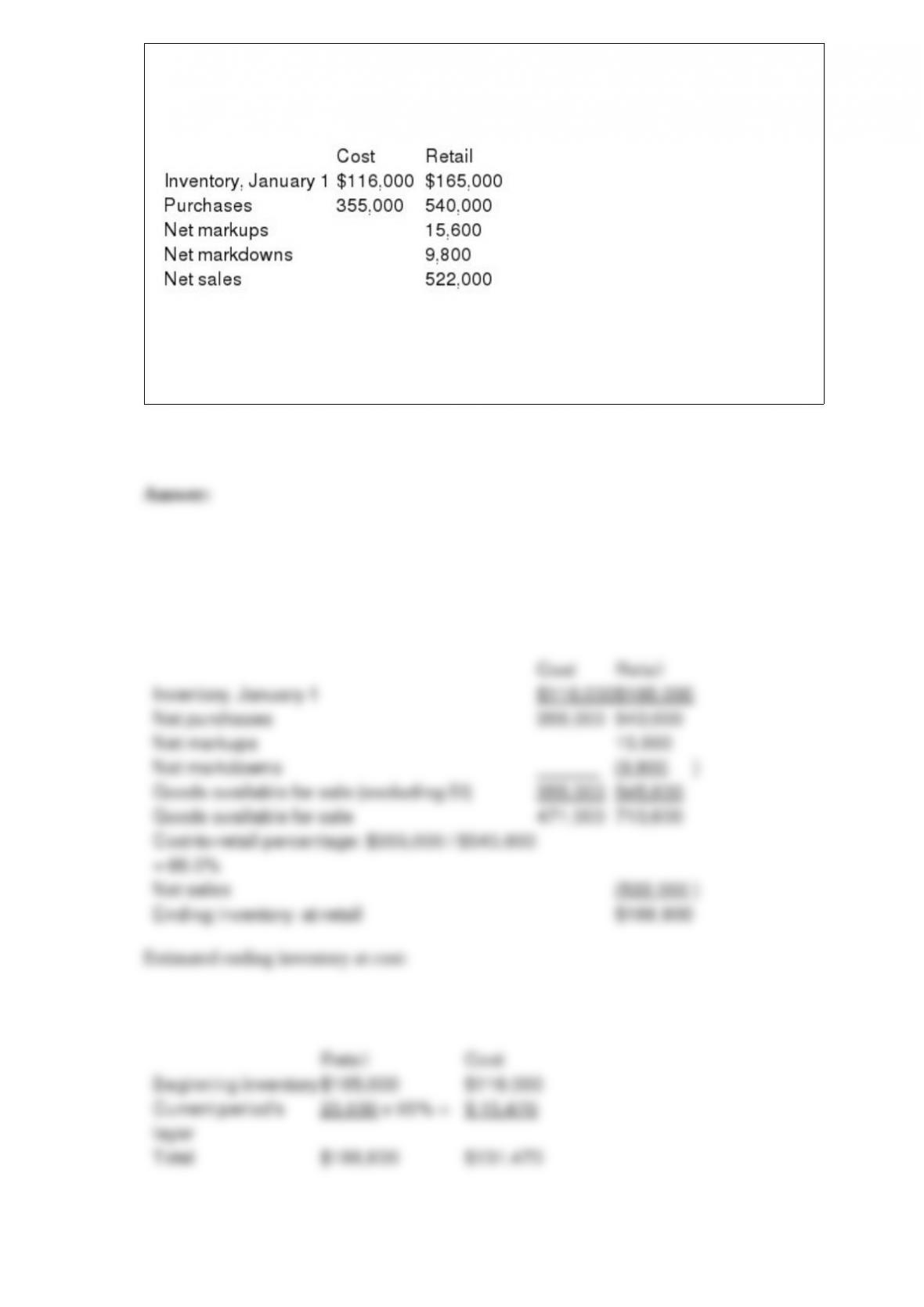

Murdock Industries uses a periodic inventory system and the LIFO retail method to

estimate its ending inventories. The following data has been summarized for December

31, 2016:

Required:

Estimate the LIFO cost of ending inventory. Assume stable retail prices during the

period.

On April 1, 2016, Parks Co. purchased machinery at a cost of $42,000. The machinery

is expected to last 10 years and to have a residual value of $6,000. Required: Compute

depreciation for 2016 and 2017 and the book value of the machinery at December 31,

2016 and 2017, assuming the sum-of-the-years’-digits method is used.

The following note disclosure appeared in a recent annual report of Halliburton: Our

receivables are generally not collateralized. Included in notes and accounts receivable

are notes with varying interest rates totaling $12 million at December 31. At December

31, 39% of our consolidated receivables related to our United States government

contracts, primarily for projects in the Middle East.

Explain the reason that Halliburton indicates that its receivables are generally not

collateralized. What significance does this have to the reader?

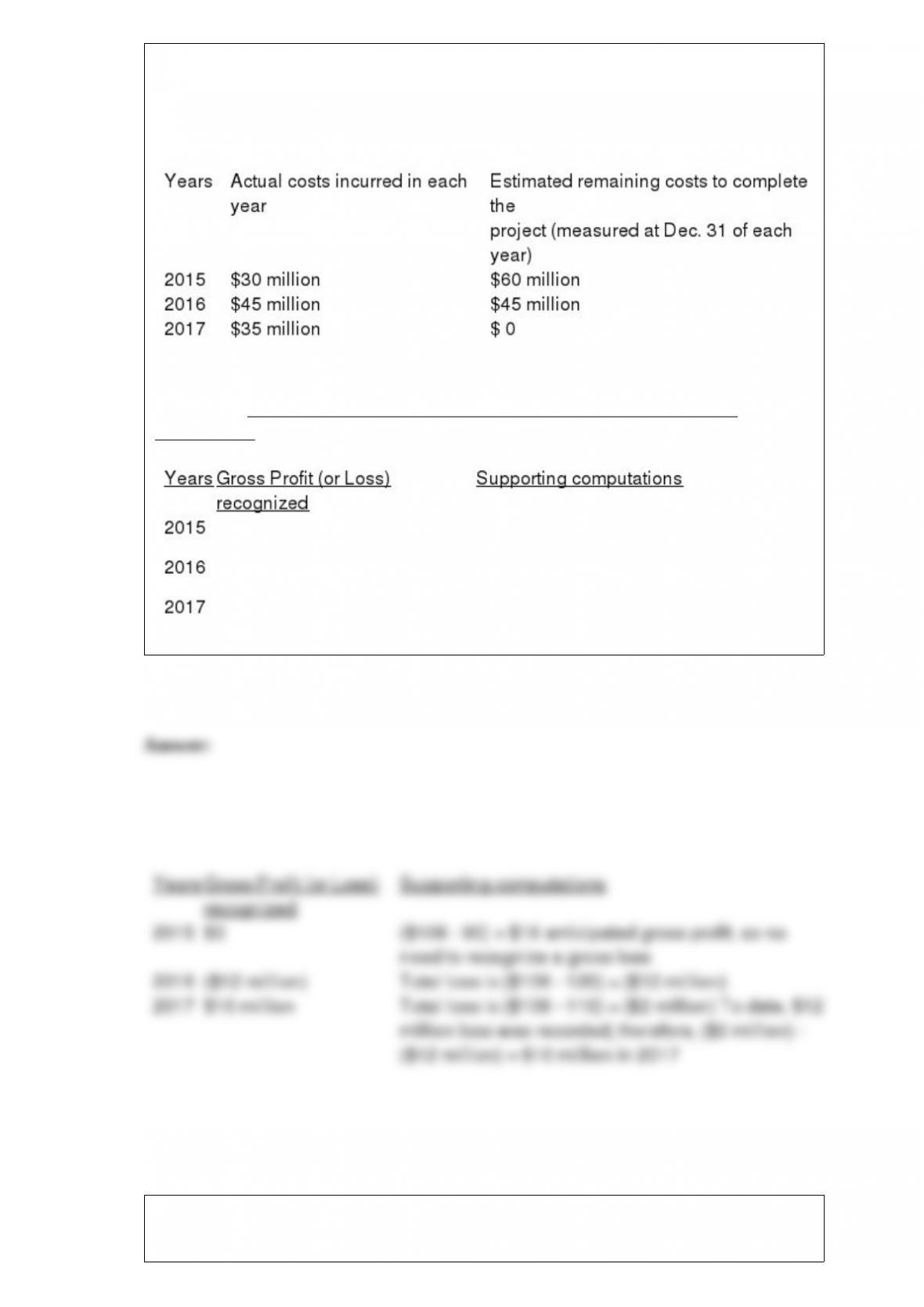

Beck Construction Company began work on a new building project on January 1, 2015.

The project is to be completed by December 31, 2017, for a fixed price of $108 million.

The following are the actual costs incurred and estimates of remaining costs to

complete the project that were made by Beck’s accounting staff:

Required: What amount of gross profit (or loss) would Beck record on this project in

each year, assuming that Beck recognizes revenue for this project upon completion of

the project? Place answers in the spaces provided below and show supporting

computations.

Mattson Company receives royalties on a patent it developed several years ago.

Royalties are 5% of net sales, to be received on September 30 for sales from January

through June and receivable on March 31 for sales from July through December. The

patent rights were distributed on July 1, 2015, and Mattson accrued royalty revenue of

$60,000 on December 31, 2015, as follows:

Mattson received royalties of $65,000 on March 31, 2016, and $80,000 on September

30, 2016. In December, 2016, the patent user indicated to Mattson that sales subject to

royalties for the second half of 2016 should be $800,000.

Required:

1) Prepare any journal entries Mattson should record during 2016 related to the royalty

revenue.

2) What changes should be made to retained earnings relative to these royalties?

On January 1, 2016, Bell Co. issued $10 million of 10-year convertible bonds at 105.

On January 1, 2021, the bonds were converted into common stock with a market value

of $11 million. Upon conversion, Bell would recognize: