A ____ is a document that reflects the revenues and/or costs that are under the control

of a particular manager.

a. quality audit report

b. responsibility report

c. performance evaluation report

d. project report

Actual fixed overhead minus budgeted fixed overhead equals the

a. fixed overhead volume variance.

b. fixed overhead spending variance.

c. noncontrollable variance.

d. controllable variance.

Rosewood Corporation

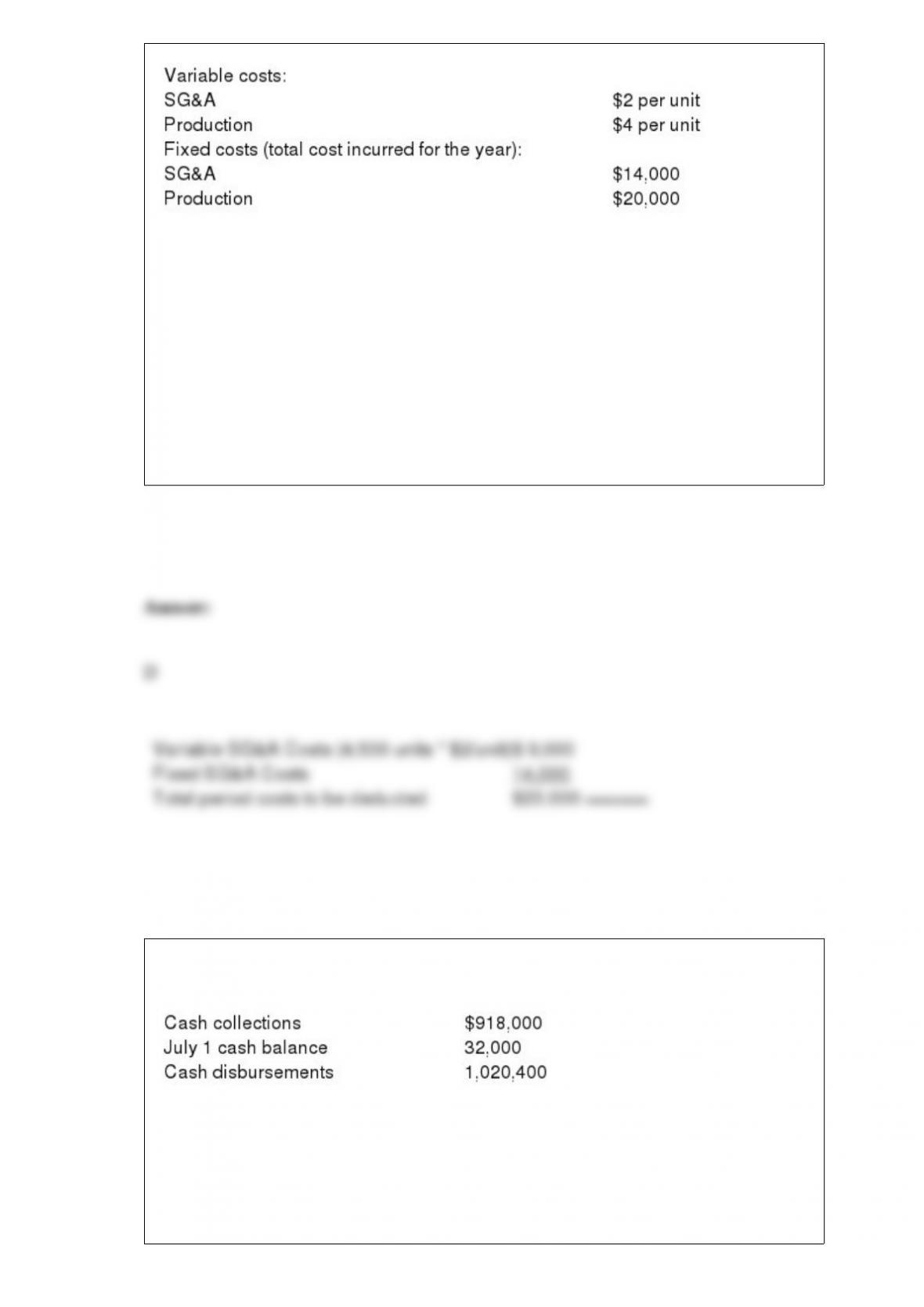

Rosewood Corporation produces a single product. The following cost structure applied

to its first year of operations:

Refer to Rosewood Corporation. Assume for this question only that Rosewood

Corporation produced 5,000 units and sold 4,500 units in the current year. If Rosewood

uses absorption costing, it would deduct period costs of

a. $24,000.

b. $34,000.

c. $27,000.

d. $23,000.

Bentonville Medical Center has provided you with the following budget information for

July:

Bentonville has a policy of maintaining a minimum cash balance of $30,000 and

borrows only in $1,000 increments. How much will Bentonville borrow in July?

a. $ 70,400

b. $ 71,000

c. $100,400

d. $101,000

Diversity applies to differences in

a. race.

b. religion.

c. culture.

d. all of the above.

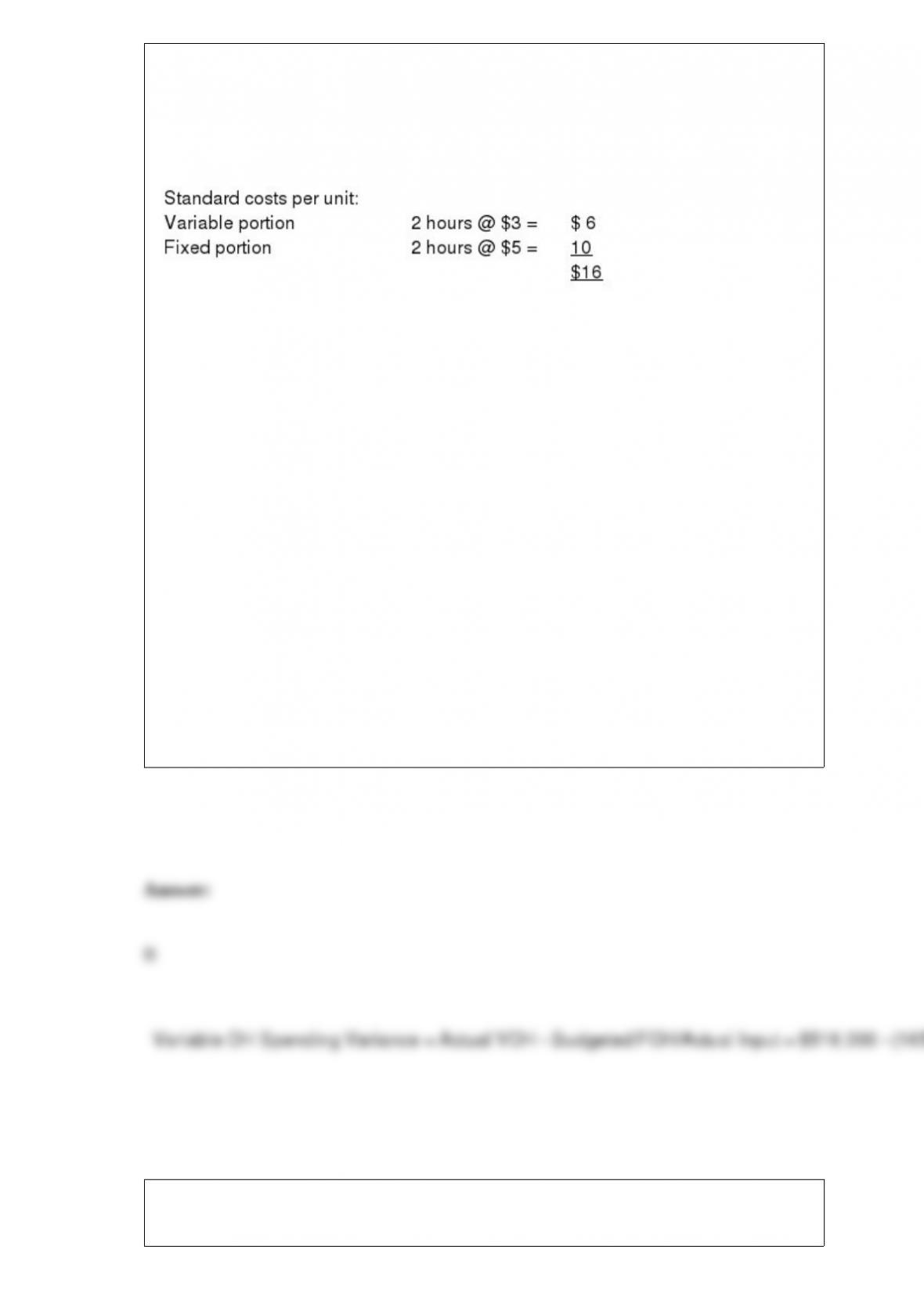

Texas Metal Company

Texas Metal Company has developed standard overhead costs based on a monthly

capacity of 180,000 machine hours as follows:

During November, 90,000 units were scheduled for production, but only 80,000 units

were actually produced. The following data relate to November:

Actual machine hours used were 165,000.

Actual overhead incurred totaled $1,378,000 ($518,000 variable plus $860,000 fixed).

All inventories are carried at standard cost.

Refer to Texas Metal Company. The variable overhead spending variance for November

was

a. $15,000 U.

b. $23,000 U.

c. $38,000 F.

d. $38,000 U.

In a job-order costing system, the use of indirect material would usually be reflected in

the general ledger as an increase in

a. stores control.

b. work in process control.

c. manufacturing overhead applied.

d. manufacturing overhead control.

A significant cost of quality that is not recorded in the accounting records is the

a. failure cost for a customer complaint center.

b. cost of reworking products to bring them up to specification.

c. opportunity costs of forgone future sales.

d. appraisal cost for product equipment.

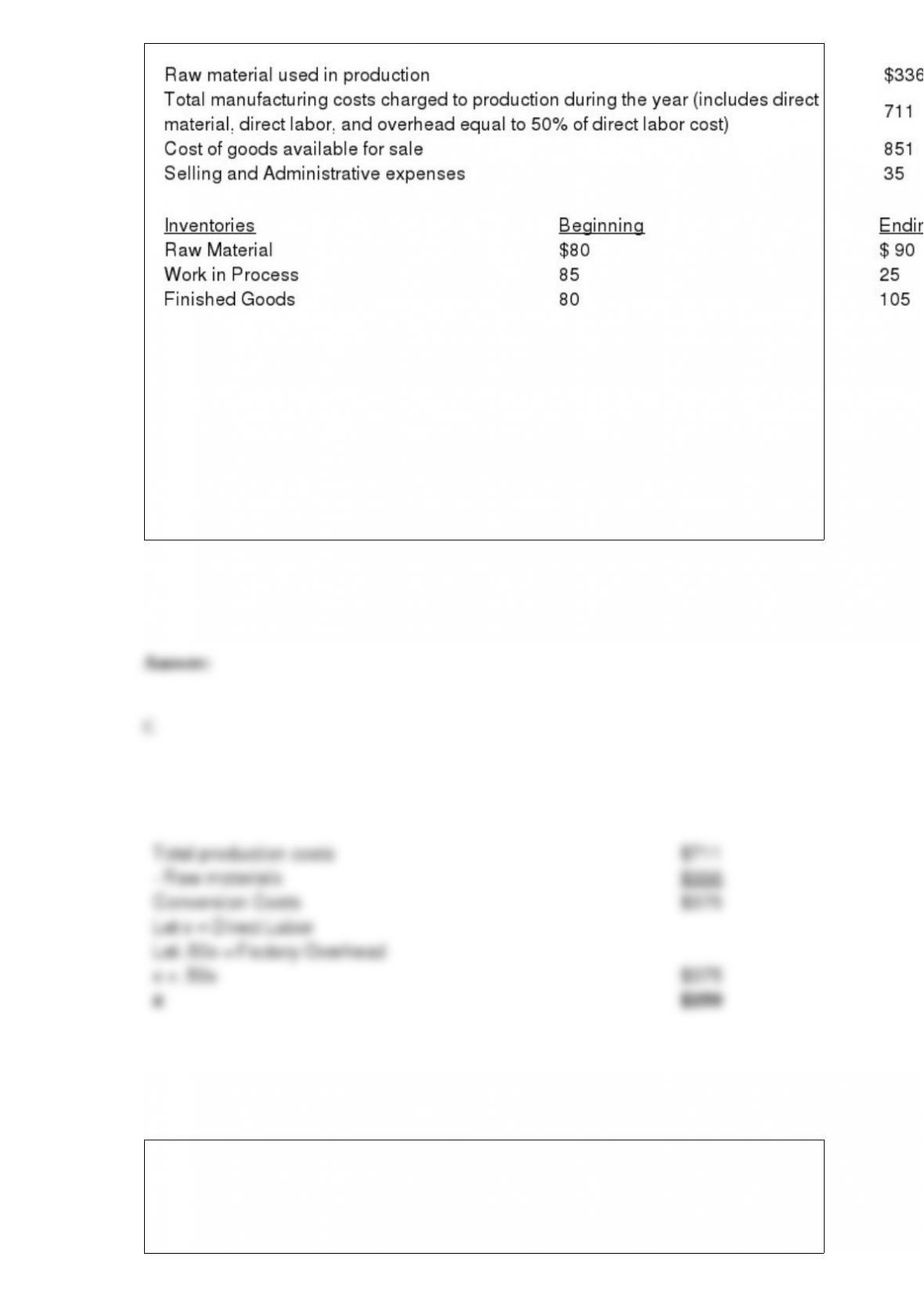

Bridges Corporation

The following information has been taken from the cost records of Bridges Corporation

for the past year:

Refer to Bridges Company. Direct labor cost charged to production during the year was

a. $125

b. $188

c. $250

d. $375.

Refer to Richardson Company. If Richardson Company were using variable costing,

what would it show as the value of ending inventory?

a. $120,000

b. $64,500

c. $27,000

d. $24,000

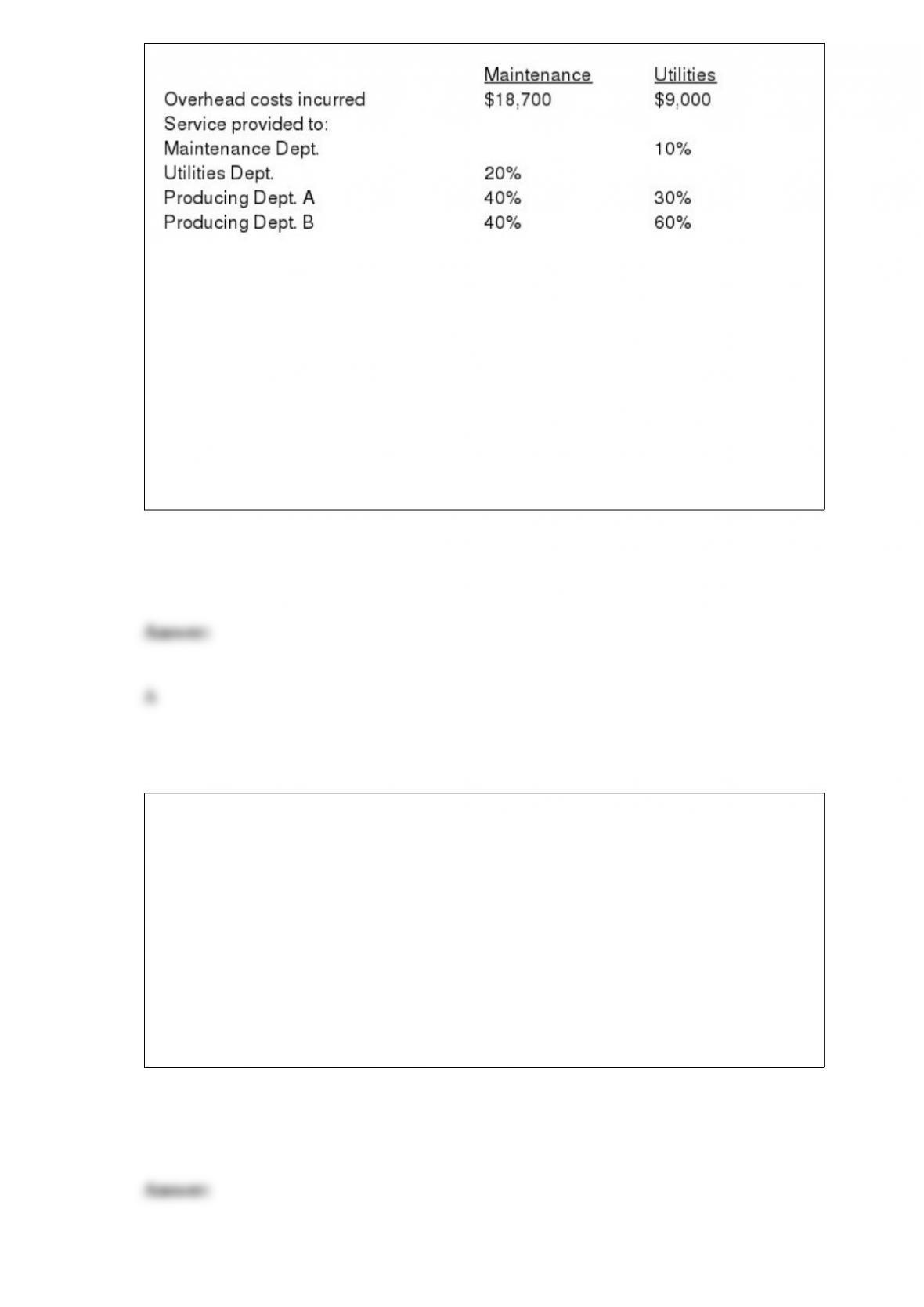

Lincoln Corporation

Lincoln Corporation distributes its service department overhead costs directly to

producing departments without allocation to the other service departments. Information

for January is presented here.

Refer to Lincoln Corporation. Assume that Lincoln Corporation distributes service

department overhead costs based on the algebraic method. What would be the formula

to determine the total maintenance costs?

a. M = $18,700 + .10U

b. M = $9,000 + .20U

c. M = $18,700 + .30U + .40A + .40B

d. M = $27,700 + .40A + .40B

Parker Company manufactures tables. If raw material used was $80,000 and Raw

Material Inventory at the beginning and end of the period, respectively, was $17,000

and $21,000, what was amount of raw material was purchased?

a. $76,000

b. $118,000

c. $84,000

d. $101,000

Performance measurements and a reward system are part of which cost management

element?

a. motivational

b. informational

c. reporting

d. all of the above

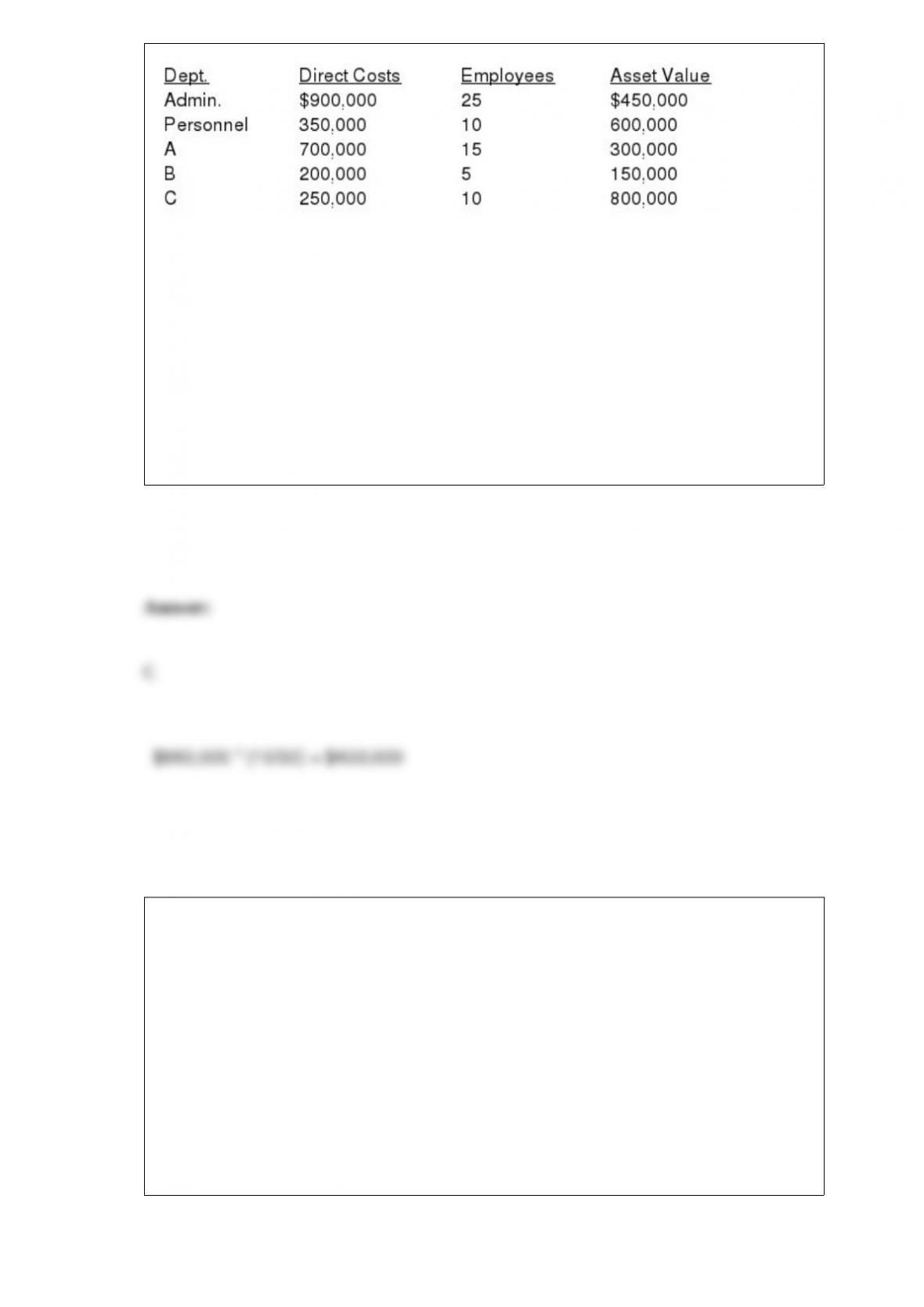

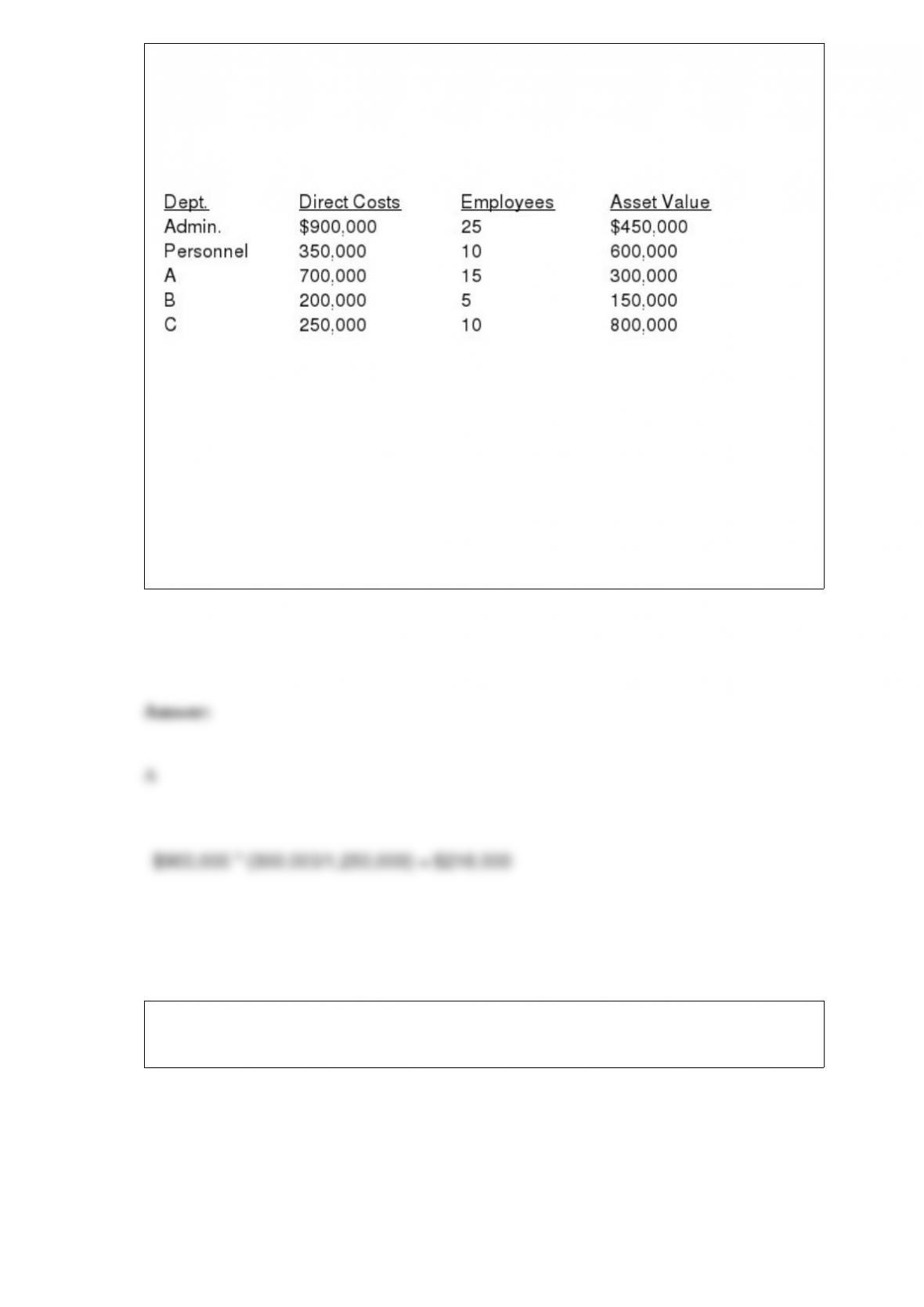

Bradley Corporation

Bradley Corporation has three production departments A, B, and C. Bradley

Corporation also has two service departments, Administration and Personnel.

Administration costs are allocated based on value of assets employed, and Personnel

costs are allocated based on number of employees. Assume that Administration

provides more service to the other departments than does the Personnel Department.

Refer to Bradley Corporation. Assume that Administration costs have been allocated

and the balance in Personnel is $860,000. What amount is allocated to A (round to the

nearest dollar)?

a. $213,964

b. $106,982

c. $430,000

d. $0

A company annually consumes 10,000 units of Part C. The carrying cost of this part is

$2 per year and the ordering costs are $100. The company uses an order quantity of 500

units. If the company operates 200 days per year, and the lead time for ordering Part C

is 5 days, what is the order point?

a. 250 units

b. 1,000 units

c. 500 units

d. 2,000 units

The Institute of Management Accountants’ Code of Ethics

a. is a legally enforceable contract with all management accountants.

b. should be viewed as a goal for professional behavior.

c. is a legally enforceable contract with all CPAs.

d. provides ways to measure departures from ethical behavior.

Which of the following would be an appropriate alternative to the use of ROI in

evaluating the performance of an investment center?

a. yes yes

yes

b. no yes

no

c. yes no

no

d. yes no

yes

A transfer pricing system is also known as

a. investment center accounting.

b. a revenue allocation system.

c. responsibility accounting.

d. a charge-back system.

Kaizen costing helps to

a. reduce product costs of products in the design and development stage.

b. keep the target cost as the primary focus after a product enters production.

c. keep profit margin relatively stable as product price declines over the product life

cycle.

d. reduce the cost of engineering change orders during each stage of the product life

cycle.

The method of budgeting that adds one month’s budget to the end of the plan when the

current month’s budget is dropped from the plan is called ____ budgeting.

a. long-term

b. operations

c. incremental

d. continuous

Total manufacturing costs for the year plus beginning Work in Process Inventory cost

equals

a. cost of goods manufactured in the year.

b. ending Work in Process Inventory.

c. total manufacturing costs to account for.

d. cost of goods available for sale.

CVP analysis relies on the assumptions that costs are either strictly fixed or strictly

variable. Consistent with these assumptions, as volume decreases total

a. fixed costs decrease.

b. variable costs remain constant.

c. costs decrease.

d. costs remain constant.

Industrial Solutions Company

Industrial Solutions Company produces three products from the same process that has

joint processing costs of $4,100. Products R, S, and T are produced in the following

quantities: 250 gallons, 400 gallons, and 750 gallons. Industrial Solutions Company

also incurred advertising costs of $60,000. The ad was used to run sales for all three

products. The three products occupy floor space in the following ratio: 5:4:9. (Round all

answers to the nearest dollar.)

Refer to Industrial Solutions Company. Assume that Industrial Solutions chooses to

allocate its advertising cost among the three products. What amount of advertising cost

is allocated to Product R using the floor space ratio?

a. $30,000

b. $17,806

c. $1,139

d. $16,667

Bradley Corporation

Bradley Corporation has three production departments A, B, and C. Bradley

Corporation also has two service departments, Administration and Personnel.

Administration costs are allocated based on value of assets employed, and Personnel

costs are allocated based on number of employees. Assume that Administration

provides more service to the other departments than does the Personnel Department.

Refer to Bradley Corporation. Using the direct method, what amount of Administration

costs is allocated to A (round to the nearest dollar)?

a. $216,000

b. $150,000

c. $288,000

d. $54,000

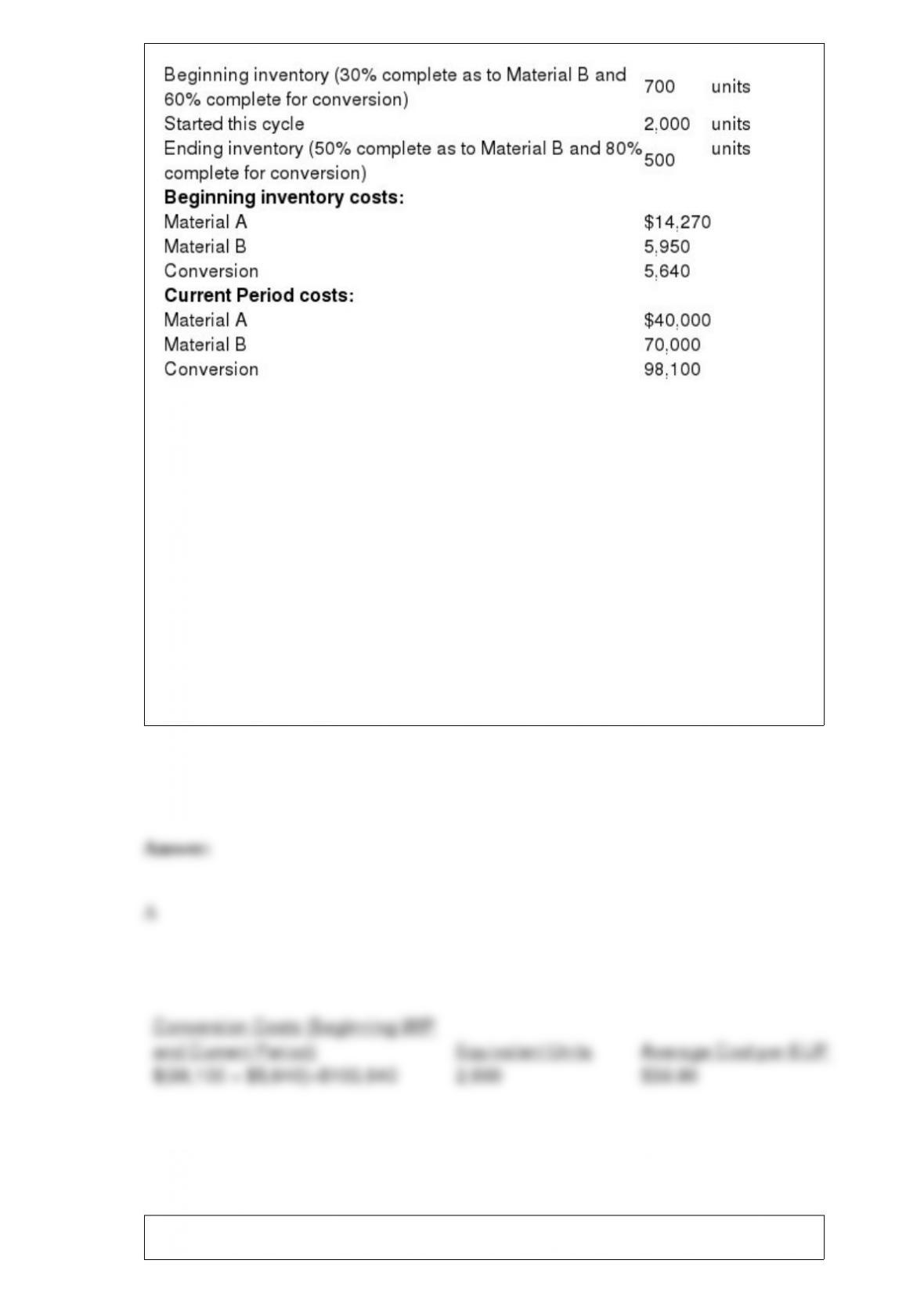

Saturn Corporation

Material A is added at the start of production, while Material B is added uniformly

throughout the process.

Refer to Saturn Corporation Assuming a weighted average method of process costing,

compute the average cost per EUP for conversion.

a. $39.90

b. $45.00

c. $43.03

d. $47.59

Core competencies are not

a. internal functions crucial to the success and survival of a company.

b. attributes that keep a firm from competing.

c. different for every organization.

d. considered influences on corporate strategies.

Abnormal spoilage is

a. spoilage that is forecasted or planned.

b. spoilage that is in excess of planned.

c. accounted for as a product cost.

d. debited to Cost of Goods Sold.

The weighted average method is thought by some accountants to be inferior to the FIFO

method because it

a. is more difficult to apply.

b. only considers the last units worked on.

c. ignores work performed in subsequent periods.

d. commingles costs of two periods.

Superior Armored Car Co. is considering the acquisition of a new armored truck. The

truck is expected to cost $300,000. The company’s discount rate is 12 percent. The firm

has determined that the truck generates a positive net present value of $17,022.

However, the firm is uncertain as to whether it has determined a reasonable estimate of

the salvage value of the truck. In computing the net present value, the company

assumed that the truck would be salvaged at the end of the fifth year for $60,000. What

expected salvage value for the truck would cause the investment to generate a net

present value of $0? Ignore taxes. Present value tables or a financial calculator are

required.

a. $30,000

b. $0

c. $55,278

d. $42,978

Chronologically, the last part of the master budget to be prepared would be the

a. pro forma financial statements.

b. cash budget.

c. capital budget

d. production budget.

When multiple labor categories are used, the monetary impact of using a higher or

lower number of hours than a standard allows is referred to as a labor yield variance.

If revenues are intentionally underestimatedduring the budgeting process,

______________________________ has been created.

What distinct advantage does a return on investment measure have over a residual

income measure? Explain.

A(n) _________________________ measures the resources consumed by a

manufacturing process.

A standard cost card is prepared after manufacturing standards have been developed for

direct materials, direct labor, and factory overhead.

The effect of substituting a non-standard mix of materials during the production process

is referred to as a material mix variance.

Negotiated transfer prices are most appropriate for customized high-volume and

high-cost services.

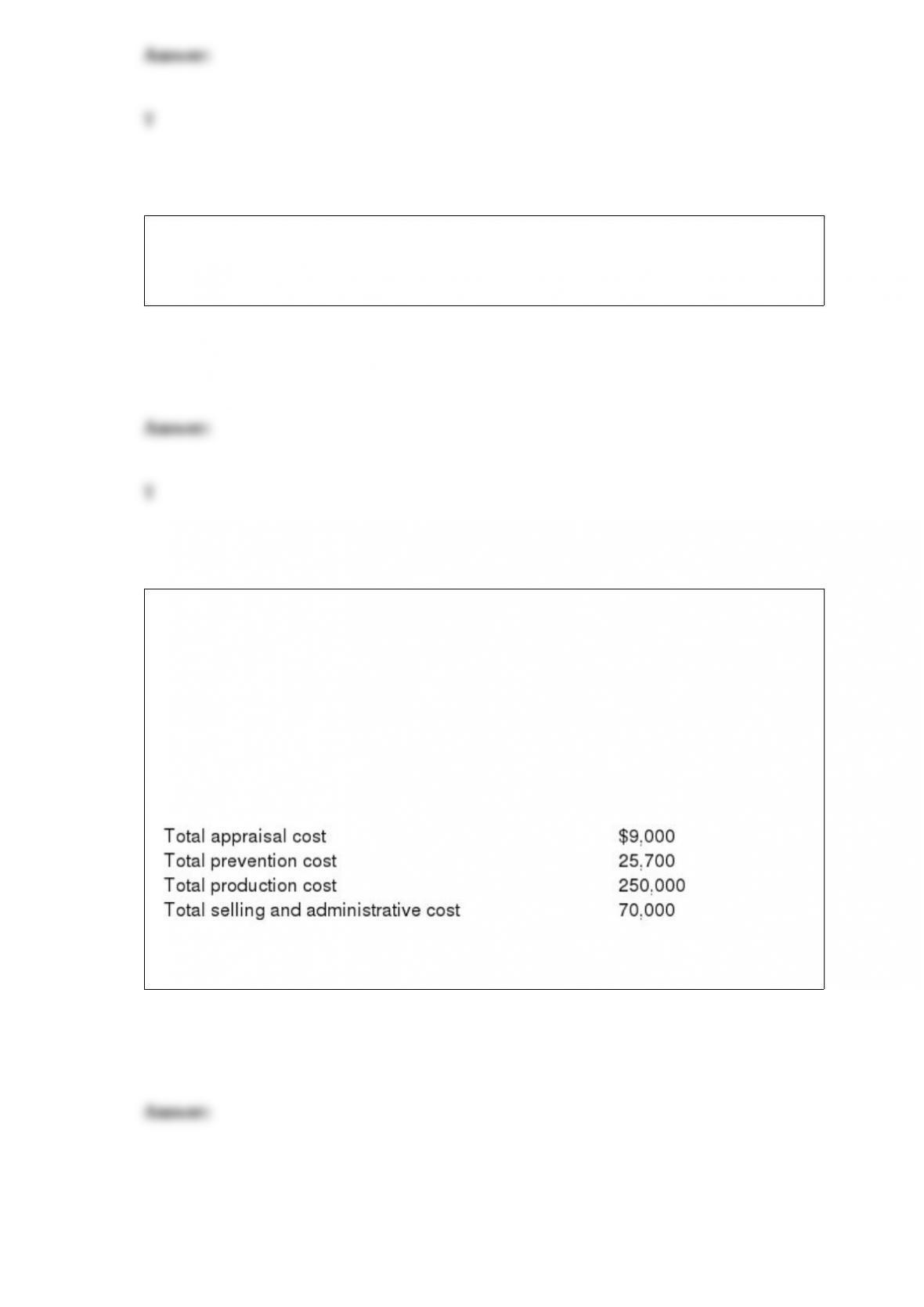

Outdoor Oasis, Inc.

Outdoor Oasis, Inc. has just finished its first year of business. Outdoor Oasis, Inc.

makes decorative outdoor furniture. The firm manufactured 2,500 pieces of furniture

during the year: 2,400 were sold at garden centers for $456,000; 100 pieces were

defective and could only be sold as scrap metal (25 pounds each and can be sold for

$2.50 per pound). No defective units could be reworked. During the year the following

costs were incurred:

Refer to Outdoor Oasis, Inc. Compute the total quality cost incurred by the company

during the first year of operations.

Identify and discuss how sales and costs are affected during the five stages of the

product life cycle.

Pareto analysis is frequently used to aid management in deciding where to concentrate

quality prevention cost dollars.

Costs of normal shrinkage and normal continuous losses in a process costing

environment are handled by the method of accretion.

Phantom profits result when absorption costing is used and sales exceed production.

What is data mining and how is it used?

Total units produced during the period divided by the value-added processing time is

referred to as ______________________________.

An operations flow document shows all processes necessary to manufacture one unit of

a product.

A ratio comparing the present value of a project’s net cash inflows to the project’s net

investment is referred to as the ____________________________________.

Financial accounting is most concerned with meeting the needs of external users.

Why do managers frequently prefer variable costing to absorption costing for internal

use?

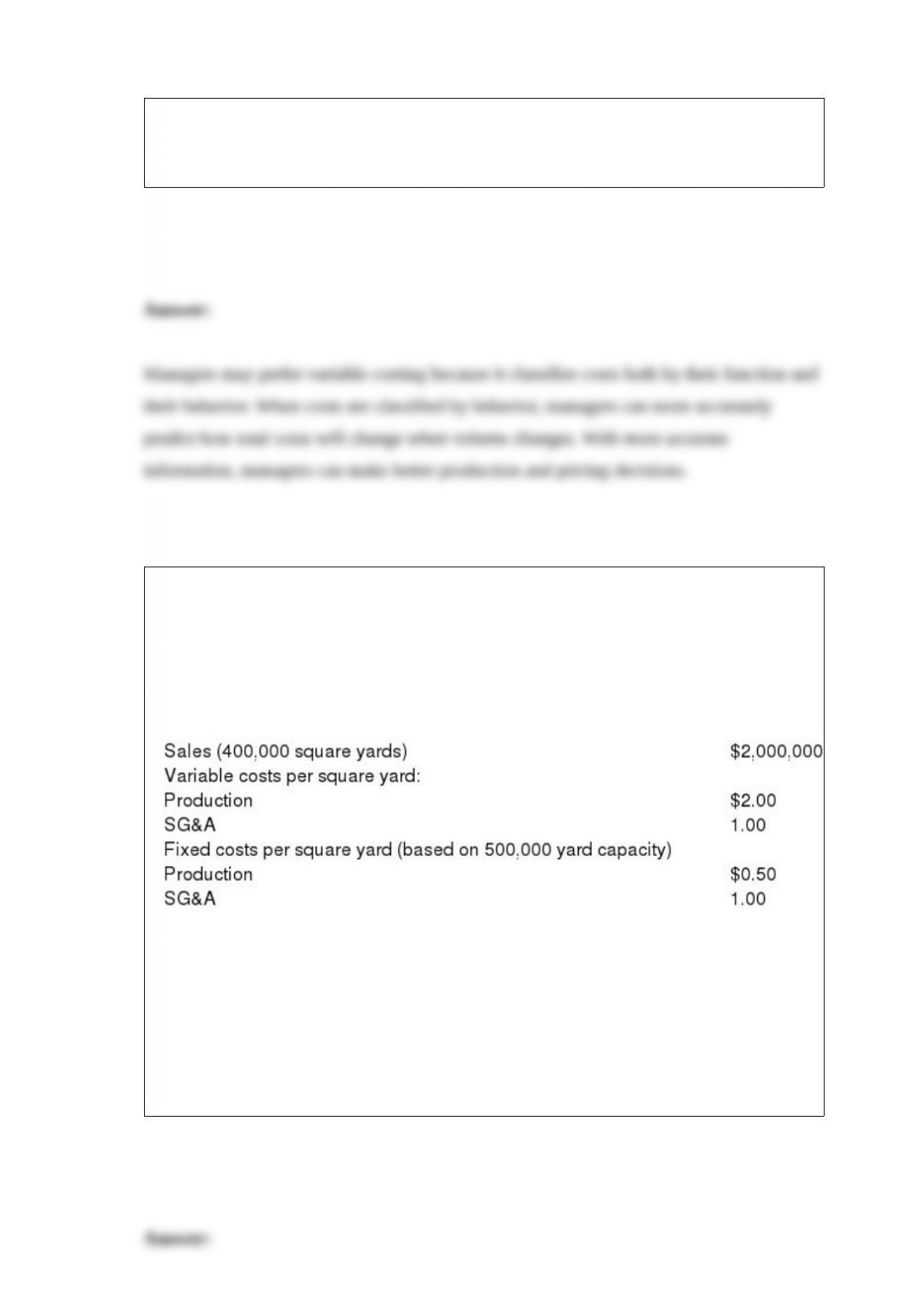

Castle Homes Corporation

The Carpet Division of Castle Homes Corporation manufactures a single grade of

residential grade carpeting. The division has the capacity to produce 500,000 square

yards of carpet each year. Its current costs and revenues are shown here:

The Housing Division currently purchases 40,000 yards of carpeting (of the grade

produced by the Carpet Division) each year at a cost of $6.50 per square yard from an

outside vendor.

Refer to Castle Homes Corporation. If the Housing and Carpet Divisions agree on the

internal transfer of 40,000 square yards of carpet at a price of $4.00 per square yard,

how will overall corporate profits be affected?