1) A direct materials quantity standard generally includes an allowance for waste.

2) The costs assigned to units in inventory are typically lower under variable costing

than under absorption costing.

3) Suppose a company evaluates divisional performance using both ROI and residual

income. The company’s minimum required rate of return for the purposes of residual

income calculations is 12%. If a division has a residual income of $6,000, then its ROI

is greater than 12%.

4) The net cash provided by operating activities on the statement of cash flows does not

include any dividends paid to the company’s own shareholders.

5) Direct material costs are generally fixed costs.

6) Comparing a static planning budget to actual costs is a good way to assess whether

variable costs are under control.

7) All other things being the same, a decrease in average operating assets will decrease

return on investment (ROI).

8) To increase total asset turnover, management must either increase sales or reduce

total stockholders’ equity.

9) When fixed costs are included in the cost of goods sold, the gross margin percentage

should increase and decrease with sales volume.

10) Costs are accumulated by department in a process costing system.

11) An increase in appraisal costs will usually result in a decrease in internal failure

costs.

12) Relative profitability should be measured by dividing a segment’s market share by

its revenues.

13) The formula for the times interest earned ratio is: Times interest earned = Earnings

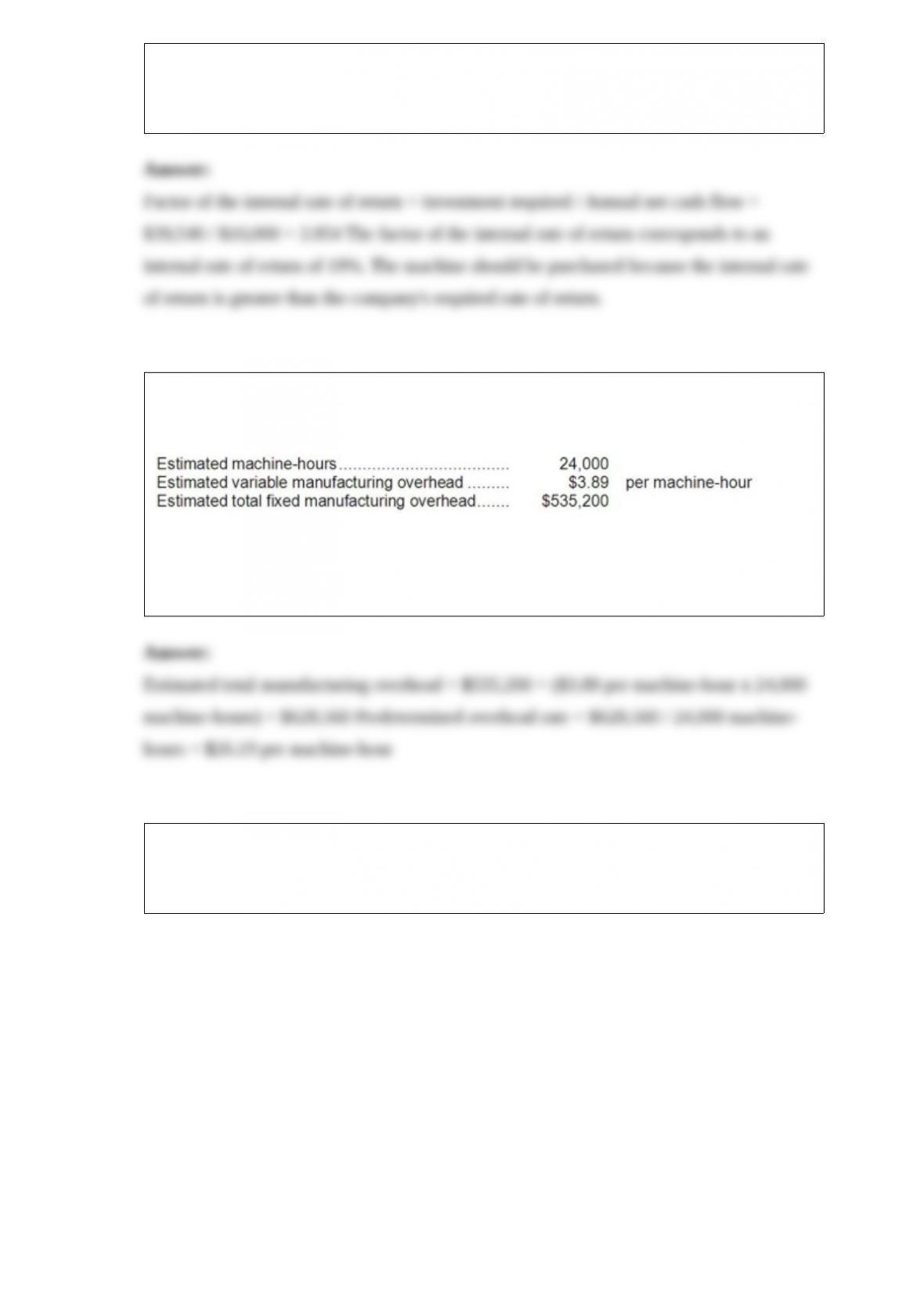

before interest expense and income taxes Interest expense.

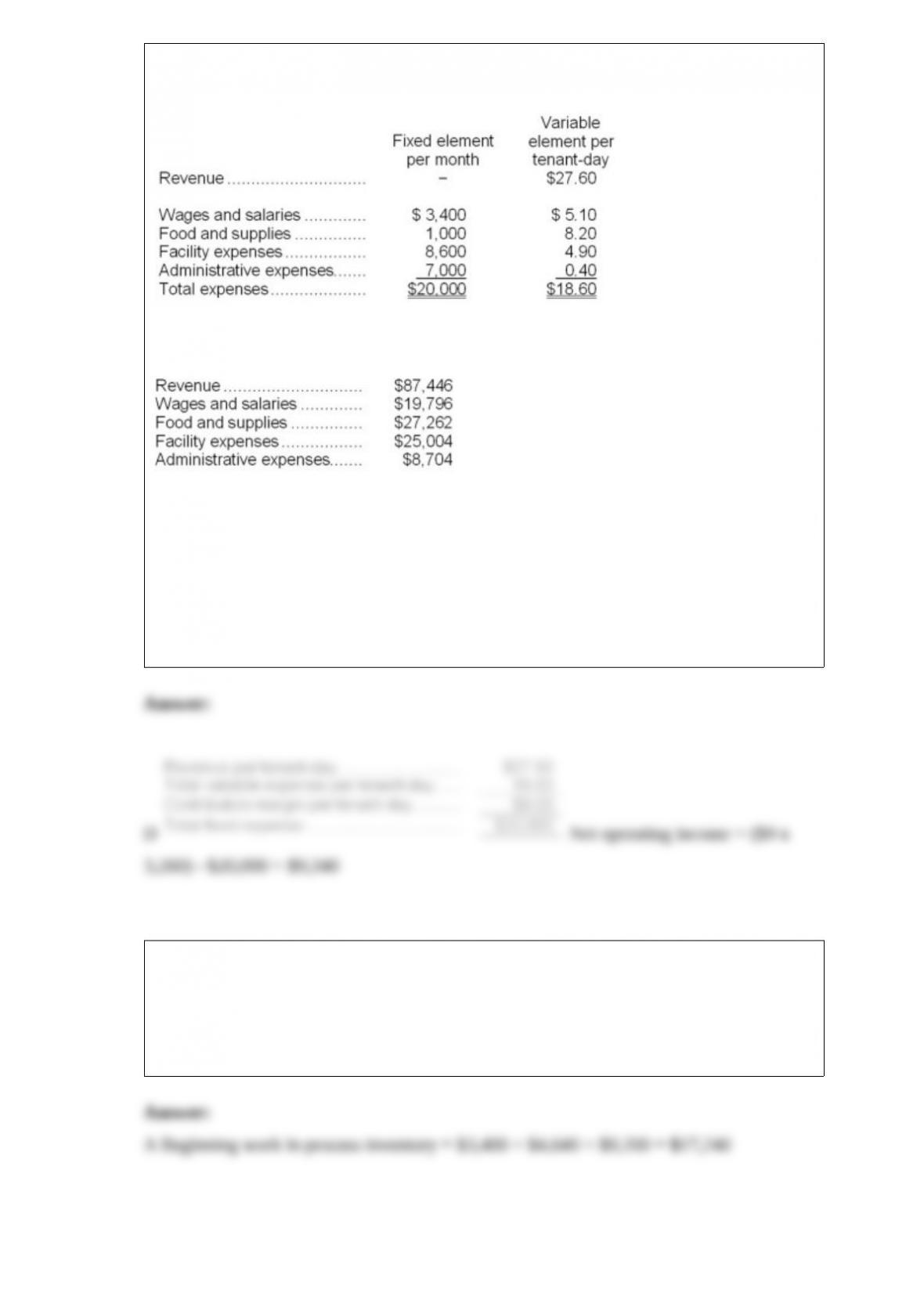

14) Zenon Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During July, the kennel budgeted for

3,300 tenant-days, but its actual level of activity was 3,260 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Actual results for July:

The net operating income in the flexible budget for July would be closest to:

A.$9,700

B.$6,599

C.$6,762

D.$9,340

15) The cost of goods manufactured for May was:

A.$109,670

B.$124,620

C.$143,300

D.$126,820

16) At an activity level of 6,900 units in a month, Zelinski Corporations total variable

maintenance and repair cost is $408,756 and its total fixed maintenance and repair cost

is $230,253. What would be the total maintenance and repair cost, both fixed and

variable, at an activity level of 7,100 units in a month? Assume that this level of activity

is within the relevant range.

A) $648,270

B) $639,009

C) $650,857

D) $657,531

17) The net cash provided by (used in) investing activities for the year was:

A.$(81)

B.$(66)

C.$66

D.$15

18) Which product makes the LEAST profitable use of the grinding machines?

A) Product A

B) Product B

C) Product C

D) Product D

19) Using the high-low method, the estimate of the fixed component of electrical cost

per month is closest to:

A) $7,371

B) $5,731

C) $5,875

D) $5,840

20) If the company bases its predetermined overhead rate on the estimated amount of

the allocation base for the upcoming year, by how much was manufacturing overhead

underapplied or overapplied?

The management of Aamot Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller

has provided an example to illustrate how this new system would work. In this

example, the allocation base is machine-hours and the estimated amount of the

allocation base for the upcoming year is 43,000 machine-hours. In addition, capacity is

47,000 machine-hours and the actual level of activity for the year is 42,100

machine-hours. All of the manufacturing overhead is fixed and is $828,610 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year.

A.$17,343 Overapplied

B.$86,387 Underapplied

C.$86,387 Overapplied

D.$17,343 Underapplied

21) ( Mercer Corporation is considering replacing a technologically obsolete machine

with a new state-of-the-art numerically controlled machine. The new machine would

cost $250,000 and would have a ten-year useful life. Unfortunately, the new machine

would have no salvage value. The new machine would cost $12,000 per year to operate

and maintain, but would save $55,000 per year in labor and other costs. The old

machine can be sold now for scrap for $10,000. The simple rate of return on the new

machine is closest to:

A.17.9%

B.7.5%

C.22.0%

D.7.2%

22) The following information relates to Marter Manufacturing Corporation for next

quarter:

How many units should the company plan on producing for the month of February?

A.360,000 units

B.362,000 units

C.358,000 units

D.398,000 units

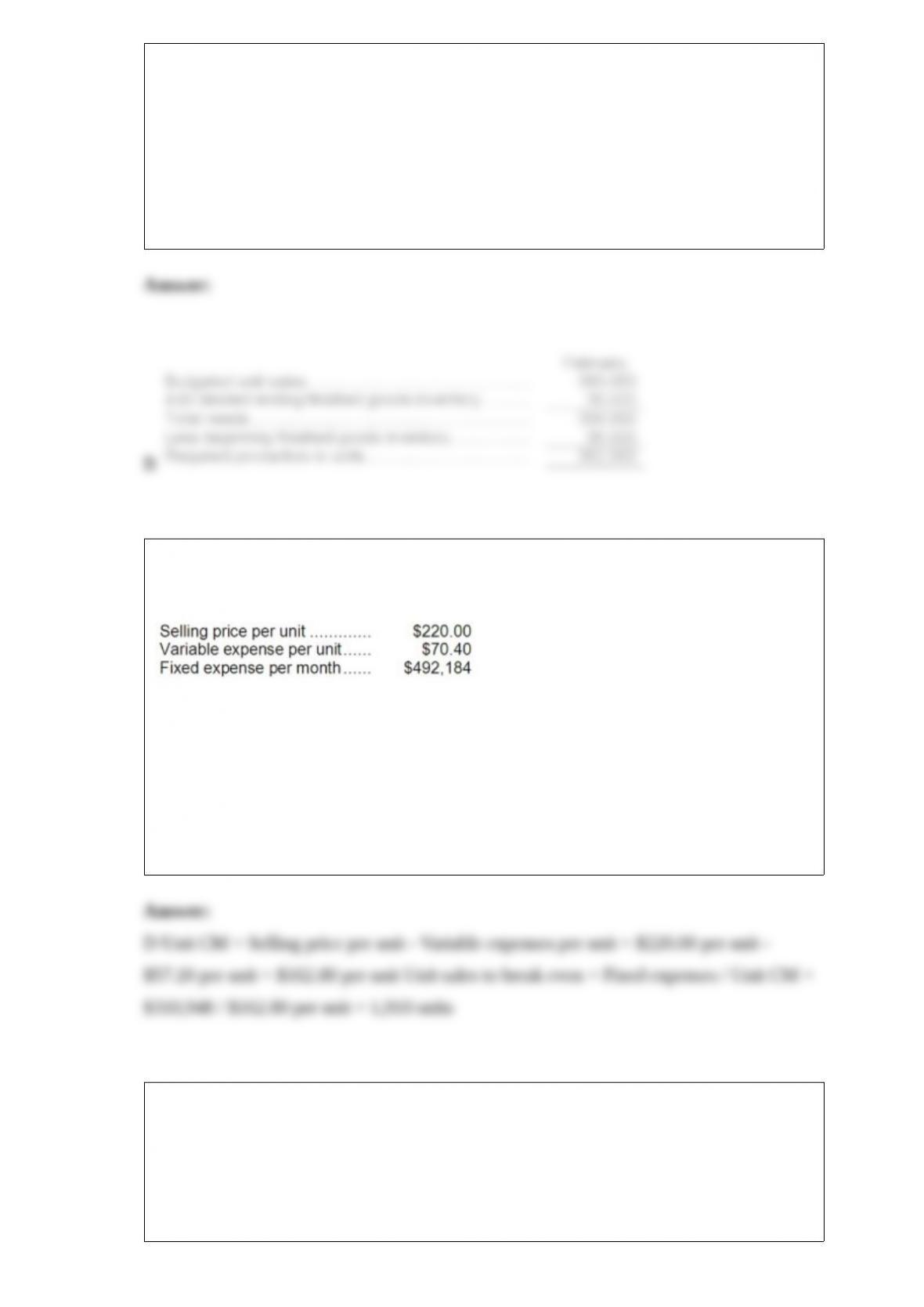

23) Blackner Corporation produces and sells a single product. Data concerning that

product appear below:

The break-even in monthly unit sales is closest to:

A.1,413 units

B.2,920 units

C.5,436 units

D.1,910 units

24) ( Allen Corporation’s required rate of return is 14%. The company is considering the

purchase of a new machine that will save $10,000 per year in cash operating costs. The

machine will cost $39,540 and will have an 8-year useful life with zero salvage value.

Straight-line depreciation will be used.

Required:

Compute the machine’s internal rate of return. Would you recommend purchase of the

machine? Explain.

25) Huckeby Corporation bases its predetermined overhead rate on the estimated

machine-hours for the upcoming year. Data for the upcoming year appear below:

Required:

Compute the company’s predetermined overhead rate.

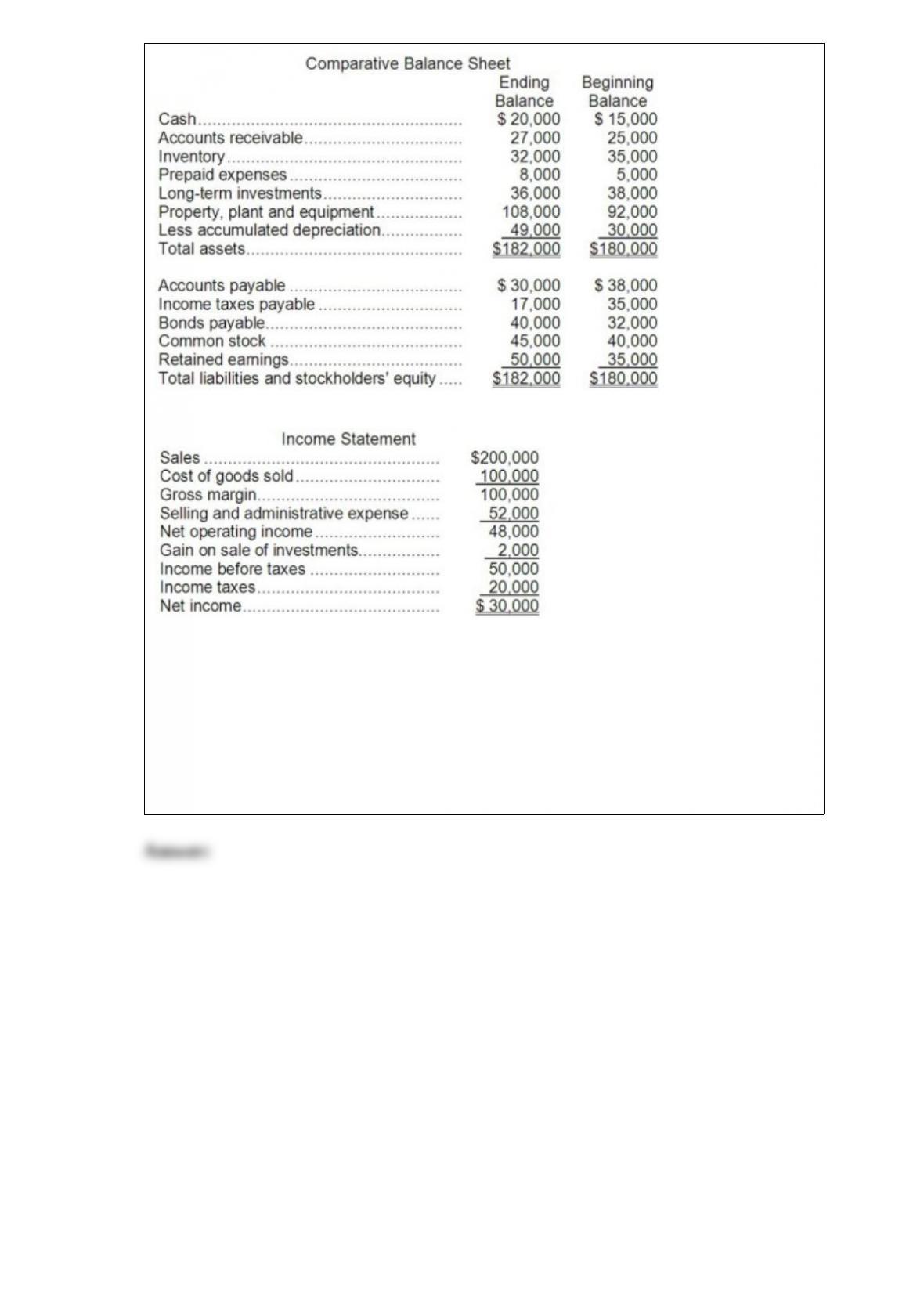

26) Carson Corporation’s comparative balance sheet and income statement for last year

appear below:

Carson did not dispose of any property, plant, and equipment during the year. It

constructs its statement of cash flows using the direct method.

Required:

Using the direct method, prepare in good form the operating activities section of the

statement of cash flows.

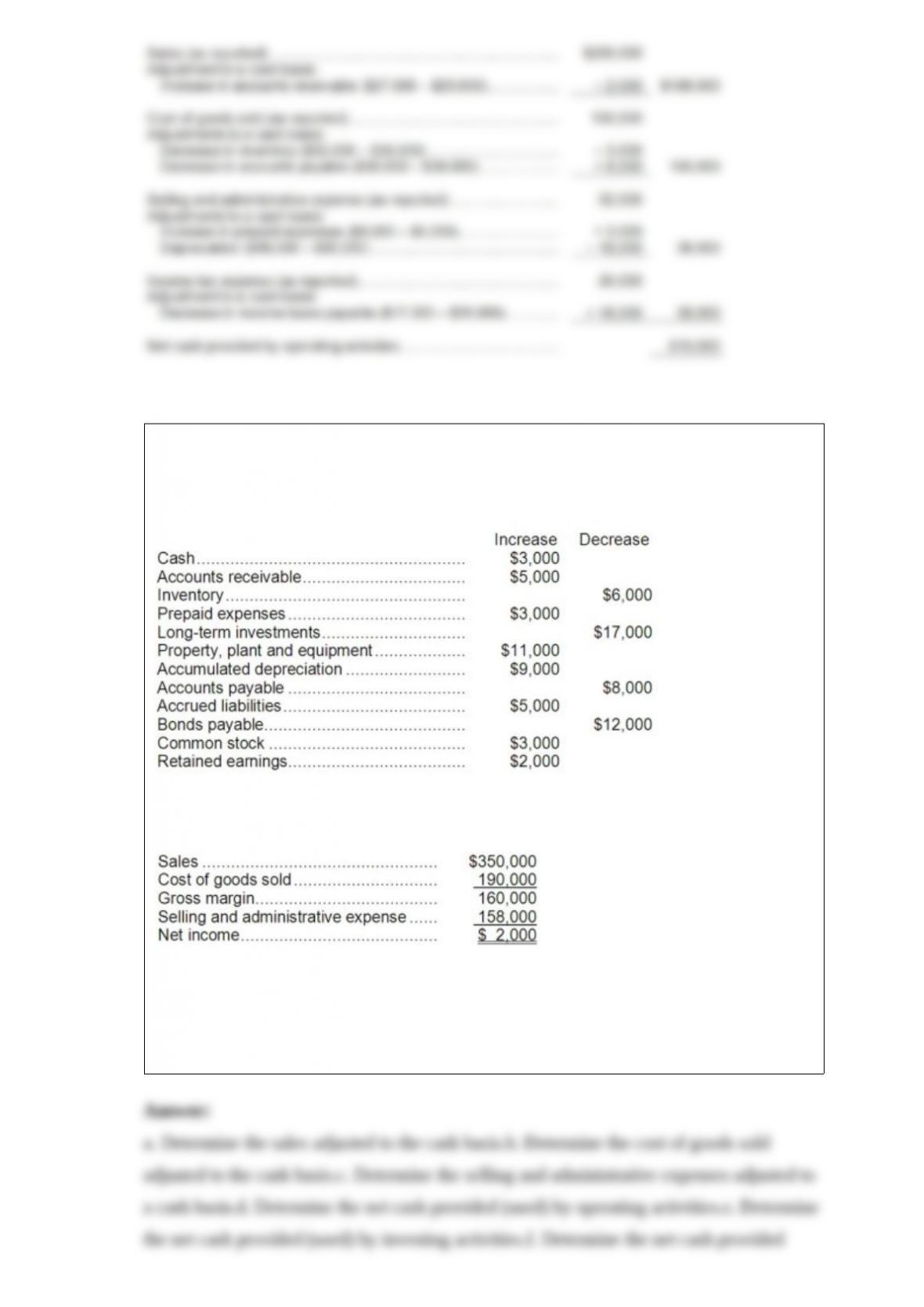

27) The changes in each balance sheet account for Carver Corporation during the year

just completed are as follows:

Carver Corporation’s income statement for the year just ended shows the following:

The company did not dispose of any property, plant, and equipment, buy any long-term

investments, issue any bonds payable, or repurchase any of its own common stock

during the year. Carver Corporation uses the direct method to construct its statement of

cash flows.

28) In December, one of the processing departments at Weisz Corporation had

beginning work in process inventory of $20,000 and ending work in process inventory

of $14,000. During the month, the cost of units transferred out from the department was

$244,000.

Required:

Construct a cost reconciliation report for the department for the month of December.

29) In February, one of the processing departments at Mateus Corporation had

beginning work in process inventory of $20,000 and ending work in process inventory

of $30,000. During the month, $206,000 of costs were added to production and the cost

of units transferred out from the department was $196,000. The company uses the FIFO

method in its process costing system.

Required:

Construct a cost reconciliation report for the department for the month of February.