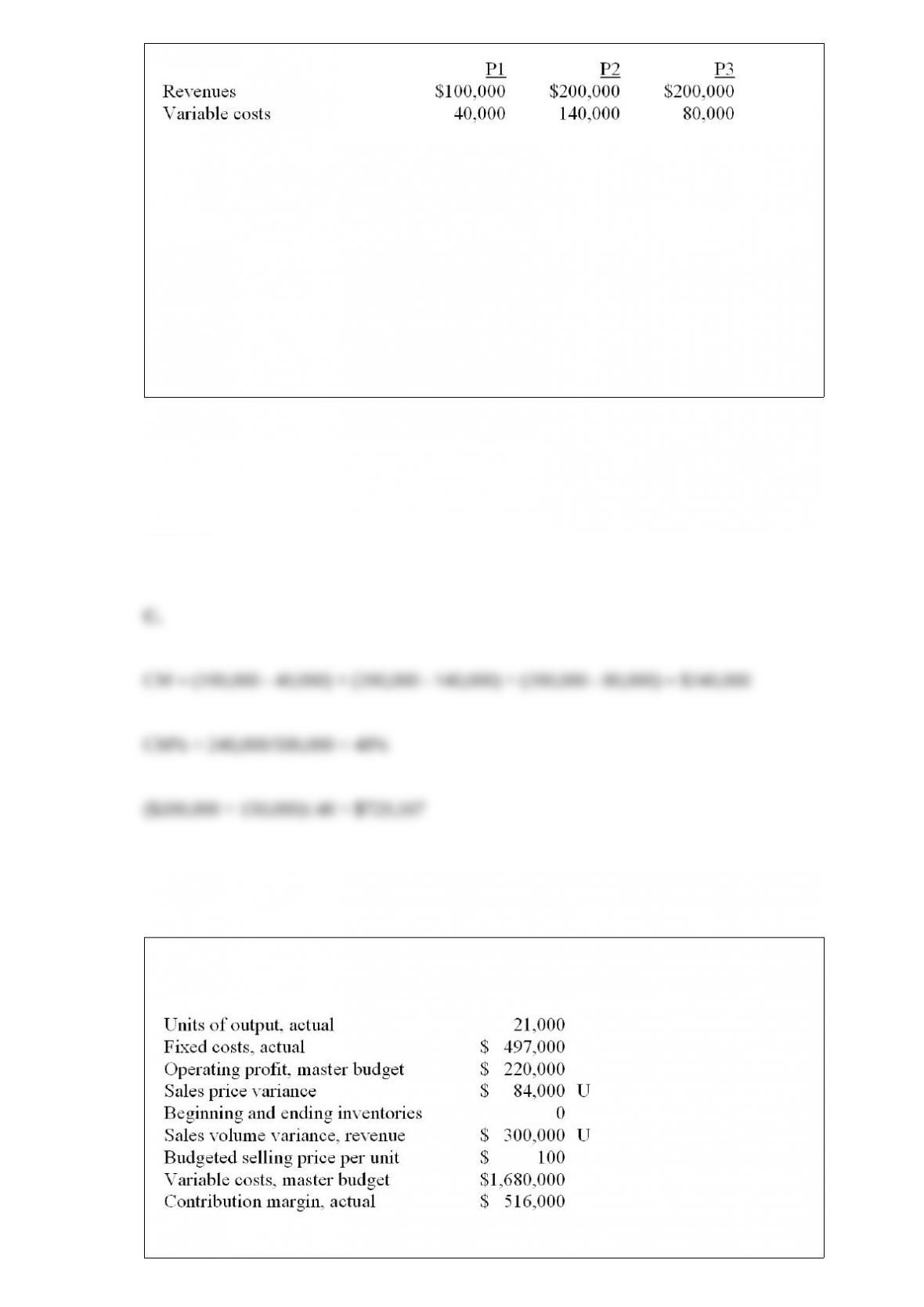

Kanmore produces and sells three products. Last month’s results are as follows:

Fixed costs total $200,000. What sales volume would generate an operating profit of

$150,000? (Assume the current prodcut mix)

A. $650,000

B. $610,000

C. $729,167

D. $850,000

Answer:

The Kessler Company has the following information pertaining to the month of March:

Required:

Prepare a performance report for March including columns for the (a) actual results, (b)

flexible budget, (c) flexible budget variance, (d) master budget, and (e) sales activity

variance.

Answer:

In general, if a potential transfer has no effect on divisional profits,

A. no transfer will take place between the divisions.

B. managers will be indifferent between making the transfer or not.

C. the organization should not intervene to force a transfer.

D. the optimal transfer price is the opportunity cost for the buying division.

Answer:

The practice of setting price below cost with the intent to drive competitors out of

business:

A. predatory pricing

B. target pricing

C. target costing

D. peak-load pricing

Answer:

Which of the following organizational policies is most likely to result in undesirable

managerial behavior? (CMA adapted)

A. Patel Chemicals sponsors television coverage of cricket matches between national

teams representing India and Pakistan. The expenses of such media sponsorship are not

allocated to its various divisions.

B. Joe Walk, the chief executive officer of Eagle Rock Brewery, wrote a memorandum

to his executives stating, “Operating plans are contracts and they should be met without

fail.”

C. The budgeting process at Madsen Manufacturing starts with operating managers

providing goals for their respective departments.

D. Fullbright Lighting holds quarterly meetings of departmental managers to consider

possible changes in the budgeted targets due to changing conditions.

E. At Fargo Transportation, managers are expected to provide explanations for

variances from the budget in their departments.

Answer:

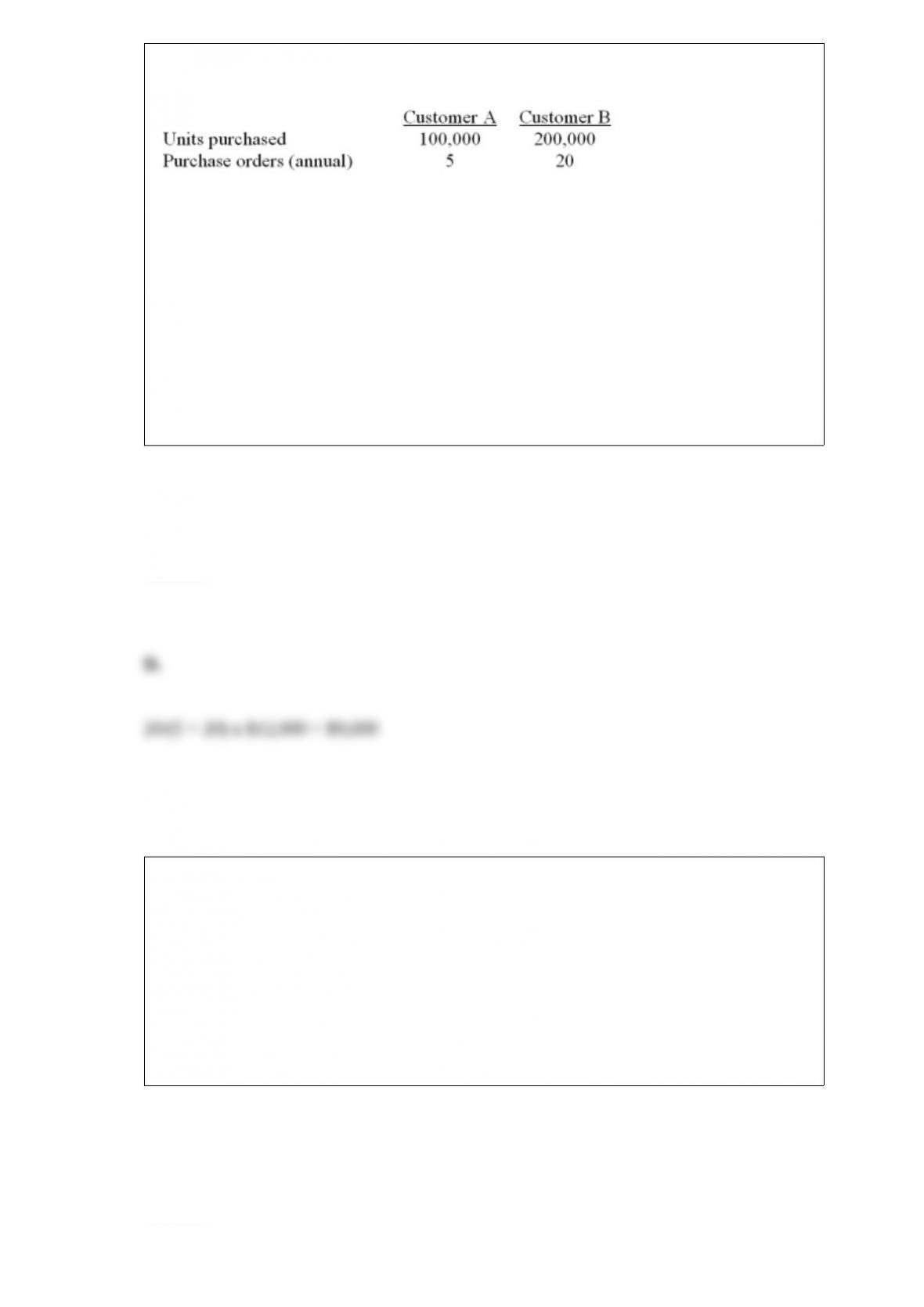

Beta Company is preparing its annual profit plan. As part of its analysis of the

profitability of its customers, management estimates that the $12,000 for sales support

should be assigned to the individual customers from the information given as follows:

What is the amount of the sales support costs that should be allocated to Customer B

assuming Beta uses purchases orders to compute activity-based costs?

A. $2,400

B. $4,000

C. $8,000

D. $9,600

Answer:

Budgetary slack can best be defined as

A. underestimation of budgeted expenses.

B. underestimation of budgeted revenues.

C. overestimation of long-term assets.

D. overestimation of current liabilities.

Answer:

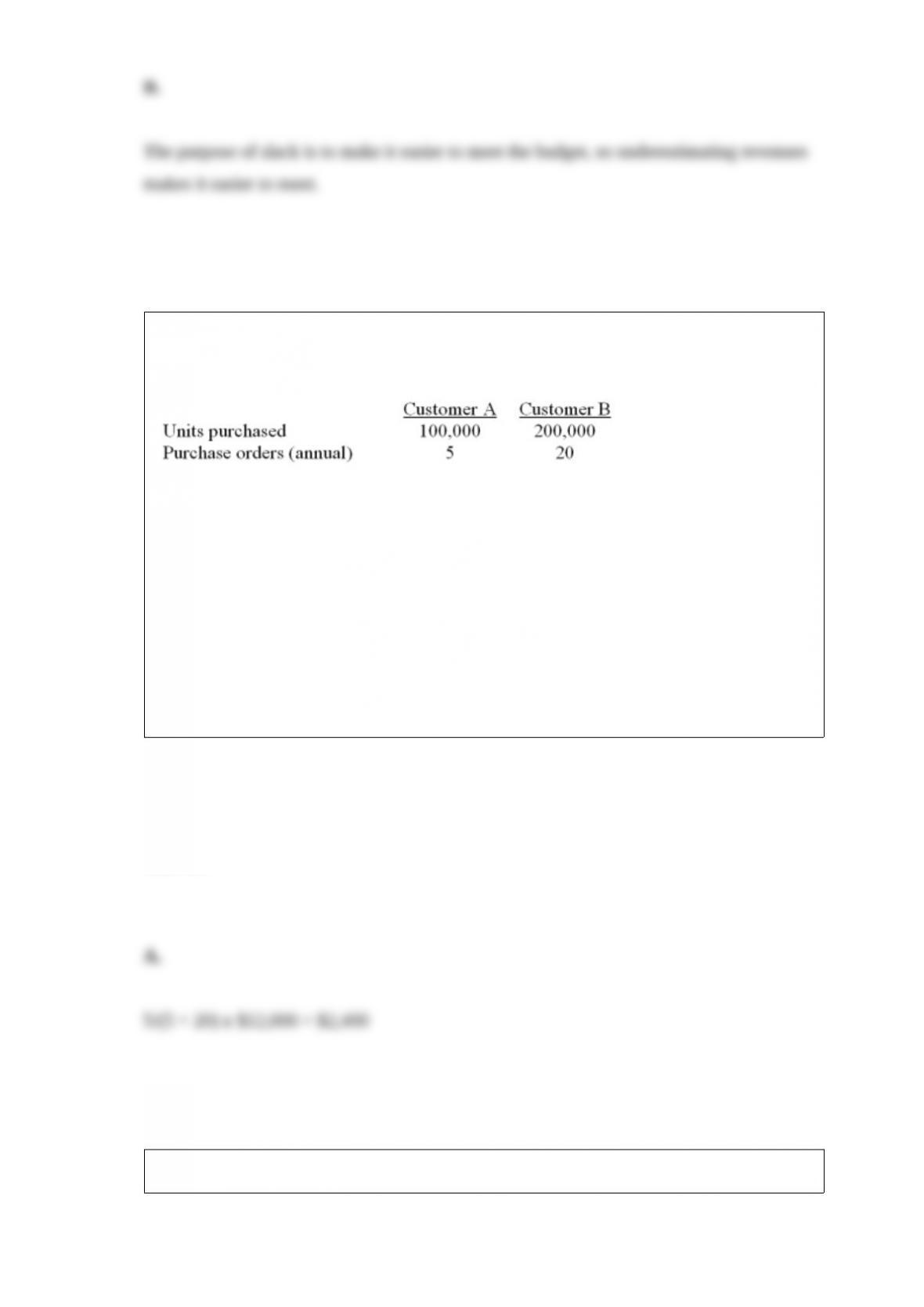

Beta Company is preparing its annual profit plan. As part of its analysis of the

profitability of its customers, management estimates that the $12,000 for sales support

should be assigned to the individual customers from the information given as follows:

What is the amount of the sales support costs that should be allocated to Customer A

assuming Beta uses purchases orders to compute activity-based costs?

A. $2,400

B. $4,000

C. $8,000

D. $9,600

Answer:

Dickey Company had total underapplied overhead of $15,000. Additional information

is as follows:

What is the actual total overhead for the period?

A. $50,000

B. $45,000

C. $80,000

D. $87,000

Answer:

Manufacturing cycle efficiency is computed by dividing process time by

A. moving time + storage time.

B. storage time + inspection time.

C. moving time + storage time + inspection time.

D. process time + inspection time + moving time.

E. process time + moving time + storage time + inspection time.

Answer:

Chipper Division of Acme Corp. sells 80,000 units of part Z-25 to the outside market.

Part Z-25 sells for $40, has a variable cost of $22, and a fixed cost per unit of $10.

Chipper has a capacity to produce 100,000 units per period. Jones Division currently

purchases 10,000 units of part Z-25 from Chipper for $40. Jones has been approached

by an outside supplier willing to supply the parts for $36. If Acme uses a negotiated

transfer pricing system, what is the maximum transfer price that should be charged for

this transaction?

A. $40

B. $36

C. $32

D. $22

Answer:

Which of the following costs are not considered in a differential analysis for a

make-or-buy decision?

A. Indirect materials and indirect labor if the item is manufactured internally

B. Direct materials and direct labor if the item is purchased

C. Variable overhead if the item is manufactured internally

D. Fixed overhead that can be avoided if the item is purchased

E. Fixed overhead that will continue if the item is purchased

Answer:

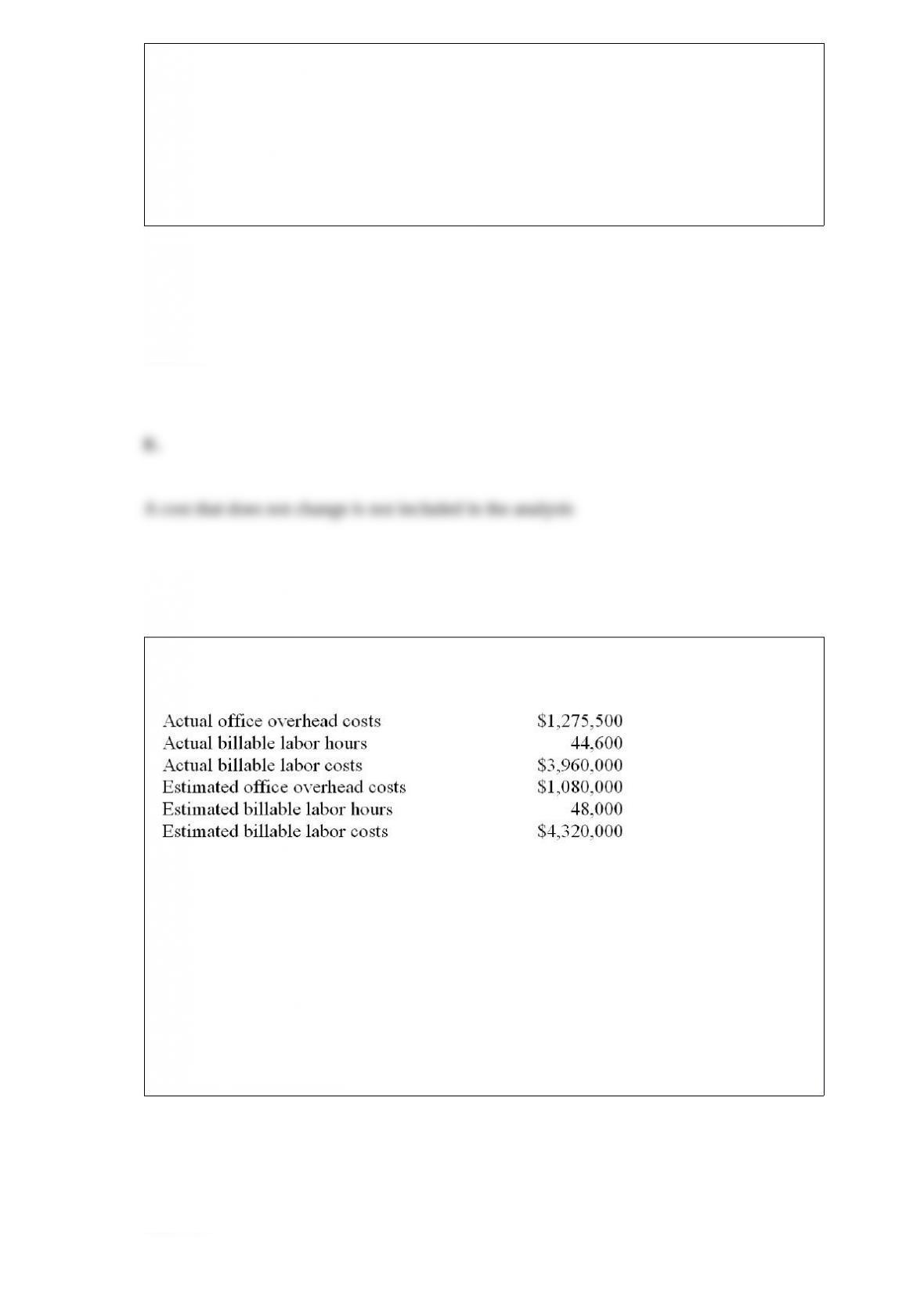

The following information has been gathered for Cheatham Law Offices for its fiscal

year ending December 31:

What is the predetermined office overhead rate per billable labor hour?

A. $28.60

B. $26.57

C. $22.50

D. $24.22

Answer:

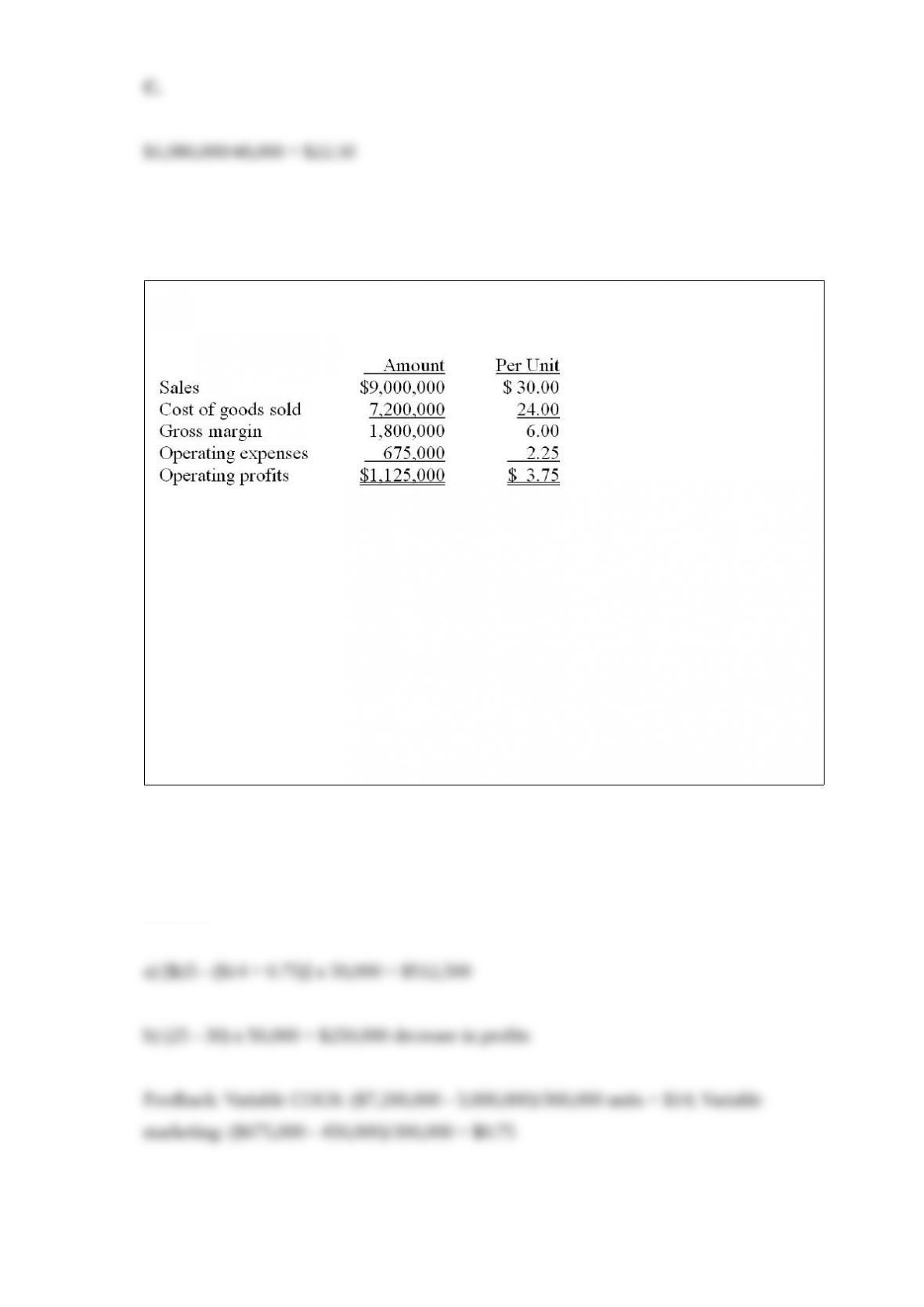

The following information relates to the Klessig Company for the upcoming year.

The cost of goods sold includes $3,000,000 of fixed manufacturing overhead; the

operating expenses include $450,000 of fixed marketing expenses. A special order

offering to buy 50,000 units for $25.00 per unit has been made to Klessig. Fortunately,

there will be no additional operating expenses associated with the order and Klessig has

sufficient capacity to handle the order.

Required:

a) How much will operating profits increase if Klessig accepts the special order?

b) Assume that Klessig is operating at full capacity. How much will operating profits

change if Klessig accepts the special order?

Answer:

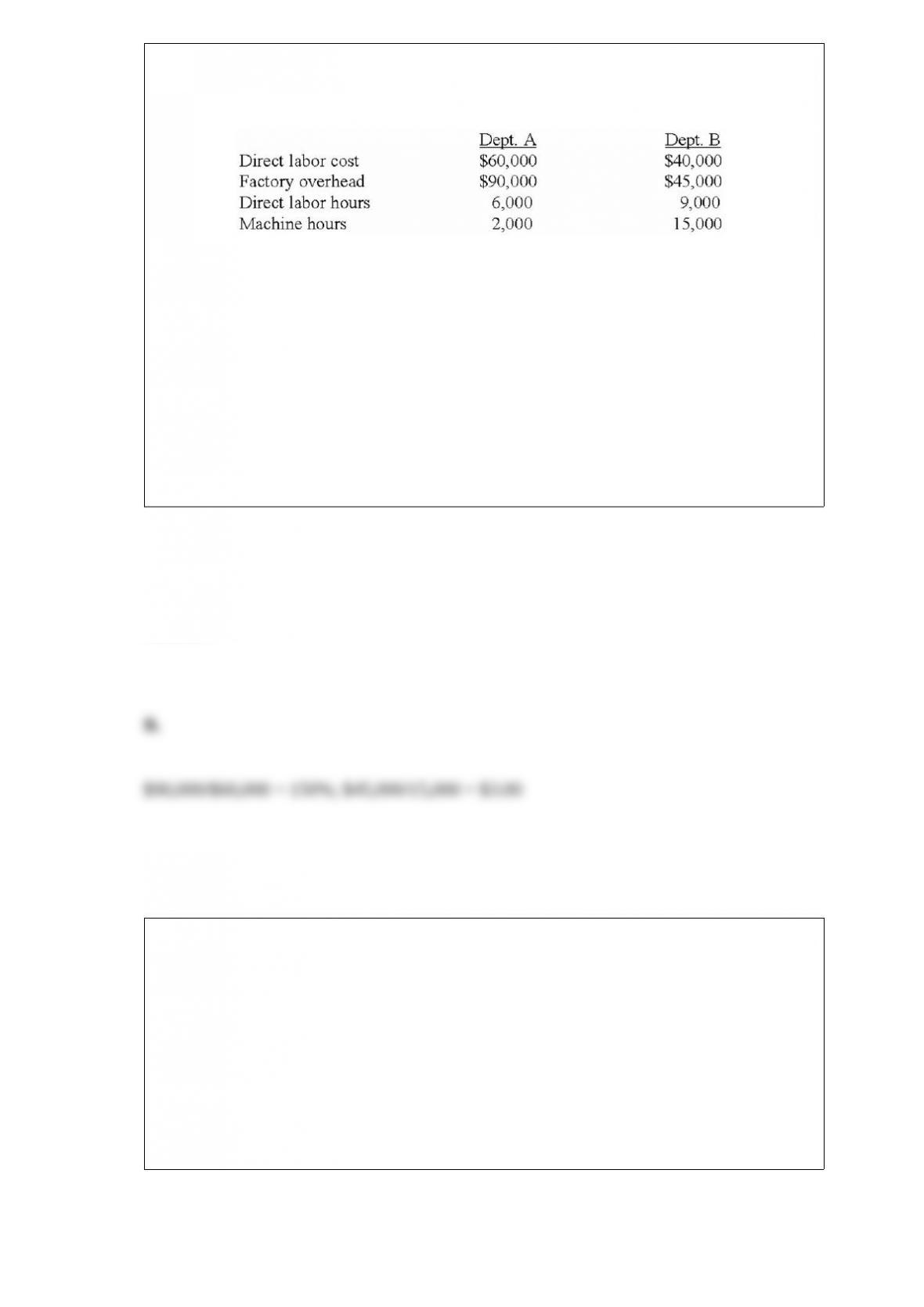

The Silver Company uses a predetermined overhead rate in applying overhead to

production orders on a labor cost basis in Department A and on a machine hours basis

in Department B. At the beginning of the year, the company made the following

estimates:

What predetermined overhead rate would be used in Department A and Department B

respectively?

A. 150% and 300%.

B. 150% and $3.00.

C. $1.50 and 300%.

D. $1.50 and $3.00.

Answer:

In general, a balanced scorecard is used to evaluate an organization’s performance

using

A. standard costs and variance analysis.

B. multiple financial and nonfinancial measures.

C. financial statements and ratio analysis.

D. the Board of Director’s audit committee.

Answer:

Which of the following is an example of a prevention cost?

A. Machine inspection

B. Warranty repairs

C. Field testing

D. Marketing costs

Answer:

Shawano Corporation applies overhead based upon machine-hours. Budgeted factory

overhead was $266,400 and budgeted machine-hours were 18,500. Actual factory

overhead was $287,920 and actual machine-hours were 19,050. Before disposition of

over- or underapplied overhead, the cost of goods sold was $560,000 and ending

inventories were as follows:

Required:

a) Compute the amount of overhead applied to production.

b) Prepare the journal entry to dispose of the over/under-applied overhead using the

write-off to cost of goods sold approach.

c) Prepare the journal entry to dispose of the over/under-applied overhead using the

proration approach.

Answer:

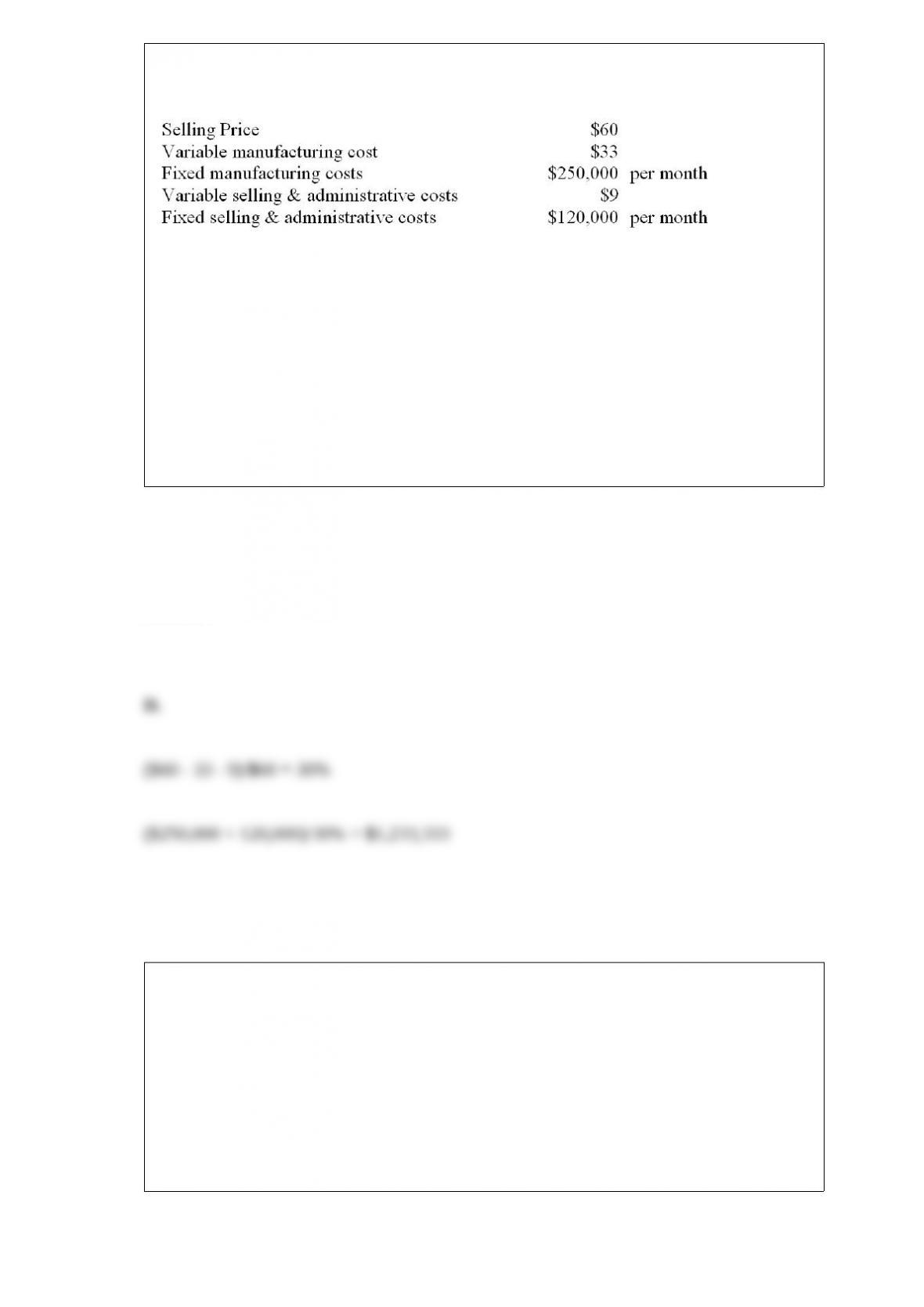

RedTail Mfg has the following data:

What dollar sales volume does RedTail need to break-even?

A. $822,222

B. $833,333

C. $900,000

D. $1,233,333

Answer:

Parkside Inc. has several divisions that operate as decentralized profit centers.

Parkside’s Entertainment Division manufactures video arcade equipment using the

products of two of Parkside’s other divisions. The Plastics Division manufactures

plastic components, one type that is made exclusively for the Entertainment Division,

while other less complex components are sold to outside markets. The products of the

Video Cards Division are sold in a competitive market; however, one video card model

is also used by the Entertainment Division. The actual costs per unit used by the

Entertainment Division are presented in the next column. (CMA adapted)

The Plastics Division sells its commercial products at full cost plus a 25% markup and

believes the proprietary plastic component made for the Entertainment Division would

sell for $6.25 per unit on the open market. The market price of the video card used by

the Entertainment Division is $10.98 per unit.

A per-unit transfer price from the Video Cards Division to the Entertainment Division at

full cost, $9.15, would

A. allow evaluation of both divisions on a competitive basis.

B. satisfy the Video Cards Division’s profit desire by allowing recovery of opportunity

costs.

C. provide no profit incentive for the Video Cards Division to control or reduce costs.

D. encourage the Entertainment Division to purchase video cards from an outside

source.

Answer:

Under which of the following conditions will the FIFO method produce the same cost

of goods manufactured as the weighted-average method?

A. There is no ending inventory.

B. There is no beginning inventory.

C. The beginning and ending inventories are equal.

D. The beginning and ending inventories are both 50% complete.

Answer:

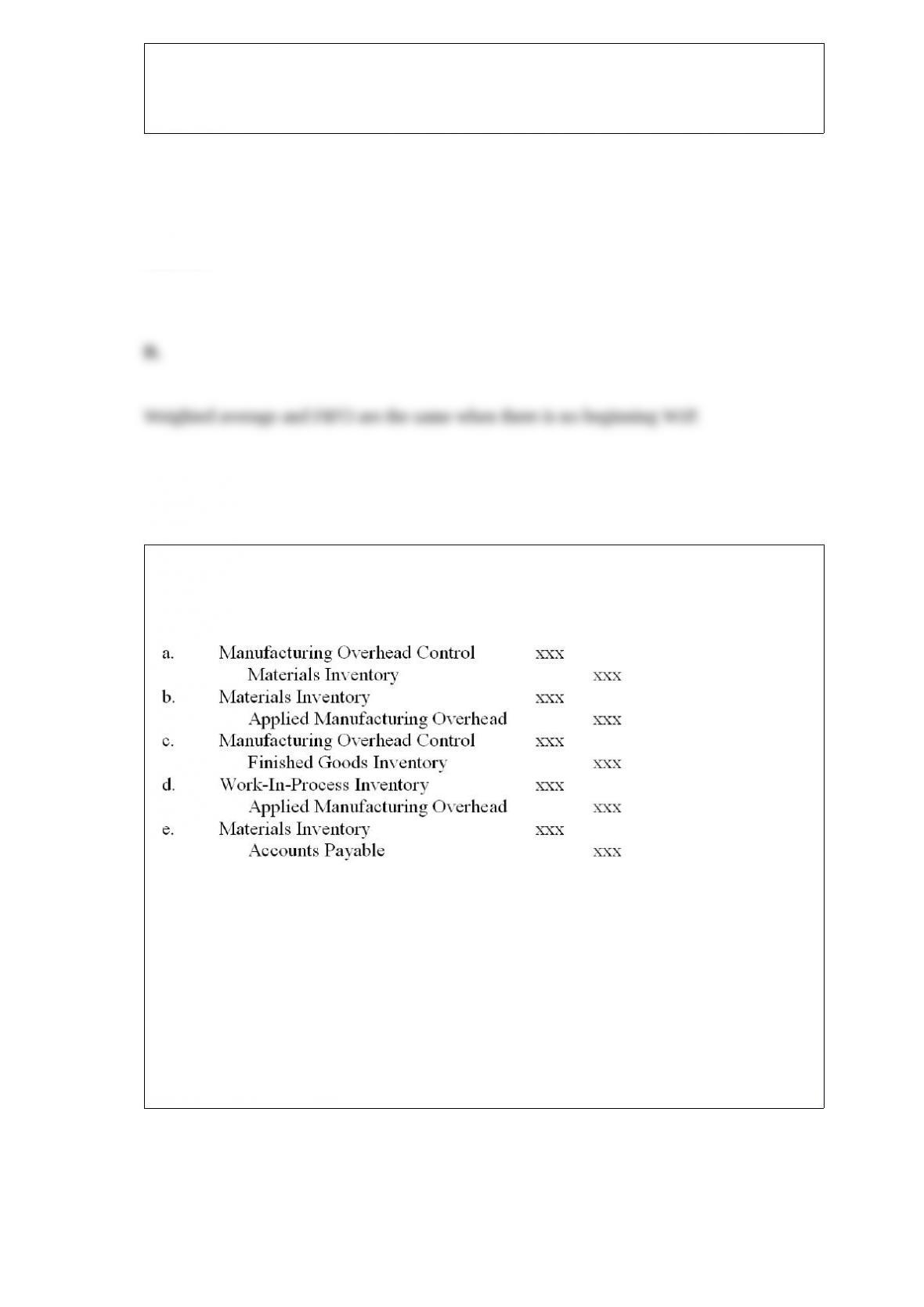

The journal entry to record the actual manufacturing overhead costs for indirect

material is

A. a

B. b

C. c

D. d

E. e

Answer:

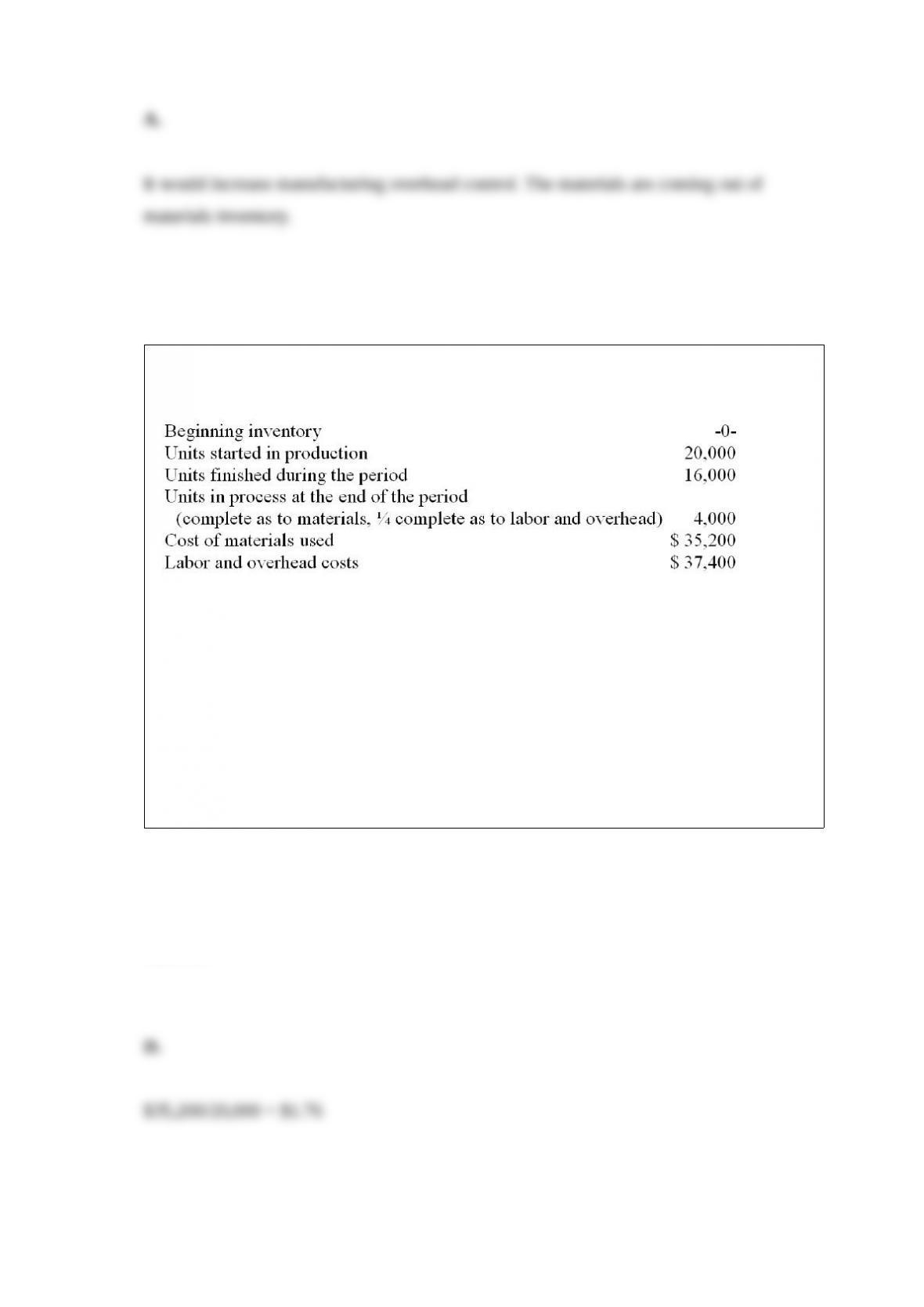

The WISCO Company uses a weighted-average process costing system. The following

data are available:

Unit cost of material is

A. $2.20.

B. $2.07.

C. $1.85.

D. $1.76.

Answer:

Which of the following is not an appropriate use of transfer pricing?

A. product costing

B. decision making

C. establishing standards

D. evaluating performance

Answer:

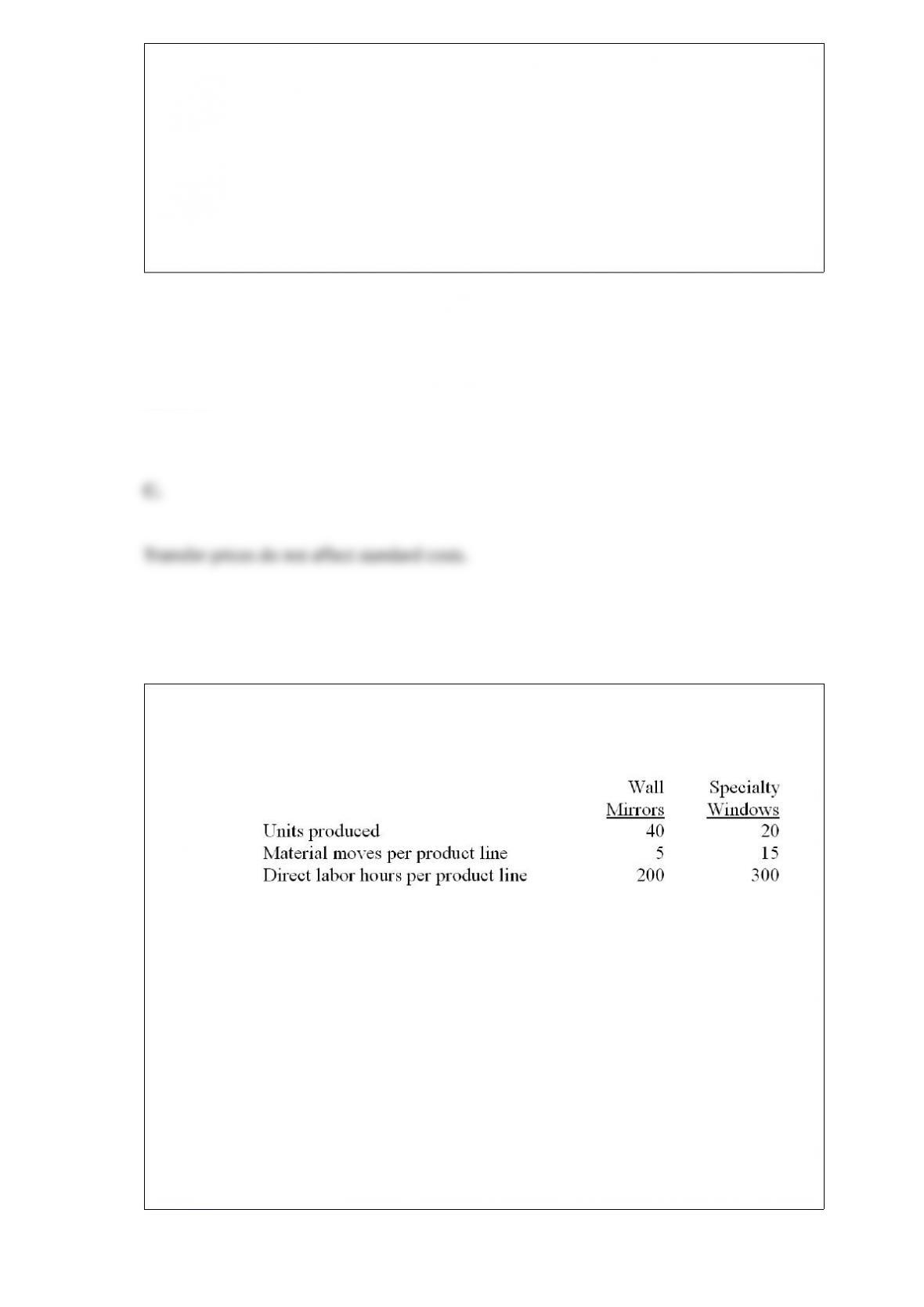

Zela Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Budgeted material handling costs: $50,000

Under an activity-based costing (ABC) system, the materials handling costs allocated to

one unit of wall mirrors would be

A. $625.00

B. $312.50

C. $833.33

D. $1,000.00

Answer: